pixelfit

pixelfit

SLR Investment Corp. (NASDAQ:SLRC) is a business development company that's been around since 2010. With a discount to NAV and a yield over 10%, it's another candidate for investment worth reviewing.

While I think the business is mostly sound, there are a few weaknesses I perceived that I wanted to discuss. Ultimately, I consider SLRC to be a decent Hold.

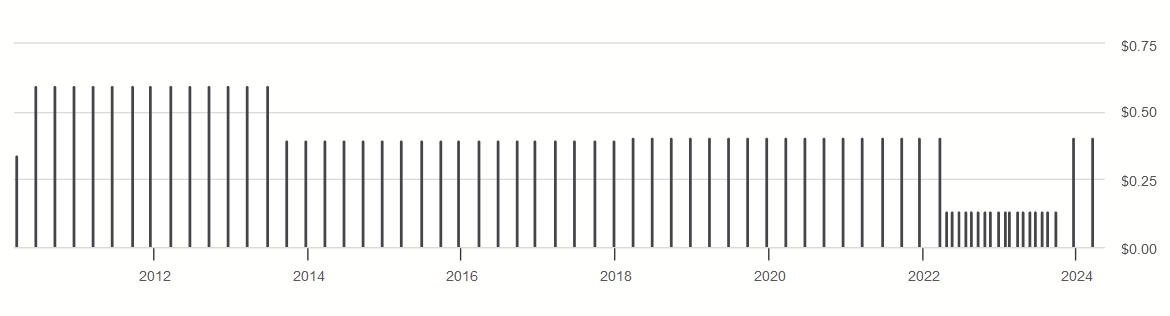

Since the dividend is the main component of a BDC's return, let first look at the history there.

Seeking Alpha

The company has usually paid quarterly dividends (before making the curious decision to do monthly distributions). The annual rate was stable over the past decade, but we can see that, just before that, the dividend was higher, being paid at $0.60 quarterly rates before being reduced to $0.40. What was the reason for this?

In a 2013 press release, they explained that this stemmed from the liquidation of certain investments, such that the capital was no longer producing yield. CEO Michael Gross was even quoted there as saying:

We believe the third fiscal quarter dividend approximates the run-rate earnings of our portfolio post these monetizations. We intend to seek to grow our investment income, and correspondingly our dividend, through the deployment of our over $500 million of available capital, which includes the proceeds from these monetizations.

Yet, clearly, that did not occur. It would be years before the quarterly dividend would increase to $0.41.

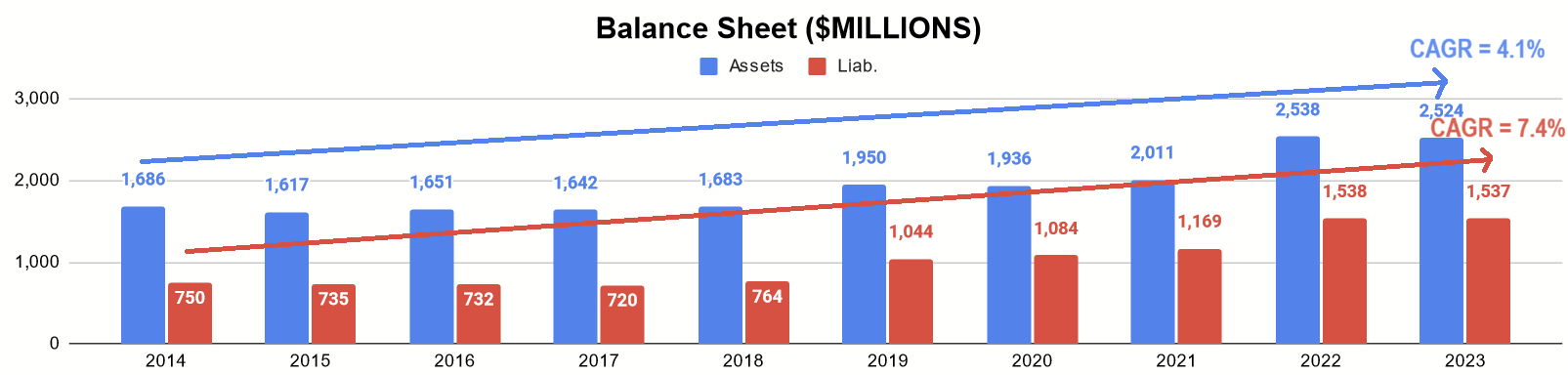

Interestingly, while BDCs with their high distribution requirements often have to sell more shares to raise capital for growth, SLR hasn't been doing that. Total shares stood at about 42 million for most of the past decade. Only in 2022 did they issue more (by about 12 million), as part of their merger with SUNS. The balance sheet has largely been grown by taking on long-term debt.

Author's display of 10K data

As we can see, assets only grew at a CAGR of 4.1%, while liabilities grew 7.4%. This has had the effect of decreasing the NAV per share over time, but the dividend has remained intact.

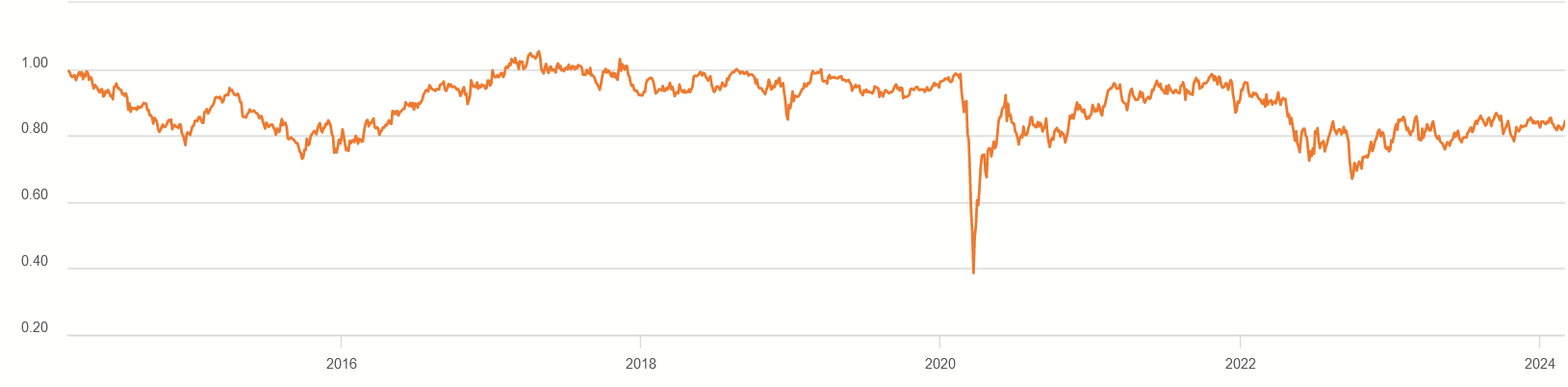

Prive/NAV History (Seeking Alpha)

The chart above shows how the shares have rarely ever traded above NAV, and the past year shows the most prolonged and steepest discounts to NAV in the shares' history, perhaps reflecting concerns that the NAV will continue to decline and, with it, the dividend.

Interestingly, the dividends did not increase as interest rates rose, which has been a common feature for BDCs and other lenders whose portfolios primarily hold floating-rate investments (like SLR's does). For example, 72% of their portfolio carried floating-rate interest in 2021 (2021 Form 10K, pg. 80), just before the hikes.

This can perhaps be explained by the loss they recorded on PhyMed, one of their larger investments (2022 Form 10K, pg. 72).

2022 Form 10K

It was one of their bigger holdings at the time. With a 16% interest rate, that was about $6M in interest income lost, which works out to about $0.11 of potential EPS. A dividend increase was possible as floating rates increased, but that is harder if principal is lost. 2023 also saw a $28M loss from their investment in American Teleconferencing Services.

It's worth noting that all of this data includes a series of mergers and acquisitions that occurred, which I'll go over as I discuss the business model below.

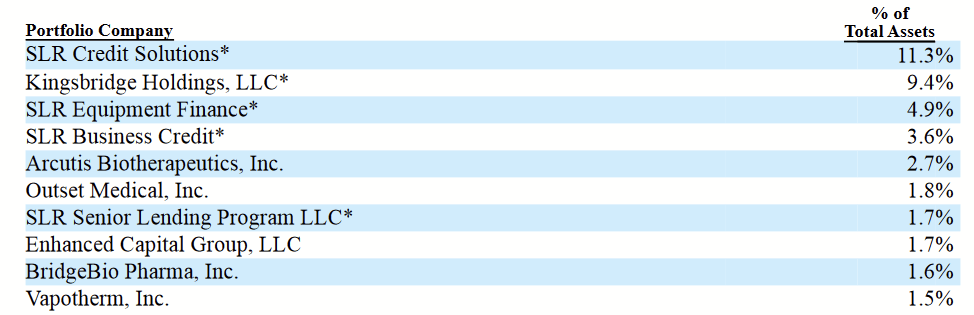

Overall, the company primarily lends to middle market companies, which SLR defines as those with revenues between $50M and $1B. Several of the top holdings in SLR's portfolio are subsidiaries of the company through which they do more specific categories of investment.

2023 Form 10K

It is, therefore, worth summarizing what each of those subsidiaries do and how they fit into the BDC structure.

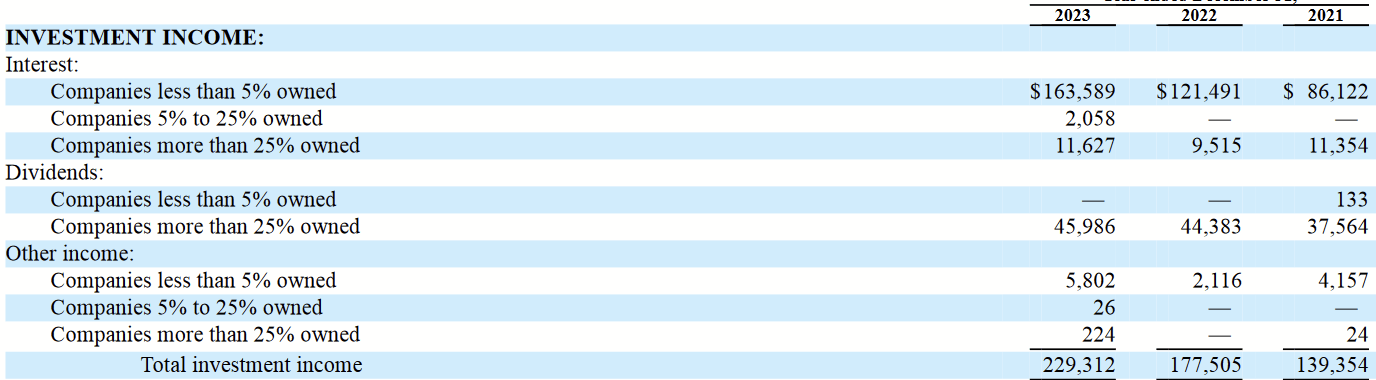

Because it's had so much M&A over the last decade, this is why a good chunk of their investment income is from dividends.

2023 Form 10K

In addition to the main company, these subsidiaries have their own debt and localized balance sheets. While I did talk about failed investments earlier, the limited liability for each of them would offer some protection to SLR if any of the subsidiaries performed especially poorly.

Through these subsidiaries and SLR proper, the Investment Advisor (SLR Capital Partners) generally seeks to make investments ranging in size between $5M and $100M. Senior secured loans are preferred for the safety they provide to principal. Middle-market companies are sought because they generally lack access to capital from more traditional lenders (who prefer larger, more liquid companies). This allows a BDC like SLR to underwrite with higher interest and more protective covenants.

The investment approach is very hands-on. Underwriting is done to fit the type of financing structure their borrower needs. Heavy due diligence occurs before capital is committed and afterwards. This includes on-site visits, monthly financial updates, and active coordination with borrowers in the successful execution of the project being financed.

2023 Form 10K

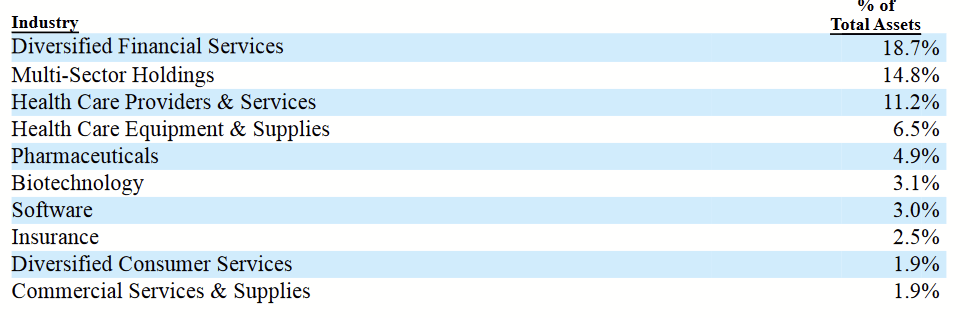

The portfolio's assets are diversified into 151 companies across many industries, but there are areas of concentration (financial services and healthcare). It's also helpful to look at how these investments are structured across the portfolio.

Author's display of 10K data

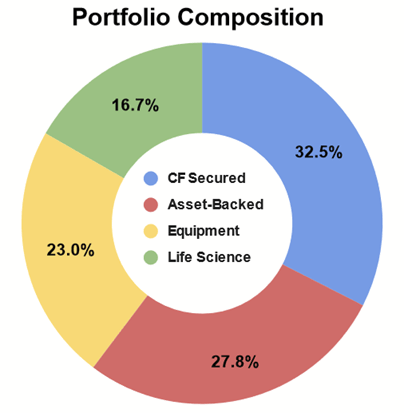

A majority of the investments are cash-flow secured or asset-backed. This still leaves sizable portions in equipment leases and life sciences funding (drawing from their different healthcare investments).

2023 Form 10K

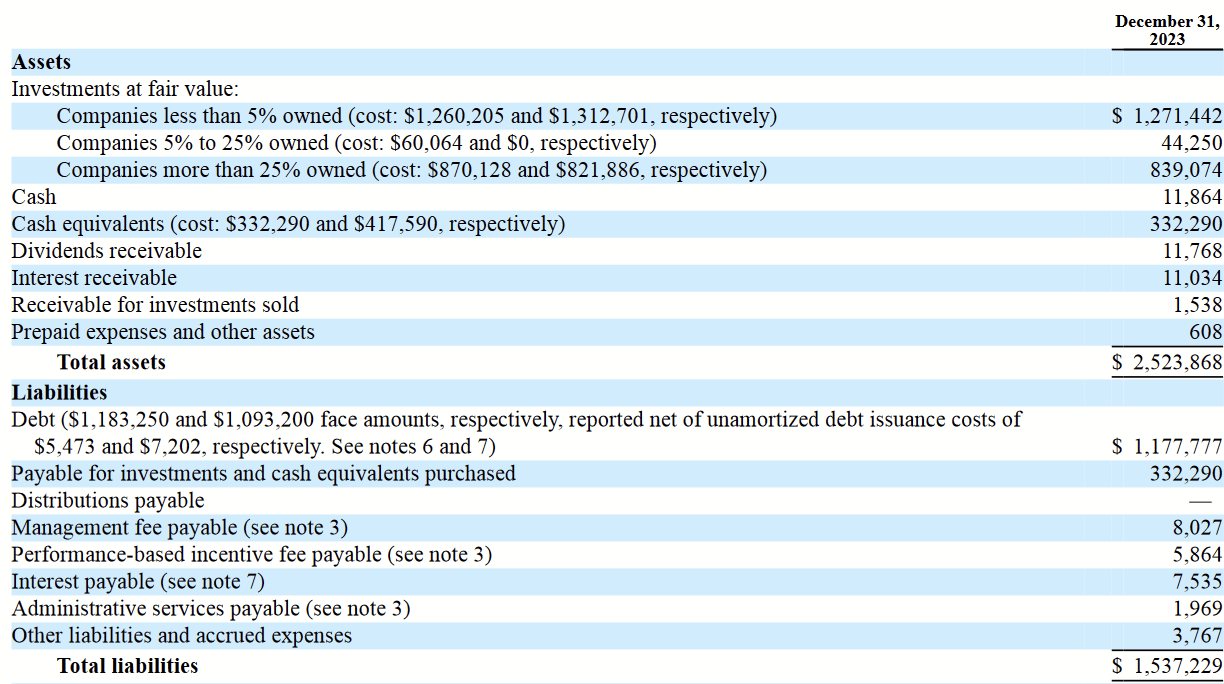

While I mentioned that the company increased leverage over the years, their asset coverage ratio is about 190%, while the law only requires them to cover 150%. Still, how is that $1.1B in debt broken down?

Summary of Debt (2023 Form 10K)

Most of this is debt drawn from the higher-interest credit facility. The unsecured notes (and these are many issues) bear fixed rates at less than 4%. Nearly all of it will be due in the next few years.

Since the dividend is going to be the main form of return for an investment like this, let's talk about what could impact that going forward. Most of this will be words of caution, and I don't want to fail to give credit where it is due. SLR successfully navigated COVID, supply chain disruptions, and inflation without having to cut their dividend so far. There's good reason to think most of the portfolio is fine. We still want to be vigilant, though.

SLRC's dividend did not rise as interest did, in spite of its mostly floating-rate book. We talked about the failed investments that contributed to that. That doesn't mean the dividend will continue to remain flat if rates decline. In fact, this is more likely, given the smaller number of assets after those losses.

2023 Form 10K

The company is kind enough to show us the impact of such decreases. Every 1% decline in SOFR on the current portfolio will reduce NII by $0.06 per share.

As the unsecured notes come due, which is a substantial portion of the debt, there is the question of how much of these will be repaid versus refinanced. Given that these were issued before interest rates increased, chances are that any new fixed-rate debt to replace this will come with a higher interest expense (the unsecured notes are all less than 4% currently), will which also hurt NII and potentially challenge the dividend.

SLR clearly has a specialty in equipment leases that you don't see with every BDC, and it seems to stem from the personal experience of the management and organic relationships that have formed. These aren't bad business opportunities by default, but there are some features that make them a bit riskier.

For one, the equipment is a depreciating asset. It's harder for them to retain the principal over time. Moreover, if such a secured asset is held, it's not easy to redeploy that capital like straight cash would be. Even unused, cash on hand can collect interest. Equipment can come with storage costs, by comparison.

SLR has yet to be severely hampered by these things, but little details like this can matter if other things (like a more distressed macro-environment) create problems for the company.

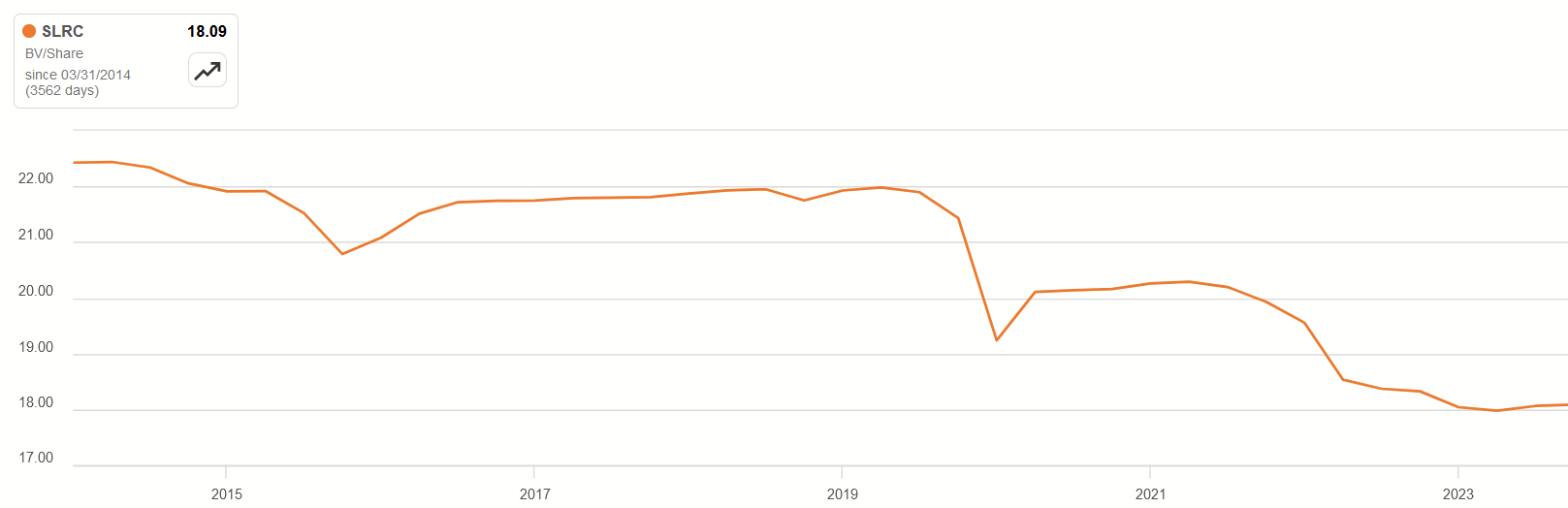

Earlier I discussed the history of the price of SLRC in relation to its NAV. What about the NAV in and of itself?

NAV Per Share History (Seeking Alpha)

Trading between $15 and $16 as I write this, SLRC offers a not-so-small discount to NAV. Yet, there seems to be a likely reason for the discount: it's been a trend of decline, considering my earlier discussion of how liabilities increased faster than assets. The market likely expects this trend to continue. While NAV and dividend payouts are not always perfectly correlated, a shrinking NAV could mean a balance sheet that could struggle to support a standing dividend.

I think investors should watch this carefully and perhaps ask for a bigger discount.

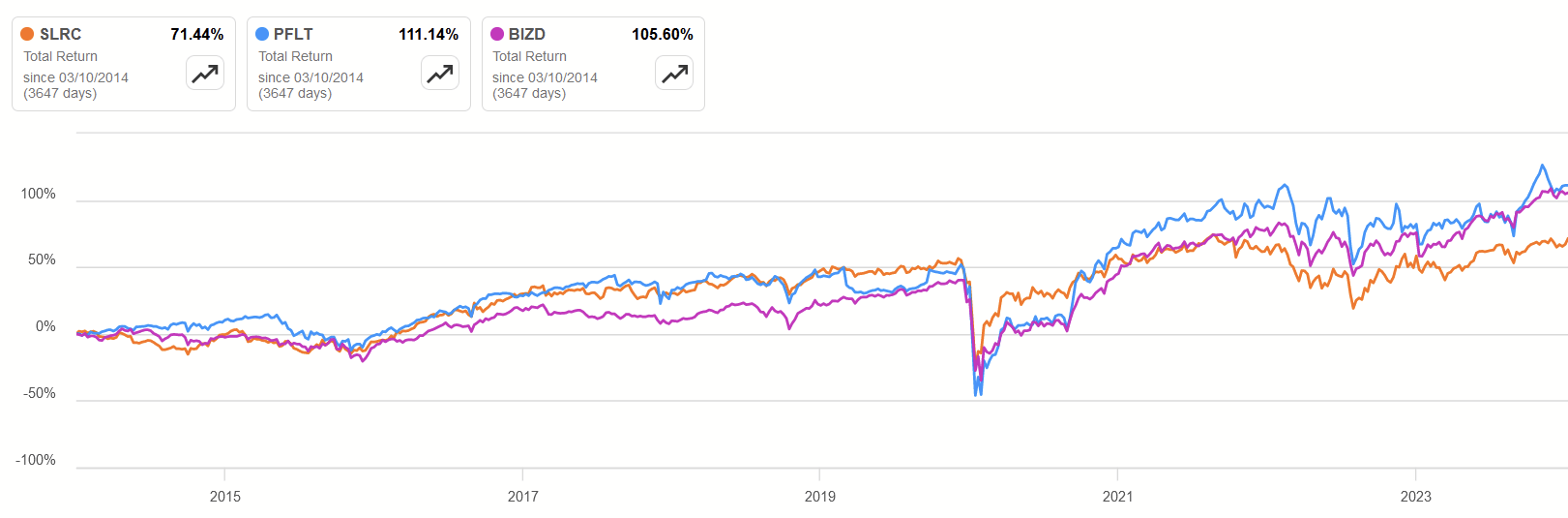

SLR Investment Corp has had a mostly successful history of distributing dividends to its shareholders. Over the past decade, it hasn't been cut at all. Yet, I think there are cracks in the armor and potentially some missed opportunities. Additionally, comparing its total returns to PennantPark Floating Rate Ltd (PFLT), a BDC that I like, and to VanEck BDC Income ETF (BIZD), a diversified BDC fund, we see that its total returns don't hold up as well.

Total Returns (Seeking Alpa)

Given these mixed results, comparative weakness, but the otherwise attractive yield over 10%, I consider SLRC to be a HOLD. Investors who already own it can still benefit from collecting its distributions, but I suspect that, if they look around, they can reinvest into alternatives with better risk profiles.