skynesher

skynesher

I wrote about Semrush Holdings (NYSE:SEMR) previously with a buy rating as I believed it could continue to see 20% growth as it continues to see pricing expansion and move towards capturing more enterprise-level customers. I reiterate my buy rating for SEMR as the momentum continues to stay very strong in this business. Management's FY24 guidance also continues to point to 20% growth ahead, similar to my expectations. More importantly, SEMR showed strong traction in penetrating the upmarket segment and also improving profitability, which I see as catalysts that could drive valuations upward.

Impressive 4Q23 earnings reported by SEMR, where revenue grew 21.2%, driven by new customer additions and the expansion of ARPC as SEMR continues to execute on their cross-sell and up-sell strategy. Gross margins also expanded 100bps Y/Y to 83.6%, which, coupled with good opex management, led to positive non-GAAP EBIT margins of 8.7%. Consequently, this led to a strong adj. EPS performance of $0.08. On the cash flow side of things, because of strong topline performance and cost management, SEMR managed to generate positive operating cash flow of $11.6 million, which is a big step up in margin from -14.1% to 13.9%, which helped SEMR end the year with a net cash balance of $237.3 million.

The strength of SEMR growth continues to be strong, and I expect a strong year ahead as well. The two key metrics that I monitor are ARR and ARR per customer, which both showed very strong momentum. For ARR, 4Q23 ARR came in at $337.1 million, which saw growth accelerate to 23% vs. 21% in 3Q23, marking the second consecutive quarter of ARR growth acceleration. To give a better context of why this shows really strong momentum, note that 4Q tends to be seasonally weaker for SEMR as its SMB customers typically slow down spending in 4Q and increase in 1Q. As such, the fact that ARR actually accelerates really shows how strong the demand is for SEMR products. Assuming no major churn, 4Q23 $337.1 ARR also implies FY24 will grow at least by ~10%, which is more than half FY24-guided growth.

Looking at the first quarter, we are off to a strong start with respect to net new customer additions, as we're seeing a similar seasonal pattern to previous years where customers that paused their subscriptions in Q4 returned to the platform in Q1, a trend we attribute to the holidays. Company 4Q23 earnings

The second metric, ARR per customer, also points to very positive traction in capturing enterprise-level customers. In 4Q23, ARR per customer growth accelerated in the quarter, from 6% growth in 3Q23 to 8% growth in 4Q23, ending the year with an ARR per customer of $3,121. Although part of the growth was helped by the price increase implemented in 3Q23, if we read in between management comments, it suggests that they are capturing larger customers (upmarket). In particular, they pointed out that SEMR is focused on targeting companies with larger marketing departments, and that this group of customers generate double-digit ARR and have a far higher ARPU than the average customer. I would also think that the fact that SEMR was able to grow ARR per customer while adding fewer customers vs. last quarter (1.2k vs. 2.8k net adds) suggests that they are seeing success in either (1) cross- or up-selling their products into the customer base and/or (2) penetrating the upmarket.

Another side note relating to ARR per customer is that I see potential for more price hikes that would be very positive for margin expansion. As I noted above, in 3Q23, SEMR raised prices on new customers and a small cohort of existing customers. So far, the response has been positive. Management has noticed that the response has been exceeding expectations, and customers are generally willing to pay a premium for the products because of the value they get from the platform. This gives me confidence that SEMR will be able to continue raising prices (which, by the way, is not being reflected in the guidance today.)

I also really liked how SEMR performed at the bottom line, as it reported very strong profit improvement, suggesting that growth did not come at the expense of cash burn. Notably, SEMR continues to sustain strong gross margins, and that margin expansion at the EBIT line indicates SEMR's ability to realize strong operating leverage via a larger revenue scale. From here, I believe EBIT and net margin will continue to expand, and I do believe that the guidance for 10–11% EBIT margin is possible for FY24.

May Investing Ideas

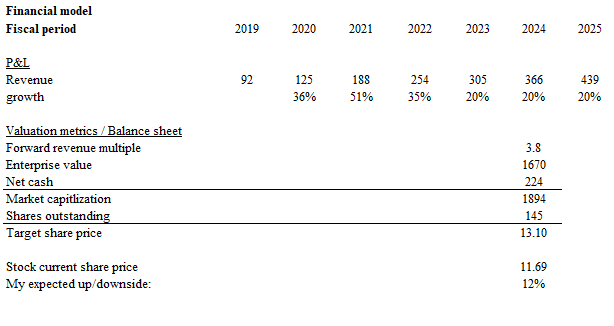

Based on my research and analysis, my expected target price for SEMR is $13.10 in my base case.

In my previous post, I talked about the price increase and macro risk, which I think still exist today. An additional risk I like to note is the impact of the Fed rate cut. I believe a majority of investors are looking for rates to be cut this year, which will help drive asset prices up. However, given the sticky inflation and low unemployment rate, my worry is that the Fed might not cut as much as what the market expects (the expectation now is for a 3 cut, or 75 bps). If so, SEMR could see heavy pressure on valuation given that it is still not generating meaningful cash flow.

I give a buy rating for SEMR due to its impressive momentum, upmarket traction, and improving profitability. Revenue grew 21.2% in 4Q23, with ARR growth accelerating to 23%, ARPU expansion indicate also successful cross-selling and up-selling strategies. Notably, profitability and cash flow margin has seen strong improvements. As for valuations, my base case target price of $13.10 based on continued 20% revenue growth and current valuation multiples. However, I do see upside potential if SEMR continues to show profitability improvement, which should help close the valuation gap between itself and DV.