JHVEPhoto

JHVEPhoto

Celestica Inc. (NYSE:CLS) stock has gained as much as 3x its value from a year ago, and continues to trade near all-time highs. The company has consistently delivered positive quarterly progress, especially with its hyperscaler business’ continued capture of immediate AI opportunities. This has largely overshadowed CLS’ inherently elevated exposure to cyclical weakness in some of the core verticals of its Advanced Technology Solutions (“ATS”) segment.

Looking ahead, CLS remains well positioned to capitalize on AI-driven demand. The company’s hyperscaler-related revenue grew 32% y/y to almost $3 billion in 2023. And this secular tailwind is expected to persist through 2024. Reinforcements include resilience in industry capex prioritization towards AI infrastructure, improving supply availability, as well as start of productions at CLS’ newly expanded facilities in Thailand and Malaysia this year. This couples favorably with anticipated reacceleration in industrial end-market demand at its ATS segment, and a recovery in the troughed communications end-market at its Connectivity and Cloud Solutions (“CCS”) segment.

However, emerging tailwinds for CLS’ hyperscaler end-market and the improving outlook for its traditional core businesses in electronics manufacturing services (“EMS”) are netting out to a much lower extent of growth than what meets the eye. Management’s revenue guidance for 2024 remains unchanged from what was previously presented in November at $8.5+ billion, which implies only about 7% y/y growth. This also tracks towards CLS’ long-term target for 10% CAGR in revenue and earnings over the long-term, which potentially implies limited accretion to total addressable market, or TAM, from emerging AI opportunities.

Admittedly, CLS has done well on maintaining a growth mix that drives margin expansion. This is corroborated by a raised adjusted FCF guidance for the year from $175+ million to $200+ million, despite the maintained revenue outlook. But the combined growth and profitability metrics anticipated over the near-term continue to trail those of its AI peers (queue Nvidia (NVDA) and Super Micro Computer, Inc. (SMCI)) by wide margins, nonetheless.

We believe CLS’ latest hyperscaler momentum has put the stock on the map of AI “picks and shovels” contenders. And the incremental benefit from immediately available AI opportunities to CLS’ fundamentals through its hyperscaler exposure has provided a degree of differentiation from its lower-multiple EMS peers. This was likely what had encouraged CLS’ steep upsurge in recent quarters, lifting the stock out of its previous discount relative to peers with a comparable growth profile. While we believe there is still a valuation gap to close, driven by CLS’ underlying fundamental outlook, further upside ahead will likely slow.

Specifically, we like the characteristics of durability to CLS’ long-term growth and profitability trajectory. But the valuation gap between CLS and its peers with a comparable outlook has narrowed. This coincides with CLS’ inherent lack of outsized AI-driven growth exposure compared to current thematic winners in the market.

Looking ahead, we believe the core driver of CLS multiple expansion will revert from AI optimism back to its actual fundamental performance, which is durable, though modest. This is expected to bring forth a much more gradual realization timeline to its upside potential despite persistent AI market momentum, which also, inadvertently, subjects its valuation to higher execution and market-related risks ahead.

CLS separates its business into two primary segments – namely, ATS and CCS. The ATS segment primarily caters to solutions and components manufacturing for the aerospace and defense, industrial, healthcare, and capital equipment verticals. Meanwhile, the CCS segment primarily caters to enterprise and communications end-markets by providing offerings such as server and storage programs, hardware/software design solutions, and other customized IT services. Hyperscalers currently account for more than 60% of CCS revenues, highlighting where the AI opportunity for CLS primarily resides. Most are generated from sales to enterprise end-markets, while AI-related opportunities in the communications end-market are also picking up.

Specifically, CLS’ enterprise revenues showed strong acceleration exiting 2024 in tandem with “strengthening demand for AI/ML compute from hyperscaler customers”. As discussed in a previous coverage, the primarily driver of AI workloads is expected to gradually transition from training activity to inferencing, as newly deployed generative AI solutions go to market. Specifically, inferencing activity and related compute spending is expected to become double of training’s by 2025. And the urgency to build-out supportive infrastructure is growing, as evidenced by continued capex prioritization to AI developments at hyperscalers.

Data compiled by author

This accordingly highlights the strong demand environment for CLS’ enterprise business solutions, such as its server and storage programs, over the near-term. The persistent secular AI tailwinds also pair favourably with an emerging recovery in the communications end-market. Specifically, AI transformation at hyperscalers has also driven incremental demand for next-generation networking solutions capable of addressing the latency requirements and scalability of increasingly complex workloads.

This is a tailwind to CLS’ Hardware Platform Solutions (“HPS”) business, especially as AI compute demands usher in an upgrade cycle to 800G networking infrastructure. The impending 800G upgrade cycle, which promises more than double the data transmission speed of preceding 400G and 100G technology, coincides favorably with the ramp-up of CLS’ latest family of 800G networking switches. Specifically, the DS500 and DS4101 800G network switches introduced in Q4 are optimized for high-performance computing and AI/ML workloads. The next-generation networking solution, which likely commands a higher average selling price and better margin profile than its predecessors, is expected to reinforce CLS’ sustained long-term growth trajectory.

Yet on a net basis, CLS management is only expecting minimum total revenue growth in the high-single digit percentage based on their provided guidance of $8.5+ billion. This would represent slight deceleration from 2023, which reeled from declines in the ATS business.

The moderate pace of anticipated full year growth also implies steep deceleration in enterprise end-market revenue growth in 2H24. Specifically, management had guided enterprise end-market growth in the high-60% range for Q1, alongside a resumption of low single-digit percentage growth in the communication end-market over the same period. And through the course of full year 2024, management is expecting CCS segment revenues to grow in the low double-digit percentage range.

Let’s assume the moderate pace of communications end-market revenue growth persists through 2024, despite the favorable networking demand backdrop. Even under this stable scenario, enterprise end-market revenue growth would have to decelerate significantly from the high-60% growth range in order for full year 2024 CCS segment revenue growth to be in the low double-digit percentage range.

The conservative guidance comes at a time of improving industry supply availability, additional capacity at CLS’ Thailand and Malaysia facilities coming online later this year, and resilient capex commitment from hyperscalers to corroborate pent-up demand. Specifically, the initial phase of the CLS Thailand facility’s 100,000 square feet expansion is expected to come online in Q1, with the second face coming only in 1H25. This pairs with an additional 80,000 square feet of capacity in its Malaysia facility that will start coming online in 1H24. Despite these tailwinds, CLS’ anticipated performance potentially implies a much lesser exposure to AI-driven TAM expansion as compared to market’s favored thematic names.

In addition, CLS is also exposed to revenue concentration risk. Its top 10 customers currently account for more than 60% of its annual sales. And one of its key hyperscaler customers generated 29% of CLS’ total revenue exiting 2023, or 22% for the whole year. CLS has cited a strong, decade-long business relationship with the large hyperscaler customer, which it can leverage to further its AI market share. The hyperscaler’s co-investment in CLS’ capacity expansion initiative in Thailand also mitigates the company’s exposure to risks of significant revenue loss. However, this close-knitted business relationship could potentially be limiting CLS’ exposure to incremental arm’s length-driven AI opportunities in the hyperscaler segment. This could accordingly result in further risks of precluding CLS from optimizing AI-driven TAM expansion, and limit its market share gains and growth outlook in the long-run.

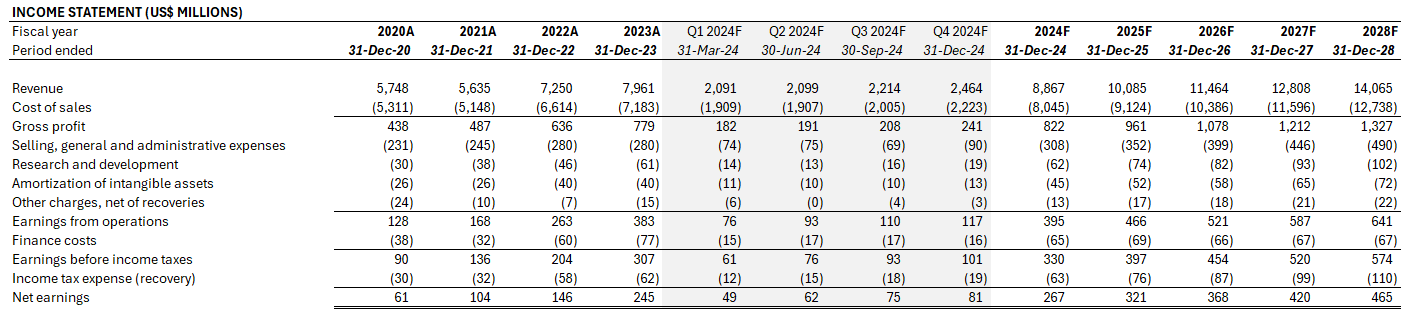

Taken together, we are forecasting total revenue growth of 11% to $8.9 billion for CLS. This is slightly higher than the base guidance of $8.5 billion provided by management, which we view as conservative and leaves room for upside surprise. However, this has likely already been considered by markets, given the average consensus revenue estimate is in a similar range of about $8.8 billion.

Author

Specifically, we expect ATS revenue to reaccelerate in 2H24, resulting in full year growth of 4% to $3.5 billion. This will be primarily driven by continued resilience in A&D opportunities, and an anticipated pick-up in the industrial and capital equipment businesses in 2H24 with new program ramps. Meanwhile, the CCS segment is expected to keep growing its share of revenue mix. We expect CCS segment revenue to increase by 16% y/y to $5.4 billion in 2024, which slightly outpaces management’s guidance for low double-digit percentage growth. This would also be favorable to CLS’ bottom line, given the CCS segment’s record margins exiting Q4 and continued benefits of economies of scale as new programs ramp.

Author

However, the anticipated results also imply CLS’ largest beneficiary of impending AI tailwinds – namely, its enterprise end-market – is headed for a drop-off in momentum. Admittedly, the incremental capacity coming online later this year should reinforce CLS’ capture of pent-up hyperscaler opportunities driven by AI developments, and offset the tougher PY compare facing 2H24. Yet management’s conservative guidance implies risks of normalizing demand in the back half of 2024 and/or potential capacity constraints to servicing incremental hyperscaler opportunities outside of its largest customer. Our forecast expects sales generated from the communications end-market to grow at 4% to revenue of $2.74 billion in 2024. Meanwhile, sales generated from the enterprise end-market is expected to grow at 32% to revenue of $2.67 billion in 2024, which implies significant deceleration through the year.

Over the longer term, we expect CLS’ revenue to grow at an annual average of about 10%, which is consistent with management’s goal. This is expected to further operating leverage improvements and margin expansion at CLS, and contribute to earnings growth at a 10% CAGR over the longer term.

Author

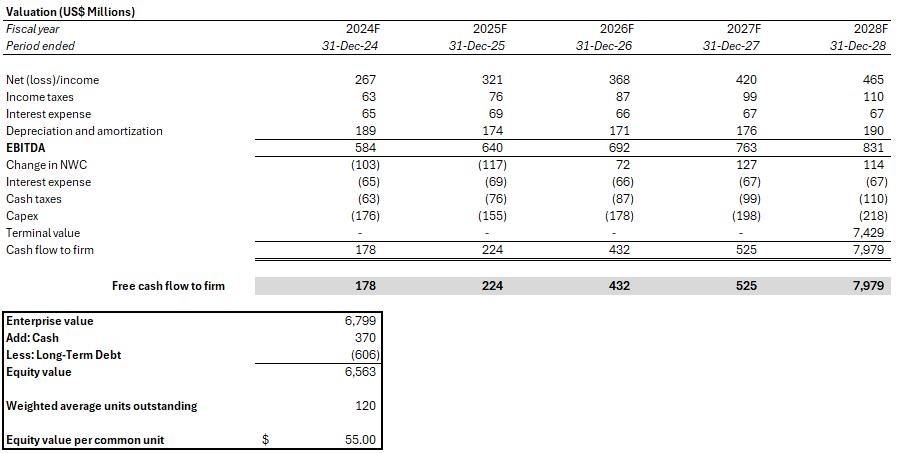

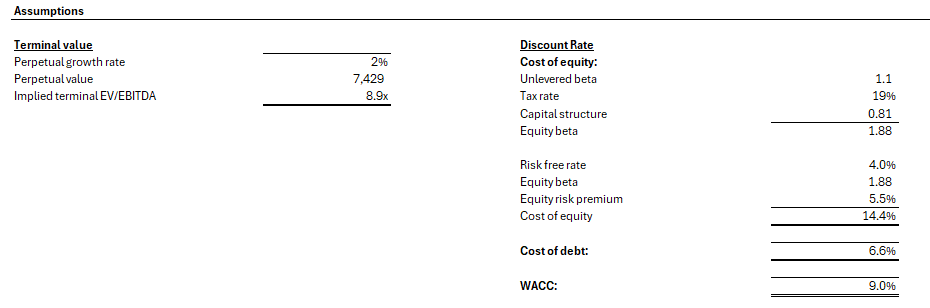

Our price target for CLS is $55, which implies upside potential of 28% from current market levels at about $43 apiece. The price is derived from a discounted cash flow analysis. The cash flow projections are taken in conjunction with the fundamental forecast above, and considers elevated capex spend through 1H25 to facilitate ongoing capacity expansion projects in Thailand and Malaysia. The analysis assumes a 2% implied perpetual growth rate on 2028E EBITDA to determine terminal value. This is in line with CLS’ stable growth profile, despite outsized industry momentum expected in the near-term. The analysis also applies a 9% WACC, which is in line with CLS’ capital structure and risk profile.

Author Author

Although our Celestica Inc. valuation analysis anticipates further upside potential in the stock, we expect CLS’ benefit from emerging AI momentum to soon normalize. Despite the combination of persistent tailwinds, such as incremental capacity to address pent-up hyperscaler demand and resilient industry capex spend on AI, CLS maintains a conservatively stable growth guidance. This could potentially cause CLS’ AI halo to fade on a relative basis to its picks-and-shovel semiconductor peers, as investors return focus to CLS’ moderate pace of hyperscaler market share gain, and demand consistent positive progress to justify valuation multiple expansion prospects. This would also increase CLS’ exposure to execution risks ahead, which could potentially bring the stock to trade back at its previous discount in the low-multiple EMS peer group.