FOTOGRAFIA INC./E+ via Getty Images

FOTOGRAFIA INC./E+ via Getty Images

The Sherwin-Williams Company (NYSE:SHW) appears poised to outperform the US paint market in 2024. The company is coping relatively well with a more challenging operating environment characterised by higher mortgage rates pressuring new housing starts and existing housing sales. However, the near-term demand environment remains muted and I believe there are lack of catalysts in the near-term that may push the stock multiple upwards during the next 12 months. I am currently cautious and assign a hold rating to the stock.

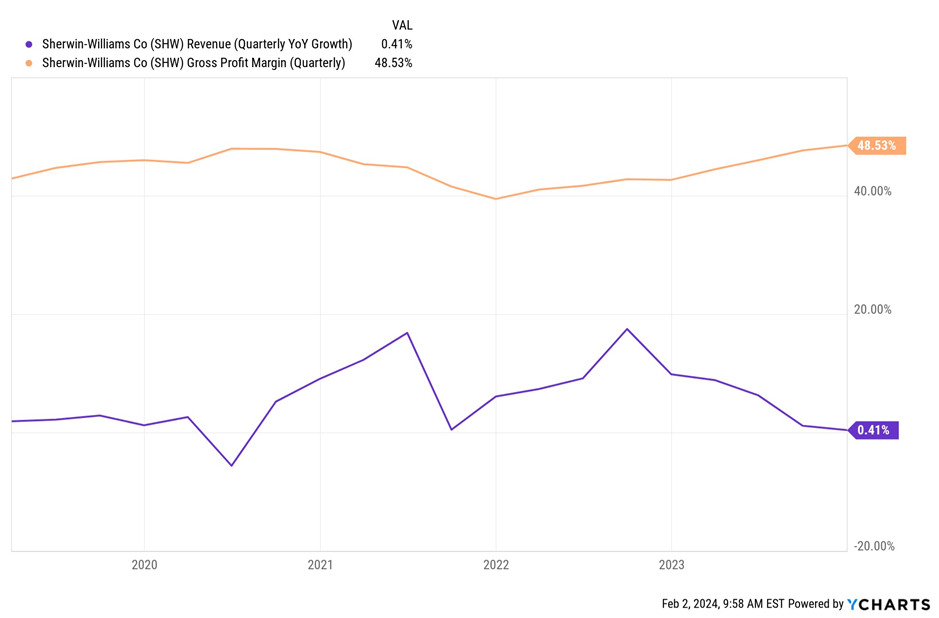

Sherwin-Williams reported its fourth-quarter earnings last month, that exceeded the firm's guidance. The enterprise benefitted from lower raw material costs. As a result, the gross margin expanded year-on-year substantially from 42.7% to 48.5% and improved sequentially from 47.7%. Paint Stores Group drove the sales growth (+2%) led by volume growth in protective and marine as well as in the commercial and residential repaint end market. SHW’s sales declined in new residential end markets, but the company believes that it outperformed the market. Sales at Consumer Brands Group were still affected by low demand from do-it-yourself clients.

Though the broader 2024 macroeconomic setup has improved from 2023 -- a year in which Sherwin still delivered record financial results -- lingering demand uncertainties across new residential, residential repaint (the existing home sales portion of the portfolio), DIY and general industrial underlie conservative full-year EPS guidance. As anticipated, Sherwin is pointing toward low-single-digit volume growth this year, though better-than-expected pricing gives us confidence it can deliver on its 2024 sales-growth target. At the midpoint, 2024 adjusted EPS guidance of $10.85-$11.35 is roughly 7% higher than 2023. Sherwin expects roughly flat 1Q sales, though PSG should be up low- to mid-single digits as its 5% pricing increase (effective Feb. 1) starts to roll through.

Sherwin-Williams broadly competes across most key paints and coatings end markets, with particular prominence in architectural, general industrial, automotive refinish, packaging, and protective and marine. Architectural represents the largest end market globally, followed by general industrial. Sherwin primarily serves architectural customers through its largest segment, Paint Stores Group. The company also has architectural exposure through its Consumer Brands Group, which is primarily DIY and now includes the Latin America architectural business. The industry landscape can broadly be broken out into seven key end markets, with the top global companies showing varying exposure to each. Currently, most indicators like slowing housing starts and falling PMI readings across the company’s end markets suggest volume headwinds, and hence I believe a cautious stance on architectural demand outlook is warranted in the near-term. The in US residential repaint may become more apparent in the near term as elevated mortgage rates -- still averaging above 7% nationally -- keep pressure on existing-home sales. In a tight housing market, however, this dynamic could support new residential into 2024. I expect continued pressure across the DIY end market as inflation constrains consumer purchasing power, and sentiment, particularly in Europe, remains low.

SHW’s revenue growth remained constrained in 2023 as weak global DIY demand continued. Global persistent inflation and economic uncertainty are muting purchasing power and confidence and the DIY end market, which constitutes a significant portion of the CBG's revenue is expected to remain soft in the near term, along with stabilizing-but-lower demand in Europe and choppiness in Latin America, which I believe will result in muted sales growth.

Going forward, margin expansion in the Performance Coatings Group will be important to long-term performance as the company seeks improvement of at least 500-600 bps from acquisitions, above-market volume growth and market-share gains. The raw material costs for the company declined in 2023 resulted in an improvement in gross margins during the course of the year as illustrated in the chart below. SHW improved its balance sheet, with ~$3.54B in total liquidity, including $276.8 million in cash and short-term investments (up from $198.8 million in Q4 2022), and $3.341B available under its $3.75B total credit facilities.

YCharts

The long-term margin story is starting to unfold in Sherwin's Performance Coatings Group, despite a lackluster industrial demand environment and continued global economic uncertainty. The segment has expanded its adjusted EBIT margin in 2023 and I believe positive pricing and accelerating raw-material deflation should help underpin PCG's margin performance in the near-term. Although the company will need to navigate a difficult demand environment in2024, it remains focused on outperforming the US paint market over the long term, suggesting continued top-line gains in Paint Stores Group.

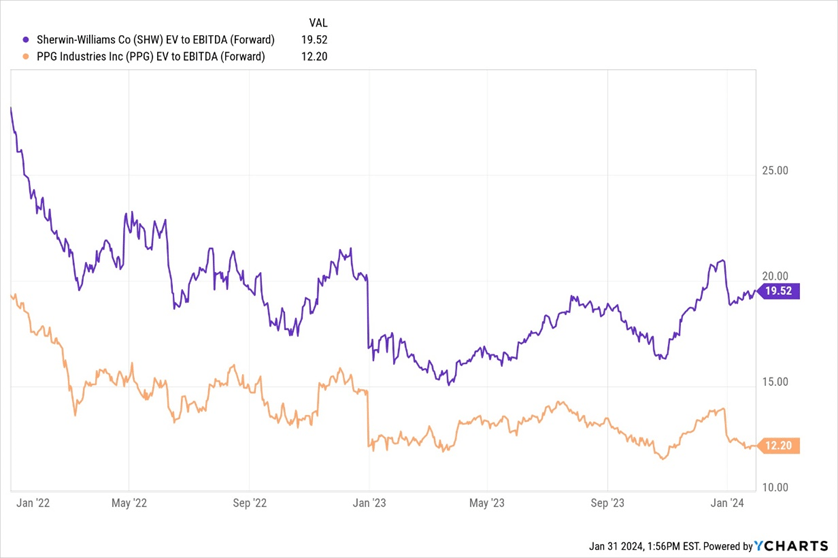

SHW’s forward EV/EBITDA multiple, calculated using consensus forward EBITDA number, has continued to trend down over the past year, however the company still trades at a significant premium to peer coating company PPG Industries, Inc. (PPG) which I believe is due to SHW’s greater US housing exposure. PPG is a global manufacturer and supplier of coatings but has continued to trade at a discount to SHW due to the company’s high exposure to Europe.

Although I believe Sherwin is an excellent consumer franchise, and its value can move up sharply in an environment of flattening or falling interest rates, currently higher interest rates and volume uncertainty for the year ahead will weigh on the share price performance in my view. Revenue and margin in Sherwin-Williams' Consumer Brands Group will likely remain constrained in 2024 as the business contends with continually weak global DIY demand. It's becoming increasingly clear that the inflation-impaired consumer is prioritizing discretionary spending in areas other than house projects, with the management noting in the earnings call that it doesn't see a macroeconomic catalyst ahead that could drive a meaningful improvement in consumer demand.

SHW is estimated to generate $4.5 billion in EBITDA in fiscal year 2024 as per Capital IQ estimate. The stock is currently trading at ~20x forward EV to EBITDA which is at a premium to its primary coatings peer (PPG) and roughly the same as the company’s five-year average multiple. The shares of Sherwin-Williams are 25% higher over the past 12 months, which has pushed the stock’s valuation multiples upwards. I understand why investors like SHW (favorable industry dynamics, pricing power, housing recovery exposure, etc.), but with shares today trading at an elevated multiple, I do not necessarily find today to be a compelling entry point. I believe if the multiple trends closer to its 2023 low, which was at ~15x, the stock would offer a compelling enough risk/reward as opposed to current levels. SHW's 10-year historical EV/EBITDA multiple range has been between 14-21x, and at 20x I believe the stock is very close to fair value leaving limited room for upside. Hence, I stay cautious for now and assign a hold rating to the stock.

YCharts

Although there are demand concerns going forward in 2024, there are some offsets that may help drive healthy financial performance that include resilient residential repaint and solid backlogs in commercial, property maintenance and protective. This may result in market share gains and be a catalyst for the stock. Moreover, a slash in interest rates would potentially be a positive catalyst for the share price and I would continue to keep an eye on that going forward in the year.

Furthermore, although global demand pressures are muting volume expectations, declining costs -- particularly for raw materials -- may support modest margin expansion in 2024 that will pose an upside risk. Importantly, raw-material availability issues appear to be in the rear-view mirror, which has led to increased visibility and a significantly better operating environment.

Although I believe SHW is a high-quality company with durable earnings power, the paints and coatings industry faces stiff challenges in 2024 including the prospect of limited volume growth. PMI readings across key global regions continue to illustrate contraction, while consensus expectations for 2024 GDP and industrial growth reflect only modest growth this year. I see limited catalyst for the stock in the near-term and assign a hold rating to the stock.