BrilliantEye

BrilliantEye

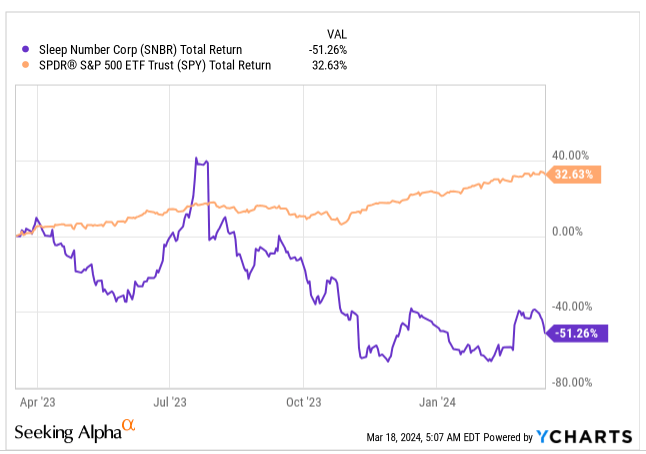

The stock of Sleep Number Corporation (NASDAQ:SNBR), a wellness technology company which is considered to be the 3rd largest bedding retailer and etailer in the U.S. (Source: Furniture Today), has likely given a lot of sleepless nights to its shareholders; over the past year, at a time when the key benchmark has risen by close to a third, our focus stock has lost over half its value.

YCharts

Prima facie, given the relatively high ticket prices associated with the company’s portfolio of smart beds, there’s a sense that this may never quite become a mass-market brand. For context, last year, the company’s network of smart sleepers stood at 2.8m, but that accounts for just over 2% of total U.S. households.

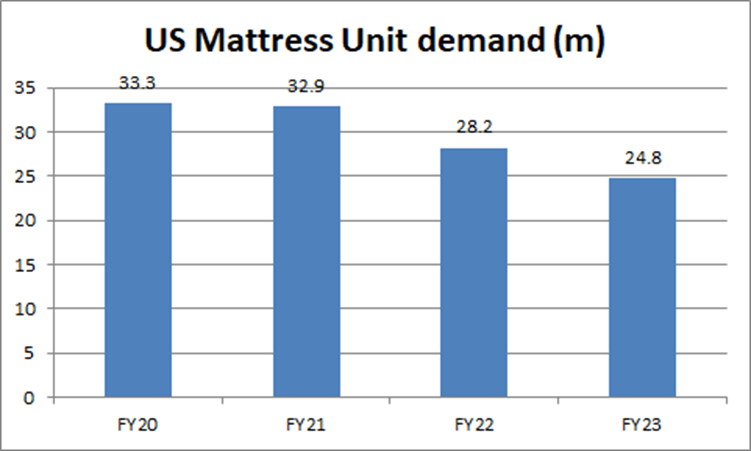

Then, it also doesn’t help that demand for mattresses in general have been on a downward trajectory, since peaking in FY20, with double-digit YoY declines seen in each of the past two years.

International Sleep Products Association

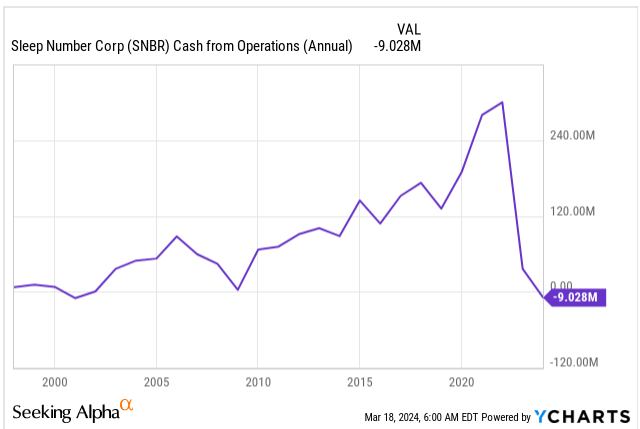

Then, the company’s EBIT which stood at $193.5m back in FY21, has collapsed by a fifth, and wasn’t even sufficient to cover its interest bill last year. Meanwhile, the company’s financial gearing (debt and operating leases as a function of EBITDAR) has almost doubled from levels of 2.2x seen in the pandemic year to 4.1x. Compounding the issue, we have, for the first time in a long time, seen SNBR’s inability to not generate any positive operating cash flow on an annual basis.

YCharts

Clearly, SNBR is in a bad way. However, we see still see a few encouraging sub-plots and are enthused by some of the recent decisions taken by the management team to right the wrongs.

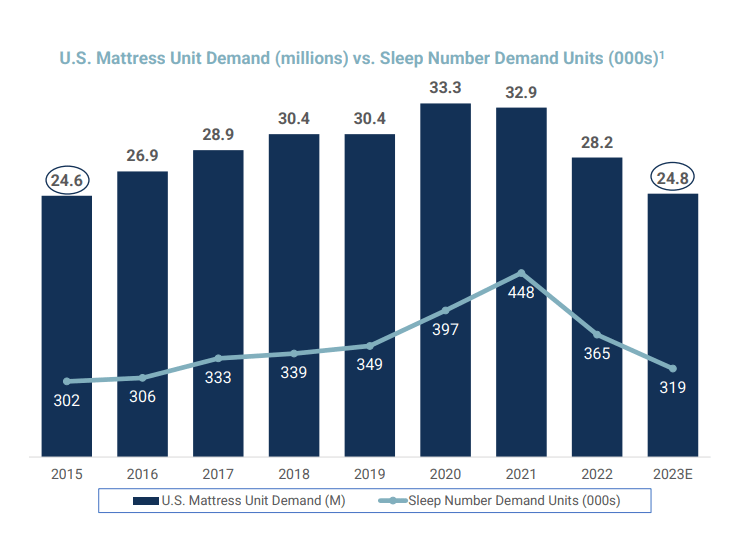

Industry Unit volume declines have been a lingering trend for many years now, but SNBR has still done well to hold share in a challenging environment and this suggests there are people who still see merit in the product portfolio. As things stand, industry volumes are now at levels last seen around a decade ago, in 2015 (24.6m units), but note that SNBR’s own unit volumes are up by 6% during this period.

SNBR

Now, even if one were to assume yet another challenging year of de-growth for the industry (SNBR itself is expecting a mid-single-digit decline on the topline), we’re encouraged by the initiatives that management has taken to right-size the cost base.

Management took some pricing actions over the past year, and that coupled with favorable commodity dynamics, were already instrumental in driving gross margin progression of 80bps in FY23. Looking ahead to FY24, the goal is to extract another 100bps of improvement, from further raw material cost initiatives, value engineering, additional efficiencies via their home delivery network. For a company to extract an aggregate improvement of 180bps on the GM front when its top line has been collapsing is no mean feat. When the market starts growing again, GM progression could well get back to the low 60s range.

On the operating front, we’ve seen the company reduce its workforce (the team size has been curtailed by 25% relative to what was seen in FY21), resort to greater outsourcing, and simplify it service programs. We’re also likely to see meaningful improvements when it comes to trimming the number of stores. Already last year the net stores opened was relatively flattish (672 at the end of FY23 vs 670 in FY2), but this year it will come down by another 25-30 stores. All in all, investors could be looking at a $40-$45m YoY reduction in the OPEX cost base of FY24.

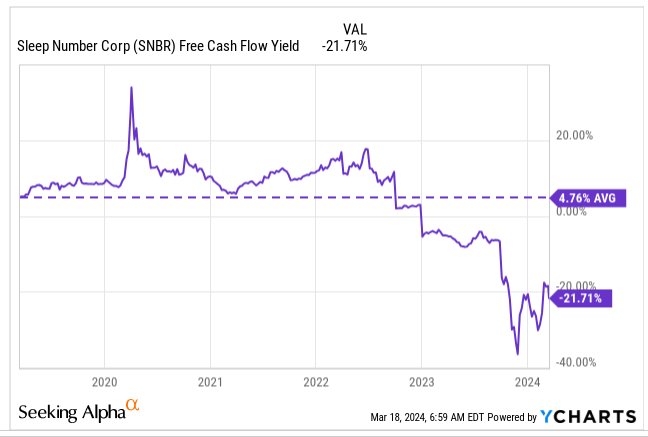

In addition to that, improvements will likely also been seen on the FCF front, after the firm failed to generate any positive figure last year. Between Q3 and Q4 we already saw CAPEX commitments drop by half, and in FY24 for the whole year, it will likely come in 50% lower at only $30m.

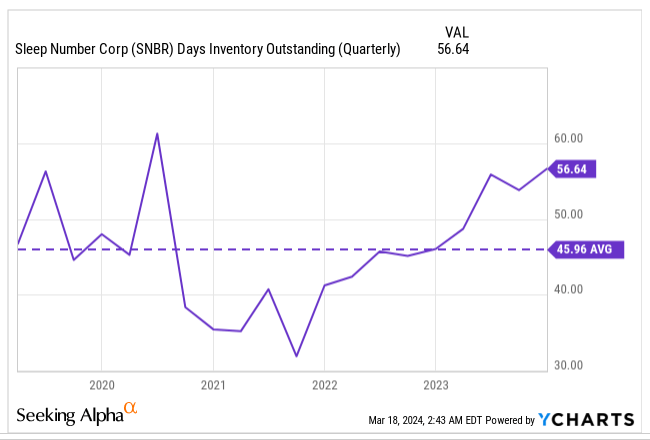

Also note that SNBR’s days in inventory is currently 23% above what they normally maintain, and adjustments here should reflect well on the working capital outlay.

YCharts

In fact, on the recent earnings call, management was keen to reiterate that working capital which had been a use of cash for the last two years, was likely to be a source of cash in FY24. The goal in FY24 is to now bring through positive FCF of $60-$80m. This should help bring the stock’s FCF yield (which is currently floundering deep in the negative zone) a lot closer to its long-term average of nearly 5%.

YCharts

With positive FCF of roughly $70m next year, management feels they can bring down their leverage to less than 3.75x.

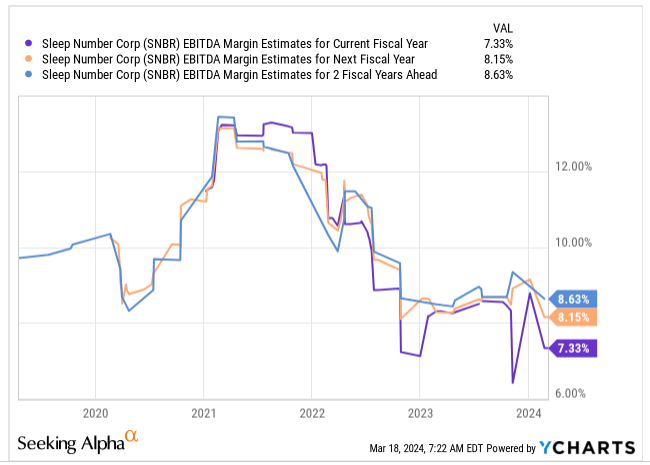

As noted in the previous section, Sleep Number is poised to generate significant benefits on the OPEX base which should do a world of good for the company’s EBITDA margins. Crucially note that EBITDA margin progression won’t just end with this year, and as the market bottoms out and starts growing again (potentially from FY25), we could see further improvements over the next two year.

Well, that’s certainly what consensus estimates are pointing towards; after coming in at 6.7% last year (on an adjusted basis), EBITDA margins are poised to increase every single year through FY26 (aggregate improvement of nearly 200bps).

YCharts

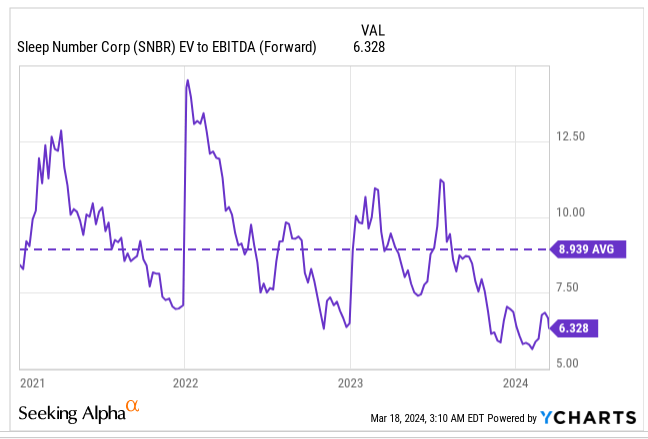

In light of such a sustained EBITDA improvement trajectory, we feel the stock’s current forward EV/EBITDA multiple of just 6.33x looks very attractive, particularly as it represents a ~30% discount over the stock’s long-term average.

YCharts

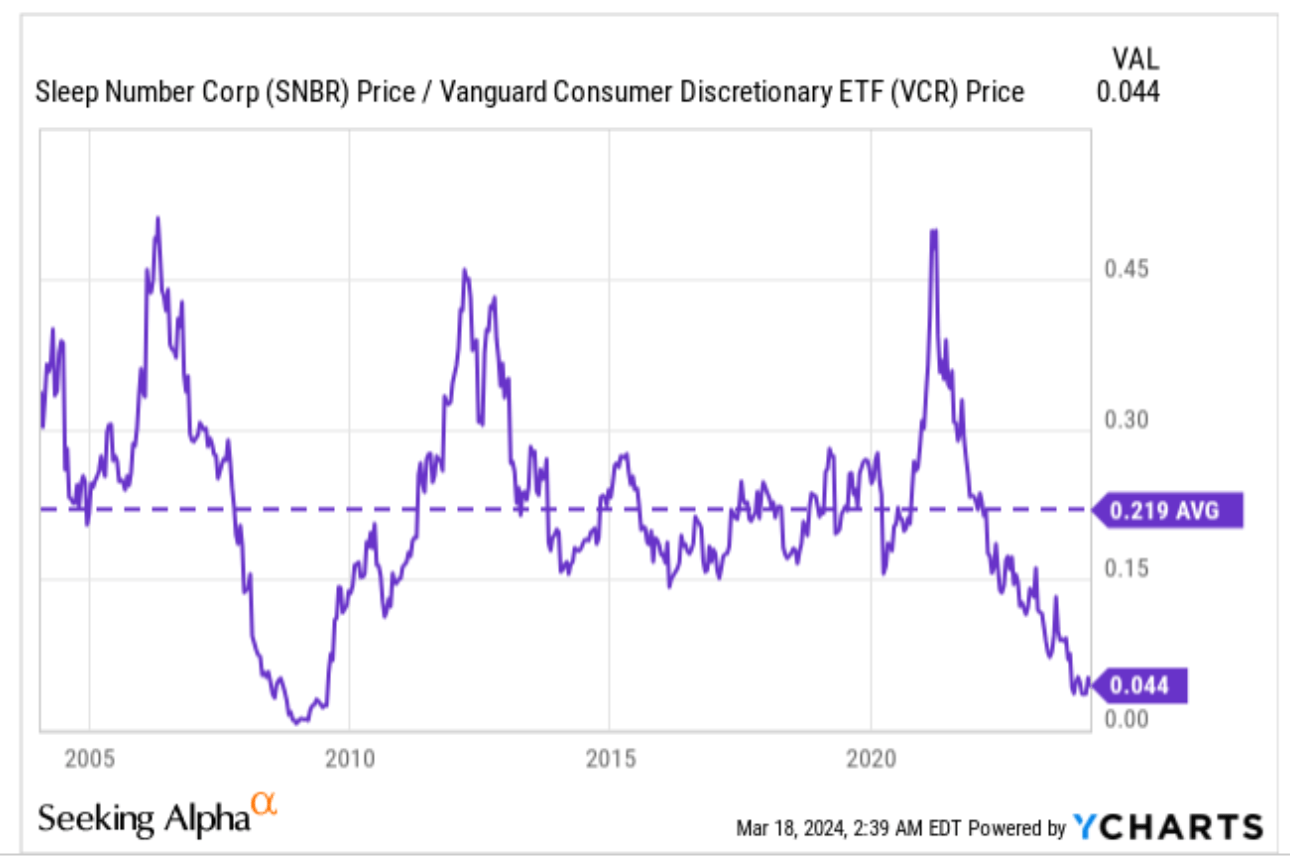

We also like SNBR because we feel that its relative strength versus its discretionary peers has been overextended towards the downside (the current ratio is only one-fifth of its long-term average), and could potentially mean-revert in the periods ahead. As things stand, the ratio is not far from the GFC era lows, from where we saw a bounce.

YCharts

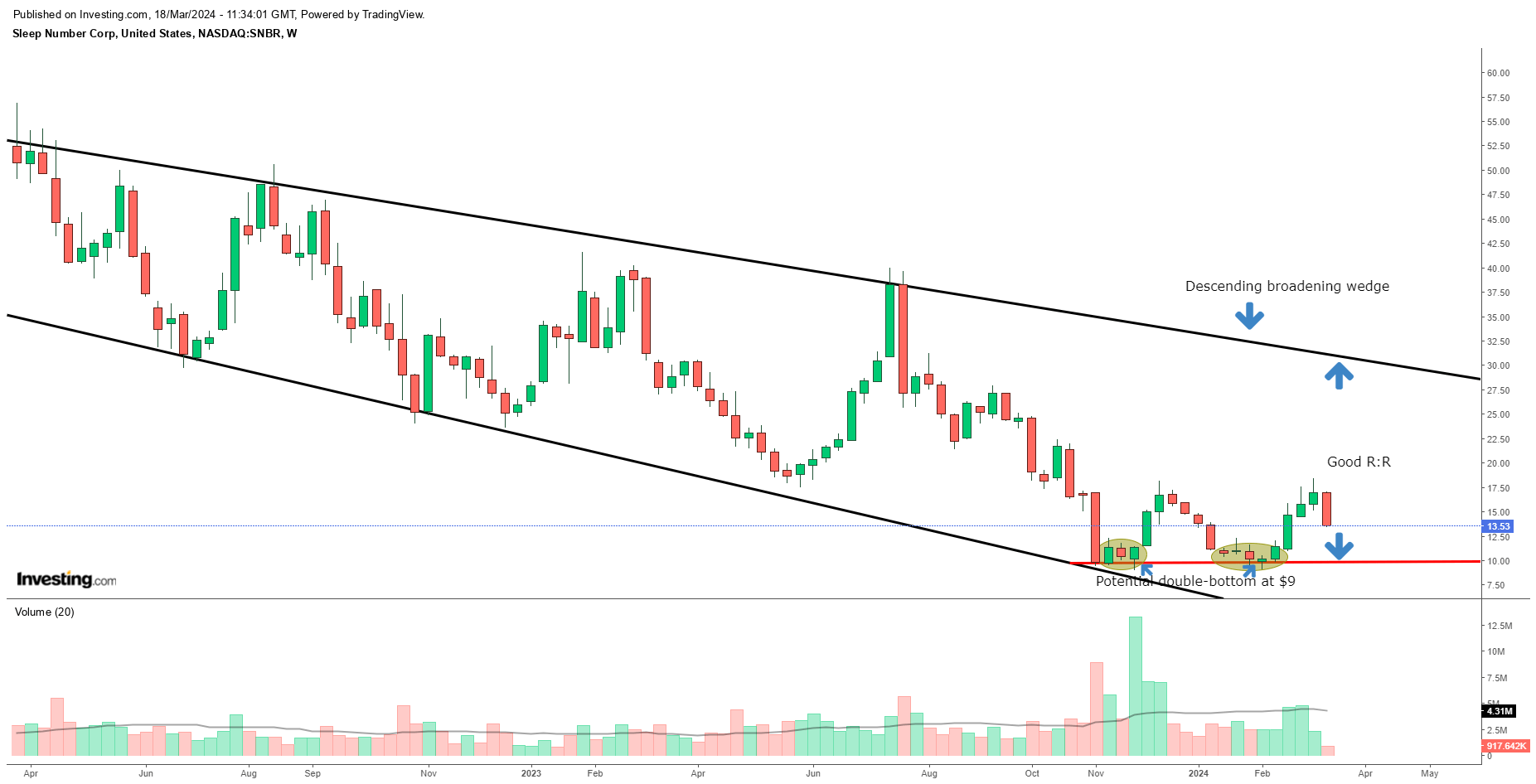

Finally, if we look at SNBR’s own weekly price imprints for the last two years, it appears that the stock has followed a descending broadening wedge pattern, which has demonstrated a high probability of troughing at lower levels, and then reversing course. Even if you want to discard this pattern, note that the price still has ample runway to hit its upward sloping resistance.

In recent weeks, we’ve seen the stock bottom out at the $9 levels, followed by another re-test which saw it pivot from there again. To conclude we think the stock is a BUY here, and investors considering this stock can go long at current levels, using the $9 levels as a potential stop.

Investing