branislav_bubanja

branislav_bubanja

Silicon Motion Technology Corporation (NASDAQ:SIMO) is one of the lesser-known semiconductor investments and a key player in non-volatile storage technology. However, I consider it to be overvalued at this time, and I see risks in its market over the next few decades.

Silicon Motion is a global leader in the supply of NAND flash controllers and solid-state storage devices. It fully develops and brings to market high-performance, low-power semiconductor products for original equipment manufacturers and other customers in consumer electronics, enterprise storage, and mobile communications.

Its main product offerings can be broken down into three distinct categories:

SIMO is primarily in the NAND flash memory market, which is a type of non-volatile storage technology that requires no power to retain data. This functionality makes it a key element for storage in smartphones, tablets, USB flash drives, solid-state drives, memory cards, and more. As the dominant form of flash memory, it is in high demand for its ability to store large amounts of data efficiently and reliably in a tiny physical space.

Of its competitors in the NAND flash memory market, these three stand out as the most significant:

Author, Using Seeking Alpha

Mordor Intelligence estimates the NAND flash memory market size will be $52.86 billion in 2024, and it expects it to reach $68.87 billion by 2029, indicating a CAGR of 5.43% over the period. It attributes this good growth to increasing demand for PCs and smartphones with more storage capacity.

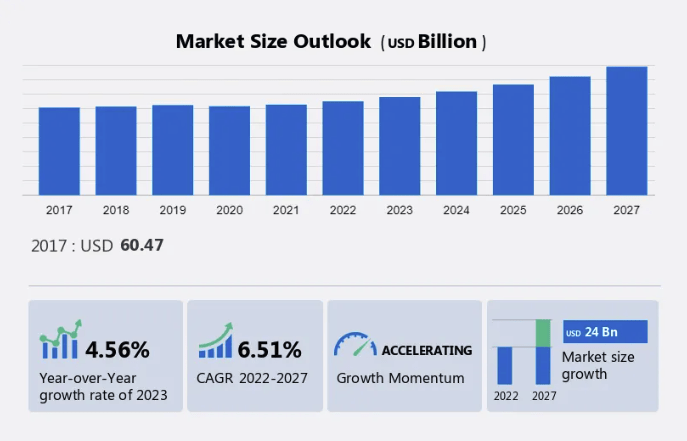

Alternatively, Technavio estimates a CAGR of 6.51% from 2022 to 2027 for the NAND flash market, attributing the growth to fabrication facilities, edge storage, and high-density storage requirements of smartphone applications.

Technavio

Investors may also be wondering, 'What are the dominant technological advancements that could be a threat to the demand for NAND flash?' Here are the five threats I have identified:

One of the primary barriers to widespread adoption of these technologies thus far is cost, and NAND enjoys significant economies of scale, which make it more favorable to the mass market at this time. There are also compatibility issues that indicate the market is not quite ready for widespread integration of faster storage technologies, and ecosystem support for higher performance will likely happen gradually.

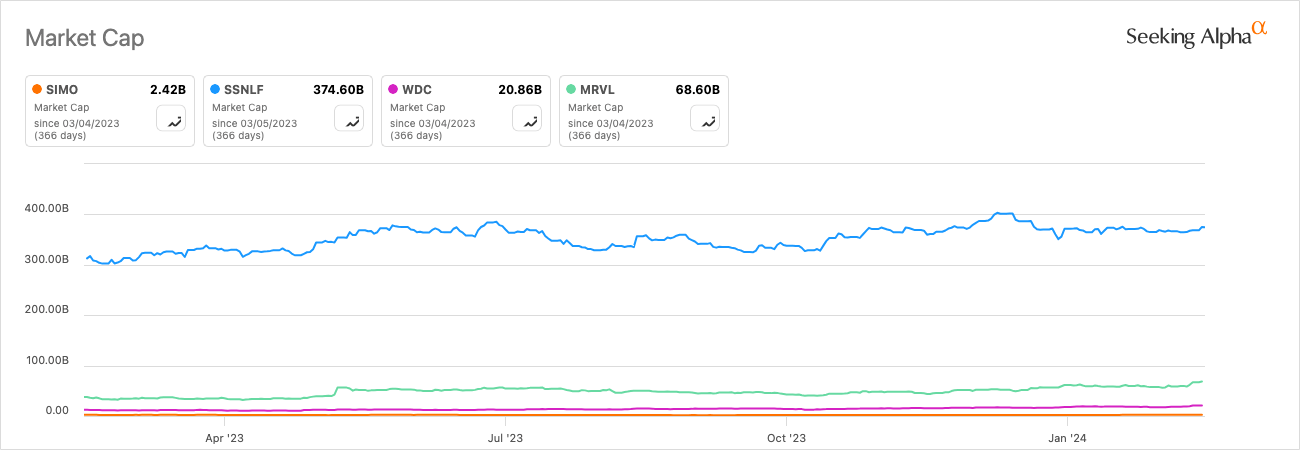

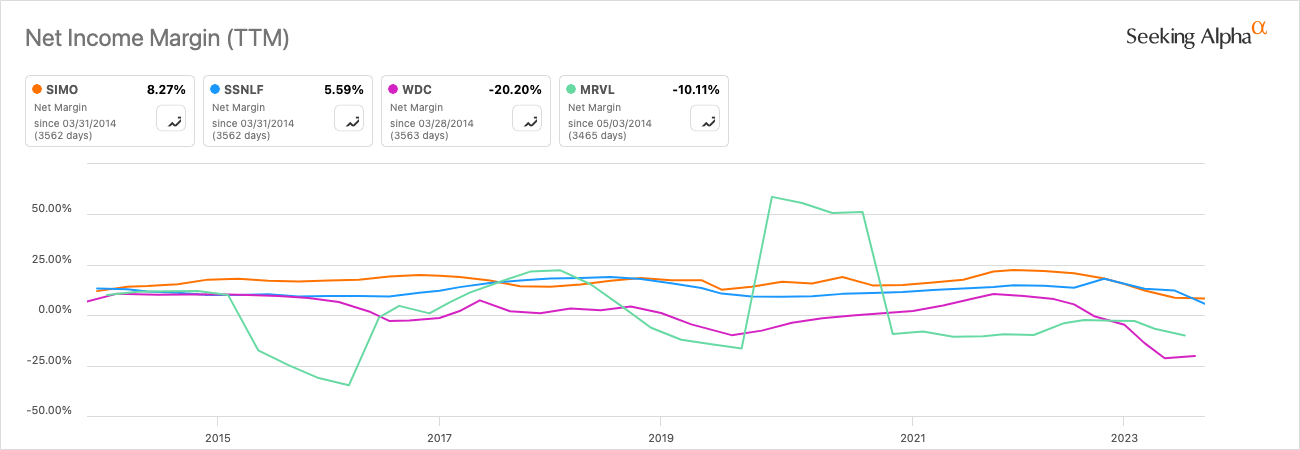

Silicon Motion has particularly good profitability when compared to peers:

Author, Using Seeking Alpha

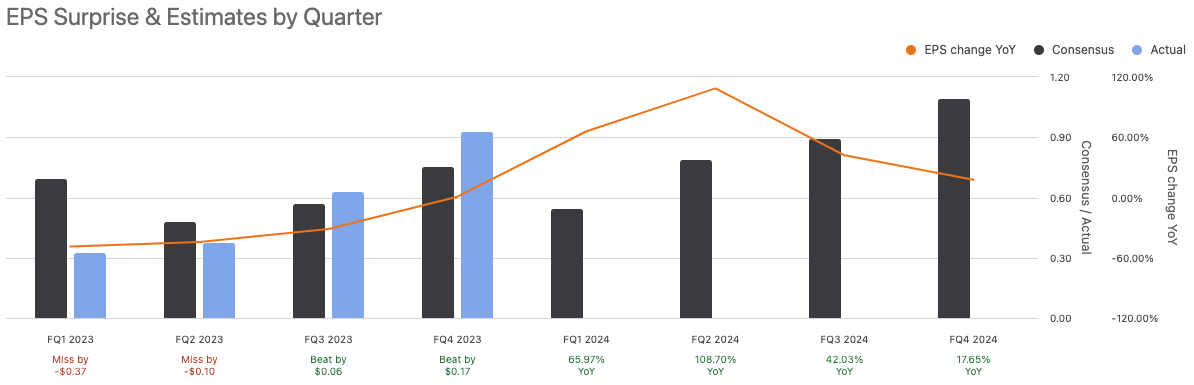

Yet, the company is going through a period of negative growth at the moment:

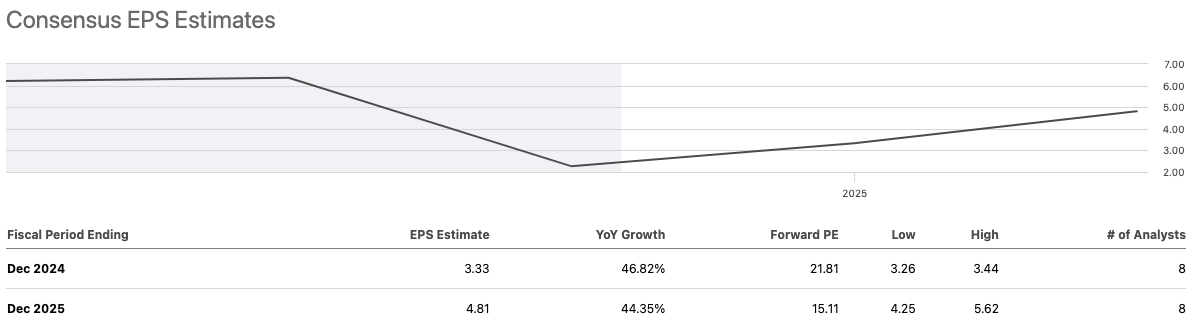

However, normalized actual EPS results for the second half of 2023 show significant earnings beats and a consensus forecast from here that indicates growth set to resume throughout fiscal 2024:

Seeking Alpha Seeking Alpha

The previous decline was largely a result of global macroeconomic weakness and lowered demand for PCs and smartphones in late 2022. Additionally, Silicon Motion entered a legal dispute with MaxLinear (MXL), who had planned to acquire Silicon Motion, but the merger was terminated. This contributed to operational and financial strain on SIMO.

One of the elements of an investment in SIMO that I consider extremely strong is its balance sheet. At the time of this writing, it has no debt and an equity-to-asset ratio of 0.73. To compare this to the competitors used in my peer analysis:

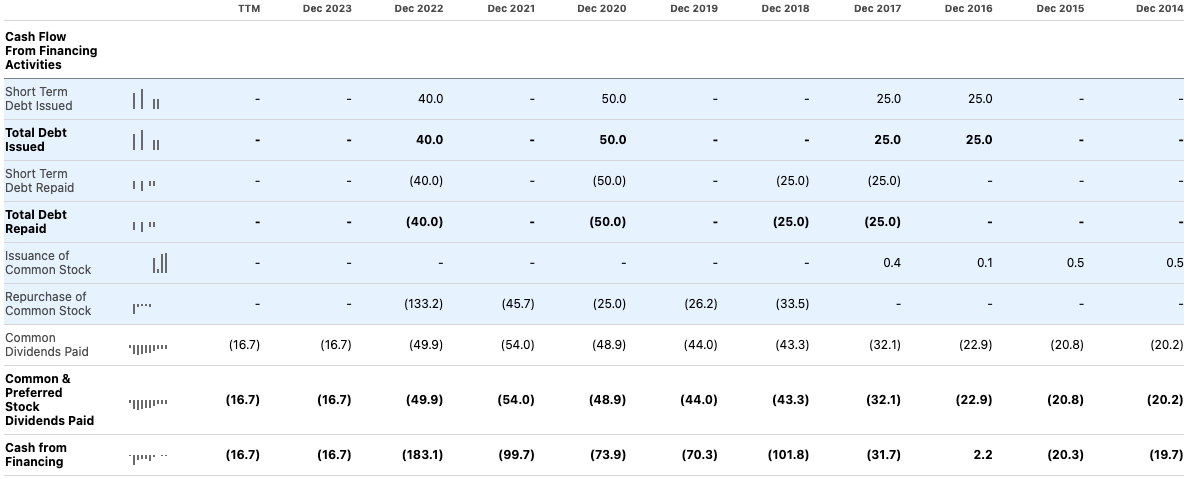

We can see on SIMO's cash flow statement the very infrequent issuance of debt and the rapid repayment of it. We can also note that it does not issue much common stock at a significant level or frequently, and has bought back a substantial amount over the past decade, indicating what I deem as excellent financial management.

Seeking Alpha

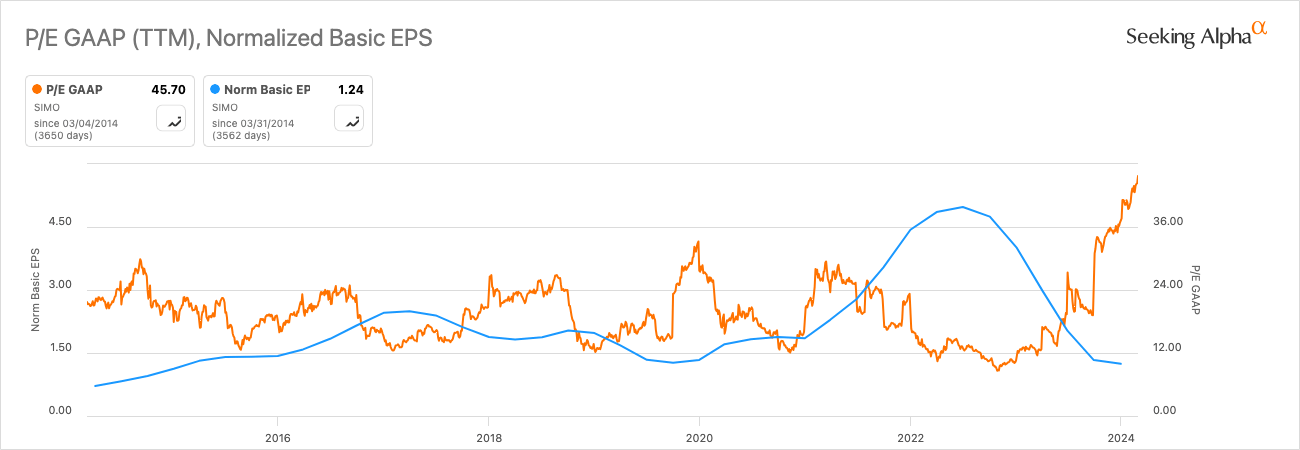

While SIMO looks like it could be a good investment over the long term, I believe the opportunity to buy into the company at a low valuation might have passed at this time. Before fiscal 2023, when earnings results were expected to give negative growth on a GAAP basis, the stock saw a significant drop in price, but since earnings estimates have again indicated continued growth, the stock price has risen to what I consider an unfavorable valuation.

Seeking Alpha

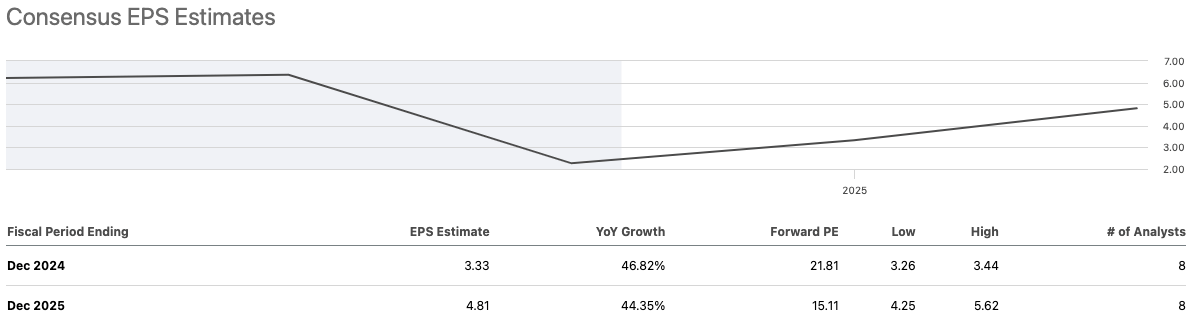

to reiterate, the earnings forecasts for fiscal 2024 and 2025:

Seeking Alpha

This indicates a 45% YoY growth for two years, yet the P/E ratio has risen above 18.5, which is its average over the past 10 years, to 45, indicating 143.24% growth, when instead, I believe it should be trading around roughly 35, indicated by the 90% growth elucidated in consensus future earnings estimates. Therefore, I estimate a fair value for the shares of $55.50, compared to a present stock price of $71.50, indicating a 28.83% premium.

I consider a significant long-term risk for SIMO is if it cannot successfully manage a mass-market transition to NAND flash alternatives that provide more efficiency. There is a likelihood that some of the faster options to NAND I discussed above become the mainstream choice over time, and technology ecosystems may evolve to support the more advanced alternatives. I have not seen press releases or public discussion on large executions in MRAM, ReRAM, FeRAM or PCM within the company. Therefore, as an ultra-long-term investor, I am apprehensive about the long-term viability of an investment in SIMO.

I consider SIMO a good company and vital in the supply of NAND technologies, which seems to have significant market growth to come over the next decade. However, due to the present valuation and risks with the market over multiple decades, I am hesitant to allocate to SIMO at this time. My analyst rating for the stock is a Hold.