andresr/E+ via Getty Images

andresr/E+ via Getty Images

After a fiscal year 2022 where margins were compressed due to high inflation and growth slowed a little bit, Select Medical Holdings (NYSE:SEM) has reported a 2023 that invites optimism, since it seems that margins have already stabilized, and prospect for growth is on the horizon again.

According to the most recent guidance, the company would be trading at a Forward PER of between 12 and 14x. A more than compelling valuation for a company with such a reliable business model.

Select Medical operates specialty hospitals and outpatient rehabilitation clinics, which are focused on providing care for patients with complex medical conditions who cannot be treated in a common hospital, since their problems are rather specific and usually require prolonged periods of treatment. The company operates nearly 2,800 hospitals and rehabilitation centers under numerous brands, such as Select Specialty Hospitals, Concentra, NovaCare, among many others, making it one of the largest players in the industry.

Select Medical Family Of Brands (Select Medical Website)

The main thing that makes this business model appealing, in my opinion, is that patients who come to these centers are usually willing to pay whatever it takes since their problems require immediate and specialized attention. Moreover, clients typically seek the center with the best reputation, patient care, and expertise. This makes a price war unlikely, instead, all of SEM's competitors would aim to compete by offering the highest quality, which prevents the company's margins from being compressed by competitors.

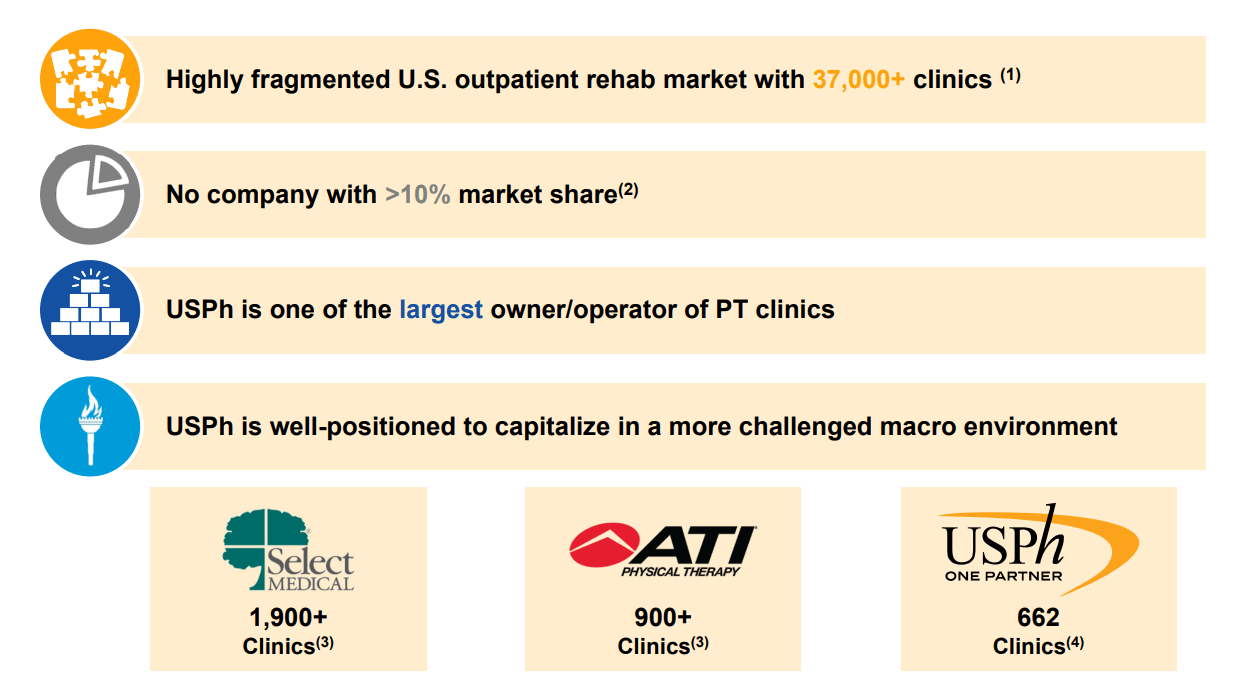

Also, the market for treatment centers and hospitals is pretty fragmented, with lots of small regional or family-run competitors and no company owning more than 10% of the market share. This presents an opportunity for consolidation, allowing the industry's largest competitors to buy smaller, less profitable companies at low prices and blended in to increase their occupancy rates, thanks to the national scale of Select Medical, which would ultimately improve its profitability. Basically, the chances for growing inorganically are quite interesting, but also a growing and aging population, combined with a higher prevalence of chronic conditions, can contribute to organic growth too and according to a study by Grand View Research, this market is expected to continue growing at rates of 7.5% annually in the coming years.

Competitive Landscape (USPh Investor Presentation)

The company's revenue has grown 9% annually in the last decade, and although we cannot consider it as high growth, it's really sustainable and stable. In fact, since 2008 there has not been a year in which the top line stopped growing, which tells us about an extremely resilient business.

In terms of margins, we can observe quite a bit of stability in EBITDA too, except in 2022 where the inflationary environment led to an increase in labor and other operating costs, however, these seem to be stabilizing, and the margin returned to 11.5%, close to the 12% average.

Author's Representation

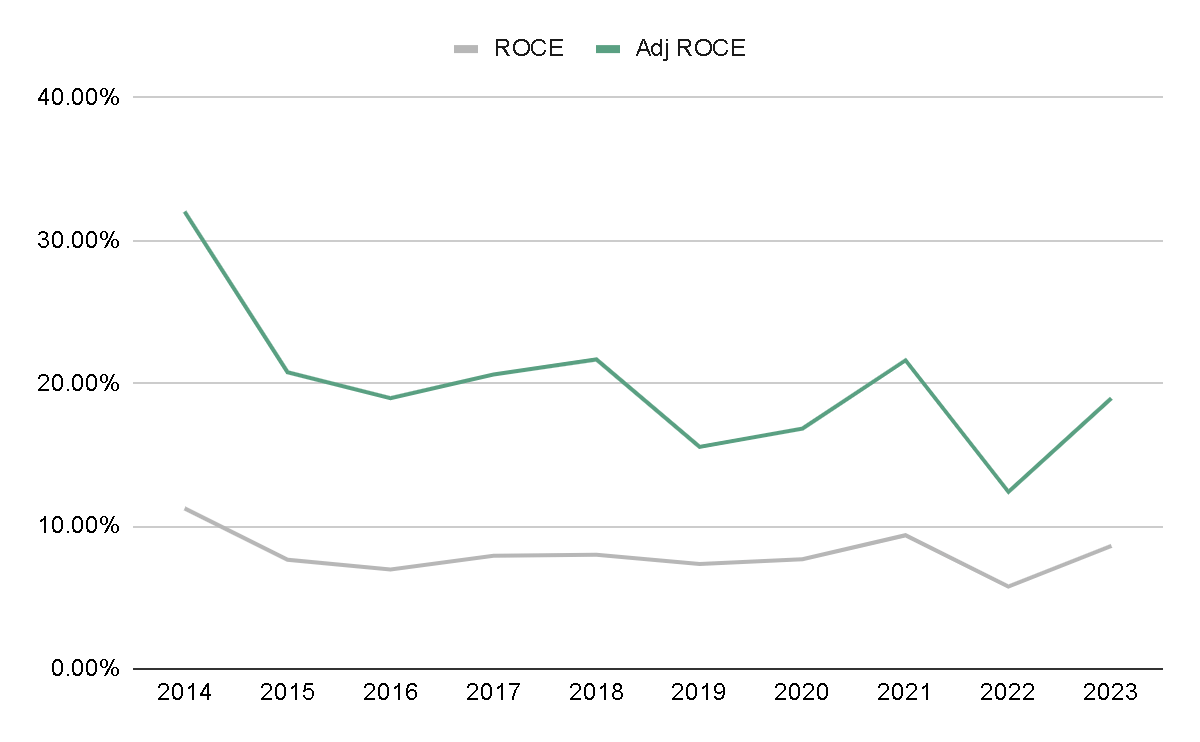

Moreover, the company is quite profitable, achieving returns on employed capital between 7% and 9%. Although this ratio may not seem exceptionally high, we must remember what I mentioned earlier about growth opportunities through acquisitions. These acquisitions end up creating goodwill on the balance sheet, which distorts profitability.

If we adjust this ratio by excluding goodwill, assuming a scenario where the company ceased acquiring companies regularly, the ratio would have averaged 20% over the last decade. This is a highly profitable business.

Author's Representation

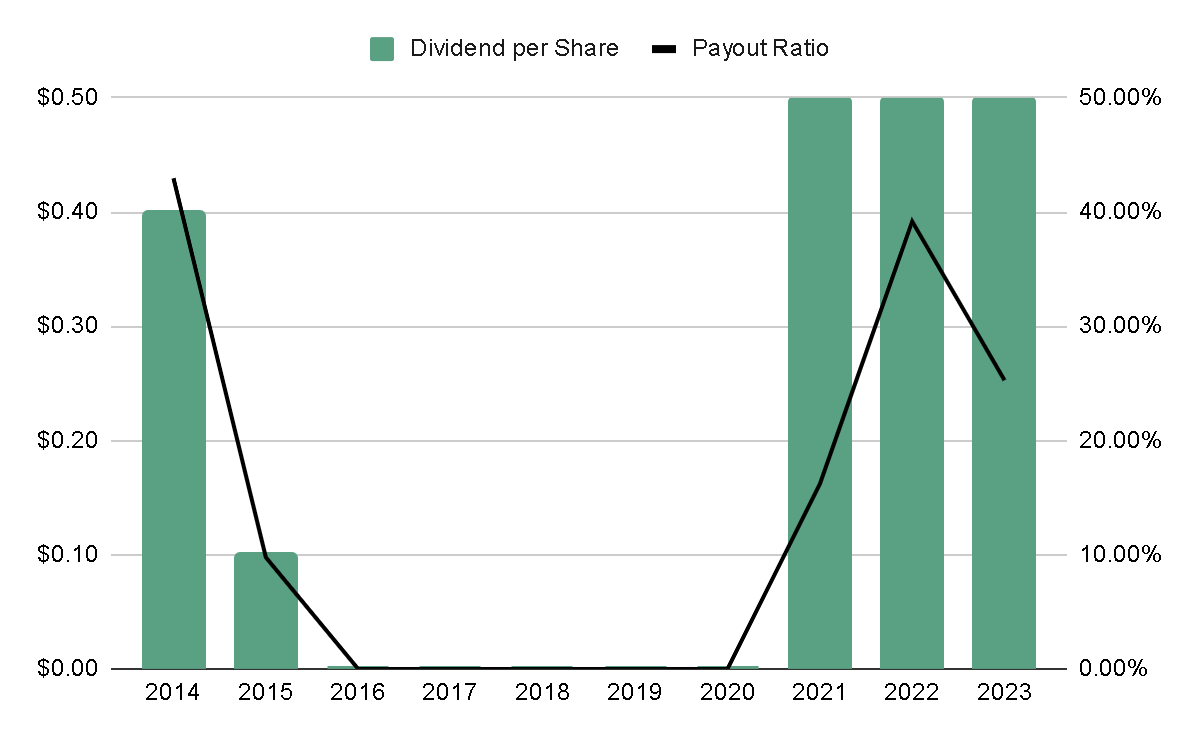

Currently, the company pays a dividend with a yield of 1.8%, which is appealing and only represented 25% of the Net Income of 2023. However, management isn't very interested in maintaining or growing this dividend, and it's more of a source of returning value to shareholders occasionally and as long as the company doesn't see another way to allocate that capital

Author's Representation

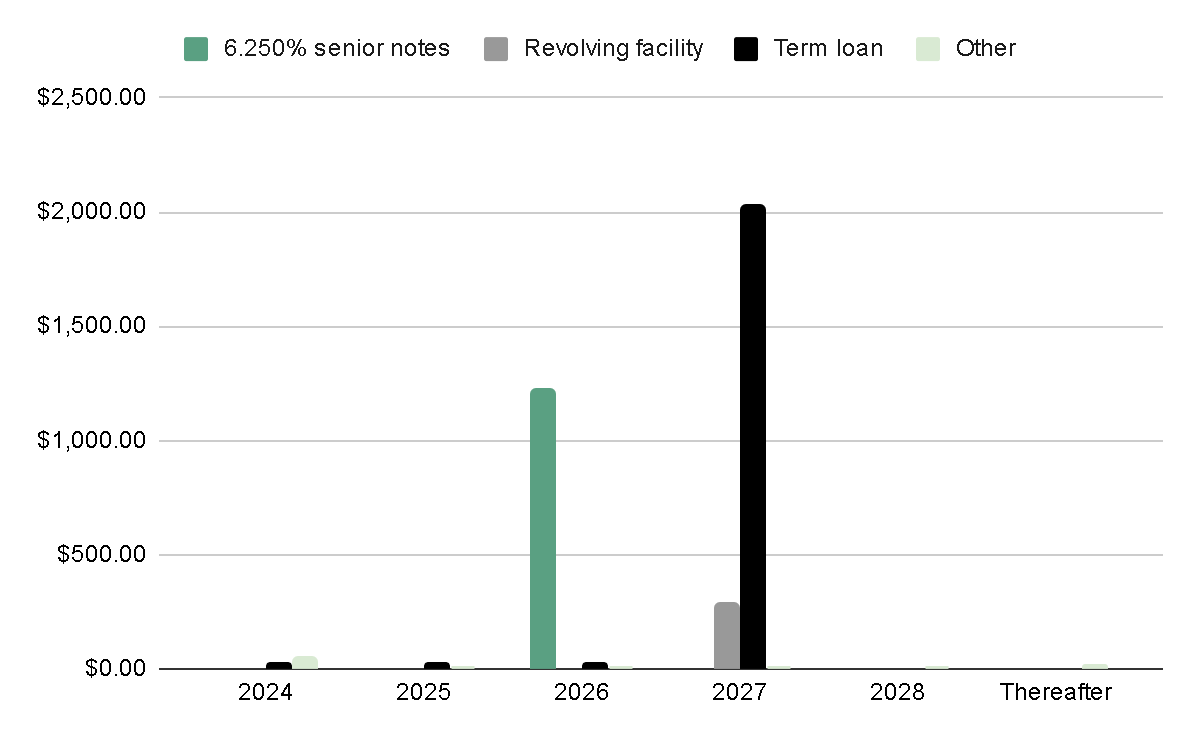

Now, delving into one of the aspects that raises the most concerns, from my point of view: The indebtedness.

The company has heavily relied on debt to finance its growth in recent years, in addition to being quite intensive in leases. This has meant that it currently has $3.66 billion in debt and $1.67 billion in leases, while cash and equivalents don't even reach $100 million and the EBITDA generated is $760 million, representing a Net Debt/EBITDA ratio of more than 6x.

In situations like these, I think that beyond simply looking at a basic leverage ratio, it's best to review the debt structure to evaluate how risky it is for the company to maintain these levels of debt.

Author's Representation

Digging deeper into the debt structure, 97% of it is in a term loan and senior notes, with maturities ranging between 2026 and 2027. This implies that the company has a window of two to three years to explore ways to reduce leverage levels before needing to renegotiate the debt.

In my view, while maintaining these levels of leverage is a risk, there seems to be room for maneuver. Being a company with such predictable cash flow, I think that there'll be ways to meet debt obligations. Additionally, insiders hold 20% of the company's shares, so there's skin in the game and I don't believe they would be happy if the company faced bankruptcy due to excessive debt, risking the loss of their assets.

Author's Representation

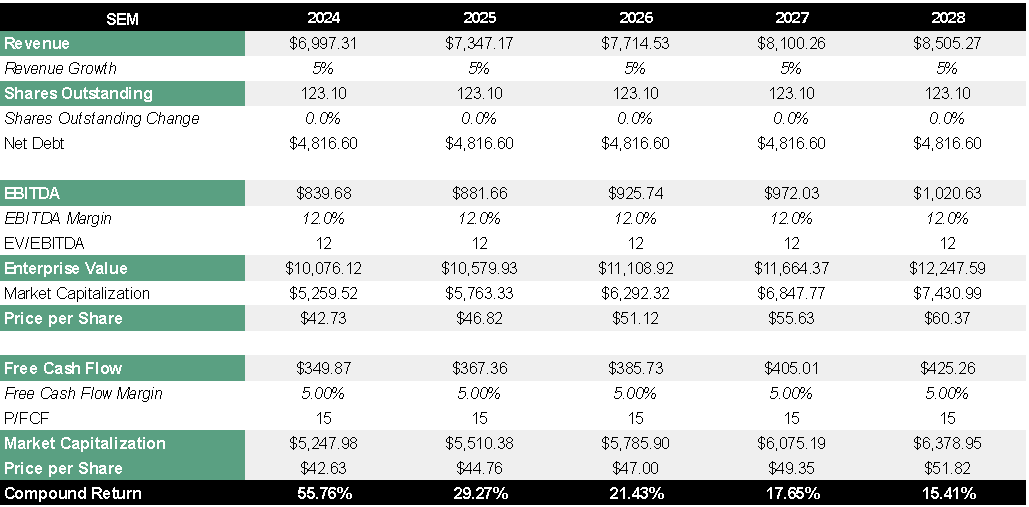

To get an idea of what return we could expect if we bought the company at the current price, I'd like to make a projection of revenue and profit margins and then apply a valuation multiple based on historical multiples of the company and its close competitors.

Regarding top line growth, I believe assuming 5% annual growth is quite conservative but realistic. In fact, management's expectation is to grow approximately that (reaching $7 billion in revenue) with EBITDA margins back to the usual 12%.

We are issuing our business outlook for 2024 and expect revenue to be in the range of $6.9 billion to $7.1 billion. Adjusted EBITDA is expected to be in the range of $830 million to $880 million.

I don't foresee that there will be aggressive buybacks and the dividend could even be cut at any time, due to the fact that there're very important debt maturities in 2 and 3 years. With these assumptions, the expected return would be around 15% per year, so it seems to be an attractive investment option.

Author's Representation

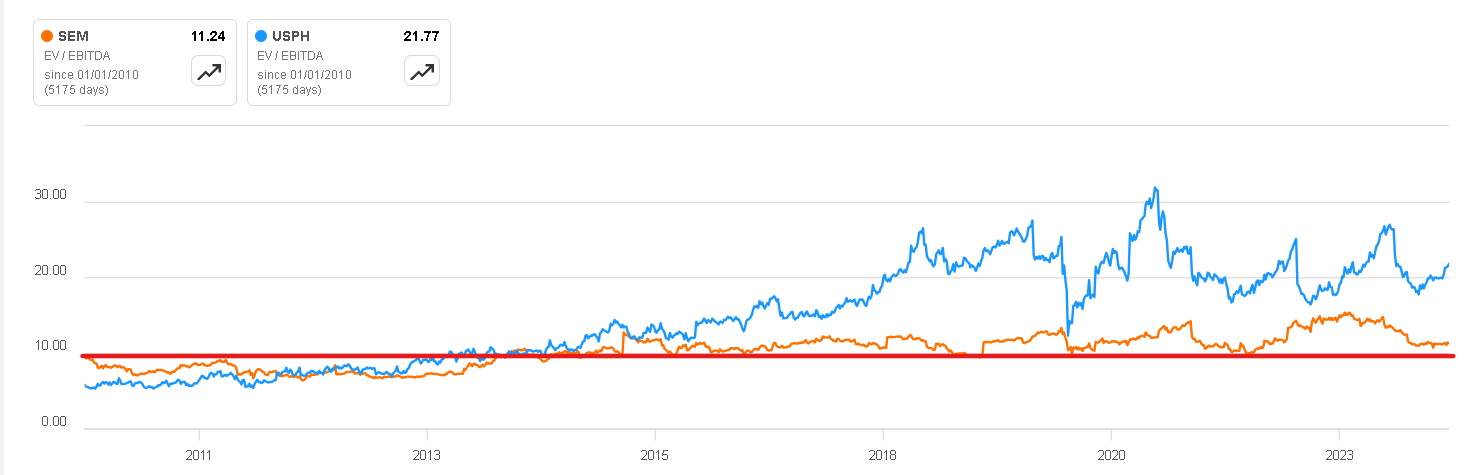

As I mentioned previously, I made the choice of the multiple of 12x EBITDA and 15x Free Cash Flow based on the average multiples since 2010. In the case of SEM, these are usually above 10x EV/EBITDA and although USPh is usually quoted at double from this, I think debt risk causes SEM to maintain a lower valuation multiple.

EV/EBITDA Multiple (Seeking Alpha)

The first and most obvious risk is that of debt. The company has significant levels of leverage and although in the last 10 years the average Net Debt/EBITDA Ratio has been 6x, I think that in an environment like the current one, with high interest rates, staying this indebted is not so healthy. Even so, with the recent signs of interest rate cuts coming in the next twelve months, we could consider that maybe the worst is over and from here on, this risk would decrease as rates fall, and the company can access cheaper debt.

Another aspect that I do not know if it is a risk as such, but it is a less attractive characteristic of the sector, is the fact that numerous clients usually come from government-sponsored healthcare programs such as Medicare and Medicaid, in which there is usually greater regulation regarding the payments that Select Medical can make to its clients. Therefore, I do not expect the company's margins to expand by any means, since profitability is usually subject to government restrictions.

In my opinion, the company operates a business that is simple to understand, but with solid competitive advantages and sources of future growth, both organic and inorganic, while already being one of the largest competitors in the country. Furthermore, the current valuation appears to be reasonable for the quality of the business, trading at a P/E of 14x.

While there are risks, some quite significant, from my personal perspective, the company should be able to do well in the coming years. For all this, I have decided to assign it a 'buy' rating, although I would understand those who don't feel comfortable entering right now.