Robert Way

Robert Way

At the Lab, we've been closely monitoring the OPEC+ Decision and its profound impact on the Oil Major, a topic of significant importance in the industry. Today, we are back to analyze Shell plc (NYSE:SHEL) (OTCPK:RYDAF), but before moving on to additional company key takeaways, it is vital to report the latest update on oil.

As a reminder, to avoid a global glut, OPEC+ decided to extend oil production cuts by around 2 million barrels per day (2% of global crude oil production) by 2024-end. This extension comes in response to increased output from non-cartel Countries. What's new to price is that Russia, Iraq, Kuwait, and Algeria will likely reduce their respective production by 417k, 220k, 135k, and 50k barrels per day. In addition, Saudi Arabia had already announced its intention to support its economic transformation plan with an oil production cut extension. Furthermore, there are exogenous shocks on potential supply disruptions. Last week, Ukraine knocked out a Russian refinery in a major attack. This attack was carried out by a drone that hit Rosneft's largest oil refinery.

To support the oil price, we should also report the following: 1) economic growth forecasts for the current year have also been revised upwards, and 2) industry data showed that US crude inventories unexpectedly fell by 5.521 million barrels last week amid rising demand from the world's largest oil consumer. Brent price already reached our yearly level; however, following the above news, we believe the oil price will likely stabilize at around $80 per barrel.

Aside from the above MACRO implication, our Shell buy rating was supported by 1) the company's capital allocation priorities, 2) investments toward green projects with already earnings in the renewable segment at $705 million in 2023, 3) a cost-saving plan, and 4) supportive remuneration.

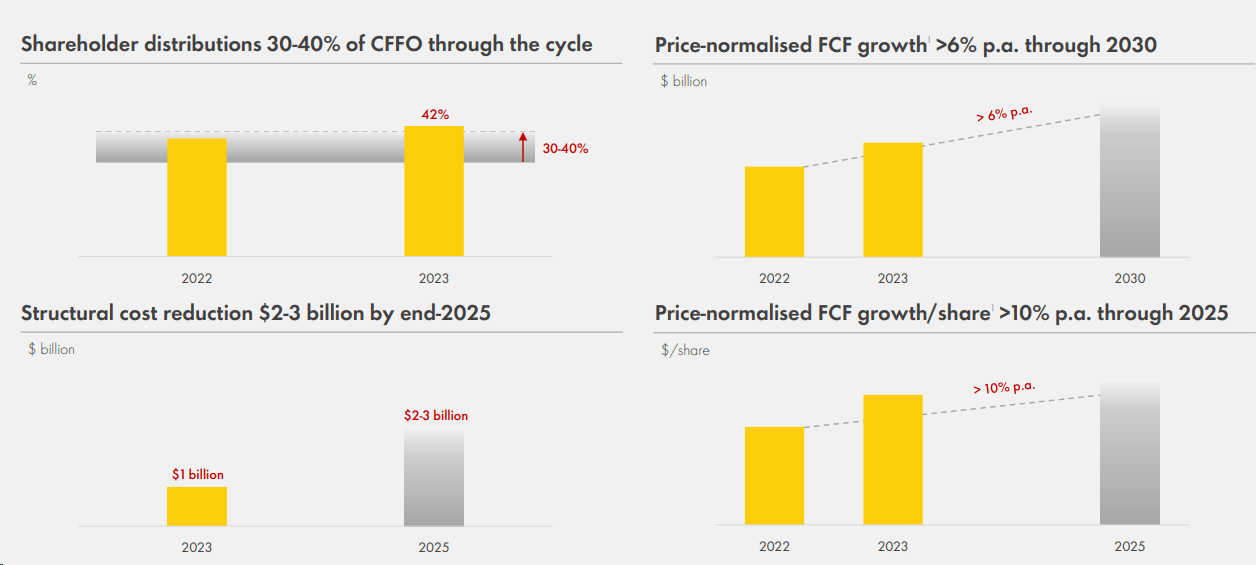

Key assumptions need to be changed after the Q4 results. These new outputs are well represented in Fig 1 and confirm Mare Evidence Lab's equity investment story.

Shell Upside in a Snap

Source: Shell Q4 results presentation - Fig 1

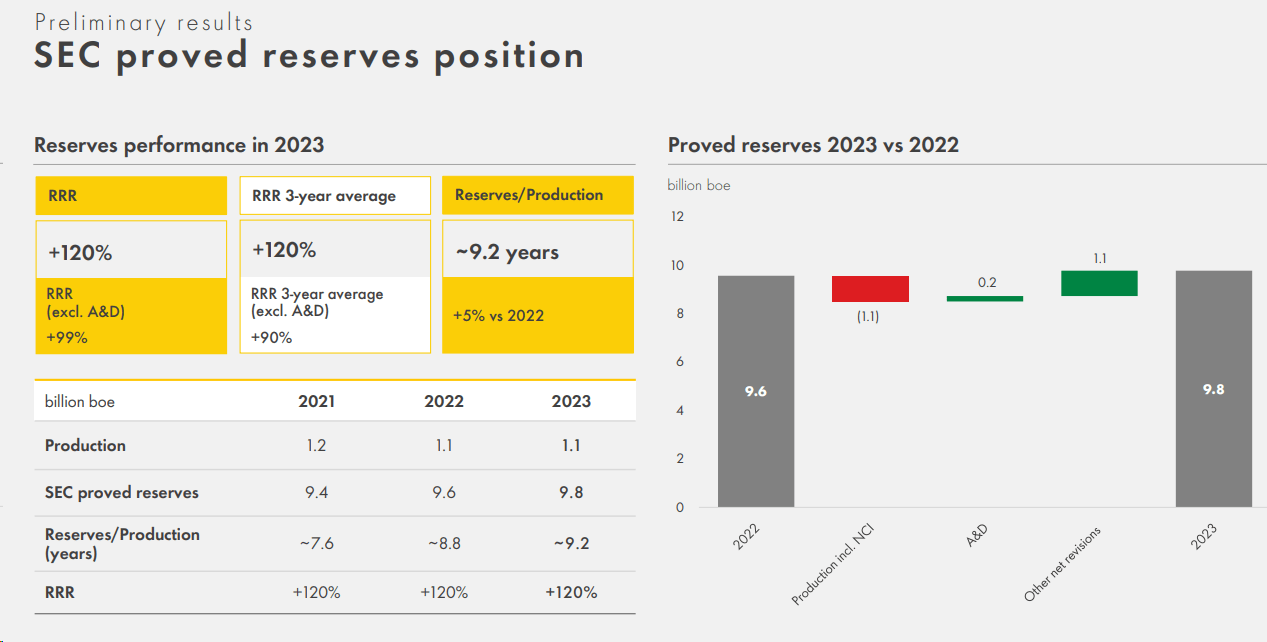

Shell reserve evolution

Fig 2

Considering the MACRO oil consideration following the latest OPEC+ decision and factoring in Shell's higher-than-expected cost savings, we decided to change the company's estimate and increase our target price. We also update our model to reflect Shell's project timing and portfolio changes. We have increased our CFFO estimates by 2%, and our earnings forecasts have increased by 4% in 2024-2026. On Shell's bottom line, we arrived at a net income of almost £19.29 billion with an EPS of £310p. We incorporated CAPEX at the lower end of Shell's outlook. In our estimates, we projected an investment of $23 billion (£18.25 billion).

The company has an attractive valuation, with a Brent oil price barrel at $85/$80 in 2024 and 2025. With the above Brent estimates, the Oil Player trades on a 16% FCF yield. This is higher than its EU competitors, such as Total (9%) and Eni (11%). On average, US peers trade at an FCF yield of 11%. Despite that, we should consider that the company has a lower dividend yield of around 5%, while the sector is above 6%. That said, Shell has a sector-leading buyback yield of 7%.

Going to the valuation, on a reverse basis, Shell is trading at an 8x P/E while its peers are above 10x. In our peers' P/E analysis, we report that Eni, Exxon, and Chevron are trading at 10.04x, 12.72x, and 13.6x, respectively. Therefore, applying a 10x P/E multiple, we increased Shell's valuation to 3,100 pence ($75 in ADR). In the long view, there is an upside to Namibia divestments and LNG long-term contracts, which protect the company from spot market volatility.

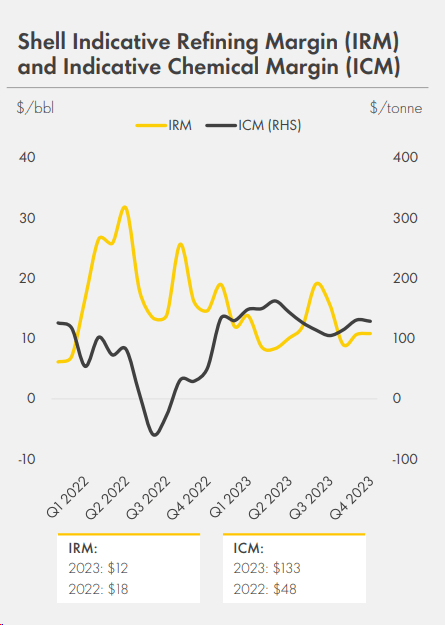

Downside risks include 1) failure of the $25 billion asset divestment program, 2) value disruptive M&A to fund renewable energy capacity, 3) a lower Brent oil price, 4) refining margin crack-spread volatility (Fig 3), and 5) higher than expected CAPEX with its related execution risks.

Refining margin volatility

Fig 3

Our team confirmed Shell as a top pick in the European integrated oil & gas sector. The fiscal year 2023 results and Q4 performance confirmed our investment thesis, and we see Shell as a capital discipline leader within the industry. With oil above $80 per barrel, Shell will be able to remunerate shareholders while continuing to deleverage. We positively view the acceleration of its start-up activities in Canada as well as its ambition to reduce OPEX costs. In addition, with higher reserve, the company removed an overhang for the stock. Attractive valuation and tasty remuneration make Shell a long-standing buy.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.