Thitima Uthaiburom/iStock via Getty Images

Thitima Uthaiburom/iStock via Getty Images

When I last wrote about digital marketing software company Similarweb Ltd. (NYSE:SMWB), I worried that reduced guidance flagged likely future weakness in the company’s results. I did not see a clear path for converting the company’s increased free users into paying subscribers. The company did not describe its AI offering, SimilarAsk, in a compelling way. Yet, the company’s valuation was low enough to warrant considering a bet on a better future.

Fast forward to Q4 2023 earnings, and Similarweb has answered enough of the questions to convince me to upgrade the stock from hold to buy. Most importantly, Similarweb answered the questions by achieving a major milestone of profitability and free cash flow. Absent any sudden macroeconomic shocks, indicators suggest that the company can sustain its current momentum.

In Q4 of 2023, Similarweb pulled itself out of negative territory for the first time since its IPO. The company achieved non-GAAP profitability and positive free cash flow. A 30 percentage point improvement in non-GAAP margins drove profitability. From the transcript of the earnings conference call:

“Our focus on operating efficiency throughout 2023 drove excellent results culminating in us generating $3.5 million in positive free cash flow in the fourth quarter, a 6% free cash flow margin. We achieved our stated goal of becoming free cash flow positive.”

Similarweb earned a non-GAAP operating profit of $4.7M. The GAAP operating loss came to $1.1M. The company adjusted Q4 GAAP operating loss to non-GAAP operating profit with the following:

The non-GAAP operating margin netted out to 8%. The company expects to be free cash flow positive throughout 2024. Management even confidently declared “now that we’ve got profitability we intend to stay there.” Of course, getting to GAAP profitability will be an even more significant milestone.

While cost-cutting helped to drive profitability, management indicated that process is over. The company is now focused on obtaining profitable growth and working toward “the rule of 40.” The rule of 40 claims that a software company will achieve sustainable growth with its revenue growth rate plus its profit margin at least equal 40%.

The company suggested that it is getting better at converting free customers to paying ones (at the entry level) but did not create a direct narrative. The company reported 13M visitors in total to the website’s tools for an annual total of 120M visits. Accordingly, management called the pipeline “robust” and reported that “we are adding new customers and expanding our penetration into our market.” Entry-level customers are riding a “seamless” on-boarding experience and increasing engagement with the product. The low acquisition costs at the entry level presumably helped boost profitability.

The addition of 341 accounts in Q4 was the company’s highest since its IPO. The company reported that all its segments showed “strong momentum.” In particular, “the big CPGs of the world, telco and financial services and big tech…were doing well.”

Similarweb’s momentum looks further sustainable, with 42% of ARR (Annual Recurring Revenue) locked into multiyear contracts. Remaining performance obligations (RPOs are the total contracted revenue not yet delivered to customers and not yet recognized as revenue) are now a record $195M. Finally, Similarweb anticipates further (small) improvements in the churn rate for contracts below $100K.

In the shareholder letter and earnings presentation, Similarweb described a trough for NRR (net revenue retention) after declining from 109% to 98% over the last 5 quarters:

“our Q4 performance on both logo retention and upsells should affect NRR positively in future periods. Notably, our logo retention of our over $100,000 customers remains high at 96%.”

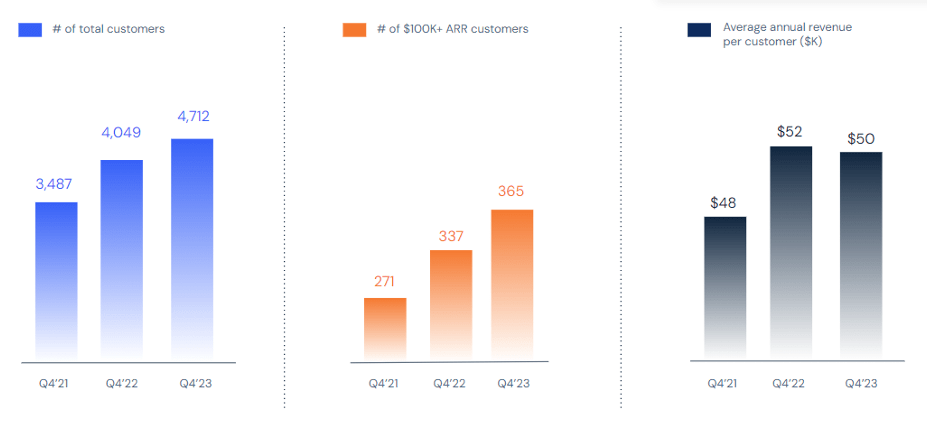

The chart below from the shareholder letter shows Similarweb’s momentum with the average revenue per customer flattening from the surge of entry level customers. (The company also explained “existing customers are increasing budget constraints that impact upsells and downsells.”)

Similarweb's momentum (Similarweb Q4 2023 shareholder letter)

While Similarweb warned that “global macroeconomic conditions will continue to present some challenges for us and our customers over the coming year,” overall guidance looks promising.

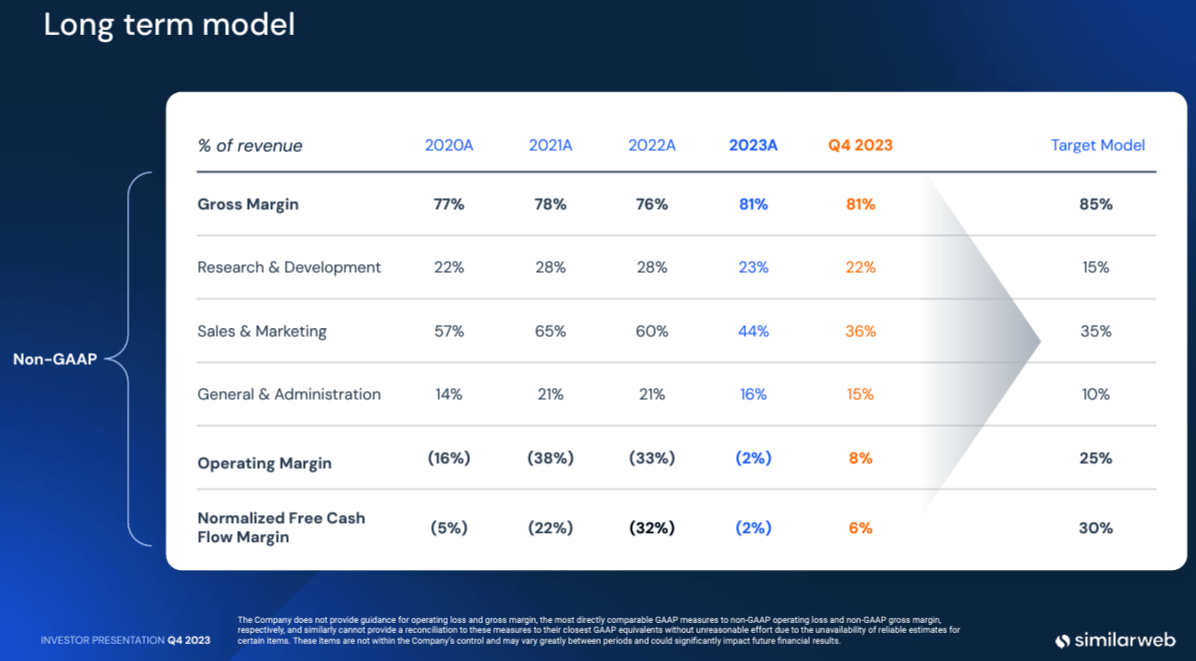

Slide 24 from the earnings presentation provides the long-term targets for investors to monitor.

The long-term trajectory for Similarweb (Similarweb Q4 2023 earnings presentation)

My main disappointment in Similarweb’s results was the lack of additional detail on its AI product, SimilarAsk. While the concept is compelling, I was not convinced about its functionality from the description in the last earnings report.

In this latest report, the company said little and apparently did not even call out the product by name. The earnings presentation includes a small reference to SimilarAsk on its product evolution slide, calling it a version one generative AI beta product. In the earnings conference call, management generically pointed out

“one area where we have a great opportunity to drive market penetration is with our mobile data and app intelligence, as well as by unleashing our own Gen AI…with our data.”

The most interesting commentary on AI capabilities came in reference to Similarweb’s customers after an analyst asked “can you just give us an example on the Gen AI side and how your data fits in?”:

“…because of Gen AI…people behave differently, they search differently. They use a lot of companies implement copilots and AI. So there’s a lot of demand from the big corporate around consumer behavior change. So [if] my consumers behave different than before and then they need market visibility and this is where [Similarweb] is best in the world to give you visibility on…behavior change.”

Needless to say, I am now even more eager to hear and see what SimilarAsk will deliver.

Similarweb’s latest earnings signal a pivotal juncture of performance and strategic execution. Despite my disappointment in the lack of clarity on progress on AI, I am more focused for now on the apparent sustainability of momentum in revenue growth and profitability.

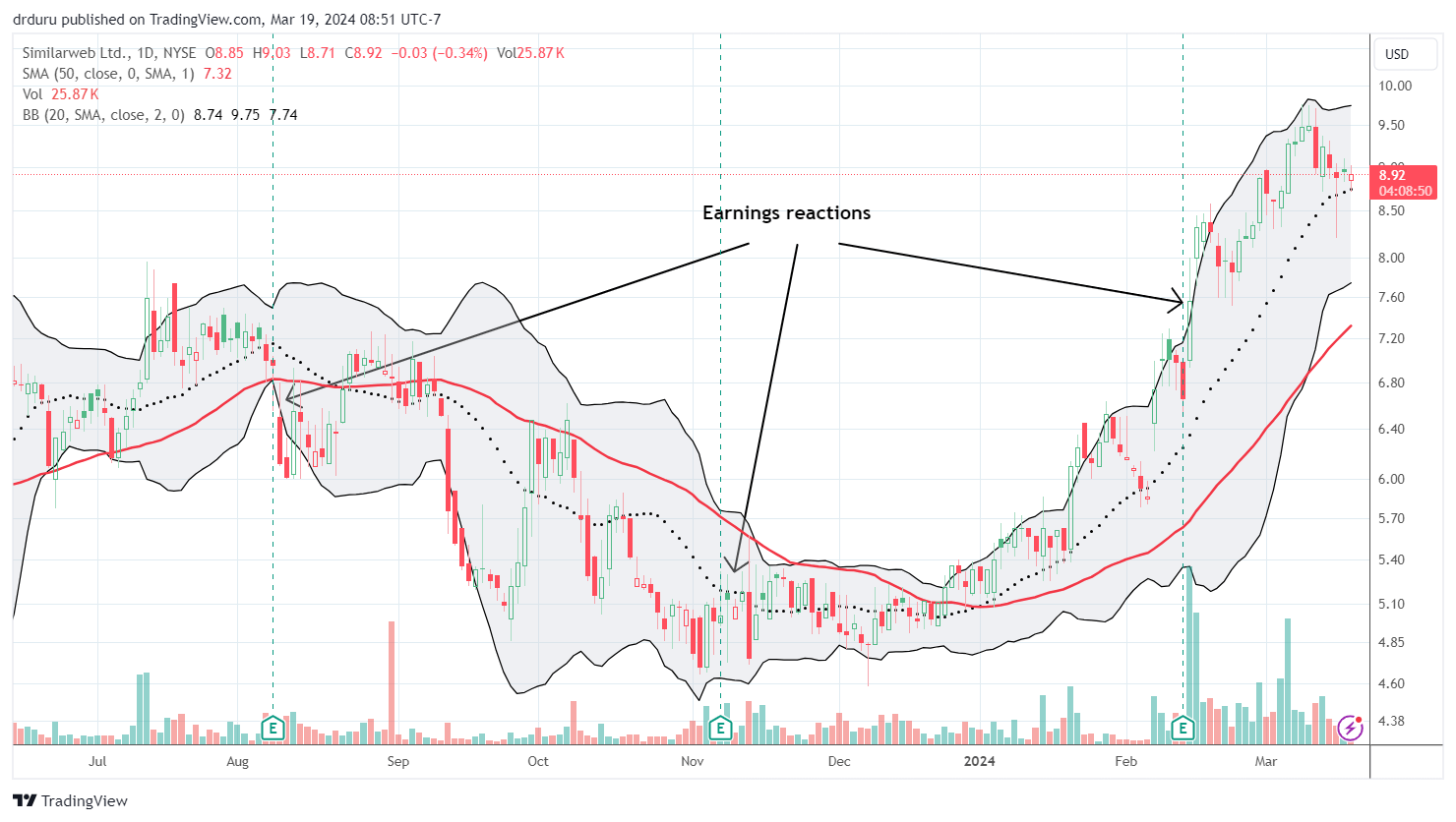

Investors rewarded Similarweb with price momentum in the stock. SMWB surged 13.5% post-earnings and has not looked back since. The subsequent breakout to levels last seen in the summer of 2022 mark an important technical milestone. Moreover, the 20-day and 50-day moving averages are trending upward (the dashed and red lines respectively in the chart below). SMWB is also still relatively cheap trading around 3.1 price/sales. Thus, considering all the recent developments, I upgraded SWMB from a hold to a buy.

SMWB's recent price momentum reflects the pivot in business performance. (TradingView.com)