RonFullHD

RonFullHD

I believe Shoals Technologies (NASDAQ:SHLS) stands up there with some of the best solar energy investments at this time, alongside Enphase. I consider it far outperforming its competition in its areas of expertise. My market analysis reveals this year to be an exceptional opportunity to buy into the long-term growth opportunity in Shoals stock at a significant undervaluation.

Shoals is well-known for its electrical balance of systems (EBOS) technologies for a range of clean energy infrastructure, including storage and EV charging as well as solar. EBOS solutions connect solar panels and other clean energy devices to the electrical grid.

In 2024, Shoals announced an $80 million investment in an effort to expand its U.S. manufacturing capabilities. It intends to relocate operations to a larger facility in Portland, Tennessee, expecting to create 550 new jobs. The expansion, driven by rising demand for solar EBOS products, highlights the firm's commitment to meeting demand. At this time, the firm's total manufacturing capacity has reached 35GW, potentially expanding to 42GW, fulfilling demand through to late 2025.

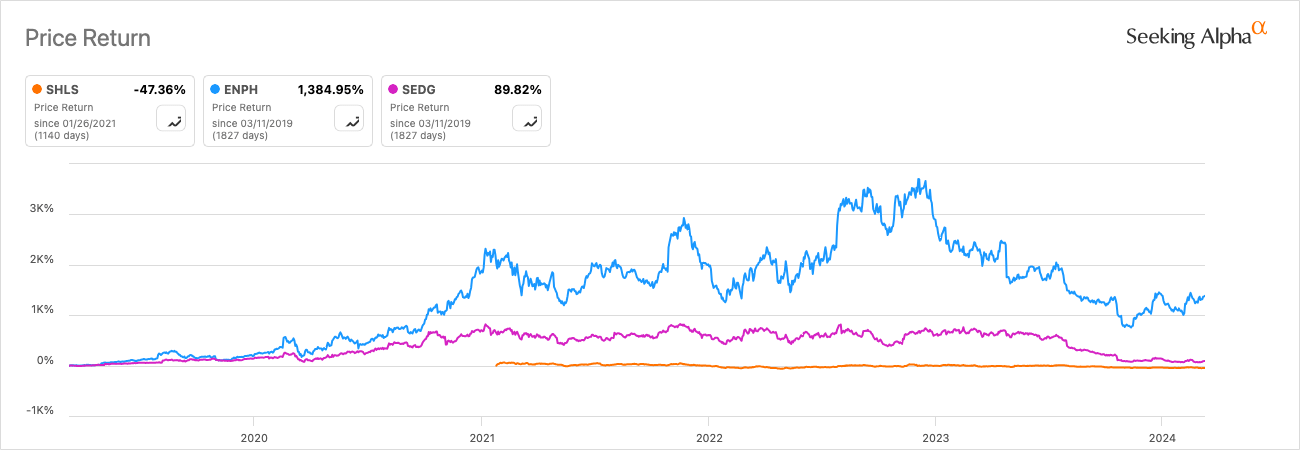

Consider the following graph, which outlines the significant drop in dominant solar energy company valuations over the past year:

Seeking Alpha

This can largely be attributed to supply chain challenges throughout 2022, affecting utility-scale deployments, but also residential, commercial, and community solar segments. Despite continued high demand, there were project delays and increased costs, which affected investor sentiment. Additionally, new tariffs and regulatory uncertainties presented downside risks, rising interest rates affected installer sales activity, and financial product shifts and price increases also contributed to slowing residential growth.

Many official bodies have a positive long-term outlook for the solar market, with cumulative solar installations expected to be five times larger by 2033 than in 2022. However, there are valid concerns surfacing related to market saturation and grid capacity limitations, and growth is anticipated to slow down as market penetration increases.

Despite these challenges, the future looks resoundingly positive when the balance is measured. An increasing number of corporations are joining global initiatives such as the RE100, which aims to procure electricity entirely from renewables. The Inflation Reduction Act and multinational efforts to address climate change are anticipated to boost the solar market throughout 2024, according to Deloitte.

Additionally, the solar sector achieved a decade-long high in corporate funding in 2023, with a 42% YoY increase reported. There was strong growth in private market financing and debt financing despite a decrease in venture capital and a slight dip in M&A due to higher borrowing costs.

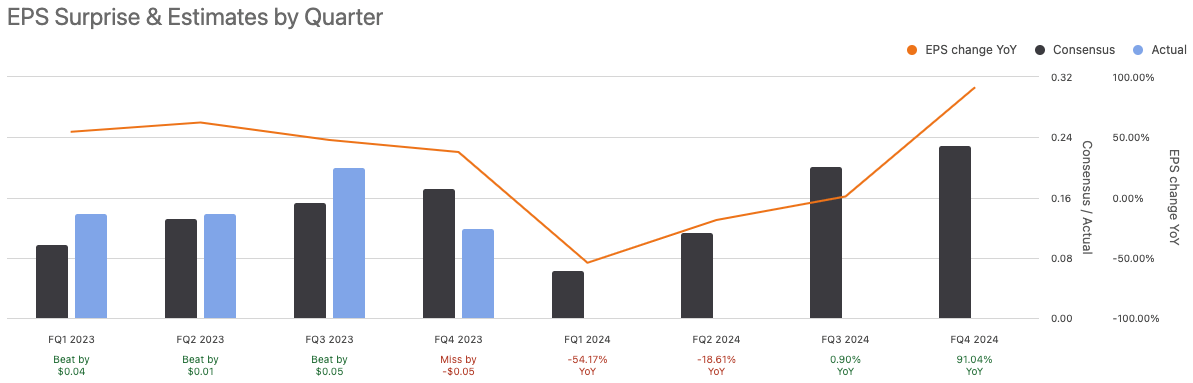

In Shoals' Q4 fiscal 2023 earnings, it missed normalized EPS estimates by -$0.05, and it also missed GAAP EPS estimates by $-0.03. It missed revenue estimates by -$1.74 million. These results all indicate the continued challenge for Shoals during this period of slower and negative growth common in the solar market.

Seeking Alpha

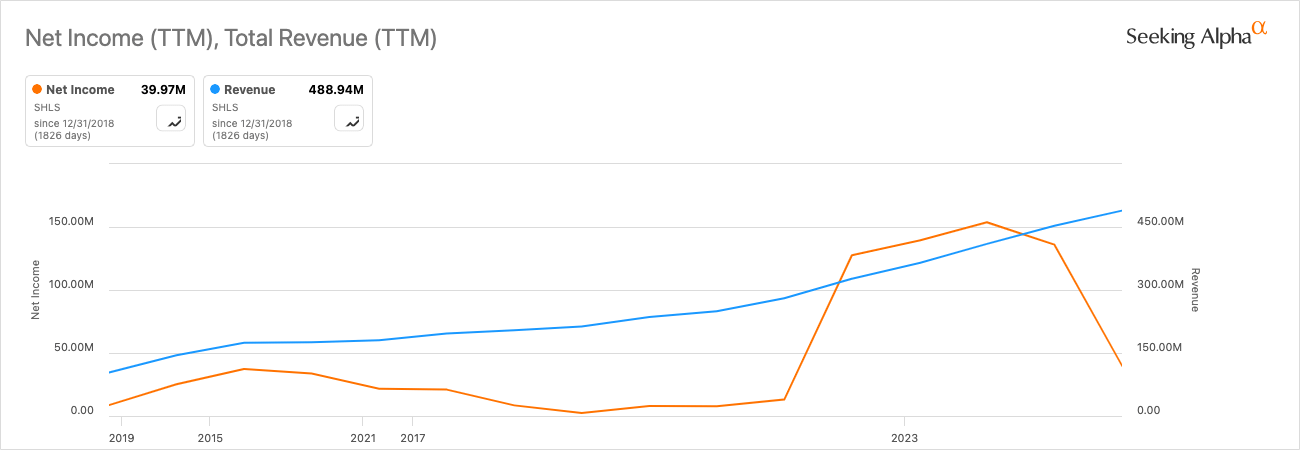

We can also see from the above chart that normalized EPS estimates for the next two quarters are expected to show significant YoY EPS contractions, particularly in the first quarter. However, even though it missed expectations in Q4 of fiscal 2023, it should be noted that its quarterly revenue of $130.4 million was a 38% YoY growth. It has also noted its backlog and awarded orders increasing 47% YoY to $631.3 million.

For the full-year fiscal 2023, its revenue grew 50%, to $488.9 million, compared to $326.9 million the year before, "driven by higher sales volumes as a result of increased domestic demand for solar EBOS," quoted from its earnings release.

For full-year fiscal 2024, the company outlined the following expectations in the recent results:

This indicates an overarching positive for Shoals, despite present concerns around momentum, investor sentiment surrounding the solar market, and valid short-term risks related to earnings estimates revisions, which could result in downside over the next year. Over the long-term, present results and future expectations outlined by the company indicate good long-term growth to resume.

Shoals has remarkably strong top-line growth, but it has less strong profitability at this time. Consider its YoY revenue growth of 49.55% compared to its YoY EPS GAAP contraction of 71.76%.

Author, Using Seeking Alpha

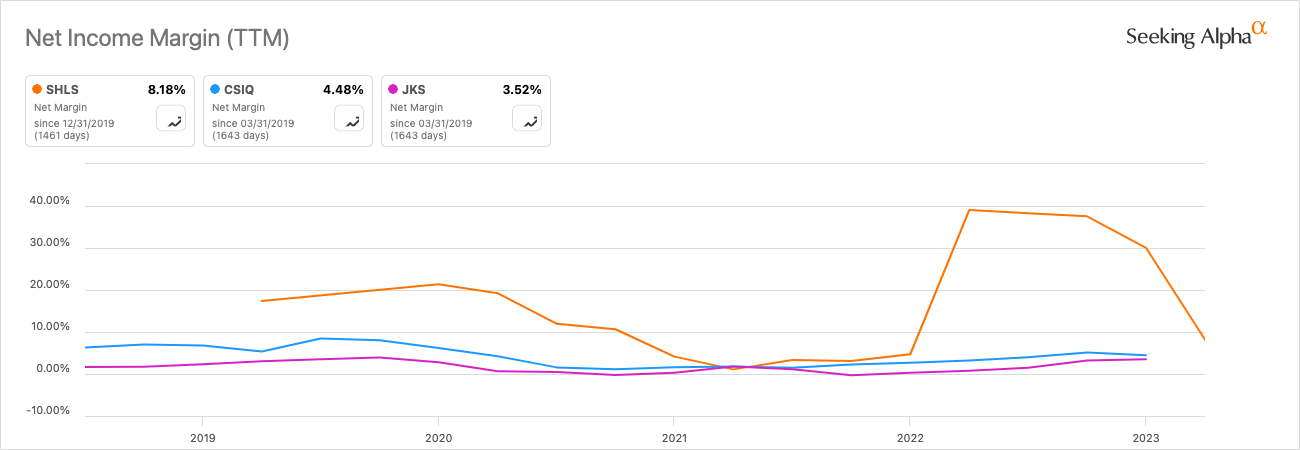

If we compare its net income margin to peers who operate at a similar market cap in solar energy, in areas of operation overlapping with EBOS solutions, we can see how Shoals has the potential for higher profitability but with considerable instability in this over the past five years:

Author, Using Seeking Alpha

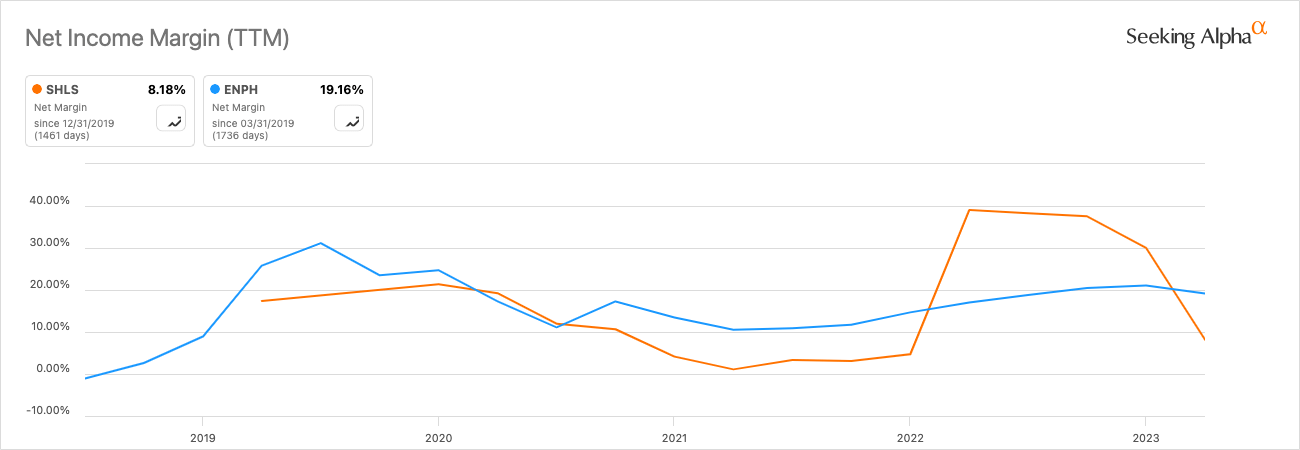

I believe it is also prudent for me to compare Shoals to Enphase (ENPH), which is a company that has significant long-term investment potential and of which I am a shareholder. Enphase shows a more reliable net margin over time:

Author, Using Seeking Alpha

One of Shoals' outstanding features is its equity-to-asset ratio of 0.65, which places it in a strong position in its industry. Compare it to the three peers I have used in my competitive analysis above:

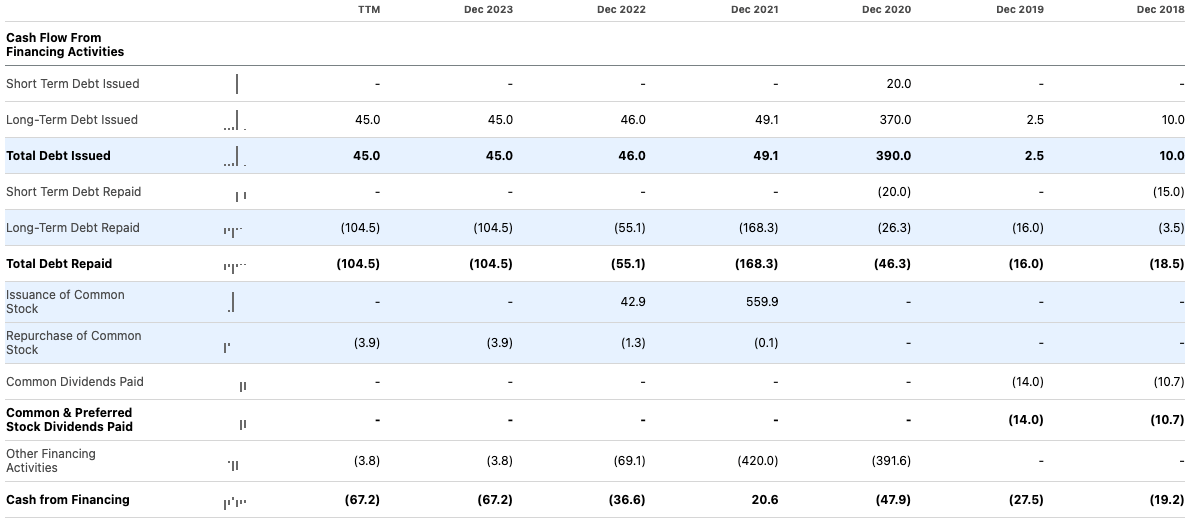

This evidently puts Shoals in a position of significant financial advantage, so I delved deeper into the balance sheet to ascertain just how strong it might be. What I found was a company that looks to me to be careful in how it receives financing, with two notable large financing occasions since 2018; one was a $559.9 million issuance of common stock in 2021, and the other was a $390 million issuance of debt in 2020. Other than this, the company has been very reserved in diluting shareholder value and adding leverage to the balance sheet. In addition, its debt repayments are annual and large following its high issuance of debt in 2020.

Seeking Alpha

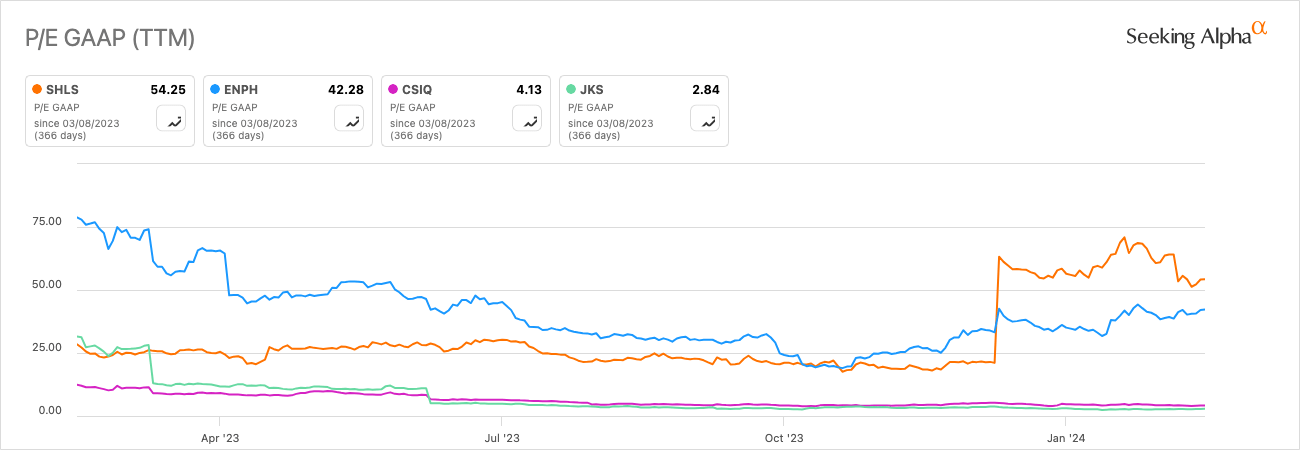

While Shoals is trading at a high price-to-earnings ratio of around 54 based on GAAP, this goes down considerably to around 29 on a forward basis. To start, we can compare its TTM GAAP P/E ratio to the peers I have used in my competitive analysis:

Author, Using Seeking Alpha

Based on this, Shoals is evidently highly valued among solar energy investments, and I believe it has a reason to be trading at a premium to its peers. However, I believe we can arrive at a conclusion of significant undervaluation for Shoals stock at this time based on discounted cash flow analysis.

For example, from my research and confirmed by the World Economic Forum, I have understood that a reasonable market CAGR for solar energy over the next 10 years is roughly 20%. Therefore, I have used this as my conservative EPS annual growth rate for the next-10-year growth stage of my discounted cash flow analysis. While I expect long-term growth to persist beyond the next decade, I have opted for a conservative 4% terminal-stage annual growth rate, in line with inflation, for my 10-year terminal stage following my growth stage. I incorporated an 11% discount rate. My fair value estimate, from a starting EPS of $0.6, is $18.75, indicating a 30.35% margin of safety on the present stock price of $13.06.

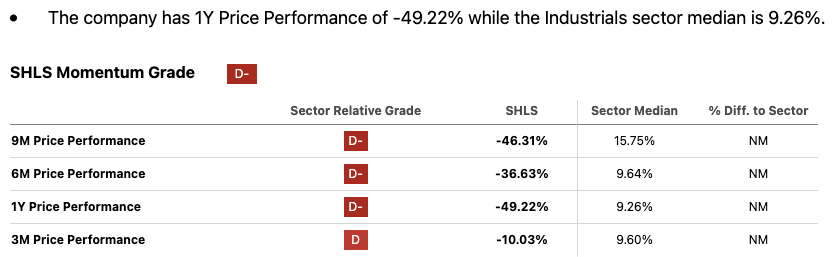

The greatest risk with an investment in Shoals at this time, which is a common theme among all solar energy companies, is its negative EPS revisions and decelerating momentum. This is outlined artfully by Seeking Alpha's quant system:

Seeking Alpha

I therefore believe that investors should be well-prepared for short-to-medium term losses if they invest now. The issue is it is impossible to invest directly at the bottom, but the evidence shows we are somewhere near when you take into account future earnings estimates. As an ultra-long-term investor, I see no trouble in holding through temporary losses for what I estimate will be a long, profitable road to high solar adoption through 2050. I do not believe that solar investing at this time has any appeal for short-term growth and momentum investors. This is a deep-value play, and it should be treated with exceptional patience, dedication, and nerve to hold through what will look like rational points to 'call it quits.'

I believe investing in the solar energy markets comes with significant challenges in the immediate future, particularly as a result of reduced investor sentiment at this time surrounding the sector, but also present difficulties in macroeconomics that are periodically reducing demand. Hence, I think an investment in Shoals is not great for short-term investors. I believe lifelong holders will make the highest profits from the best solar energy stocks, particularly when bought at this time when the market is so significantly undervalued.

However, Shoals will likely face periods of difficulty as government subsidies in the sector increase and reduce under specific leadership. I believe a Republican win with Trump reinstated will significantly reduce the sentiment and financial results of solar stocks at this time. However, investors with a long-term horizon like me could see this as an opportunity to buy more shares, as over time, I see it as almost inevitable that solar will take a front role in energy provision across the globe. However, the journey there is likely to have some significant volatility at times, as we have seen over the last year.

This could be a very rare opportunity, and Shoals' operations and financial health position it to be a value investment worth making. I already own Enphase stock, but Shoals is one of the next solar companies on my list to take a stake in.