Daniel Balakov/iStock via Getty Images

Daniel Balakov/iStock via Getty Images

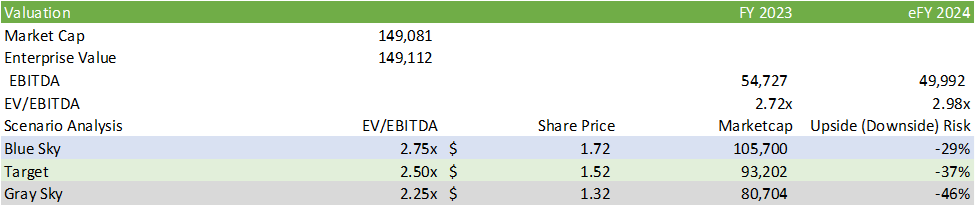

Journey Energy Inc. (OTCQX:JRNGF) is currently undergoing a major organizational transformation in which the firm will be cutting back on drilling activities, focusing capital investments on the utility business, and is actively managing the capital structure. I believe management may be biting off more than it can chew, as spinning up the gas-fired power plants are turning out to be more costly than initially projected and may become more reliant on outside financing as the firm reduces its primary source of income. I maintain my SELL rating with a price target of $1.52/share at 2.5x eFY24 EV/EBITDA.

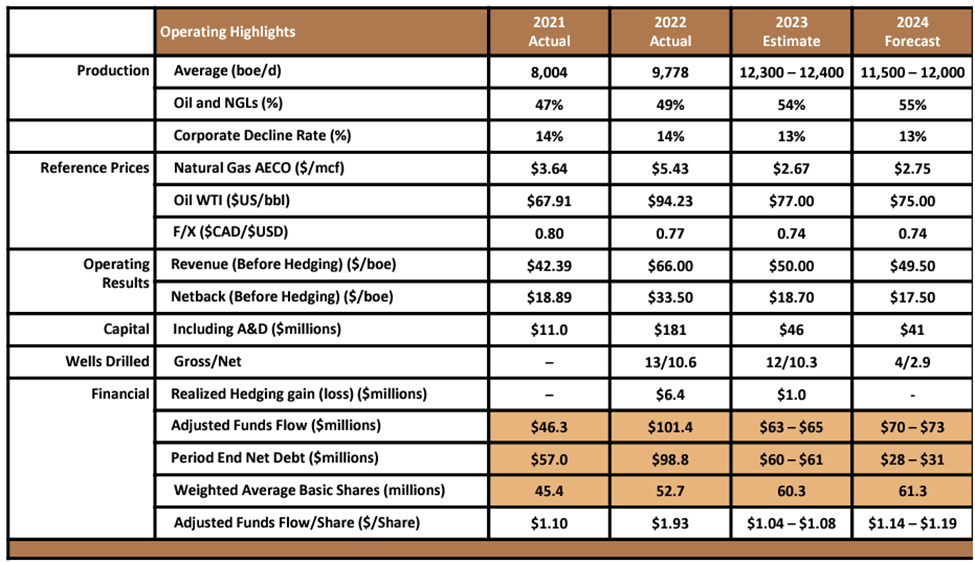

Journey Energy is currently undergoing an operational change and executing a drastic shift to their capital structure in an attempt to bolster free cash flow and to deleverage the balance sheet and free up capital. Management provided guidance of paying down $34mm of its outstanding term loan in 2024 and anticipates to generate between $70-73mm in adjusted fund flows based on $75/bbl WTI. In their Q4 ’23 earnings presentation, management denoted that they plan to increase pro forma production by 45%; however, management also guided down daily production to 12-12.4Mboe/d for eq1’24 and an average production rate of 11.5-12Mboe/d for all of eFY24, which I take as fewer net new wells being completed in eFY24 when compared to FY23, which had an estimated average production rate of 12.3-12.4Mboe/d.

Corporate Reports

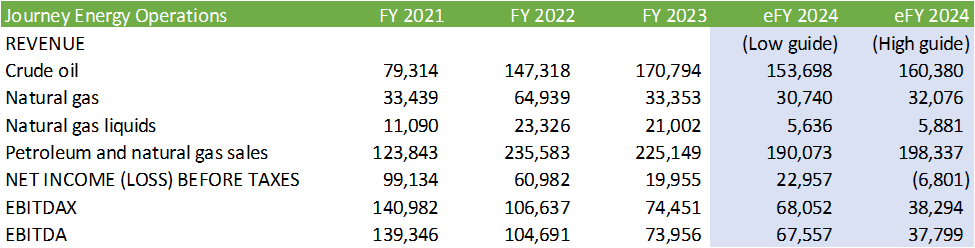

Looking at operations, the firm faced challenging comps in FY23 as their realized prices on an equivalency basis were -25% lower in FY23 vs. FY22. Natural gas faced the largest decline of -53%, oil of -20%, and NGLs of -30%. Journey also faced challenging price headwinds at their gas-fired utility with their realized price per MW declined from $241.25/WM in q4’22 to $95.16/MW in q4’23, resulting from warmer weather. As a result of this challenging pricing environment, management focused their attention to facility turnarounds. These pricing pressures trickled into Journey’s earnings as the firm faced a 7% decline in total revenue and an EBITDA margin compression from 52% down to 40%.

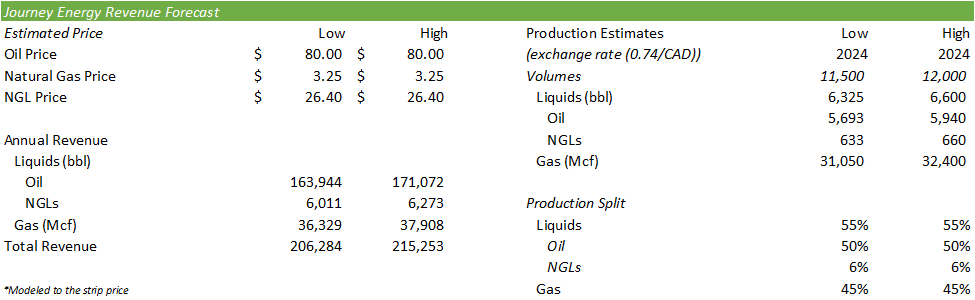

Looking at the CME strip prices for 2024, WTI appears to be priced (CL1:COM) on average at $80/bbl while Henry Hub natural gas is expected to remain below $2/Mcf through June 2024 before gradually climbing to $3.526/Mcf by December 2024. Building this into my forecast for eFY24, assuming liquids production is 10% NGLs based on the firm’s proved developed producing reserves and an average price of 33% of WTI, I forecast eFY24 production revenue to be in the ballpark of CAD$279-291mm, holding all else equal.

Corporate Reports

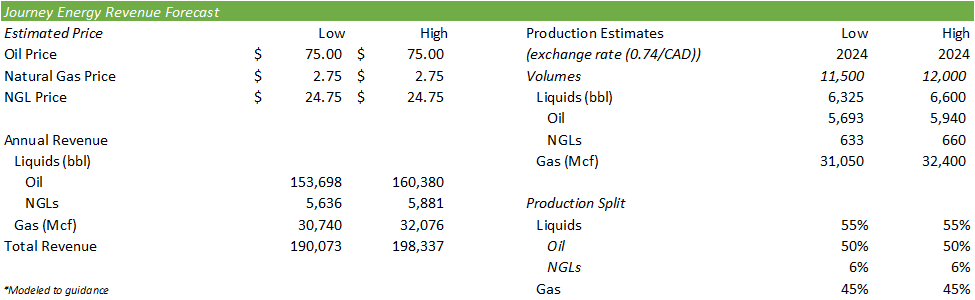

If, using management’s guidance at $75/bbl WTI and $2.75/Mcf natural gas, we can expect a continued decline in revenue generation at the wellsite of -16% at the low end and -12% at the high end of guided production.

Corporate Reports

In a flat oil market, I find it challenging to come up with a reason for management to guide production down for eFY24 other than to preserve oil in the basin, which Alex Verge, CEO, outlined in his presentation with Peter’s & Co. Management’s previous guidance for lower production was to emphasize spinning up their power generation. Accordingly, management’s plan is to refocus on the resource side of the business in eFY25. I do believe that this framework can create headwinds for the firm as O&G production is their primary cash flow generator and focusing efforts away from generating cash flow can lead to the firm having a need to fill that cash deficit with additional financing.

As management’s primary focus on the capital structure is to deleverage with these two operating factors in mind, Journey has been forced to get creative in financing the business. On March 5, 2024, Journey issued $38mm senior unsecured convertible notes with a share strike price of $5/share at a 4% discount. These notes have a 5-year duration and a rate of 10.25%. Given the share price route, these notes may be expected to mature in exchange for cash rather than equity with the assumption that the share price does not recover. Proceeds were reported to be used to pay down previously issued debt and to finance capital investments and working capital.

Corporate Reports

The firm is also ambitiously transforming operations more geared towards the utility side and anticipates bringing online ~31.6MW between their Gilby and Mazeppa power plants. According to their q4’23 report, Journey will invest $9.5mm in capital in 2024 in preparation for this new capacity. Mazeppa, on the other hand, was not provided with a start-up date and awaiting regulatory approval to restart operations. I believe Journey managing the two gas utilities will help the firm offset some of the price volatility for natural gas as the firm will more closely control the supply chain from production to utilization. The only variable component in this operating vertical will be midstream services and transport.

The business model is appealing: produce the gas and utilize it for power generation. I believe the utility can act as a hedge for Journey in which the firm can push to power generation in strong energy and soft gas markets and sell gas in strong gas markets and weaker energy markets. Though on paper this is a good idea, Journey has hit a few snags in spinning up their power generation business.

Reviewing Journey’s corporate filings, it appears that spinning up their utility power generation isn’t going according to the original plan. In their previous year’s guidance, 2024 capital spend for the Gilby plant was forecast to be $6.2mm and has since been increased to $9.5mm, a 53% increase from the previous guidance.

Management also updated the expected power generation and guided down on production from 15.5MW to 15.1MW. Though a slight reduction in expected power generation, Journey is faced with higher-than-expected capital investments paired with a lower-than-expected result. The good news is that the guided start date was maintained for q2’24. I believe that this will determine the viability of the utility business and whether pushing towards bringing online the Mazeppa facility will be financially and operationally feasible. Given that the Gilby facility is coming in over the originally forecast budget, I have reason to believe that the Mazeppa facility has the potential to be an even greater capital drain.

Given the stated discount to replacement value, I believe that Journey will uncover greater challenges in spinning up the facility than what is being voiced as slow regulatory approval. Overall, my negative outlook as originally presented in my report covering Journey Energy dated November 8, 2023, stands.

Though I do believe that this can create a unique opportunity for Journey if all goes according to plan, it is clear that this is not the case and that costs and start dates were not appropriately forecast.

I believe Journey should stick to its O&G production business as this has historically done well for the firm. With the existing and new infrastructure in place to cater to stranded barrels and LNG export capacity, I believe there is a strong opportunity for producers in their respective regions north of the border.

Considering that Journey is planning to drill less than 1/3rd of the wells in eFY24 when compared to FY23, I believe capital may become more challenging to come by for the firm and that Journey may be forced to continue utilizing high-yielding debt to finance their utility projects. Though regional economics may challenge this presumption, OFS firms like Schlumberger (SLB) and Baker Hughes (BKR) have both voiced land rig utilization is down and that there isn’t significant pricing pressure on dayrates. If I were in the position to decide whether to drill during a relatively strong oil market vs. invest in riskier, capital-intensive projects, I’d go with the latter.

Though management is right in their verbiage towards mineral valuation, I believe the share price will not reflect this value if the firm doesn’t put the miners to work or sell the assets. As an energy investor in today’s market, competing E&Ps that are offering shareholders multibillion dollar buybacks and dividend distributions, like Devon Energy (DVN) and Diamondback Energy (FANG) are much more likely to draw shareholder attention over an O&G producer that is just sitting on their assets.

Journey currently has $17mm in cash on the balance sheet with total debt summing to just over $60b. Journey paid down $24mm of their term loan in FY23 and had a net cash outflow of $14mm. Financing charges on the income statement summed to 14% and 26% for FY22 & FY23, which may potentially be lowered with the new convertible issuance.

Do note that the valuation models have been adjusted to USD at 0.74x USD/CAD.

Corporate Reports

Working out multiple scenarios for the firm, I anticipate the company to remain overvalued given the growth trajectory of EBITDA. Considering all scenarios, I do believe that the firm may be digging itself into a financial hole that will perpetuate the burden of higher interest debt. I rate JRNGF with a SELL recommendation with a price target of $1.52/share at 2.5x eFY24 EV/EBITDA.

Corporate Reports

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.