designer491/iStock via Getty Images

designer491/iStock via Getty Images

Smartsheet (NYSE:SMAR) has been one of my top picks in the project and work management software ("PWMS") space for a while now. It's compelling valuation, expanding margins, transparent management, and large growth potential for its premium capabilities have been my main reasons why I preferred the stock. In addition, the growth rate of calculated billings showed a positive turnaround in the preceding Q3 quarter, which made me conclude in a previous article that it was a good opportunity to load up on shares.

The company's most recent FY24 Q4 earnings release proved me wrong as the long-awaited topline growth turnaround seems to be postponed. Billings growth slowed again, and management provided a very conservative sales guidance for FY25 mainly resulting from weakness in the SMB segment. It's no wonder that the share price reacted negatively to this as investors begin to lose patience.

I personally, continue to hold on to my Smartsheet investment, but with a little less conviction than before, which is reflected in my rating downgrade from Strong Buy to Buy. With recent events Smartsheet became a show me story, and it could take a few quarters until a visible turnaround in fundamentals could materialize. However, valuation levels are already quite conservative, which combined with good enterprise segment results, further improving margins and a low bar set for FY25 should provide a support for the share price.

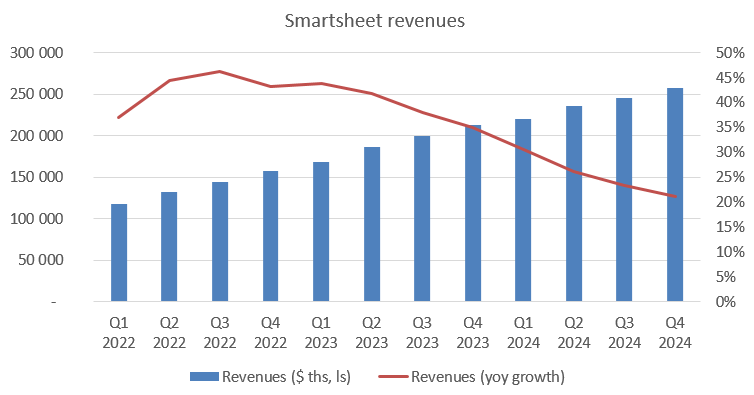

Smartsheet generated revenues of $257 million in its recently closed FY24 Q4 quarter, equaling a YoY growth rate of 21%, meaning a further slight slowdown from 23% YoY growth in Q3:

Created by author based on company fundamentals

This shows that after an exceptionally strong FY22 and FY23 the company continues to struggle with reviving topline growth. The main reason behind this trend is the continued weakness in its SMB segment, which makes up roughly 25% of revenues. SMBs have been hit by the recent high inflation environment and the resulting increase in interest harder, many of them trying to do more with less in order to stay competitive.

In the case of Smartsheet this can be evidenced by the significant difference between the dollar-based net retention rates (DBNRR) of SMBs and enterprises in the Q4 quarter. For SMBs the metric has tracked around zero, which means that ARR from existing customers in this segment stagnated yoy. Meanwhile for enterprises, the metric continued to stay over 120%, which shows that large customers continue to expand seats with Smartsheet just like management noted a few examples on the Q4 earnings call. The net result of these has been a companywide DBNRR of 116% for Q4, which is still good in my opinion in the current economic environment.

However, the bad news is that trends in the SMB segment worsened from Q3 to Q4 and management expects this trend to continue over FY25. Of course, Smartsheet tries to turn this trend over, for example by introducing a simplified pricing model and enhanced onboarding experience, but this could take time.

It's important to note at this point that weakness in the SMB segment doesn't seem company specific as competitors complained about similar trends as well. According to management the main driver behind this weakness is limited seat-expansions in the SMB segment as these companies tend to hire less in the still somewhat uncertain economic environment. Subscription cancellations without accompanying layoffs are not typical, which means that Smartsheet's platform remains sticky.

An important point where Smartsheet could enhance its topline growth is its cross-selling motion, which mainly consists of its premium capabilities extending the core project and work management platform. The most popular ones are Dynamic View, which enables personalized views for different groups of people, and Data Shuttle, which enables automated import from and export to data from other software systems. Currently, capabilities make up 34% of subscription revenues, but only less than 10% of Smartsheet customers use ate least one of them. So, there is a large runway for growth in here.

An important tool that the company introduced recently is self-discovery, which lets customers buy additional capabilities without direct contact with a sales representative. In Q4 more than $2 million of capability-related bookings resulted from self-discovery, which is more than double the $1 million in the previous quarters. In more than half of these deals the customer purchased a capability for the first time, which shows that the feature seems to be effective. In addition, until now only a limited number of premium capabilities have been available through self-discovery, which will change over the course of this year. Of course, it'll take time until these few million dollars of bookings turn into tens and hundreds of millions, but the start is encouraging.

This process will be reinforced by two new AI-related capabilities introduced by Smartsheet for general availability in FY24. One of them allows creating tailored formulas for specific problems, while the other one helps in interpreting customer data for creating text summaries. Since the beginning of February more than a third of enterprise customers utilized these solutions, so they're off to a good start.

Another important feature introduced in FY24 has been Smartsheet's free plan, which saw record conversion to paying customers in January with ~500 customers. This plan and the conversions to paid plans afterwards could be also important drivers of future revenue growth, but just like in the case of self-discovery the beneficial effects could take time.

Finally, Smartsheet has been working on a new platform design for months now, which is expected to be made generally available soon. Based on management comments this could be an important driver of sales growth as well, as there has been encouraging feedback from existing customers who trial the new view.

Based on these efforts I believe that Smartsheet is pushing hard to compensate for the growth slowdown resulting from macro headwinds, which could bear some fruit already this year. However, the real impacts of these changes will be felt over the longer term, which requires patience from investors over the short run.

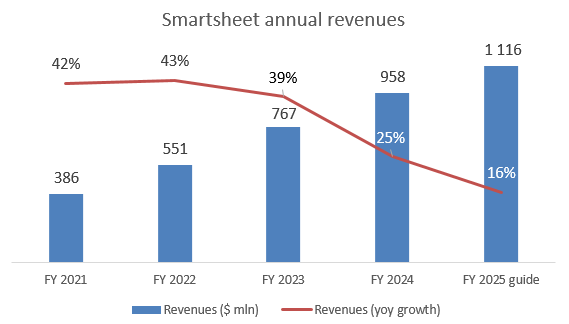

I believe Q4 earnings numbers haven't been the main reason why shares sold off after the release, it has been the quite conservative guidance for FY25, which disappointed investors. Management emphasized that they assumed continuing worsening in the SMB segment, while they didn't account for the potential revenue accretive effects of upcoming product announcements (e.g.: modernized view, extending available premium capabilities in self-discovery). With this, management has set a quite low bar for the upcoming quarters in my opinion, which can be seen in the following chart:

Created by author based on company fundamentals and estimates

The ~$1.11-$1.12 billion revenue guidance for FY25 implies 16% yoy revenue growth for this year, which would be a further significant slowdown from 25% in FY24. In times where more and more SaaS companies are on the verge of revenue growth reacceleration this doesn't seem encouraging.

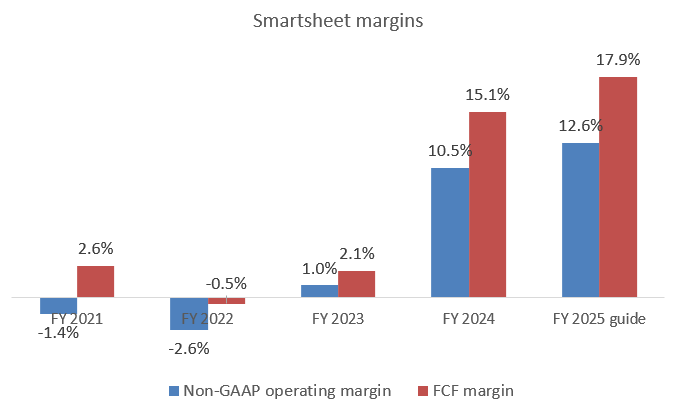

In return for slowing sales growth margins are expected widen over the year. This is positive, although not necessarily the ideal constellation expected from a growth company. Smartsheet is expected to generate FCF of $200 million resulting in a FCF margin of ~18%. Meanwhile non-GAAP operating income is expected to be ~140 million resulting in an operating margin of 12.6%. Both would mean continued improvement from FY24 levels:

Created by author based on company fundamentals and estimates

Based on this, I believe the situation of Smartsheet is much better than the recent share price performance would suggest. If improving macro conditions and the recently introduced new features help stabilizing sales growth around 20%, and FCF margin comes in somewhat better than expected Smartsheet could continue to be a Rule of 40 company in FY25 as well. In the light of this I believe the current valuation of shares reached overly conservative levels.

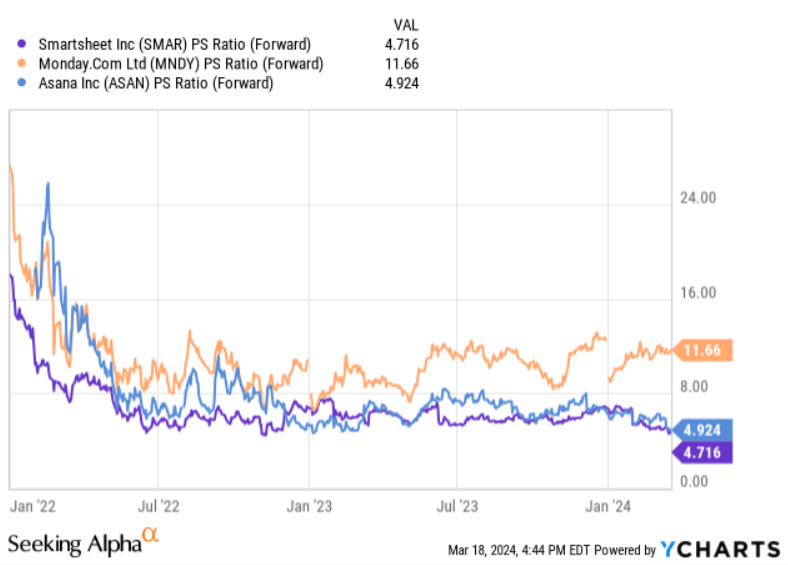

Despite continuing growth headwinds, the fundamentals of Smartsheet remain still stable. The company's 16-17% revenue growth rate guidance for FY25 combined with its 18% FCF margin forecast almost satisfies the Rule of 40 criteria. At the same time shares of the company trade only at a forward Price/Sales ratio of 4.7, which is not far from the U.S. market average of 2.3. Looking at the company's two main direct public competitors we can see the following:

YCharts

The market values the shares of monday (MNDY) significantly higher that the shares of Smartsheet, which I believe is exaggerated. It's true that Monday expects 27-28% yoy revenue growth rate for this year combined with 22% FCF margin making it a Rule of 50 company, but this doesn't explain such a wide valuation gap in my opinion.

The situation is even more surprising when we compare Smartsheet with Asana (ASAN). Management of Asana guided for 10-11% sales growth for 2024, while the company plans reaching positive annual FCF margin for the first time this year. So, compared to Asana, Smartsheet grows its revenues faster and generates significantly more free cash flow. In the light of this I wonder that the market values the shares of Asana slightly higher than the shares of Smartsheet. I believe this shouldn't last for long and Smartsheet shares should appreciate in order to close some of the large valuation gap to Monday, and to reflect the better fundamental setup than in the case of Asana.

Finally, there are some important risk factors worth considering when investing in Smartsheet's shares. I didn't mention it until now, but the CRO of Smartsheet is retiring after seven years at the company and will be replaced by Max Long former NetApp Chief Commercial Officer with decades of commercial experience. Transitions in executive positions are always a source of execution risk, so this should be monitored closely. However, as Max Long has also experience in leading sales roles at Microsoft (MSFT) or Adobe (ADBE) I believe he will succeed in bringing Smartsheet from $1 billion ARR to $2 billion soon.

Another important risk factor is the continuing slowdown in the SMB segment, which seems to affect the whole sector. It will be important to listen to competitors regarding this topic as well, in order to get a good grasp on how this situation evolves. Although the enterprise segment seems to stay strong, it's also important to keep an eye on large customer metrics before the weakness from the SMB segment would spread to this customer cohort as well. Recent product announcements and several greenfield opportunities in the enterprise segment should prevent a more significant growth slowdown there in my opinion, but it's important to monitor this closely.

Smartsheet tests the patience of investors, but I believe it's worth waiting. Valuation of shares has reached quite conservative levels, which in case of positive fundamental surprises should result in large upside for shares. Recent conservative FY25 guidance has set a low bar for the upcoming quarters, which should limit downside in my opinion. It's true, that Smartsheet became a show me story recently, but I believe the company will deserve investor's trust rather sooner than later.