JHVEPhoto

JHVEPhoto

There's a great quote out there by hedge fund manager Steve Mandel that goes something like this:

"I don't need an analyst to tell me when a 10 PE stock is cheap. I need an analyst to tell me when a 40 PE stock is cheap."

The meaning of this quote is simply that it can be tricky to find value in expensive-looking stocks, but doing so can pay off big time.

This is because high multiples can put off value-conscious investors, even if a company's potential future results around growth and profitability might actually shorten a stock's potential payback period significantly.

Finding these companies requires a bit of digging (and some speculation), but we believe that we've identified a stock that fits this situation to a T: Shopify (NYSE:SHOP).

With a sales multiple at 14x and an EV/EBITDA that currently stands at ~74x, hardly anyone is calling the stock a 'bargain' at this price point.

However, from a growth and profitability lens, the company appears ready to outperform well into the future, and we expect that Shopify's results may ultimately make today's price appear like a bargain in 2026 and 2027.

Today, we'll explore the ecommerce titan and take a look at SHOP's underlying business, the valuation, and why we ultimately think shares could make a compelling investment at this juncture, even given the heart stopping TTM valuation metrics.

Sound good?

Let's jump in.

We normally start by looking at a company's financials & prospects, but in this case, it makes sense to break down the stock's valuation first.

In short, at first glance, the stock appears expensive.

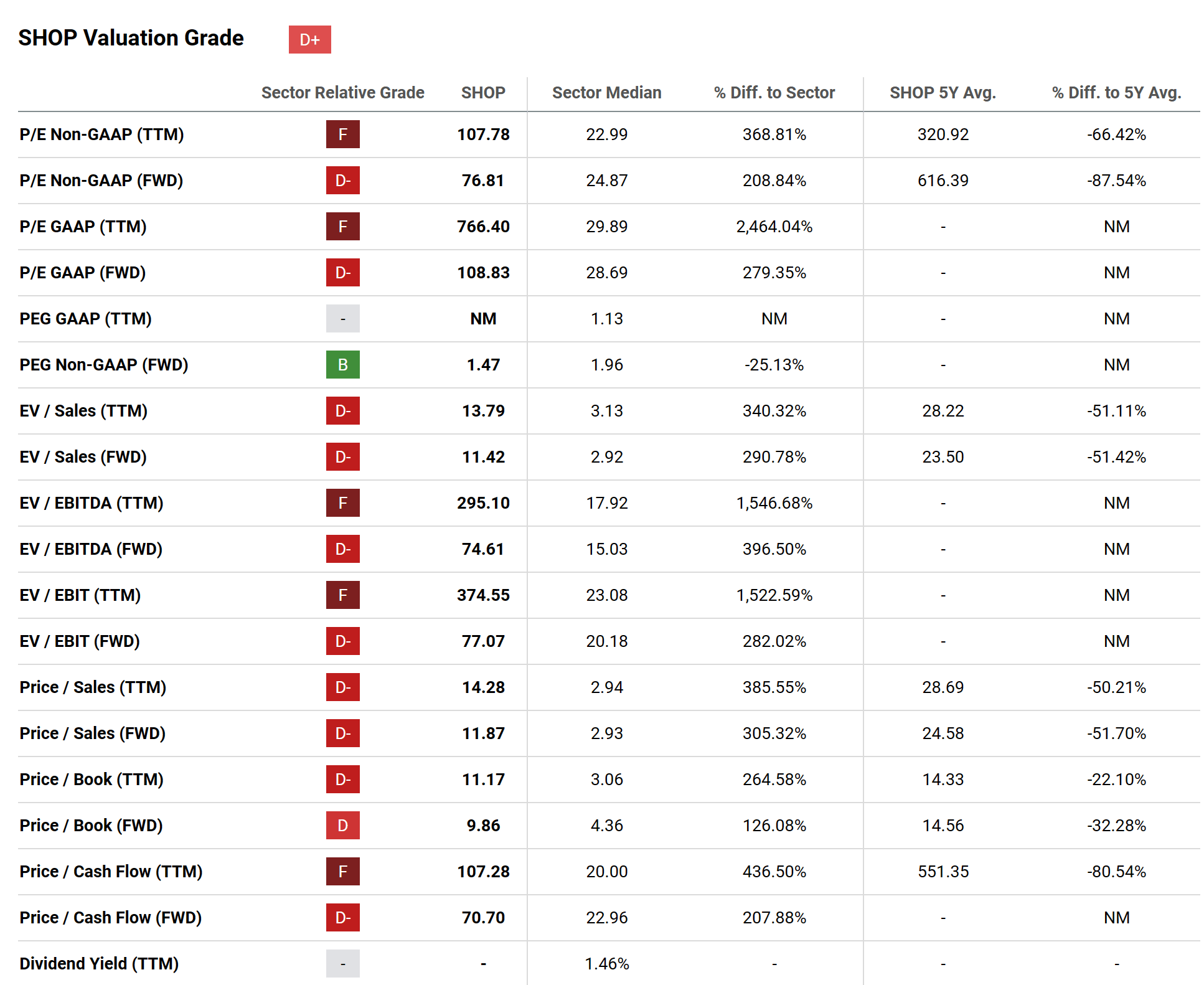

Seeking Alpha

Seeking Alpha's Quant Rating system gives the stock a "D+", which isn't exactly a promising starting point.

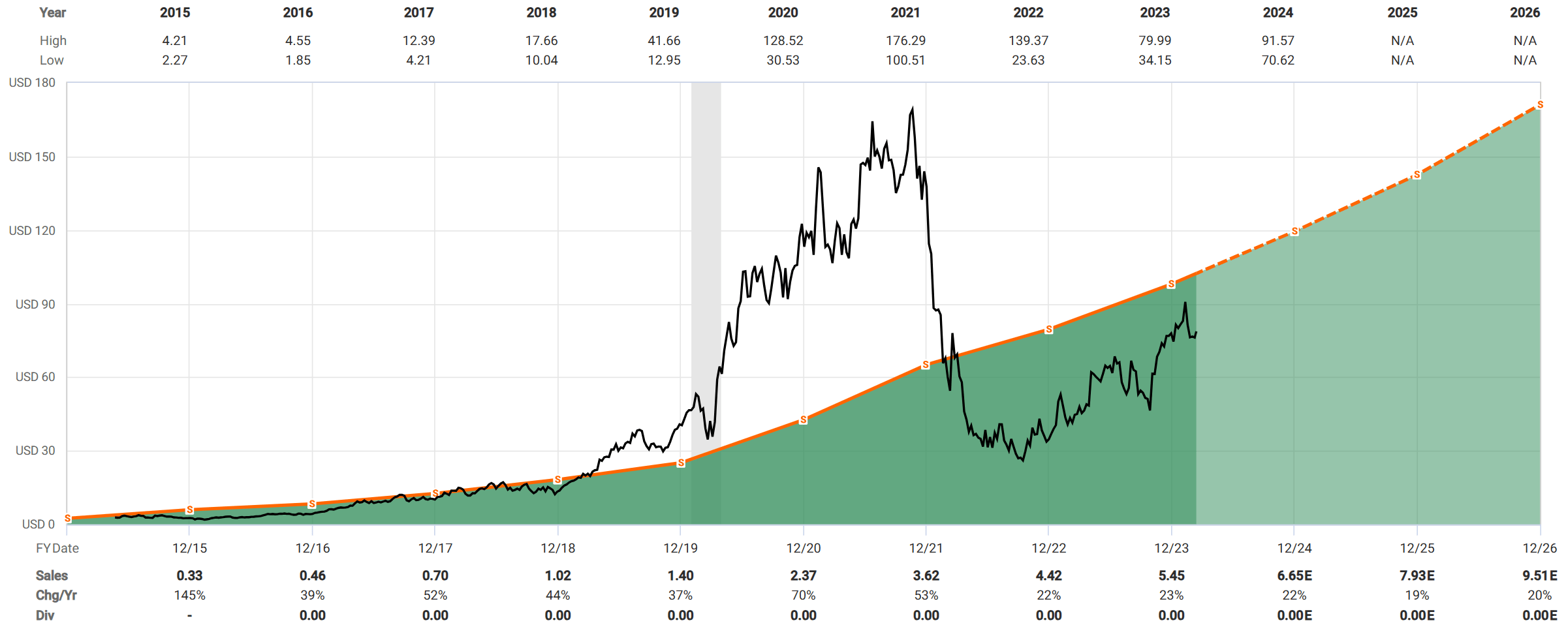

From a top level, SHOP is currently worth a little over $100 billion, but over the last twelve months, the company produced only $8 billion in sales and $132 million in net income.

This places the firm's historical valuation at a VERY high 14x sales and 765x income.

Given that the long-term income multiple of the S&P 500 typically ranges between 15x and 20x, there's no question that SHOP shares are very expensive based on the current results of the business.

Clearly, a lot of this valuation is built on SHOP's future potential to 'grow' into this valuation.

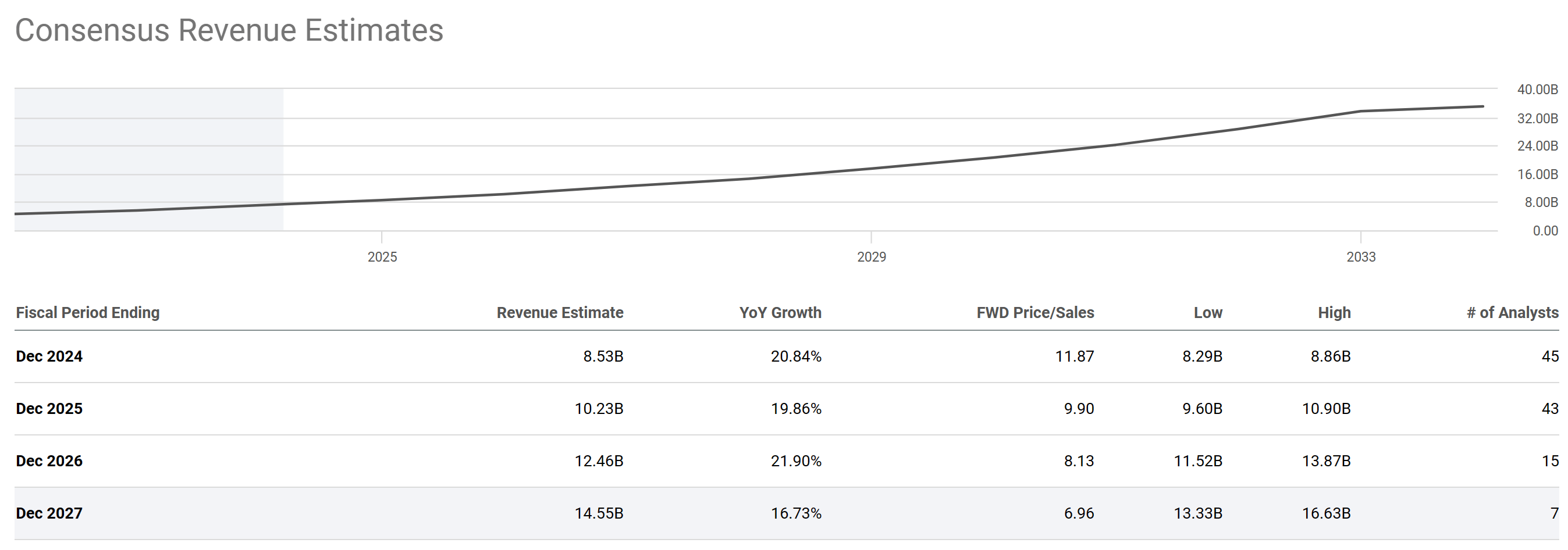

This is where we think the stock is mispriced. In short, assuming the company grows according to analyst estimates and the stock price doesn't move, the company will go from a 14x sales multiple to a 7x multiple by the end of 2027, as sales are expected to grow to about $14.5 billion:

Seeking Alpha

Something similar is expected to happen with SHOP's net income, growing from an EPS of $1.02 at the end of this year to a figure closer to $2.23 at the end of 2027.

This would put the P/E at a much more reasonable 35x. While still expensive, it's a huge 'improvement' from where things stand now.

To achieve these targets and the resulting multiple 4 years from now, analysts are projecting an average of 19.8% annual top line sales growth, as well as 32% average annual EPS growth.

In short, we think the current, baked in valuation undershoots SHOP's potential for a couple of reasons.

High Quality Revenue

First off, relatively little is made, generally, about the quality of SHOP's revenue base. Many see the company, and its technology platform, as somewhat commodified, but that's simply not the case.

For SHOP's customers, the platform is the epitome of 'Mission Critical' for businesses. Switching costs are enormous, and even if they weren't, there's no real reason to switch from SHOP's product in the first place.

The company's main product, accompanying app store, and increased reach from the 'Shop' app all make it the premier destination to begin selling products online.

This dynamic produces two things for SHOP:

In his recent bearish article, even fellow analyst Ahan Vashi conceded the following:

Over recent quarters, Shopify has exemplified the supreme value proposition of its ecosystem [business moat] by raising subscription prices on its Standard plan by 33% with little to no churn. Now, to keep up its momentum in 2024, Shopify is raising prices for its Plus plan (largely used by enterprise customers) by 15 to 25% depending on the length of the subscription.

During the Q3 earnings call, Shopify's leadership had expressed confidence in the price-value ratio of Shopify's platform being skewed toward value [i.e., more pricing power exists] and name-checked Shopify Plus and Shopify Audiences as monetization opportunities. Hence, I am not surprised at all by Shopify's pricing moves.

This is a core proponent of why we anticipate that SHOP can outperform estimates.

Improving Merchant Quality

Another core tenant of this thesis is SHOP's ability to attract, land, and monetize enterprise customers.

In the site builder / payment gateway business, it's typical to see churn as businesses mature and age out of 'beginner' products. This is the issue with Squarespace (SQSP), for example. Many people build sites and stores on the platform, but limited functionality and high per-unit prices often drives off successful businesses that want to do more.

SHOP is moving in the opposite direction. The company began from a 'beginner' solution, but is now moving up the value chain, attracting bigger and bigger customers who need a solid, dependable, competitive ecommerce solution.

Here's what Harley Finkelstein, SHOP's President, had to say on the recent earnings call:

We have signed and added to our incredible roster of merchants, bringing on more diverse businesses across verticals, geographies, and channels.

Brands like Carrier (CARR), Nike Strength (NKE), Dollar Shave Club, Banana Republic Home (GPS), Authentic Brands Group, Tim Hortons (QSR), Guthy-Renker, Buy Buy Baby, Oscar de la Renta, Everlane and On Running (ONON) to name a few.

This indicates to us that SHOP should continue to compete and win against both competitors, as well as the concept of growing and producing something internally. We suspect this is the case for most brands, as it's becoming clear that it's simply better to outsource ops and focus on product. As this trend accelerates, SHOP appears well positioned to capture this opportunity.

Falling Customer Acquisition Costs (Brand)

Finally, SHOP has seen a significant brand strengthening amongst the general populace as a result of both continued advertising, as well as word getting around about the quality of the product.

In short, these investments in marketing and product have paid off in terms of 'Brand'.

While amorphous to some degree, we think that SHOP's brand is as strong as it's ever been, which is why the company is seeing falling incremental CAC as of late, which is highly accretive to both operating margins, as well as the bottom line.

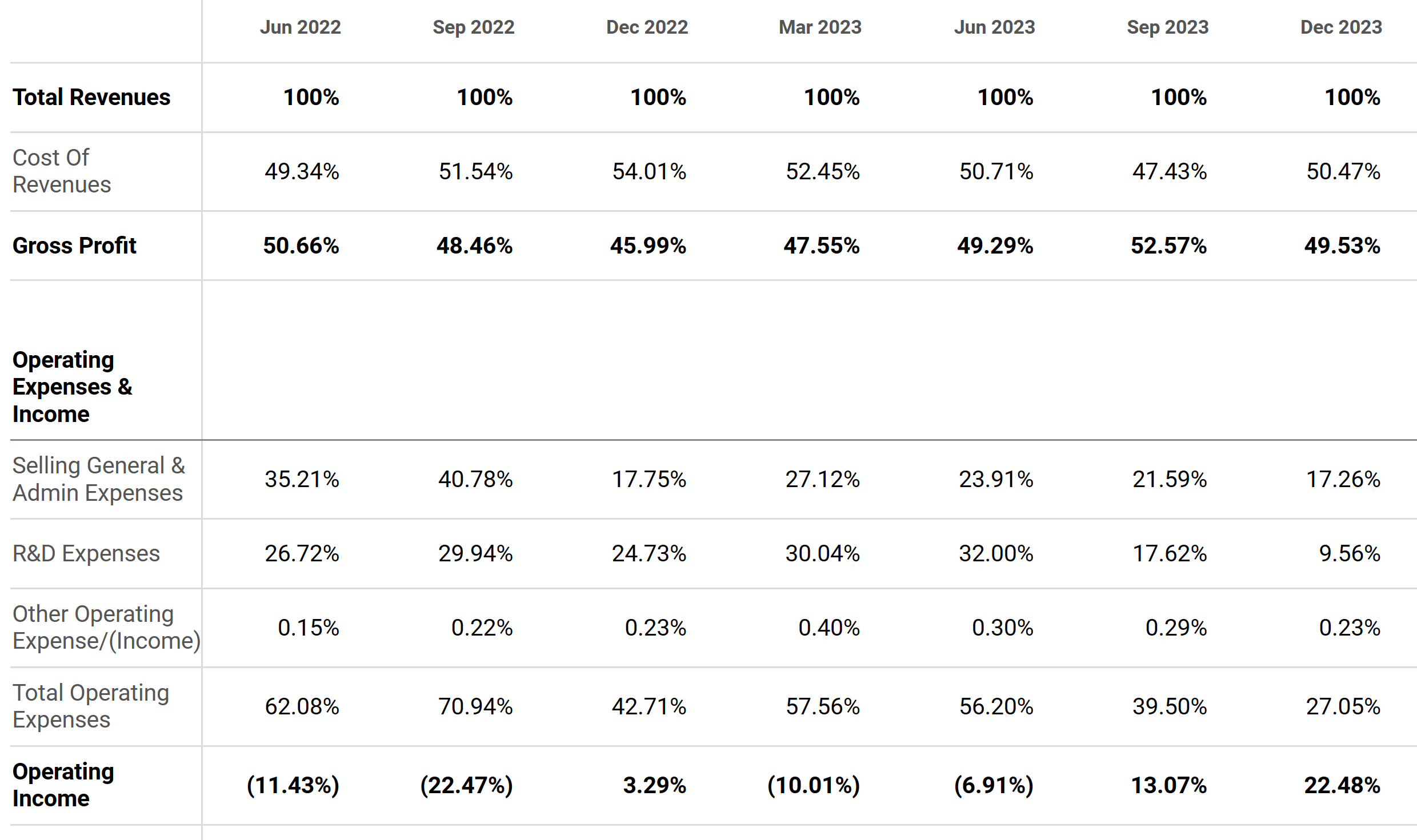

This, in part, is why we believe that operating margins have seen such a dramatic improvement over the last two quarters:

Seeking Alpha

Management had something to say about this on the recent call as well:

We further refined our algorithms for audiences, which has shown reductions in CAC of up to 50% while increasing the advertising platform partners to include TikTok, Snap, Pinterest and Criteo.

We've expanded the on-ramps for merchants into Shopify to thrive at any stage of their growth journey.

In short, while it's possible to assume that SHOP's growth rates could slow or stay stagnant over time as the company's revenue base gets larger, we think that the momentum is simply so strong that it's difficult to see what could derail things.

This all seems great, but how does any of this information translate to a profitable investment?

In short, the company appears reasonably valued if you look at its growth as of now. As we mentioned before, analysts are anticipating 19% top line growth and 32% EPS growth over the next 4 years. If the firm achieves that, then shares appear priced 'on average' for future growth.

We think shares are attractive because growth can be sustained at a higher rate.

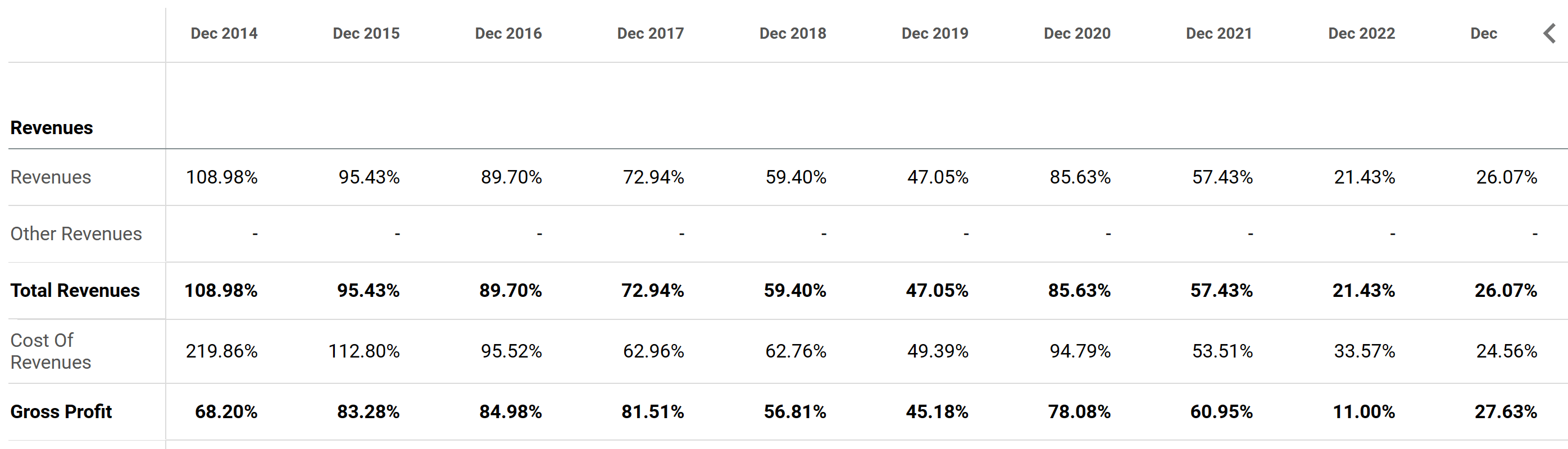

The company's historical results have proven that even in bad times (2022), top line can grow >20% YoY:

Seeking Alpha

When combined with the factors mentioned above, we see SHOP being able to sustain growth well into the >20% range for at least the next 4 years, even on a higher revenue base.

Additionally, if you look at the stock from a multiple perspective, the long-term average valuation for SHOP, as the stock has matured along its growth / profitability curve, is around 18x sales:

FAST Graphs

To be clear, we're not anticipating multiple expansion in the stock, especially as the company matures.

However, if the company's results continue to grow, then it's not unreasonable to expect that the stock won't see a decaying multiple, but rather a stable one. This should power returns that mirror growth, which, as mentioned, could be in the 20%+ annualized range, for at least the next few years as SHOP's advantages compound.

But why now?

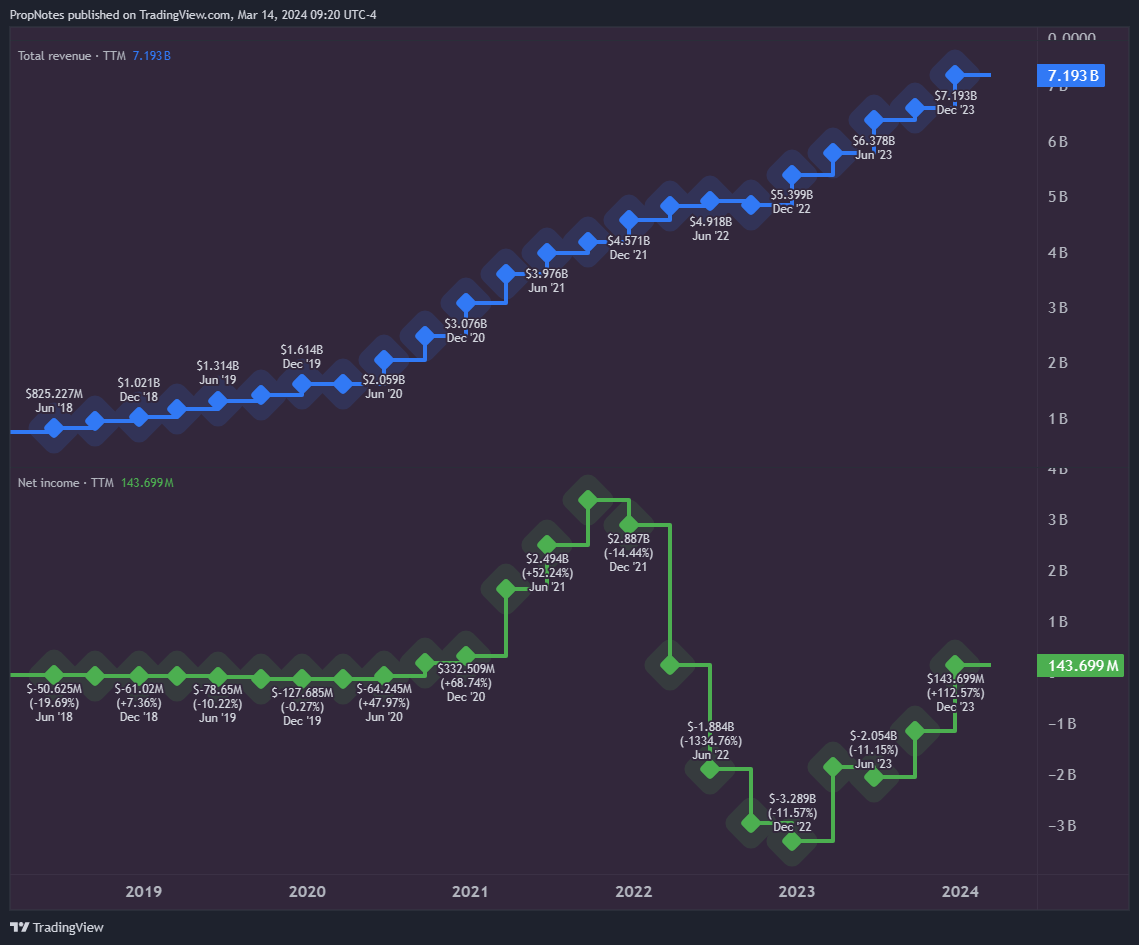

In short, we think that investors have underpriced SHOP's growth due to recent results. From 2021 to 2022, net income for the company went from nearly $4 billion to negative $3 billion, a massive $7 billion swing:

TradingView

This swing was a direct result of the monetary and stimulus bubble that occurred during that time, which saw a massive boom and bust in both ecommerce spend as well as new business formation, which had a material impact on results.

Additionally, at that time, SHOP was also pouring a tremendous amount of resources into their 'SFN' or 'Shopify Fulfillment Network', which was meant to make logistics easier for businesses on the platform and compete with Amazon (AMZN).

Thankfully, the company has since given up on that effort, outsourcing logistics to Flexport.

No matter the reason, as SHOP's results have languished, the market seems to have lost interest in the name, despite the fact that revenues have continued to grow apace.

Now, with net income back in the black and with the prospect of further acceleration on the EPS front, we think a few more positive quarters could act as an invigorating catalyst and re-ignite interest in SHOP.

If things continue at our projected rate, then we could easily see SHOP trading north of $115 by late 2025, as management cranks out consecutive 20%+ growth years.

This represents upside of nearly 50% in the not-too-distant future.

There are some risks to this thesis.

The key risk entirely centers on SHOP's growth and management's ability to execute on the opportunity. While we think the valuation is somewhat forgiving based on our analysis of growth factors, if things come up short, then it could be rough going for investors due to poorer than anticipated results that are compounded by multiple contraction.

This happened in 2021 - 2022, and SHOP shares were cut by nearly 85% from peak to trough.

This was partially due to the aforementioned SFN loss-making build out, but it was also due to a collapse of SHOP's top line multiple in the stock, as results suffered and investors lost confidence in the company's ability to grow.

Clearly, with swings like that, this is not a stock for the faint of heart.

Looking forward, the key macro factor that could drive underperformance has to do with the U.S. government.

In 2020 and 2021, the Federal Reserve injected a tremendous amount of stimulus into the economy and the market in the form of low interest rates and liquidity. As this happened, it caused organic growth and margin expansion for SHOP as people bored from the pandemic tried their hand at starting a business. As stimulus check money ran out and as GMV tumbled as inflation rose, it spelled disaster for SHOP, and platform churn.

We see something potentially happening with the recent fiscal deficits the Biden administration has been running.

Right now, the U.S. government has been adding $1 trillion to the national debt every 100 days. This fiscal stimulus has been going towards things like CHIPS, which ultimately finds its way into new infrastructure, technologies, etc.

This appears to be longer-tail use of funds, but it's still stimulus, and unless the government can reign it in, there's a fear that SHOP could tumble if the economy takes a turn.

Additionally, this stimulus has re-invigorated multiples in the market, so you're definitely not getting SHOP at a bargain-basement price.

Looking ahead, the key thing to watch is SHOP's growth rate. If it dips, then all bets are off. However, if the company can do well on this front, then the trade remains in play.

We ultimately believe that as SHOP continues to turn the profitability corner, and shares appear to be a compelling investment due to the company's growth trajectory and strong business momentum.

There are risks, but with growing GMV, a more entrenched userbase, and a strengthening brand, we believe that SHOP will likely outperform the S&P 500 over the next 4 years by a significant margin.

Thus, we rate the stock a "Strong Buy".

Cheers!