sommart

sommart

Synovus Financial Corp. (NYSE:SNV), founded in 1888 and headquartered in Columbus, Georgia, is a leading provider of commercial and consumer banking services primarily operating in Alabama, Florida, Georgia, South Carolina, and Tennessee.

The common stock's dividend profile is attractive after taking into account the company's profitability, solvency profile, and stock price. If you're mainly interested in the income potential here, the same applies to the Series D Fixed-to-Floating Rate Non-Cumulative Perpetual Preferred Stock (NYSE:SNV.PR.D) and the Series E Fixed-Rate Reset Non-Cumulative Perpetual Preferred Stock (NYSE:SNV.PR.E). Let's take things from the start...

In addition to providing commercial and consumer banking services, the company also offers a full suite of specialized products and services, including wealth management, private banking, international banking, capital markets, treasury management, asset-based lending, structured lending, mortgage services, and premium finance. It serves its clients through its wholly-owned subsidiary bank, Synovus Bank, and other offices across Alabama, Florida, Georgia, South Carolina, and Tennessee.

Moreover, the company extends its financial services through direct and indirect wholly-owned non-bank subsidiaries. Synovus Securities, headquartered in Columbus, Georgia, specializes in professional portfolio management for fixed-income securities, investment banking, asset management, financial planning, and brokerage services. Similarly, Synovus Trust, also headquartered there, provides asset management, trust services, and financial planning solutions to clients.

Recent results were generally promising. The company experienced some growth in its deposits, which climbed to $50.74 billion in 2023, marking a YoY increase of 3.82%. The loan portfolio saw a slight dip to $42.93 billion, representing a YoY decrease of only 0.8%. Further, the Weighted Average Rate (WAR) of the loan portfolio increased to 6.21% in 2023, marking a 177 bps increase.

On the profitability front, the company witnessed substantial growth, with interest revenue reaching $3.05 billion in 2023, showcasing a remarkable 46.95% increase. Net interest income remained steady, however, at $1.82 billion in 2023, reflecting a modest YoY increase of 1.1%. Similarly, non-interest income only climbed down to $404.01 million; a YoY decrease of 1.3%.

Now, net income shrank to $542.14 million, marking a notable YoY decline of 28.47%. Consequently, the company's EPS witnessed a decline from $4.95 in 2022 to $3.46 in 2023, reflecting a decrease of 30.1%.

Note, however, that net income and EPS capture an FDIC special assessment charge which was 225.74% higher than that in 2022. Also, the difference between a restructuring charge reversal in 2022 and an actual charge in 2023 further contributed to the exaggeration of lower profitability, as it involved a $27 million increase. Excluding those changes, the YoY decrease in net income would be about 16%, a much more modest step back if you will.

Looking forward to 2024, management anticipates end-of-period loan growth to be in the 0-3% range and core deposit growth between 2% to 6%. Adjusted Revenue Growth is forecast to be within a range of -3% to 1%, while guidance for Adjusted Non-Interest Expense entails a decline within the range of -5% to -1%.

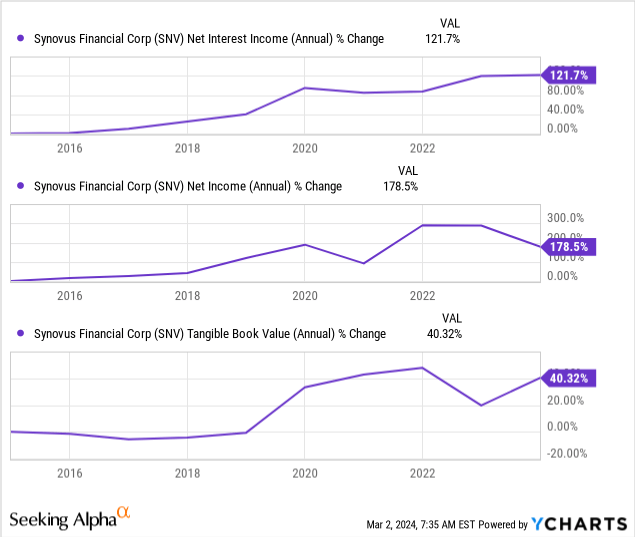

Zooming out, Synovus has been growing at a relatively fast pace during the last 10 years with strong trends in interest and net income, as well as equity growth:

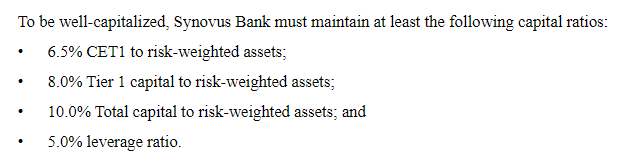

Its solvency profile doesn't raise any red flags either. The company reports the following as capital/liquidity requirements:

10-K

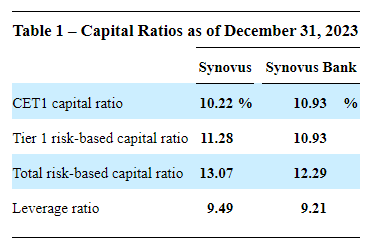

As of the end of 2023, its relevant ratios well exceeded such requirements:

10-K

The LDR as of the end of 2023 was 84%, 450 bps lower than in 2022. Moreover, the company had $2.4 billion in liquid assets, 23.95% more than by the end of 2022. Even though there is a great margin of safety here, it's important to ensure that the loan portfolio is healthy enough to preserve such a margin.

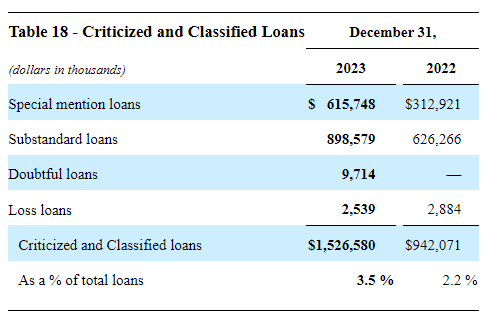

To that end, it's useful to first understand that the loans assessed as risky represented 3.5% of the portfolio by the end of 2023, a significant increase from 2.2% in 2022. Note that the amount of Special Mention loans almost doubled:

10-K

Further, the non-performing loans ratio increased by 33 basis points year-over-year, reaching 0.66%, which suggests a deterioration in loan quality over the past year. Moreover, the provision for credit losses surged by 124% compared to the previous year. Last, the net charge-off ratio climbed by 22 basis points year-over-year to reach 0.35%; a substantial increase too.

So, while the company is currently solvent and has strong liquidity, the current environment requires constant monitoring of such key metrics to be up-to-date on any strong trend away from this state.

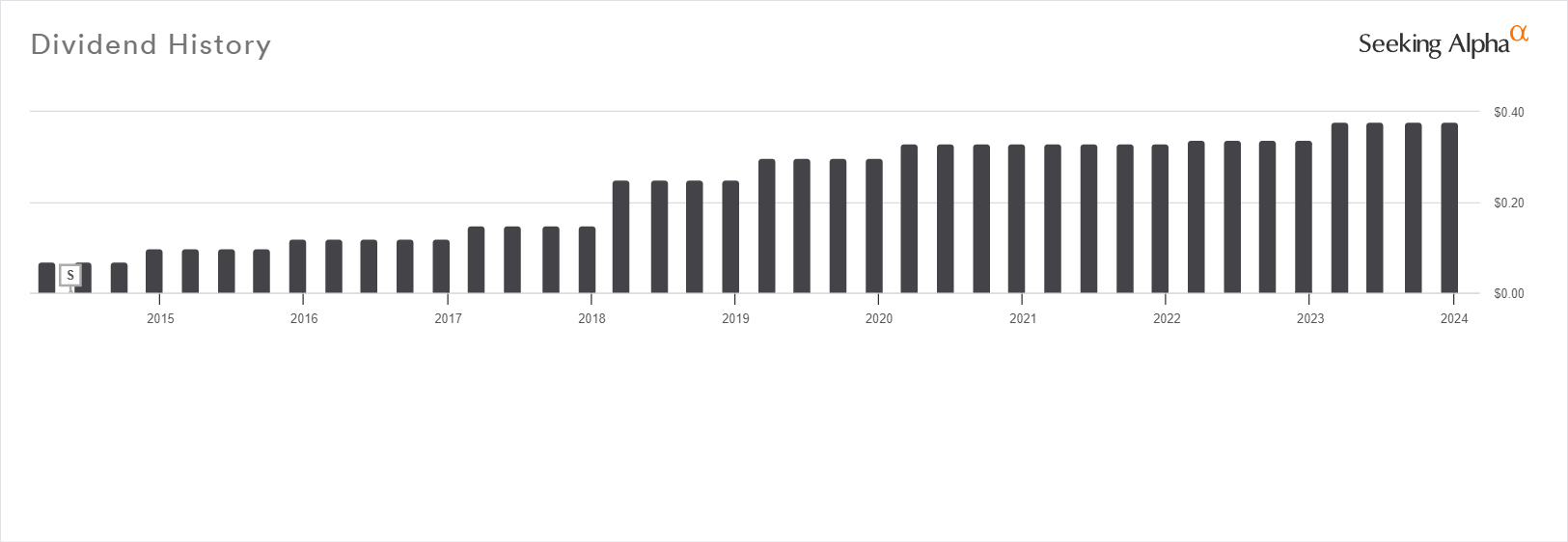

The company currently offers a quarterly dividend of $0.38 per share, indicating a forward yield of 4.01%. With a payout ratio of 36.8% and a remarkable track record of continuous dividend hikes, saying that the dividend profile is healthy would be an understatement.

Seeking Alpha

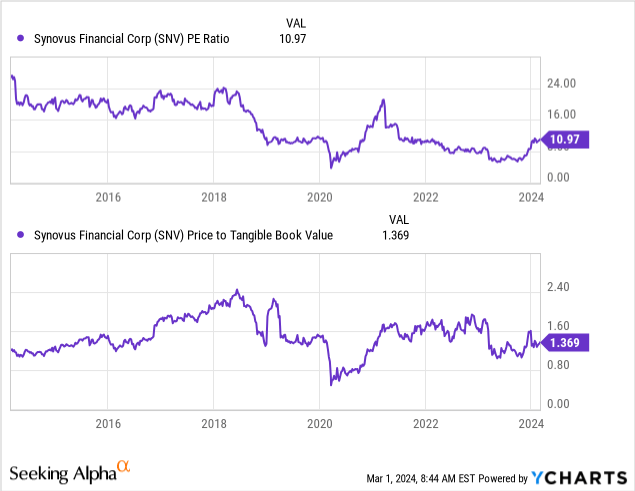

Further, the shares seem to be trading at a historically low earnings multiple, although they're offered at a premium to book value:

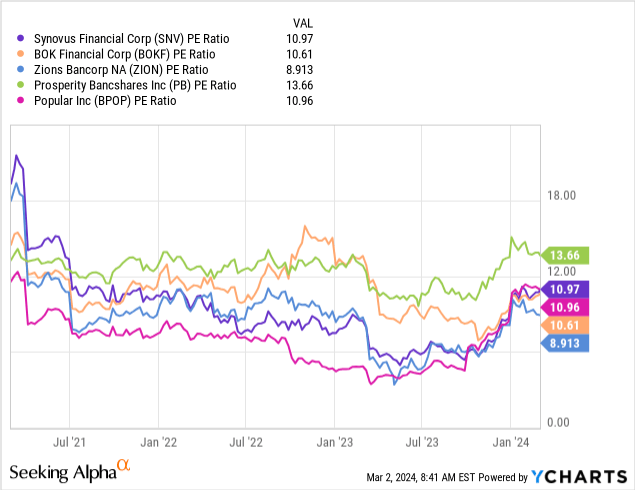

Though the price is low on an absolute basis, a comparison to peers makes it appear more or less fair:

For this reason, while SNV may be an attractive dividend pick, I wouldn't pick it as a value one.

Now, investors who are interested in SNV mainly for the income prospects may also want to consider the Series D preferreds which offer a competitive dividend yield of 8.93%, trading at a premium of 2% to liquidation preference. Keep in mind, however, that the dividend has already been adjusted to the 3-month LIBOR rate (currently 5.6%) plus 3.352%; this entails a potentially lower yield during a low-interest environment.

If you're curious about the Series E preferreds, their yield is lower at 5.85% and are trading at a more modest premium of 0.4%. However, on July 1, 2024, the rate will reset to the 5-year U.S. Treasury Rate (currently at 4.17%) plus 4.127%, so the yield could be around 8% if the rate doesn't change significantly.

It's very important to keep in mind certain risks before investing in either the commons or preferreds:

After taking into consideration both the long and short-term performance of Synovus, as well as its solvency profile and valuation, I believe that it's a very good addition to a dividend portfolio if not a value one. The preferreds are also a good alternative for those who require less volatility. So, I am rating all of them as a buy.

What are your thoughts? Do you own any of them or intend to do so? Feel free to leave a comment below and let me know. Thank you for reading!