Fahroni/iStock via Getty Images

Fahroni/iStock via Getty Images

Snap-on Incorporated (NYSE:SNA) is a +100 year old industrial business whose broad product portfolio and services are provided across 130 countries across the world. The company was originally noted for being the flag bearer of mobile distribution of auto repair tools, but has, over time, expanded its expertise and presence in other end-markets, such as natural resources, manufacturing, aerospace, and defense.

Principally, there’s quite a bit to like about Snap-on.

It’s fair to say that machines are becoming more complex by the year, and this trend is most keenly felt in SNA’s legacy auto market. For instance, as things stand, repair service centers now have to dissect and service auto models that already have well over 100 ECUs (electronic control units). The burgeoning influence of themes such as big data, AI, biometrics, the level of sophistication associated with these machines will only grow over time.

The corollary of having a higher installed base of innately complex devices is that breakdowns are likely to be more obdurate, prompting even more precious service hours. That’s where SNA’s product portfolio of critical tools can help service centers (both independent and OEM related) manage the level of complexity, whilst arriving at solutions without compromising on safety or efficiency.

Investors who are reliant on dividends will also be enthused to note that this is a business that has been doling out quarterly dividends for well over three decades now (for context, industrial firms, on average have typically only been paying dividends for around a dozen years). It has also been growing its dividends for 14 years, and over the last three years the pace of dividend growth has been rather healthy at 14-15% p.a.

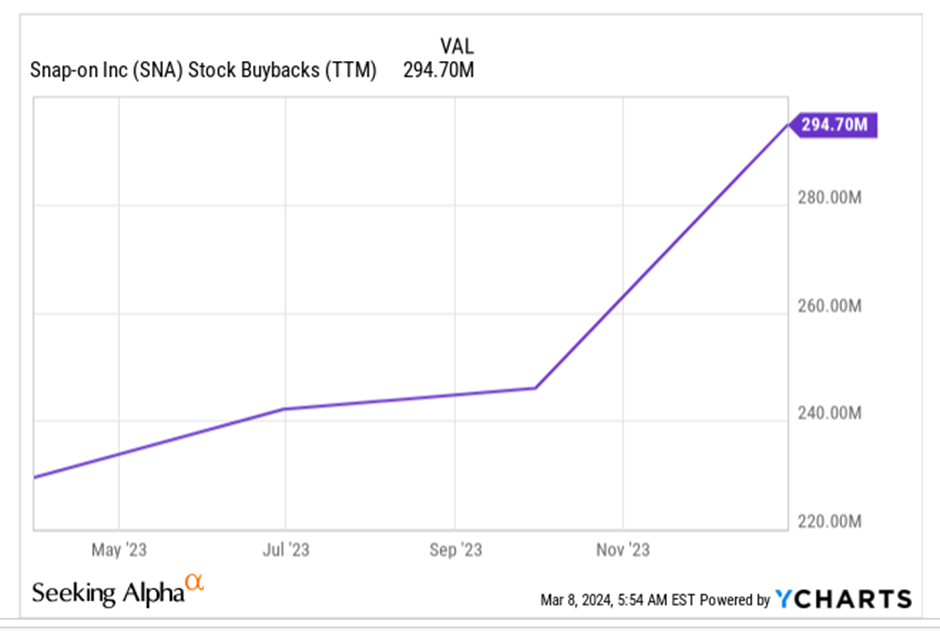

It isn’t just dividends; also consider that over the past year, the company has ramped up its buyback spend over time (currently at nearly $300m on a trailing twelve month basis).

YCharts

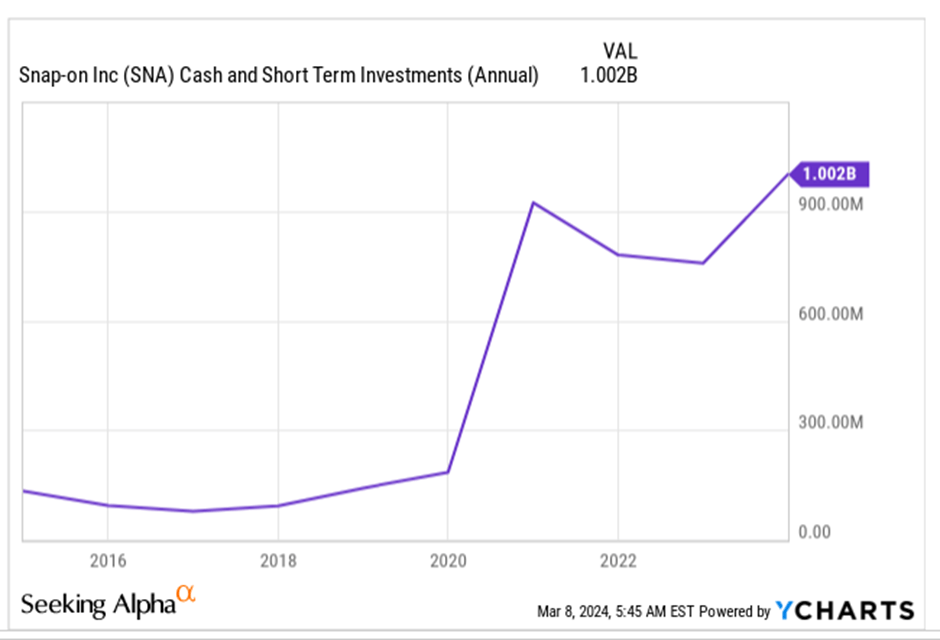

The generosity with its shareholder returns is founded on a very healthy cash position. The cash on its books as trended up at a healthy pace over the past decade, and recently crossed the landmark of $1bn (as of December 2023).

YCharts

Despite the critical nature of SNA’s solutions, and some of its fundamentally sound characteristics, we wouldn’t be too perturbed if we couldn’t get our hands on the SNA stock at this juncture.

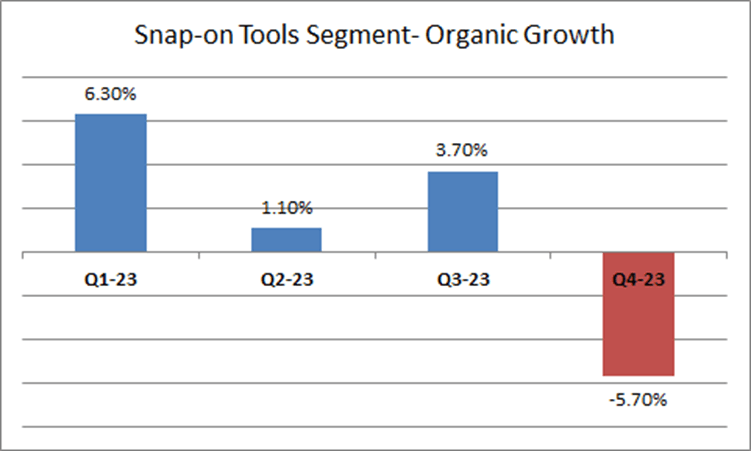

Firstly, do consider that SNA’s largest segment- Snap-on Tools, which contributed ~37% of group sales last year, has started facing some headwinds. Management recently described the performance of this segment in Q4 as “not at our standards” as organic growth which had been positive for the first three quarters, dropped by nearly -6%!

Earnings transcripts

The confidence of clients in this segment appears to have taken a hit, and management feels that there is now a predilection towards lower-ticket items. Now in the next few quarters as lower-ticket items take up a larger share over the overall mix, expect some margin pressure (given the importance of this segment relative to the overall group business). The other thing to note is that the base effect in Q1-24 isn’t too low either (this time last year the segment was delivering positive organic growth of over 6%).

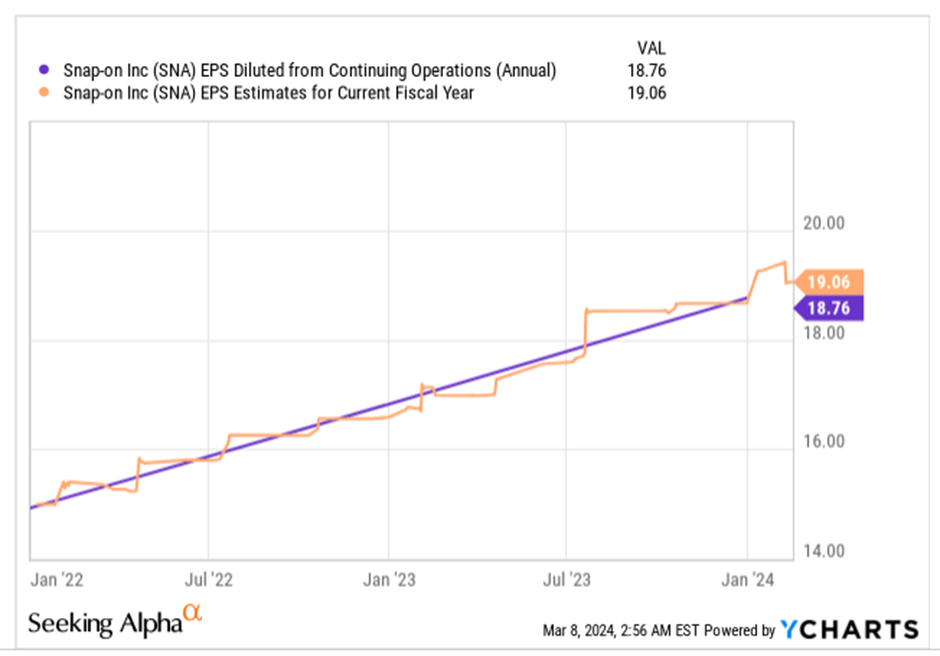

Taking a broader perspective beyond tools also consider that this is a business that has grown at 9% CAGR over the last three years, but based on consensus estimates for the current year (the average of 10 sell-side analysts), topline growth is expected to come in at a miserly pace of 2.6%.

It also does not look like SNA will generate favorable operating leverage, as EPS consensus for FY24 suggests that forward earnings growth (1.6%) will come in 100bps lower than the forward topline growth.

YCharts

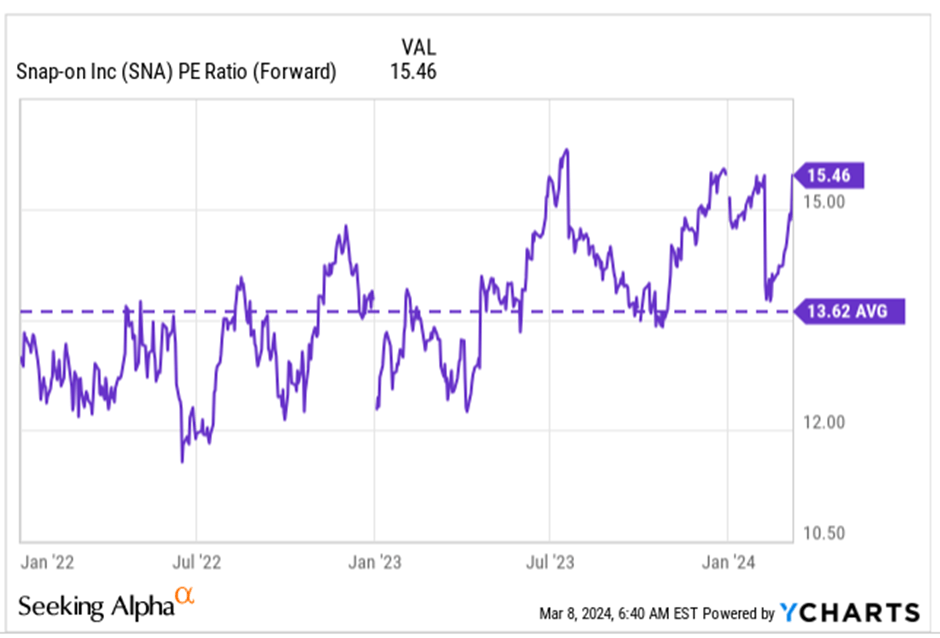

In light of such underwhelming forward earnings growth and the lack of operating leverage, it may be worth pondering, if it’s worth paying up for a forward P/E of 15.45x (which translates to a pricey PEG ratio of almost 10x), particularly when that multiple also represents a 14% premium over the stock’s own rolling 5-year average.

YCharts

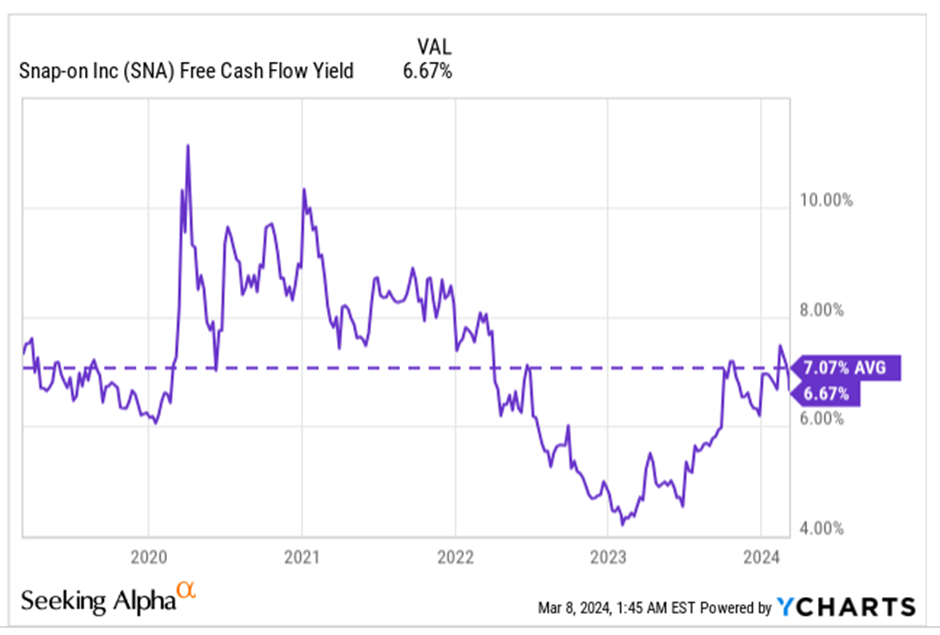

Separately, we would also point to SNA’s sub-par FCF yield position. This is a firm that has generated a very healthy operating cash flow position over the years. Last year alone, one saw a tremendous 70% spike in the operating cash flows as they generated $1.1bn for the year, but yet given that the share price is not far from lifetime highs, the FCF yield still lags the 5-year average.

YCharts

It’s also worth noting that last year’s OCF benefited a great deal from inventory drawdowns, which is not really the norm (for context over the last decade, inventory has been a source of cash only in two years). Looking ahead, we would expect inventory to normalize, particularly as SNA is likely to ramp-up its thrust in low-ticket items in the Tools space, this will likely put pressure on SNA's FCF yield.

Investors can also take a cue from the diminishing insider positioning in the SNA counter. A recent study has shown that it is amongst the top 20 US stocks that has witnessed the most insider selling over the past six months, relative to its market-cap! Furthermore, after a lull in discretionary insider sales in January, this has picked up once again in February and March of this year.

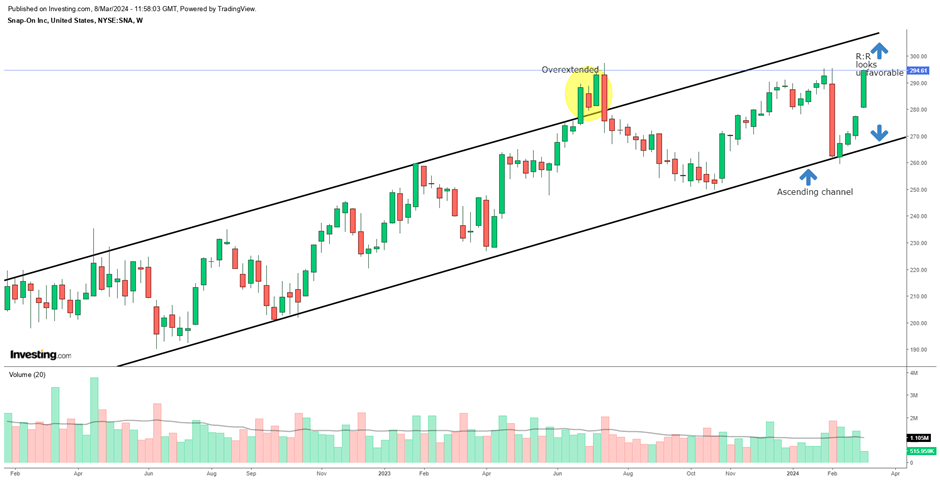

Even if one goes by what the charts are telling us, it's difficult to be too excited about SNA here, as the reward to risk positioning looks unfavorable.

Snap-on’s standalone weekly chart below shows us that the stock has been trending up in the shape of an ascending channel for over two years now. Except for a brief period in June/July last year (area highlighted in yellow), it has largely respected the boundaries of this channel. Now we have a situation, where the stock is on the verge of taking out its lifetime highs, is a lot closer to the upper boundary of the channel, and is at least around 10-11% away from its lower boundary. All these factors make the reward to risk landscape look quite unfavorable.

Investing

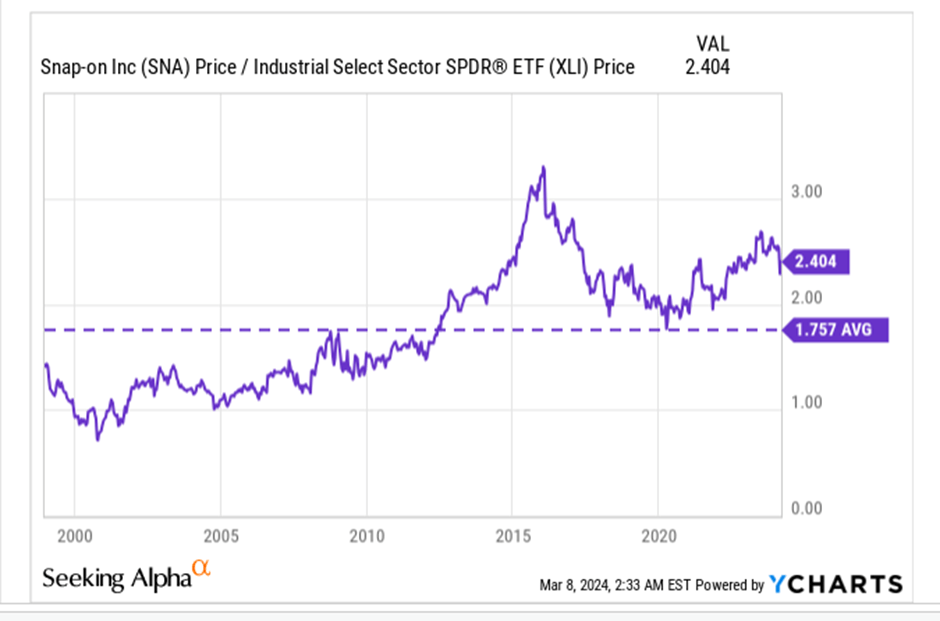

Finally, also consider that investors who are looking for beaten-down bargain opportunities within industrial stocks that comprise the S&P 500 are unlikely to take a fancy towards SNA as its current relative strength ratio (relative to a portfolio that focuses only on S&P 500-based industrial stocks) is around 37% higher than the average reading of its long-term range.

YCharts