amenic181

amenic181

Fellow Investors,

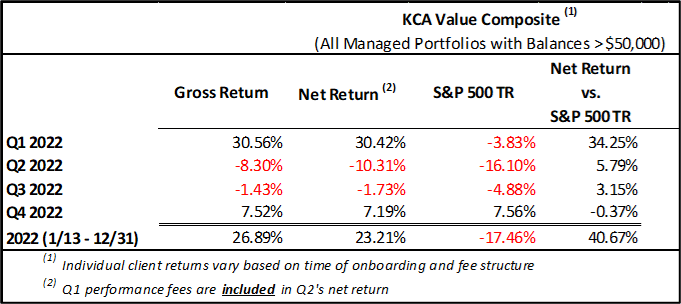

Kingdom Capital Advisors (KCA Value Composite) returned 7.19% net of fees in the fourth quarter, vs. 7.56% for the S&P 500 and 7.09% for the Russell 3000. The KCA Value Composite returned 23.21% net of fees since inception on January 13, 2022, over 40% outperformance when measured against the S&P 500.

KCA Calculations

We are pleased by our performance in 2022 (despite several missteps) and look forward to improving on our investment process in the year to come. It paid to be an energy investor this past year, despite oil and natural gas prices retreating from earlier highs. We own multiple conservatively run, well-capitalized, and cash flowing energy stocks and continue to expect strong results from them in 2023. We are also sifting through beaten-down consumer stocks trading at very attractive valuations. Similar to our energy investments, consumer companies with a history of strong capital allocation, strong balance sheets, and defensive positions are the most attractive.

As I reflect on our first year of professional investing, I’ve been struck by the mentality required to invest money with the goal of beating the market. Anyone can buy an index fund with no aspirations of outperformance and do quite well. However, investing to beat the market requires you to “beat” the person you are trading with over time.

This can manifest itself as confidence or arrogance, and the line is often blurred. Confidence is necessary to allocate capital, but arrogance provides no benefit. Confidence involves creating an investment process, identifying risks you can and cannot tolerate, and making allocations inside a framework. Arrogance adds a level of inflexibility we desperately seek to avoid, a mindset that prevents reasonable assessment of contradictory information.

We network with professional investors that think differently and invite them to challenge our ideas. We pitch ideas on Seeking Alpha, Twitter, and other investing blogs to encourage pushback on our assumptions; not because we enjoy harassment from anonymous internet personalities, but because we want to enter an investment having fully assessed the risks. We then outline “kill criteria” for each investment, events that would necessitate reducing/exiting an investment because the thesis is no longer intact. If we’re going to panic, we want to panic first.

This approach saved us from serious pain in 2022 and we will remain disciplined in 2023 as investments deviate from our expectations. We had several humbling experiences in 2022 with Dole (DOLE), Goedekers/Polished (POL), Soluna Holdings (SLNH), Alto Ingredients (ALTO), and other holdings that massively under-performed our expectations. It is likely we make future investments that don’t beat the market, but we will strive as we did in 2022 to avoid letting these destroy total returns.

Our portfolio is comprised of four main categories: 1) Core investments, 2) Special Situations and Short-Term Trades, 3) Hedging and Short Options, 4) Cash Holdings.

Core investments are long positions which we expect to hold for 12+ months and hopefully many years. This category is typically comprised of 5 – 7 equities and accounts for approximately 65% of the total portfolio.

Special situations and short-term trades are catalyst-driven investments which we anticipate holding for less than 12 months. This category is typically comprised of 8 – 12 equities and accounts for 22% of the portfolio.

Hedging and short options are used to remove specific event risk from core investments or protect the portfolio during major market moves. The category is typically comprised of 3 – 5 option positions and rarely exceeds 3% of the portfolio.

Cash holdings fluctuate throughout the year dependent on the quality of investment opportunities available. Cash holdings averaged approximately 10% of the portfolio throughout 2022.

KCA Calculations

Our outperformance was primarily driven by energy investments including Arch Resources (ARCH), Alpha Metallurgical Resources (AMR), Unit Corporation (OTCPK:UNTC), Pardee Resources (OTCPK:PDER) and W&T Offshore (WTI). Our best non-energy contributions came from Sysorex (OTCPK:SYSX) and A-Mark Precious Metals (AMRK).

ARCH, AMR, and PDER benefited from the resurgence of coal, specifically metallurgical coal pricing. In February, we highlighted in a Seeking Alpha article that ARCH appeared dramatically undervalued considering the surging price of coal, and we expected their management team to implement a shareholder-friendly capital return plan which was released shortly thereafter. The stock distributed over $30 of dividends per share in 2022, and significant repurchases of convertible debt and shares further supported the stock price.

UNTC chose to return capital via share buybacks, sold non-core acres from their production base, and grew earnings via their in-demand BOSS drilling rigs. UNTC practiced discipline by hedging their oil at $100 this summer and natural gas at $9 before pricing collapsed, partially offsetting much lower low hedges added when they emerged from restructuring in late 2020. We continue to view UNTC as one of the cheapest and best-capitalized E&P stocks in the market. To this end, on January 5th, 2023, UNTC announced a special dividend of $10 per share to be paid on January 31st. Additionally, UNTC will begin paying a quarterly dividend of $2.50 per share in Q2 2023.

WTI was our favorite trading vehicle, taking advantage of its volatile nature and gunslinging risk management department, to ride multiple >100% moves in the stock during 2022. WTI is a Gulf of Mexico E&P with a colorful CEO, no capital return plan, a valuable pile of reserves, and a slug of calls on the price of natural gas. We found this to be an exciting trade to express our belief in energy stocks, and a dangerous place to stay after sentiment peaks.

SYSX was highlighted in our Q2 letter as a terrible business that had a brief window of trading opportunity – a feature on their convertible notes allowed for the systematic dumping of common shares that was halted by a hard cap on the number of issuable shares. We took a small position when the cap was hit, more than doubling our investment in a few days, before closing our position and watching the stock implode once again.

Lastly, AMRK continues to execute and grow their direct-to-consumer bullion sales, breaking records during 2022 and building an impressive moat around their business. We significantly hindered our AMRK returns after buying calls in the first half of the year, correctly anticipating earnings beats but incorrectly expecting an increase in the stock price. The bullion market remains strong and AMRK continues making accretive acquisitions. We look forward to continuing to watch Management grow the business and create value for shareholders.

Our largest detractors were Dole Plc, Goedekers/Polished Warrants (POL.WS), and Semler Scientific (SMLR).

DOLE takes the prize as the single largest detractor on our performance, with the stock price finishing 2022 down ~33% from where we began buying. We made matters worse by adding some December 2022 calls early in the year that lost most of their value when Dole crashed below our expected floor for the stock price. Our confidence in Management was overshadowed by multiple headwinds, including negative currency impacts from a strong dollar, surging input costs, and lingering pressures from their salad recall in 2021. We still believe the assets far outweigh the current valuation, but Management’s unwillingness to address the floundering stock price via a buyback has limited recovery in the near-term.

The situation at Polished was an unmitigated disaster. The company has 1) refused to release financials since March, 2) conducted a five month investigation into undocumented warehouse workers and a CEO charging personal expenses to the business, and 3) was recently fired by their auditor and provided no update on their balance sheet, despite Company press releases that opaquely reference multiple signs of deterioration. The investigation revealed material problems; however, the pace at which the Board has disclosed (or not disclosed) information is inconceivable. We sold our warrants at a significant loss after losing faith in the Board.

Semler Scientific is a good business that declined rapidly in late 2021 and early 2022 as multiples compressed, offering a valuation we felt was compelling. Unfortunately, changes in the business during 2022, and Management’s shifting narrative, resulted in a steeply declining share price. We continue to watch the situation carefully for signs that the issues are addressed.

We continue to seek out patient investors interested in our actively managed small-cap strategy. Many investors remain hesitant given the macro deterioration and our limited track record; however, we look forward to further substantiating the advantages of our fund. We would welcome any referrals you deem appropriate.

In Q4 we continued actively posting our work to Seeking Alpha, publishing writeups on CreditRiskMonitor (OTCQX:CRMZ), A-Mark Precious Metals, Good Times Restaurants (GTIM), Express (EXPR), and The Children’s Place (PLCE). We won the Investor’s Podcast Stock Pitch competition with our A-Mark thesis, and we contributed two guest articles to Oddball Stocks Newsletter on core holdings Pardee Resources and Unit Corporation.

We appreciate you entrusting us with your investment in a volatile environment. Mike and I have invested most of our net worth with Kingdom Capital and we’ll continue to steward your capital as we do our own.

Sincerely,

David Bastian

Chief Investment Officer

This document is not an offer to invest with Kingdom Capital Advisors, LLC (“KCA” or the “firm”).

The statements of the investment objectives are statements of objectives only. They are not projections of expected performance nor guarantees of anticipated investment results. Actual performance and results may vary substantially from the stated objectives. Performance returns are calculated by yHLsoft, Inc. dba Advyzon.

An investment with the firm involves a high degree of risk and is suitable only for sophisticated investors. Investors should be prepared to suffer losses of their entire investments.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the firm described herein may differ materially from those reflected or contemplated in such forward-looking statements.

This document and information contained herein reflects various assumptions, opinions, and projections of Kingdom Capital Advisors, LLC (“Kingdom Capital Advisors” or “KCA”) which is subject to change at any time. KCA does not represent that any opinion or projection will be realized.

The analyses, conclusions, and opinions presented in this document are the views of KCA and not those of any third party. The analyses and conclusions of KCA contained in this document are based on publicly available information. KCA recognizes there may be public or non-public information available that could lead others, including the companies discussed herein, to disagree with KCA’s analyses, conclusions, and opinions.

Funds managed by KCA may have an investment in the companies discussed in this document. It is possible that KCA may change its opinion regarding the companies at any time for any or no reason. KCA may buy, sell, sell short, cover, change the form of its investment, or completely exit from its investment in the companies at any time for any or no reason. KCA hereby disclaims any duty to provide updates or changes to the analyses contained herein including, without limitation, the manner or type of any KCA investment.

Positions reflected in this letter do not represent all of the positions held, purchased, and/or sold, and may represent a small percentage of holdings and/or activity.

The S&P 500 is an index of US equities. It is included for information purposes only and may not be representative of the type of investments made by the firm. The firm’s investments differ materially from this index. The firm is concentrated in a small number of positions while the index is diversified. The firm return data provided is unaudited and subject to revision.

None of the information contained herein has been filed with the U.S. Securities and Exchange Commission, any securities administrator under any state securities laws, or any other U.S. or non-U.S. governmental or self-regulatory authority. Any representation to the contrary is unlawful.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.