AlizadaStudios

AlizadaStudios

Summit Midstream Partners (NYSE:SMLP) has seen its market cap consistently sit below $200 million. The company has an impressive portfolio of assets, but it's been held back by its rising debt load. As we'll see throughout this article, the company has a risk of rising interest rates with its debt, which can hurt its future shareholder returns.

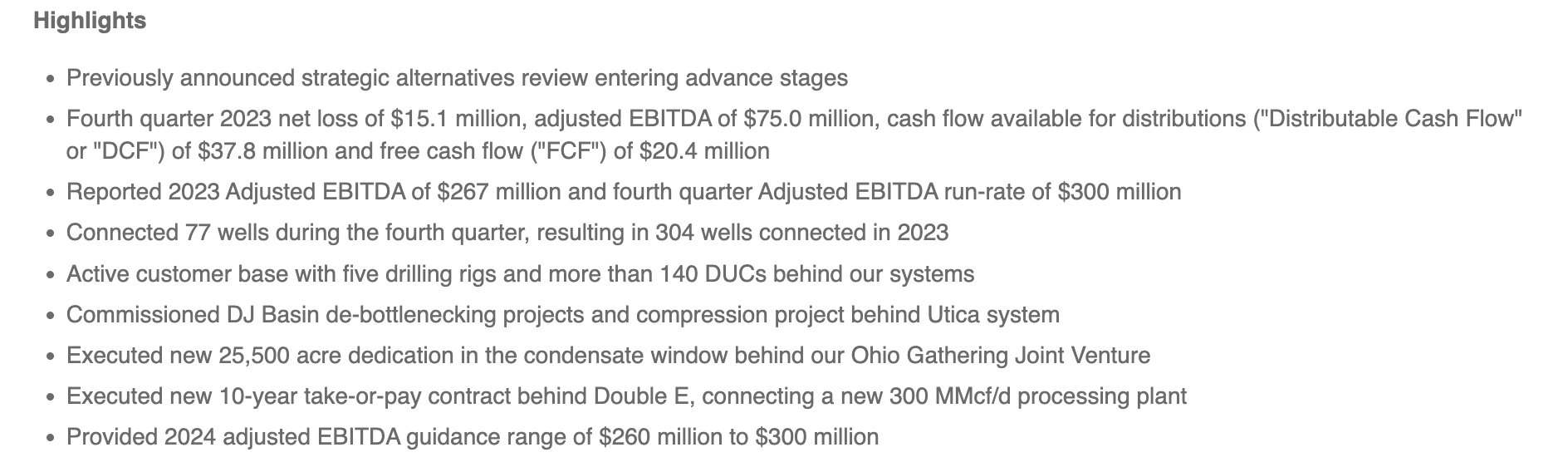

The company had a strong 2023, as it continues to look at strategic alternatives for its long-term survival.

Summit Midstream Partners Press Releasee

For the fourth quarter, the company had adjusted EBITDA of $75 million and DCF of just under $40 million. FCF was just over $20.4 million. The company connected 77 wells, with annual well connections of more than 300, although natural gas prices remain quite weak, especially as we enter the summer when demand is weaker. The company is working on de-bottlenecking ventures, and new ventures.

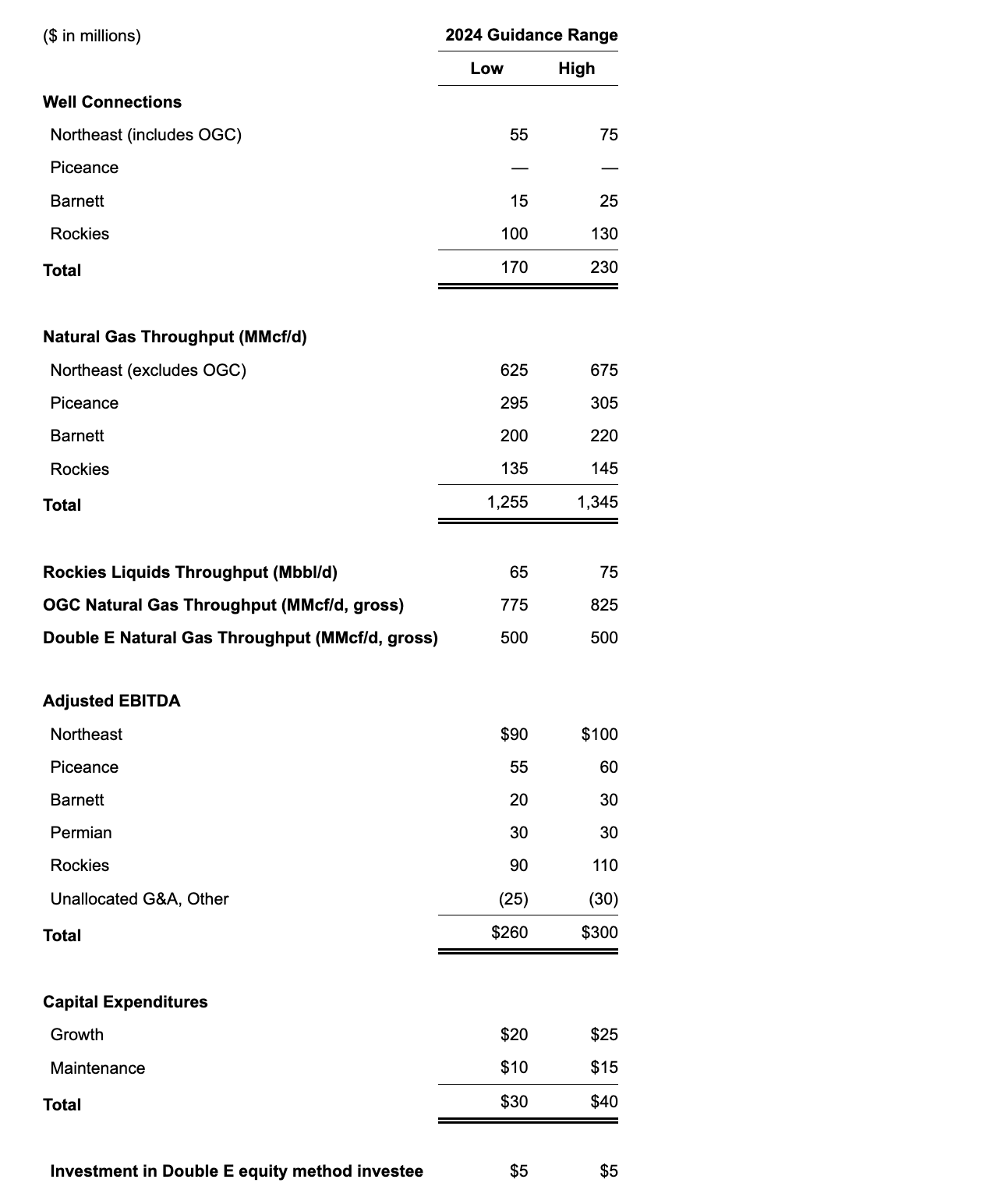

There are some huge wins. A new dedication acreage behind the Ohio Gathering Joint Venture is incredibly impressive. A 10 year take-or-pay contract behind Double E is enormous for the company's success. The company's 2024 EBITDA guidance is $280 million, ~5% above 2023, and strong performance for the company.

The company's focus is on maintaining what has been incredibly volatile volumes after weakness.

Summit Midstream Partners Press Releasee

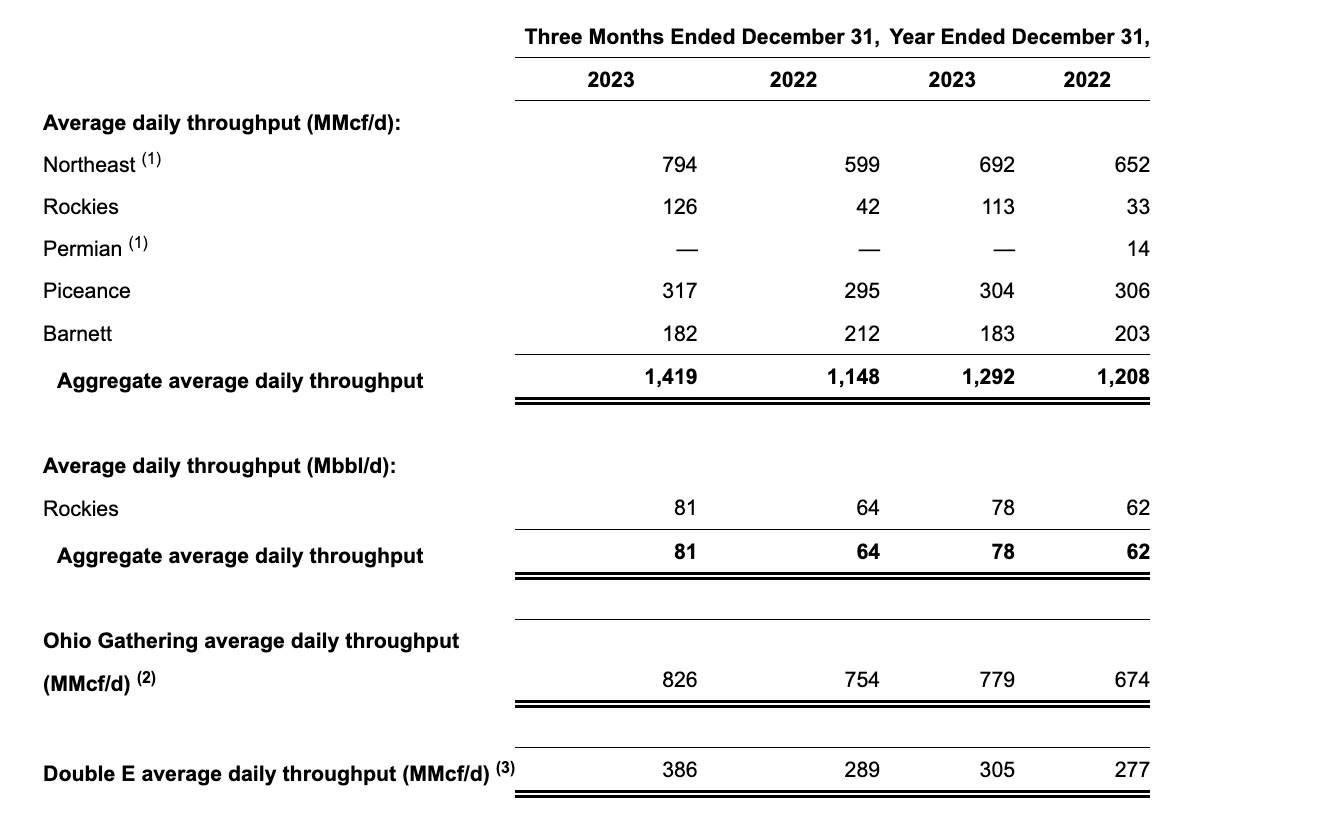

The company saw strong volume improvements alongside key areas in 2023. Specifically the company saw strong volume improvements in its key northeast segment. Rockies volume also increased dramatically as it become profitable once again. The company's only volume decline was in the Barnett, but overall volumes increased by strong double-digits.

The Double E also saw a strong increase in volumes going into the back half of the year. The Ohio Gathering system saw double-digit increases, and saw a new gathering system added. That will help overall strength in these segments going forward. These volumes show the company's continued portfolio strength.

The company's financial picture has improved dramatically quarter over quarter.

Summit Midstream Partners Press Releasee

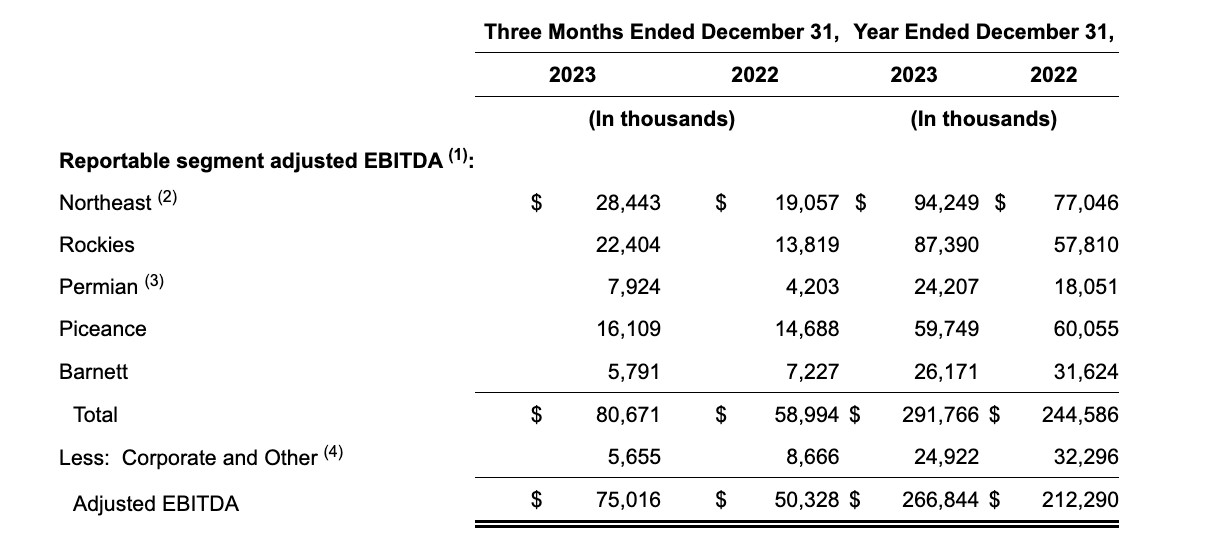

The company's quarterly adjusted EBITDA increased by more than 50% YoY, and the company's year EBITDA increased by more than 20%. The company's current guidance for 2024 is a less than 10% EBITDA increase, but it's still a slight decline from how strongly the company finished the year. However, the company's 2024 guidance indicates that that could decline slightly.

Still, the company managed to beat it's prior guidance. We remain optimistic that the company will come in and the higher end of its guidance.

Summit Midstream Partners Press Releasee

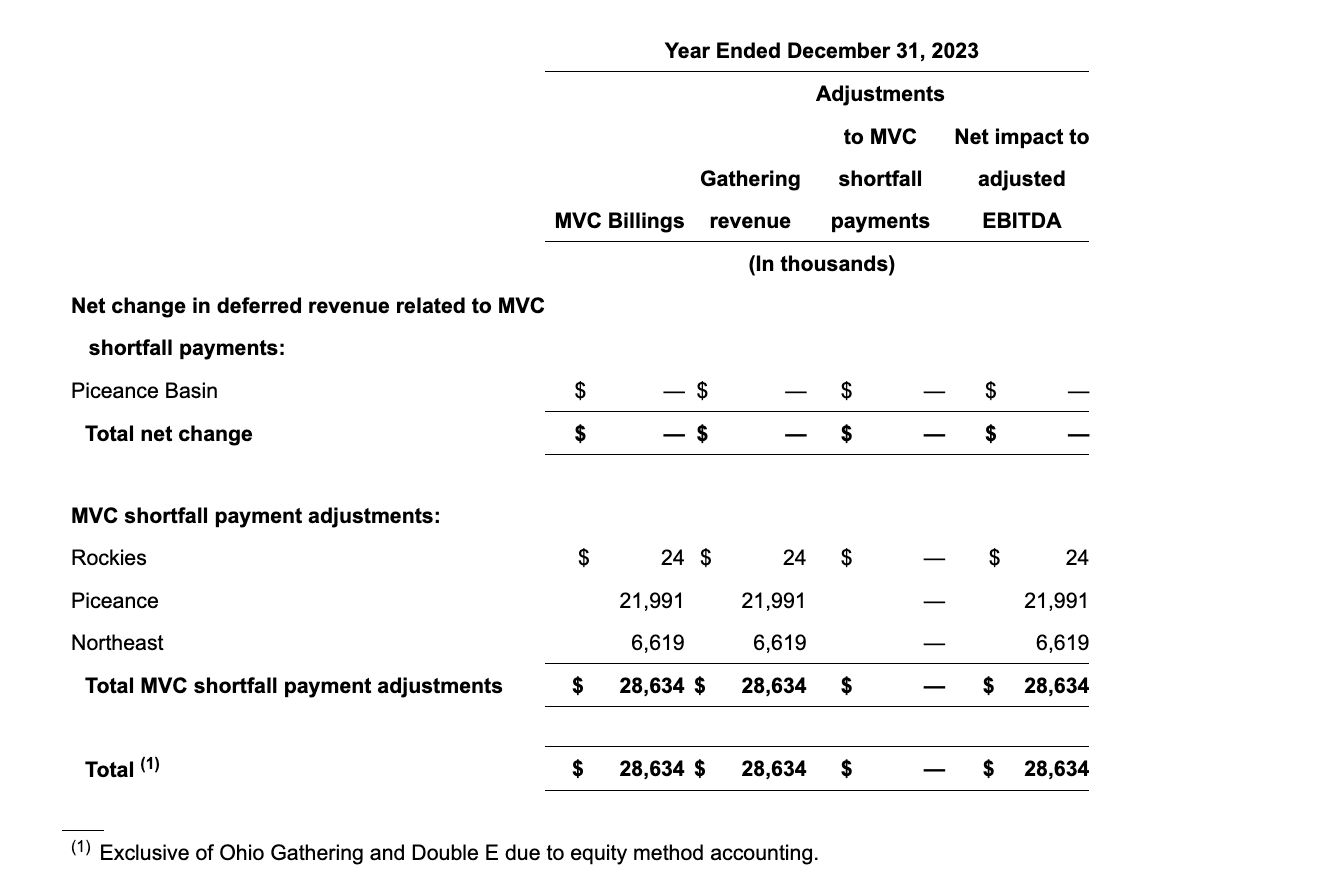

A concern within the company's portfolio is MVCs, particularly in Piceance. These are costs for customers not meeting minimal volumes, which is almost $30 million per year, almost $22 million of which is from the Piceance. No company wants to pay MVCs, it's based on a contract that they signed at a different time.

At some point the contract will end and the MVCs will go towards 0. That will hurt Summit Midstream Partners. A strong environmental improvement is needed to change this in pricing. The company's overall financial picture and its cash flow remain quite strong.

The company's outlook is for continued success in its portfolio.

Summit Midstream Partners Press Releasee

Piceance continues to show no well connections, which explains the MVCs. The company's guidance right now is for ~200 well connections, a 30% decline from 2023, and a concerning initial guidance. However, with current prices, that's not particularly unexpected. The company's well connections at the end of the day is based on natural gas prices and their strength.

The company expects at the middle of its guidance a ~10% decline in volumes, another sign of weakening prices. Still capital expenditures will be more than manageable and volumes will come in strong across the company's segments. That outlook indicates that the company will likely continue to generate strong cash flow.

The real question here is the company's debt.

The company has almost $1.4 billion in debt costing it more than $100 million in annual interest. That is dramatically hurting the ability to generate shareholder returns. The company's shareholder returns could be more than its market cap assuming it had no expenses. The company's debt comes due starting next year.

The company is obviously directing its DCF to drive returns, but with $150 million in annual DCF, it can only do so much. That means by the time this debt is all due, the company can pull its debt to below $1 billion. However, current interest rates and how they change versus 2 years ago, depends on the company's ability to refinance.

That's because if the company's DCF doubles, it no longer has any extra cash to pay down debt. We thing this is unlikely given current forecasts for interest rate cuts. The company's interest rates are at 8.5% and if it can show an ability to pay down debt, a 1% lower rate could save $20+ million in interest. We think there's a ~20% chance the company goes bankrupt.

However, given cash flow and upside, the investment is still worth it.

The largest risk to our thesis is refinancing. There's no doubt that Summit Midstream Partners will have to refinance its debt. With changing interest rates and continued uncertainty in the crude markets, the company might not be able to refinance its debt, or interest obligations might be so high that the company gets trapped.

That combination could result in bankruptcy or a slow debt for the company. The company's management is doing the best they can, but there's no guarantee their strategy pans out.

Summit Midstream Partners is an incredibly risky investment. The company has so much debt, with the associated interest rate expenses, that even an increase in interest rates could push it into bankruptcy. However, the company is doing the best it can, attempting to repurchase its debt at a discount or pay it off.

Still, even in a low natural gas price environment, the company is improving its portfolio and doing well. The next two years will be intense for the company. The company is predominantly reliant on the markets. If it can survive though, it can generate strong shareholder returns, making the company a valuable investment.