Adam Smigielski

Adam Smigielski

Each month I feature several dividend paying stocks that I don't think offer any margin of safety based on their business and current stock price. This theme irritates some dividend yield chasers, so I encourage you to vent in the comments.

When investing, your goal ought to be to have a "margin of safety" on every investment you make. Margin of safety is the difference between a company's current share price and its intrinsic value. Consider this article series an early warning siren.

These stocks might not plunge in price tomorrow, but based on my 3 to 5 year outlooks for the companies compared to their current share price, I don't see much margin of safety, but do see limited upside and considerable risk. I suggest upgrading if you own these into better positions. Sell these stocks and buy better dividend stocks with bigger margins of safety.

This month I'm looking at consumer staple stocks which often benefit from a flight to safety right before a stock market correction. All 3 of the stocks I cover today have had recent rallies that I think you should use to sell your holdings if you have any.

I do not like most consumer staples stocks long-term due to the challenged business models of most. The low margins and low growth are hard to overcome. For dividend-paying companies, the lack of growing profits also is a potential challenge for future dividend payments.

By selling the covered stocks into recent strength, if we get the correction I believe is coming, then you can pivot to better stocks soon.

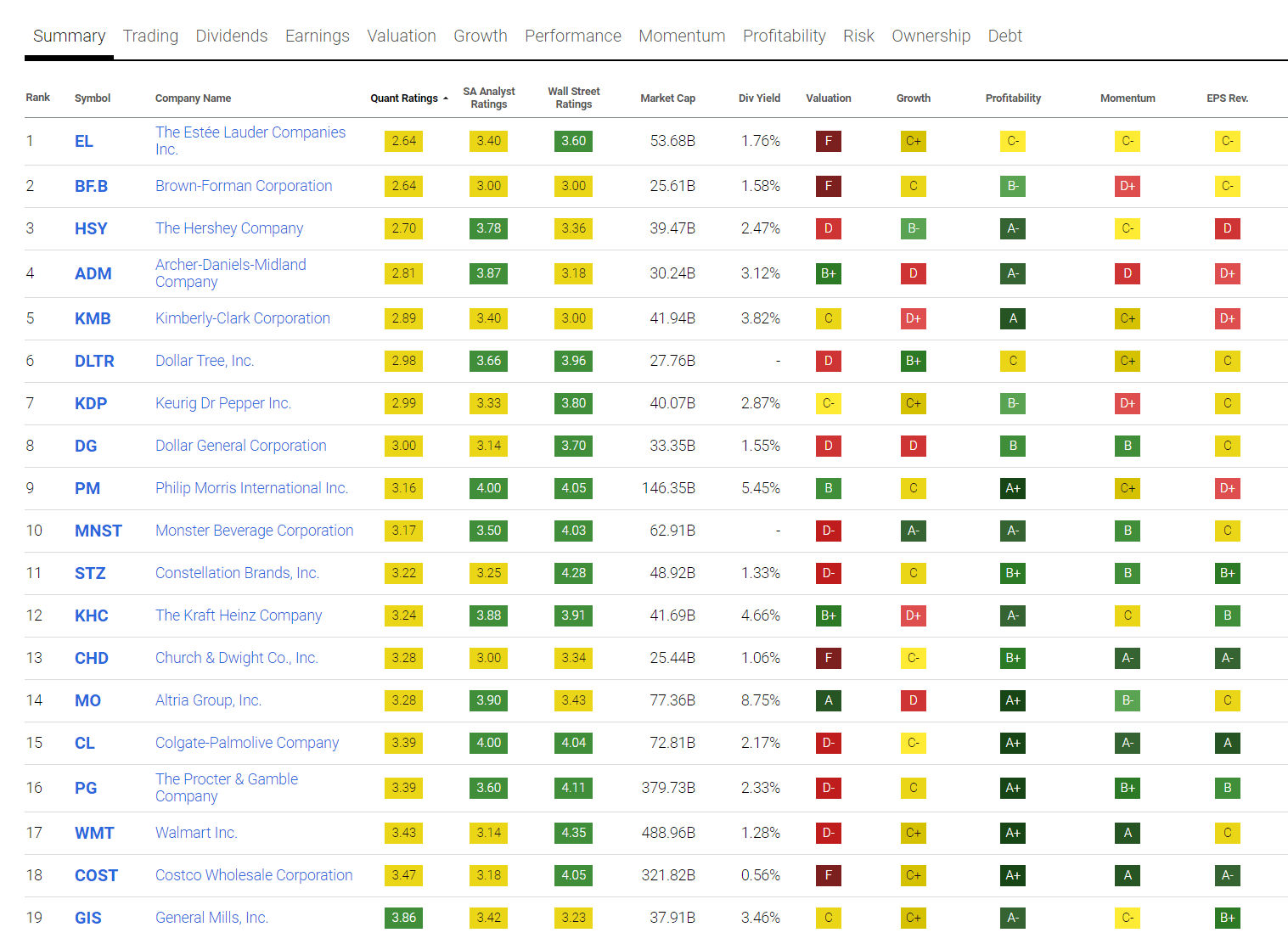

I used the Seeking Alpha Premium screener to find U.S. domiciled consumer staples companies with market caps over $25 billion that were not rated "strong buy." Here's what the list looks like:

U.S. Consumer Staples $25b+ (Seeking Alpha Premium Screener)

I have various levels of familiarity with all of the stocks listed, and after reviewing most, I'm updating my coverage on the following with sell ratings.

I last wrote about Altria in August 2017 and gave it a sell rating: There's Smoke Coming From This Dividend Champion And It's Time To Evacuate.

The price at publication was $65.15. Since then it's down 32% in share price, but has eked out a 7% gain based on that super sexy 8.9% dividend yield people like to talk about. For the record, the yield is only that high because the share price has fallen so much.

From a total return standpoint, Altria trailed the S&P 500 (SPX) considerably. Not exactly a great risk adjusted return.

I do not see much reason for Altria to turn around. Their core smoking market continues to get snuffed out and management's growth initiatives have been weak attempts.

Altria sees its earnings at about $5 this year. Their EPS forward long-term growth rate (which you can find under the Growth heading on the Seeking Alpha company page) is only forecast to be about 4%. That would mean EPS of maybe a bit above $6 in five years.

If we consider that PEG ratio should not really exceed 2, then that means the P/E should only be about 8 for Altria. That implies intrinsic value could be as low as $48 adjusted for finances a few dollars in either direction.

Morningstar gives Altria a fair value of $52 on the one year outlook. The StarMine from Refinitiv composite rating of eight top independent analyst firms has Altria rated 5.1 or neutral. Value Line gives a 3-5 year appreciation range of $60-90. I think it would be a very best case scenario to see $90/share in the next five years and that $60 is far more likely.

I think a negative surprise is quite possible for Altria given its challenged core business and difficulty growing newer businesses. To reenergize growth, many companies have to cut their dividend. Dividend growth has already fallen to about 5% the past five years. The next step would be a cut.

What would cause a dividend cut? Well, long-term debt has nearly doubled since 2017 from about $13 billion to $25 billion. And the company has been paying it down slower than originally anticipated. What if financing rates in fact do stay higher for longer in the face of slow growth?

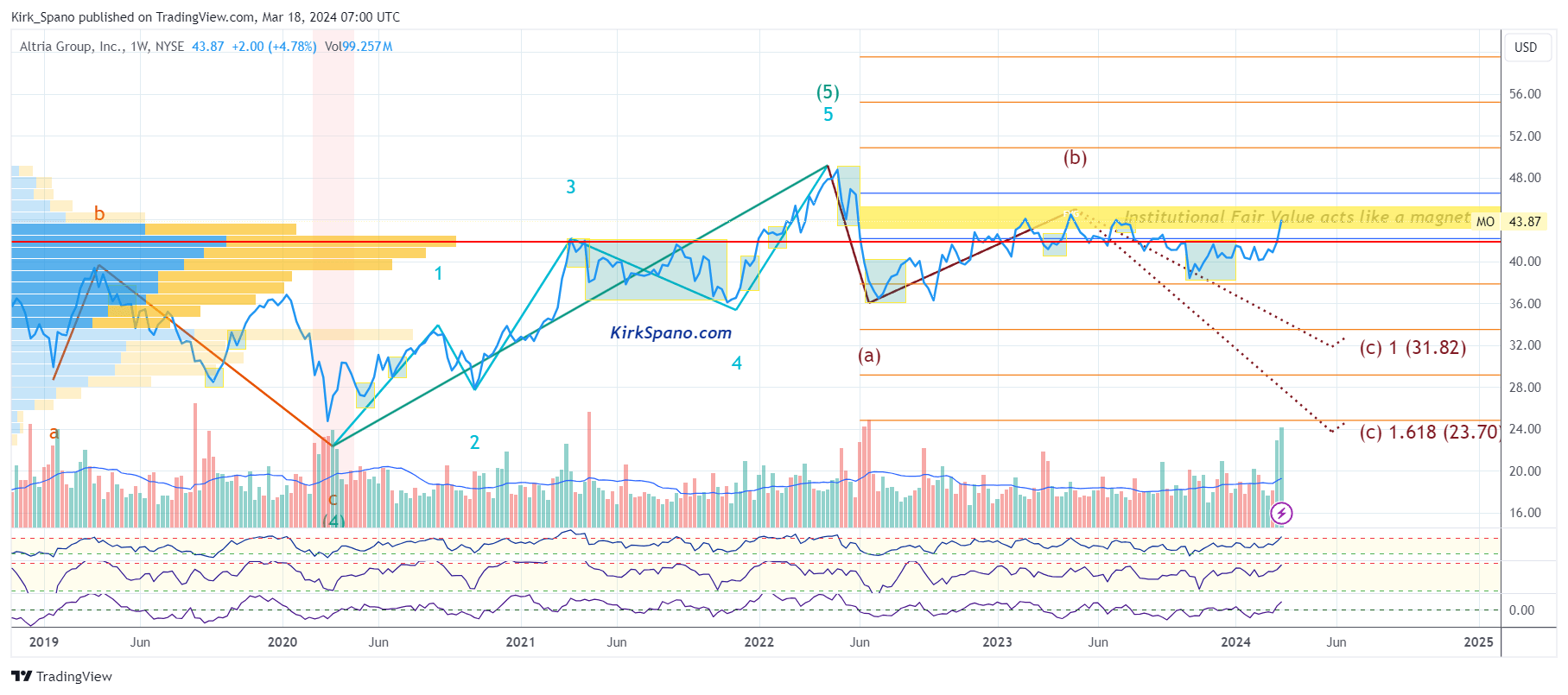

From a technical standpoint, the weekly measured RSI (vs. daily measured that traders use) is sitting above 70 which is overbought on an extended time frame. That means a high risk for price to fall soon.

In addition, two measures of institutional fair value that act like a magnets for price have been satisfied, meaning any more appreciation would be harder to earn. And an algo-driven Elliott Wave pattern recognizer also is seeing a correction in the not too distant future.

MO Chart (Kirk Spano)

Overall, there's significant fundamental and technical risk with Altria. As you can see, I'm not forecasting Armageddon for Altria. I'm no longer a short on this name and haven't been since March 2020.

I think Altria stock is about fairly valued. Going forward, I see limited upside that will be difficult to attain, high business execution risk and almost no margin of safety based on the stock price. I think you can do better, so sell it before it corrects and upgrade accordingly.

I actually have a fuller analysis of ADM coming out soon and might in fact initiate a short on it if the price runs too high.

ADM is a heavyweight in the agricultural commodities arena, specializing in the acquisition, processing, and distribution of various crops. They're the middlemen between farmers and buyers in the food, feed and energy sectors, handling everything from transportation to storage to processing. They would seem indispensable and offer a moat. But that's not true.

ADM's industry is cutthroat, with a lot of similar products and services from competitors. According to CSI Market they compete with dozens of companies including:

Competition leads to a lack of pricing power, which is compounded by the massive capital investments required to keep their operations running smoothly. The end result is razor-thin profit margins.

ADM runs the company on credit and has net margins of barely 4%.

As I search for market-leading investments, I'm looking for something that's often "asset light." ADM is "asset heavy" and has all the capex and maintenance expenses.

Firms that are "asset heavy" need to have an especially unique barrier to competition in order to be able to generate higher margins that generate profitability. Clearly no such "moat" exists with ADM.

Soybeans and corn are the backbone of ADM's operations. So, while ADM benefits from the surge in Chinese soybean consumption and government mandates for ethanol use in fuel, they also face headwinds like fluctuating demand for high-fructose corn syrup and stiff competition in commodity markets. They also have to deal with the whims of the Chinese communist party.

In short, ADM is a capex heavy company, with a lot of competition, no discernible competitive advantage and slowing growth which result in little pricing power. As a result, ADM has no durable competitive advantages and no moat. Analysts who do not understand this basic analysis should be ignored.

Owners of ADM should familiarize themselves with the recent earnings restatements and Justice Department investigation. I believe they underlie a general weakness in reporting and very challenged growth.

Ultimately, ADM's dividend is in danger of not rising much in coming years and could face a cut if financing becomes tight for them. With little upside, considerable risk and the recent rebound rally in price, I believe investors should sell ADM shares.

I have watched P&G for my entire career. It has chopped higher for a very long time. It probably is the best company I'm saying to sell in this article. P&G has good management and a narrow moat by most analysis. You know many of their brands:

...and more.

Everyone knows P&P and the stock has rallied. The recent rally though has left the company with virtually no upside the next five years.

According to Valueline, the potential share price appreciation for P&G is $175 to $215 the next five years based on forecasted earnings and the typical range on their price to earnings ratio. Virtually every bottom up analysis I found is in that range.

Last year, Warren Buffett's Berkshire Hathaway (BRK.B) sold their remaining holdings in Procter & Gamble. Buffett is famous for his thoughts on "margin of safety." He has explained that we want to buy companies whose stocks are trading at a discount to their value. In the case of P&G that's not the case.

I would add that stocks sold by Berkshire Hathaway often have a downward price trajectory soon after.

My argument here is not against the company, it's purely a risk vs. reward argument based on price and the risk that all companies come with. We're simply not getting enough margin of safety to own P&G stock.

The future is unknown, so I'm uncomfortable with the growth outlook and the potential for black swans. I would need a much cheaper price to own P&G, and as such, might consider it on a deep correction for the appropriate accounts.

Since the dividend is barely above that of the S&P 500 and there is no price based margin of safety, why own the stock individually when you can surely own a small amount through your various ETFs and mutual funds?

Sell P&G and find something with a bigger margin of safety and higher dividend.

For those who like fewer words, here's a quick take:

This has been a window of my thinking about investments in general and these companies in particular. I hope you find it useful.