Sundry Photography

Sundry Photography

I guess many investors have plunged into an investment in Snowflake because of famed value investor Warren Buffet’s rather large stake in the enterprise. Warren Buffett purchased 6.13 Million shares in Q3 2020 for $120 a share. Then, the shares zoomed up to around $400, giving a rather nice gain. But now, Berkshire’s unrealised profits are melting away like tears in rain; to quote Roy Batty.

It seems to me that Snowflake’s stock price has further to fall given the numerous red flags and rather ugly trends.

Put simply, Snowflake allows companies to place their data into an enormous digital filing cabinet in the cloud. Unlike your standard filing cabinet, Snowflake can grow and shrink depending on what an entity needs. Organisations can store tons of information without needing a load of processing power to retrieve it. This lets an enterprise scale up for large tasks, such as analyzing mountains of data, without impacting everyday tasks.

Snowflake also breaks down barriers between disparate parts of an organisation's data, such as sales records and customer feedback. This lets everyone in a company work together on the same information, which is comparable to accessing files in a shared folder.

Snowflake can also incorporate tools such as ChatGPT, which can act as a super-duper research assistant. Using ChatGPT, users can ask questions about their data in plain English. The Snowflake software helps bridge the gap by translating those questions into a language a computer understands, then analyses the results and explains them in a clear way.

In short, Snowflake keeps an organisation’s data organized and accessible, making it easier for tools like ChatGPT to unlock valuable insights from it.

A key point to note is that Snowflake’s software is proprietary, that is to say, it is not open source.

A declining revenue retention rate is a red flag for a business, particularly subscription-based or software-as-a-service companies. It often indicates a weakening ability to retain existing customer revenue. Alternatively, the company may be experiencing problems upselling and cross-selling. If this is happening, it suggests customers aren't seeing enough value in expanding their relationship.

The downward trend in the revenue retention trend is not a pretty sight for Snowflake investors.

Table of revenue retention (Author produced table)

Such a declining revenue retention rate can negatively impact a company's financial health in a variety of ways. To begin with, it can lead to decreased revenue growth as an inability to retain existing customer revenue makes it harder to achieve overall growth.

As noted, a declining retention rate can result in a fall in a company’s growth trajectory, as the table below illustrates.

| Q4 2023 | Q 1 2024 | Q 2 2024 | Q3 2024 | Q4 2024 | |

| Revenue Growth YoY | 54% | 50% | 37% | 34% | 33% |

Naturally, one would expect revenue growth in percentage terms to decline over time. Nevertheless, the horrid direction of the trend is plain for all to see, especially when one compares Q4 2023 to Q4 2024.

Naturally, many Investors pay particular attention to both customer retention metrics and product revenue growth numbers. It’s no surprise that declines in these numbers can cause stockholders to go all wobbly, the effects of which are typically reflected in a plummeting stock price.

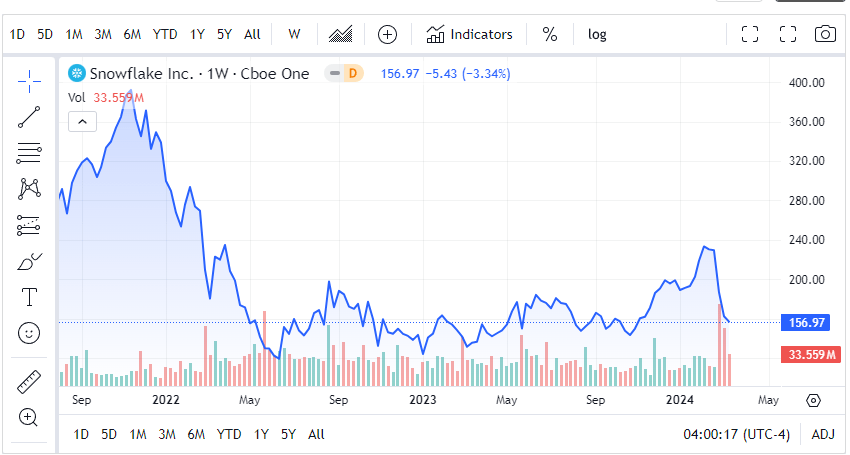

Chart of Snowflake price action (SA)

Negative trends in revenues and retention rates can also imply that a competitor is eating their lunch. Well, Snowflake does have an impressive competitor in the shape of privately held Databricks.

As of today, Snowflake’s website states that the company has 9,437 global customers, whereas, Databricks recently announced that they had more than 10,000 customers. In fact, the number of clients Databricks has signed up has increased by around 100% in a little over 2 years! (More than 5,000 in 2021).

Given that Databricks is privately held, details of revenue numbers are not easy to obtain. However, some reports claim that Databricks' revenue is estimated to be around $1.275 billion in annual recurring revenue for 2022 and is projected to reach $1.9 billion in 2023, which is a growth rate of 55.3%.

Databricks Technology

Snowflake was founded in 2012, while Databricks came a year later in 2013. Both are major players in the cloud data space, but with slightly different approaches.

Databricks differs from Snowflake in a number of important areas. To begin with, Databricks employs open-source tools, such as Apache Spark, which is a super-fast engine that can crunch massive amounts of data. Databricks makes Spark easier to use by sorting out the technical setup.

Databricks also offers its own open-source tools to help data teams. Delta Lake acts like a filing cabinet, keeping all the data organized and reliable. And MLflow is another tool, but for building and managing artificial intelligence projects, like teaching machines to recognize patterns and the like.

Proprietary Tools Or Open Source, That Is The Question

There is often a battle between proprietary and open-source tools. We are all familiar with the victory of Windows OS over Linux in desktops. However, Linux has become a dominant force in servers and web hosting. It's known for its stability, security, and customizability, rivalling proprietary options like Windows Server.

Often, there are a number of advantages of opting for open-source solutions. For instance, open source generally has a reduced upfront cost, as a result of reduced licencing fees. Then there is typically a large community of developers who may be able to identify and fix bugs faster, or foster faster innovation.

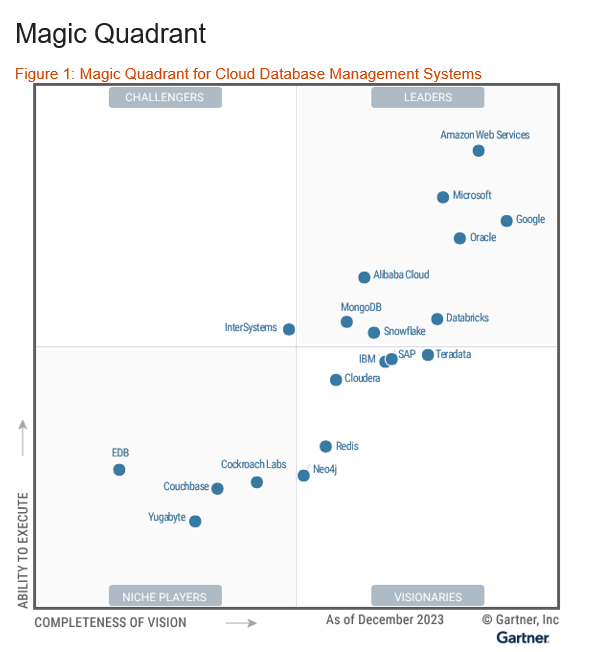

Without a doubt, both companies have a high quality offering, as evidenced by the Gartner report on the magic quadrant for cloud database management systems.

Gartner Magic Quadrant (Databricks' website)

Recently, Databricks has forged a strong relationship with a key player in the AI sector and has made an acquisition that will give the company a significant advantage over Snowflake.

In July 2023, Databricks announced that it can complete the acquisition of MosaicML. If you take a look at MosaicML’s website, you can quickly understand that Databricks has gained a significant advantage over Snowflake. While ChatGPT and MosaicML are both involved with large language models, they serve different purposes. The MosaicML software platform has been designed to assist with training large language models such as ChatGPT. Furthermore, the platform focuses on making the training process more accessible and efficient for organizations that want to create custom models. That is to say, MosaicML does not compete with ChatGPT, rather it enables ease of use.

On the 14th September, it was announced that Nvidia had coughed up a big chunk of change to participate in Databricks’ Series I funding, which raised over $500 million. It is evident from the announcement that Nvidia plan to do all the can to ensure that they get a hefty return on their investment. In my view, this cannot be viewed in a positive light by Snowflake stockholders. In the release, you will find the following quotes;

Ali Ghodsi, Co-Founder and CEO of Databricks. "Databricks and NVIDIA are building transformative AI technology, and we're excited about the business value and innovation we can bring to our customers."

"Enterprise data is a goldmine for generative AI," said Jensen Huang, founder and CEO of NVIDIA. "Databricks is doing incredible work with NVIDIA technology to accelerate data processing and generative AI models."

The above represents my view of the company, and of course I could be entirely wrong. This time next year I could be sitting here with copious quantities of egg on my face.

To begin with, Snowflake could win the proprietary versus open-source contest, resulting in the Snowflake stock price making its merry way to the moon.

Newly appointed CEO Sridhar Ramaswamy, whose knowledge and experience of all things AI is extensive, may build a team of specialists that construct a platform that can overtake Databricks.

Snowflake is facing numerous serious challenges. Their revenue retention rate is declining, which could hurt future growth. Additionally, competitor Databricks is growing rapidly and has recently acquired technology that could give them an edge. With these multiple red flags, investors may wish to revise their opinion about Snowflake's stock price.