jiefeng jiang

jiefeng jiang

The VanEck Semiconductor ETF (NASDAQ:SMH) has demonstrated remarkable performance, with a year-to-date daily total return of 31.03% and a 1-year daily total return of 81.45% as of March 22nd. SMH’s success can be attributed to its significant holdings in leading semiconductor companies, particularly Nvidia (NVDA) and Advanced Micro Devices (AMD), which have been at the forefront of the AI chip market. Nvidia, with a 20.90% weight in SMH as of the time of this writing, has been a standout performer.

However, the semiconductor industry (particularly Nvidia and AMD) is starting to see increased competition, which could lead to negative effects being born on SMH. When looking at this ETF's valuation, I believe the two biggest things to be considered are the historical compound annual growth rate (CAGR) and the potential for mean reversion.

Given the rapid growth and now increasing competition in the AI industry, a mean reversion of Nvidia stock (as a result of higher competition) is becoming a major concern for me, which would significantly impact SMH due to its large allocation to Nvidia.

Given this, I believe SMH is a hold until the ETF can diversify away from heavy allocations. I am bullish as a whole on many of the companies inside SMH, just not in the asset allocation that the fund manager has decided

The SMH ETF, which tracks U.S. semiconductor stocks, has seen an increase in performance in recent years, particularly due to the rapid advancements and growing popularity of AI technology. With the adoption of AI technologies, major companies such as Nvidia and Advanced Micro Devices have shown to be key players in the market. SMH possesses significant holdings in both of these companies; as of March 2024, NVDA comprises a significant ~21% of SMH, while AMD makes up 4.49%. Due to this, Nvidia and AMD’s strong performance can be reflected in the performance of SMH. Nvidia and AMD are large contributors to SMH’s performance, but they aren’t the only ones. The SMH is composed of 23 other companies, adding up to a total of 25 semiconductor companies.

Some of the others major contributors include Taiwan Semiconductor, (TSM) which stands at a 12.14% allocation, Broadcom (AVGO) at 7.42%, and ASML Holdings (ASML) at 4.94%. Technically, when looking at the SMH holdings list, AMD is actually the 7th largest holding. Later on in the article I will explain why AMD matters so much.

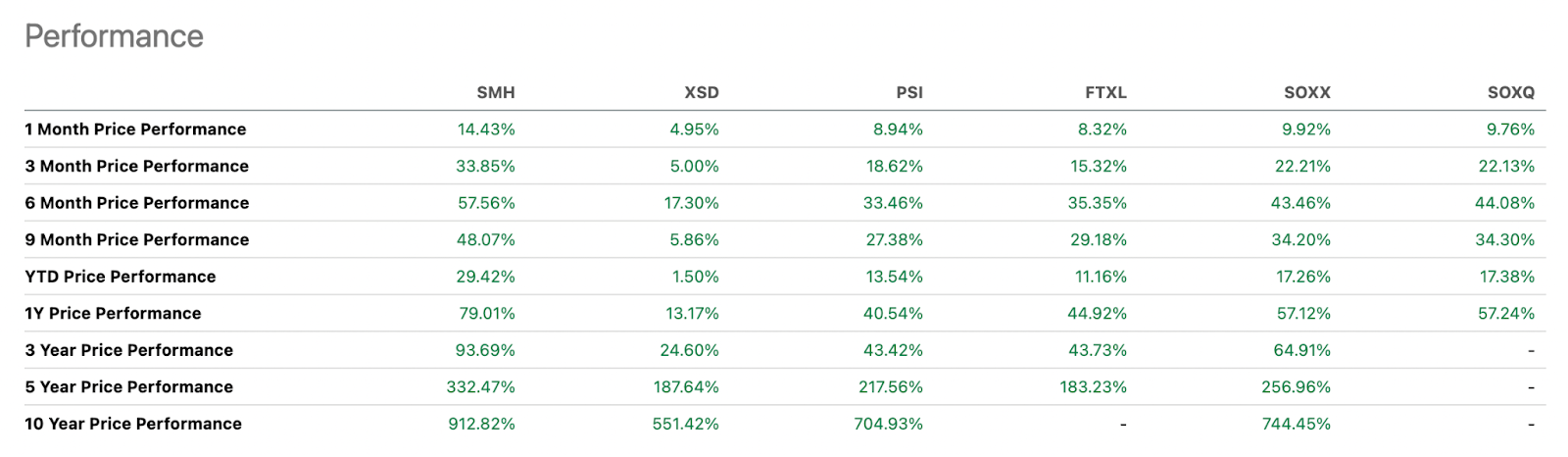

When looking at SMH's performance in 2024, the semiconductor ETF has generated a return of 29.42% and a 1-year daily return of 79.01%. These numbers match the broader success in the semiconductor industry, where SMH stood out with a trailing 79.01% 12 month return, outperforming many of their peers.

SMH ETF Performance Comparison (Seeking Alpha)

Although both NVDA and AMD contribute to the success of SMH, this contribution is uneven, with a majority of the positive impacts coming from its larger holding in NVDA. The implications of their uneven performance is something I’ll dive into later in this article.

As I mentioned above, Nvidia and AMD are some of the biggest players in the GPU industry, particularly in the AI chip market, where they have been direct competitors. This direct competition is exactly why I am focusing on AMD: these two companies interacting showcase the risks associated with competition within the market on future margins.

In 2024, AMD's MI300 series entered mass production, challenging Nvidia's dominance in high-performance computing for AI. Nvidia is responding by upgrading their product line, planning to launch new products like the B100 and GB200 chips (on top of their recent launch event this past week), which will utilize TSMC’s 3nm process. This competition is driving both companies to push the boundaries of chip performance and efficiency, benefiting TSMC as it secures orders from both companies to meet the growing demand for AI chips.

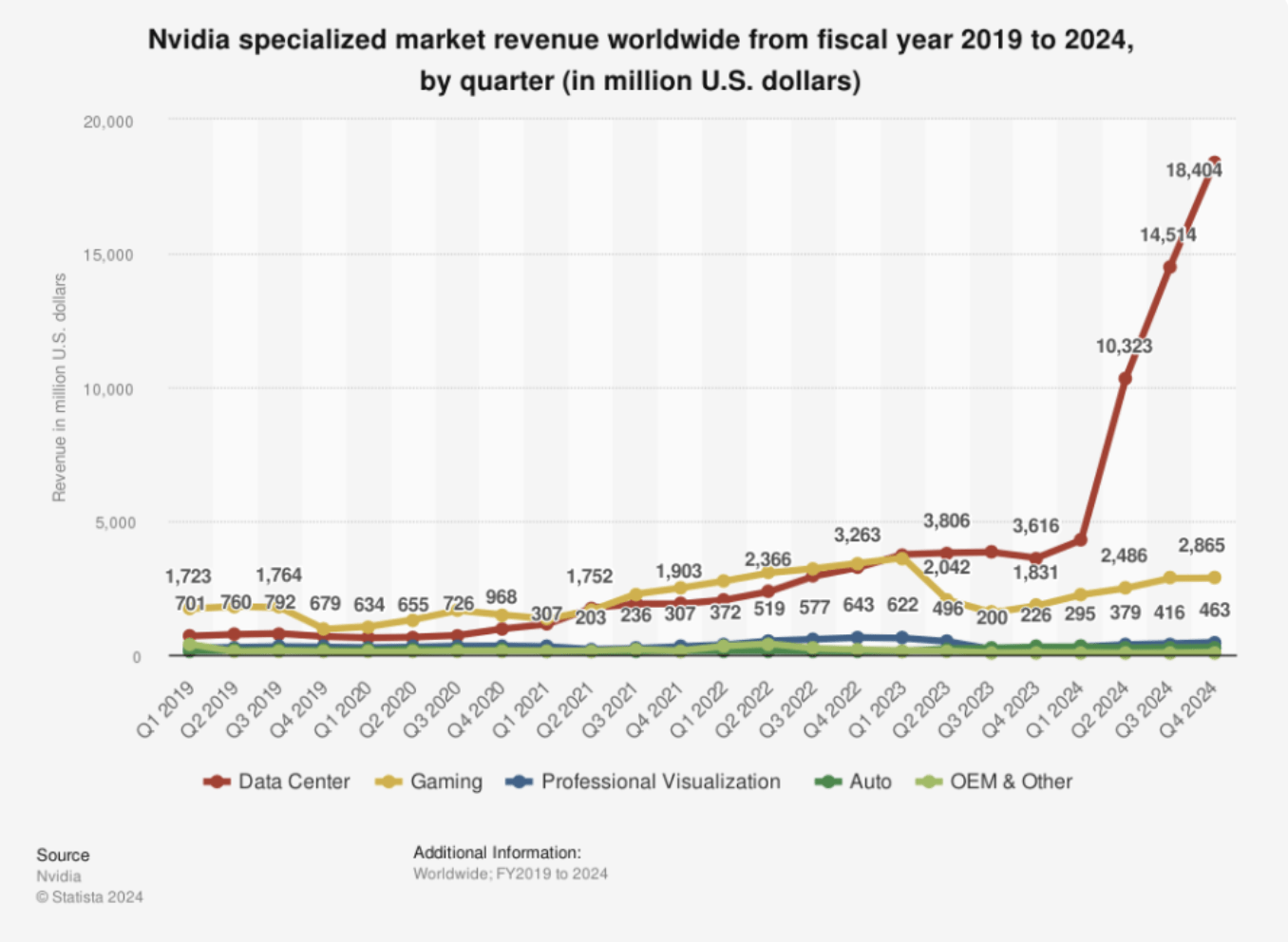

Nvidia has historically led in the AI chip market, with significant revenue growth in their Data Center segment, which includes AI chips. In FY Q4 2024, Nvidia's Data Center revenue reached $18.4 billion, far outpacing AMD and Intel. This revenue has exploded compared to other divisions.

Nvidia Division Revenue By Quarter (Yahoo Finance/Statista)

To further emphasize Nvidia’s outperformance to competitors, in the fiscal year ending FY Q4 2024, the comparable trailing 12 months net income margin for AMD was 3.77%, but NVDA stood at 48.85%, which is 12.96x greater. On top of this, in the 2024 fiscal year, their FY Q4 2024 GAAP gross margins hit 76%, increasing from the same quarter in the previous year, where they stood at 63.3%. However, in the attempt to keep up with NVDA, AMD has developed the MI300X chip which consists of a large memory capacity. While Nvidia continues to hold a dominant market share in AI chips, AMD's advancements in this area suggest a heating competition that could affect market dynamics and innovation rates. This environment may lead to reduced margins over time as companies invest heavily in research and development and possibly engage in price competition to capture or retain market share.

Nvidia actually alluded to this in their most recent conference call:

Similar to Q4, Q1 gross margins are benefiting from favorable component costs. Beyond Q1, for the remainder of the year, we expect gross margins to return to the mid-70s percent range.

It’s a small drop, but reminds us that their margins are incredibly high right now. Usually this means these margins can go down. If Nvidia’s stock price goes down, this could seriously impact SMH.

So far in 2024, SMH has performed well, with a year-to-date return of 31.03% as of the time of this writing. However, I believe this performance must be evaluated in the context of the fund’s historical compounding rate (OTC:CAGR).

Historically, SMH has shown impressive growth, with a 10-year CAGR of 24.36%. As I mentioned, currently a large portion of SMH is Nvidia. With this, Nvidia has been performing very well up 90.70% YTD.

I believe Investors should be cautious over concerns over mean reversion to the normal long run CAGR (the fund has done a whole year’s worth of performance in just 2.5 months).

As part of any fund seeing mean reversion, there could be heightened volatility. We saw this already on March 8th, their share price faced an intraday reversal of roughly ~7% (much of this was due to Nvidia).

We all know in the past 12 months, the AI GPU industry has seen insane growth and increasing demand. Throughout this process, Nvidia has powered the growth of this ETF as their business has multiplied as a result of incredible GPU demand. This can work in reverse, however, and is the source of my caution.

To emphasize, I do not think the long run trend for AI is lower from here. I certainly believe that the power of LLMs will bring massive growth to the AI GPU space, I just think competition will follow it.

As competition rises, it would not be unlikely for us to see a price drop in Nvidia and with it SMH. It is important to keep in mind how heavily a Nvidia dropoff could affect SMH.

Nvidia's value in the AI market is growing, with their data center’s AI computing target market projected to reach $250 billion annually. While I am arguing that increased competition will cause Nvidia to capture a lower market share of the growing market than they currently have, I do recognize that Nvidia has been able to maintain an immense market share in the AI GPU space (some estimate it to be over 70% market share). If I am able to see reasons that make me believe Nvidia will be able to maintain this market share (and margins) then I may definitely turn bullish on SMH (and Nvidia itself -I’m currently a hold on it too).

On the other hand, if the fund manager decides to reduce their holdings of Nvidia, I could also become bullish on the ETF. For example, SOXX has Nvidia only at a 9% allocation in their fund. I think this is a more fair representation of where an allocation should be. A 9% allocation allowed the fund (and the fund manager) to benefit from the upside should Nvidia continue to head higher, but also helps to limit the downside if Nvidia stock suffers from mean reversion in its performance, or competition heats up like I think it will.

For the VanEck Semiconductor ETF, their collection of semiconductor company holdings, reflects the dynamic and rapidly evolving nature of the AI sector and has allowed them and their investors to perform extremely well over the last 12 months. With holdings like Nvidia and AMD, major players in the AI Market, SMH has experienced an impressive year-to-date return and historical CAGR.

However, I am in the firm belief that as competition intensifies between these two companies, specifically Nvidia and AMD, risks will emerge to profit margins and market share stability impacting the heavy weighting the ETF has to Nvidia. With this, I am maintaining a hold position on SMH. If the fund manager diversifies and reallocates some of their holdings to other AI chip companies, I would be interested to reevaluate the ETF.