arcady_31/iStock Editorial via Getty Images

arcady_31/iStock Editorial via Getty Images

Kimco Realty Corporation (NYSE:KIM) is a well-managed real estate investment trust that is profiting from robust growth in rental rates in its metropolitan area-focused real estate portfolio.

The REIT also has growing portfolio occupancy and in 4Q hiked its quarterly dividend pay-out to $0.24 per share. The shopping center trust’s yield, potential for dividend growth, a low pay-out ratio based on FFO and a compelling valuation all culminate in a Buy stock classification for passive income investors.

Kimco Realty’s large and diversified property footprint was a key consideration for my last Buy stock classification.

I advised passive income investors to buy into Kimco Realty in November 2024 due to the trust’s robust NOI growth. The thesis so far has played out well, with the stock price increasing about 3% and 4Q-23 reaffirming key trends in the business.

The trust reported robust results for the most recent quarter as well and has since hiked its pay-out and paid a special dividend. Rent per square foot growth and a resilient real estate market further back up the investment thesis.

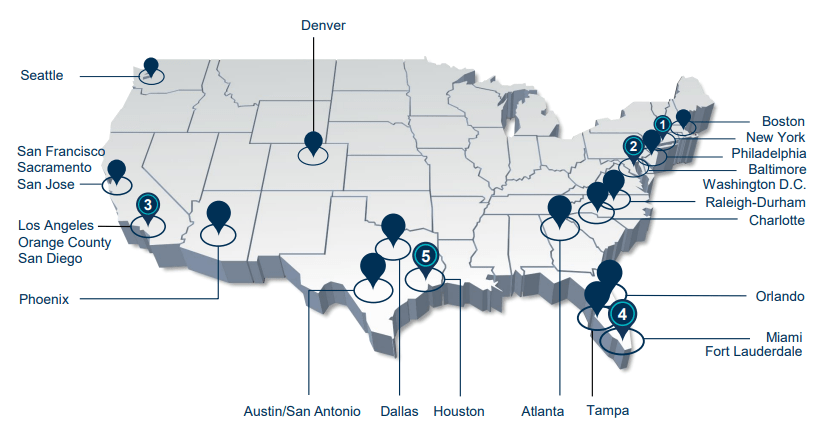

Kimco Realty owns a portfolio of open-air shopping centers that are grocery-anchored and primarily located in urban centers with strong population growth and high household incomes.

The trust produced 86% of its annualized base rent from Coastal and Sun Belt markets that include major metropolitan areas like New York, Boston, Orlando, San Francisco, Seattle and Dallas.

In total, the shopping center-focused real estate investment trust had 2.7M square feet leased to tenants in major cities in the United States.

Assets Overview (Kimco Realty Corp)

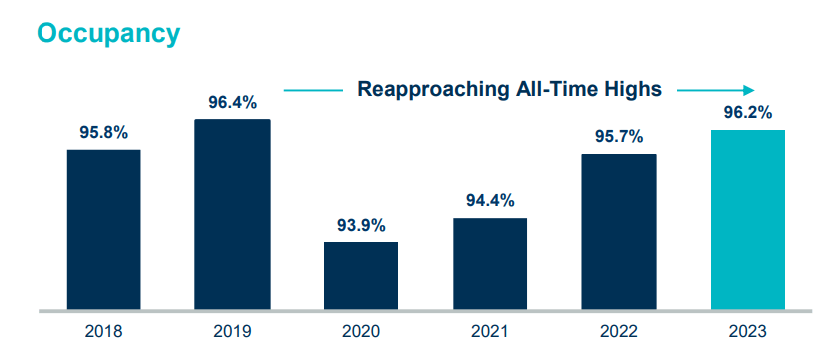

The focus on grocery-anchored open-air shopping centers ensures a steady amount of foot traffic which in turn leads to high occupancy for the trust.

The portfolio, as of December 31, 2023 was 96.2% leased which means the occupancy rate is now in striking distance of the previous all-time high of 96.4%. This high was achieved just before the Covid-19 pandemic and Kimco Realty has worked its back to this occupancy level ever since.

Occupancy Rates (Kimco Realty Corp)

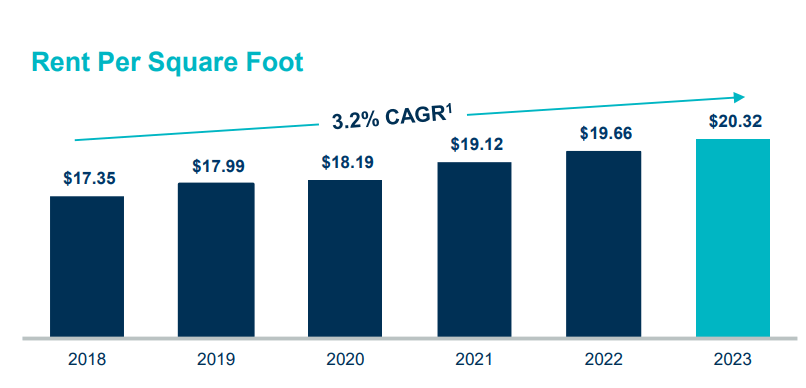

A primary driver of Kimco Realty’s success as an open-air shopping center REIT relates to its ability to raise rental rates. Being able to jack up lease rates has been the number one reason why the trust has boosted its net operating income and funds from operations over time and which ultimately also backed Kimco Realty’s dividend increases.

The trust’s shopping center strategy is paying off well since the portfolio, as I said, is grocery-anchored, resulting in predictable same-store rental growth. This strategy also helps lower the volatility of the trust’s funds from operations which are a basis for the calculation of Kimco Realty’s highly stable pay-out ratio. I anticipate Kimco Realty to add more shopping centers to its real estate portfolio moving forward and grow in its key markets.

The trust’s rent per square foot rose 3.4% YoY in 2023 to a new high of $20.32 per share and even the pandemic did not curtail Kimco Realty’s ability to hike rents. The trust is able to charge higher rates for its real estate because its properties are located in economically-vibrant markets where real estate is supply-limited. The high cost of owning properties in such cities also acts as a barrier to entry which strengthens the bargaining position of real estate landlords like Kimco Realty.

Rent Per Square Foot (Kimco Realty Corp)

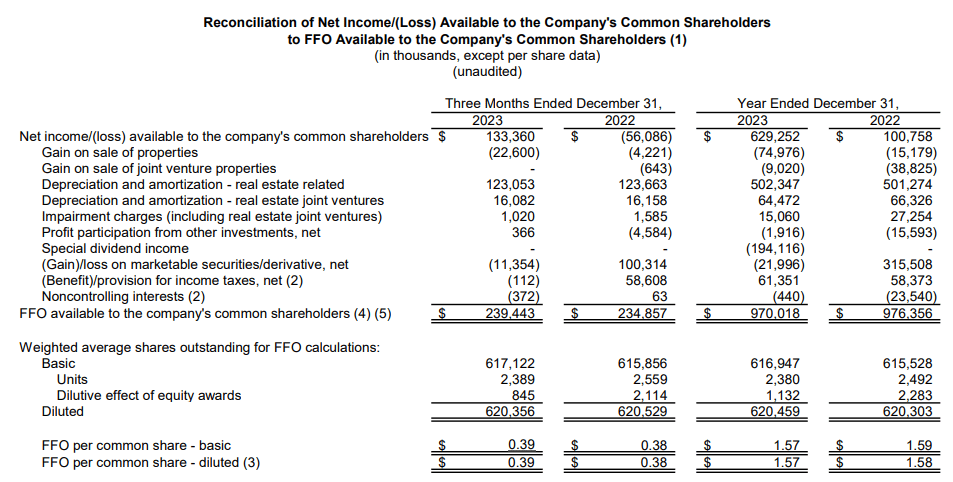

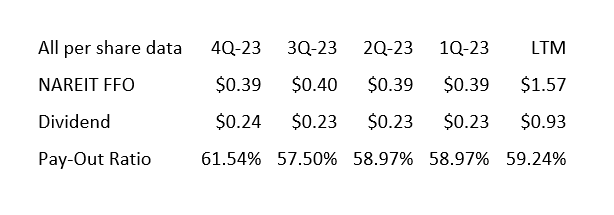

Kimco Realty earned $239.4 million in funds from operations in 4Q-23, up 2% YoY. Funds from operations is a core metric to evaluate the financial achievements of real estate investment trusts and is often used by investors to determine pay-out ratios and the safety of the dividend.

On a per share basis, Kimco Realty earned $0.39 in 4Q-23 which was more than sufficient to pay the regular dividend and afford a raise for shareholders, too.

Funds From Operations (Kimco Realty Corp)

The real estate investment trust raised its 4Q-23 regular dividend to $0.24 per share and paid a $0.09 per share special dividend also. The FFO-based dividend pay-out ratio in the fourth quarter was 62% compared to 59% in 2023.

Realty Income Corp. (O),which owns a large retail-focused real estate portfolio in the United States as well, had a dividend pay-out ratio of 76% in both 4Q-23 and 2023. Kimco Realty, though having a slightly different strategy with its focus on shopping centers, offers passive income investors better dividend coverage than Realty Income.

Dividend (Author Created Table Using Trust Information)

Kimco Realty has guided for $1.54-1.58 per share in funds from operations in 2024 which would be about flat YoY (the trust earned $1.57 per share in 2023). With the stock selling for $18.98 at the time of writing up this piece, the commercial real estate investment trust is selling for a funds from operations multiple of 12.2x.

The market might apply a discount to Kimco Realty’s FFO multiple because the trust slashed its dividend during the pandemic, resulting in a blemished dividend record. However, the trust is growing its pay-out again and the dividend is well-covered by FFO. I think that Kimco Realty could comfortably re-rate to a 15x FFO multiple (implied intrinsic value of $23) when taking into account how strong the pay-out ratio is. Given the low volatility in the FFO pay-out ratio and favorable underlying business trends (growing NOI, FFO, rents), I think that a 15x FFO multiple can be justified, not only for Kimco Realty, but also for Realty Income, for instance.

Realty Income anticipates $4.17 to $4.29 per share in funds from operations (normalized) in 2024, so the implied FFO multiple here is 12.3x. Tanger Inc. (SKT), which is specialized in open-air retail shopping destinations, sees between $2.01 and $2.09 per share in funds from operations which leads us to a 2024 FFO multiple of 13.8x.

The FFO multiple for Kimco Realty is therefore quite competitive and since the stock pays a very well-covered 5.1% yield, I think that KIM is a very promising core investment for passive income investors.

Kimco Realty has no exposure to the office market which is suffering from occupancy headwinds after the pandemic. Retail is doing quite well, however, with receding inflation potentially being a catalyst for consumer spending.

On the other hand, higher inflation, which we have seen unfortunately in February, might be a headwind to consumer-driven spending.

Kimco Realty is profiting from solid underlying business drivers in its portfolio including rent per square foot growth which in turn is backed up by a resilient market for retail space.

The commercial real estate investment trust makes a solid value proposition all around with its improving occupancy, rent per square foot growth and low FFO-based pay-out ratio.

Kimco Realty paid out less than 60% of its funds from operations in 2023 which should translate into healthy dividend growth moving forward.

The trust’s stock is selling at a competitive multiple compared to other retail-focused real estate investment trusts and the pay-out is even better covered than Realty Income’s strong monthly dividend.