Roman Mykhalchuk

Roman Mykhalchuk

March 19 was a pretty big day for shareholders of International Paper Company (NYSE:IP). Shares of the company spiked around 11%, even hitting a 52-week high. Due to declining fundamentals, the last year or so has been rather painful for investors. Since I last wrote about the company in an article wherein I rated it a ‘buy’ that was published in April of 2022, shares are down 10.2%. By comparison, the S&P 500 has seen upside of 23.4%.

The move higher was in response to news that the company is naming a new CEO. This follows a long evaluation process where the company vetted some untold number of candidates. The individual in question, Andrew Silvernail, has a phenomenal track record in business leading up to this point. And it seems as though the hope of the market is that this change in the top brass will lead to an improvement in the company's overall performance. The firm has already been undergoing a transformation aimed at boosting its bottom line and positioning itself for long term growth. So it will be interesting to see to what extent this plan changes. But I would posit that, even without any improvements from here, shares are cheap enough to warrant upside. So it is with that in mind that I have decided to reiterate the ‘buy’ rating I assigned the stock previously.

According to the press release issued by International Paper on March 19, the board of directors for the business has decided to make Andrew Silvernail the new CEO of the company, effective May 1 of this year. He will succeed the current CEO, Mark Sutton, who had previously announced that he would be leaving the enterprise. Silvernail has an extensive work history. For instance, immediately prior to this position, he was employed at KKR & Co, Inc. (KKR), which is a global investment firm that engages in private equity, real estate investing, and other activities. It focuses largely on acquisitions, leveraged buyouts, managed buyouts, various Special Situations, distressed opportunities, turn around opportunities, and much more. In recent years, much of its efforts have been focused on technology. But the company has engaged with every sort of company ranging from grocery stores to beverage providers to brokerage houses to airports and more.

To be clear, there is nothing in the press release that suggests to me that this could open the door to KKR coming into the picture for a potential buyout or something of that sort. However, the market is likely interpreting that as some non-zero probability. Prior to serving as an executive advisor at KKR, Silvernail served as the Chairman and CEO of Madison Industries. And before that, he was Chairman and CEO of IDEX Corporation (IEX) from 2011 to 2020. IDEX, for those not aware, is an $18.2 billion applied solutions business that provides customers technologies related to fluid and metering activities, health and science applications, fire and safety, as well as other diversified, products, and more. Under his leadership, the company generated a total shareholder return of more than 500%. Silvernail has held other positions as well, but you get the idea. He comes as a highly experienced executive that knows how to create value.

Author - SEC EDGAR Data

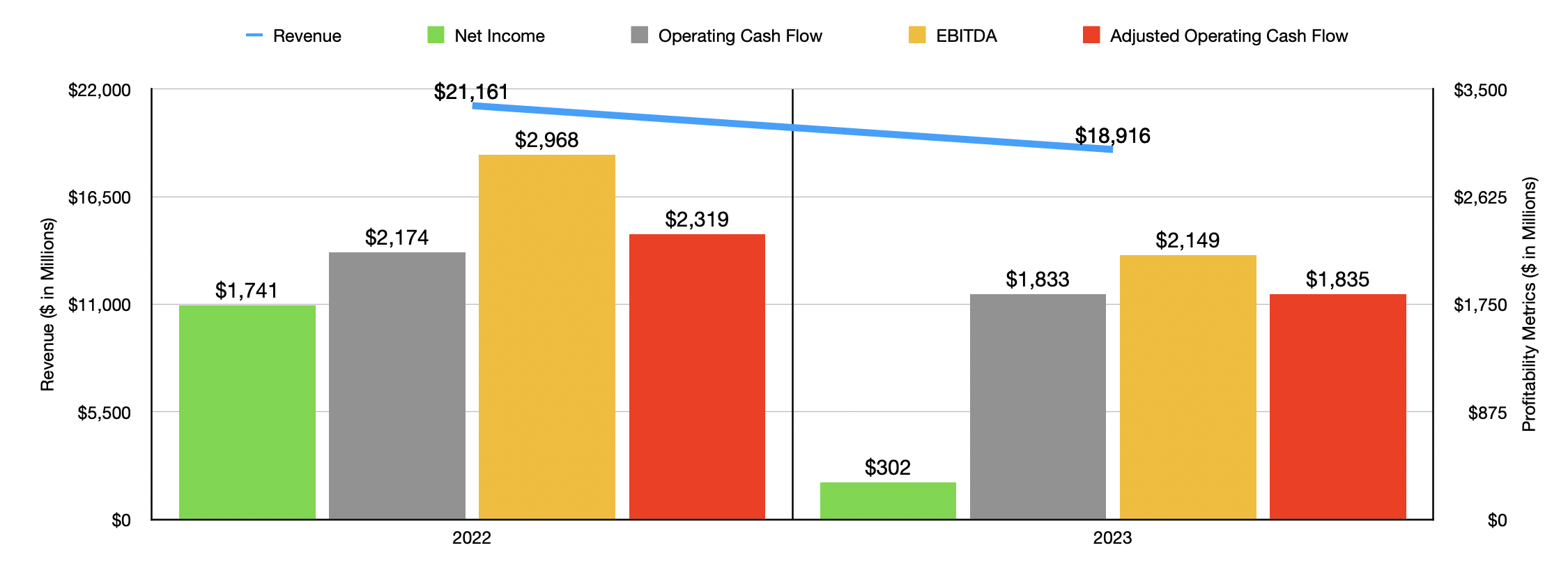

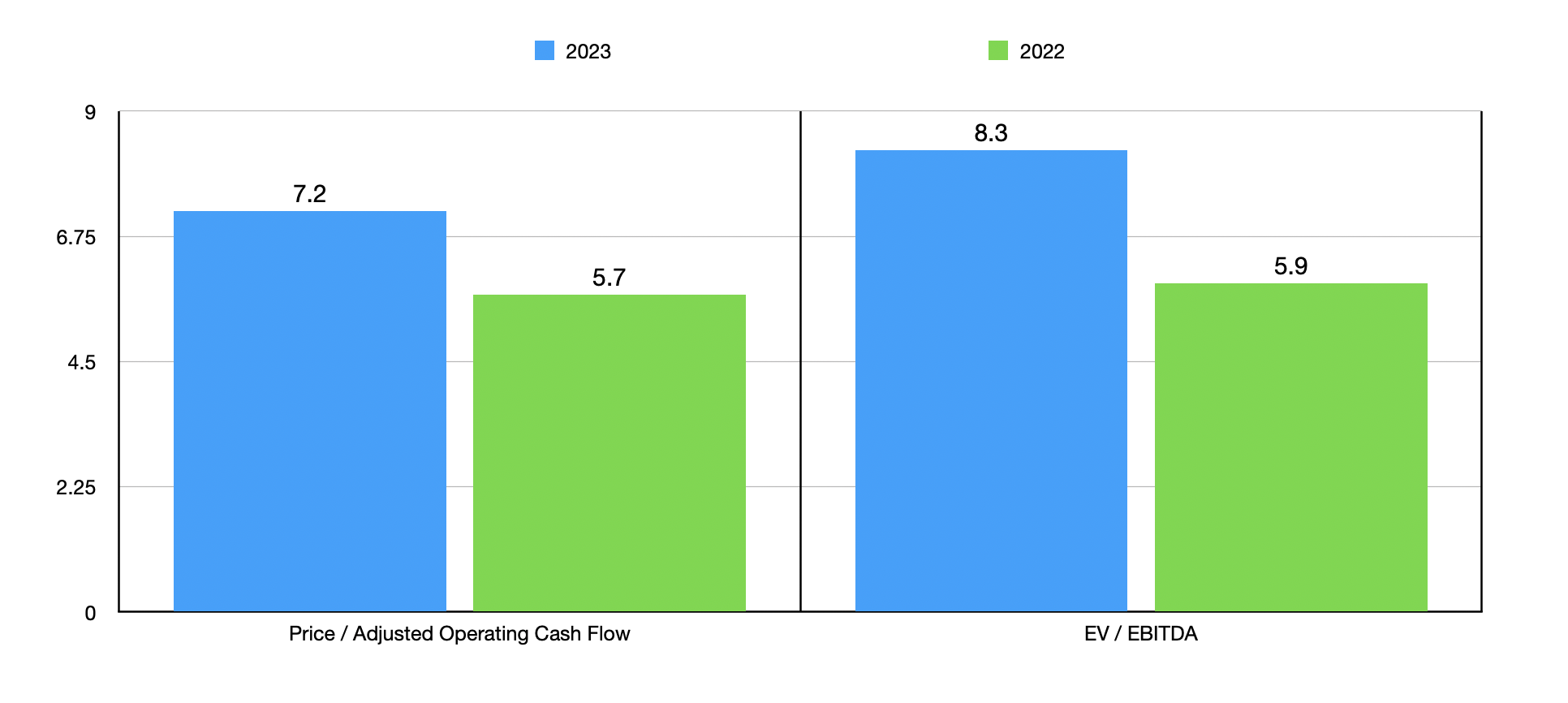

What happens next will be very interesting in my opinion. I say this because, due to weak financial performance, International Paper has consistently underperformed the market for well over a year. This has been driven by weak fundamental performance. Consider the 2023 fiscal year compared to 2022. Revenue in 2023 came in at $18.92 billion. That represents a decline of 10.6% compared to the $21.16 billion generated one year earlier. Much of this downside was driven by the firm’s Industrial Packaging segment.

The North American Industrial Packaging unit for the company reported revenue of $14.29 billion in 2023. That's a decline of 10.7% from the $16.01 billion generated one year earlier. Management attributed this to lower prices for both container board and corrugated boxes. An unfavorable geographic mix impacted sales, and sales volumes decreased for corrugated boxes because of soft demand driven by a reduction in consumer spending on non-discretionary goods and services. Retailers and manufacturers reduced inventory levels as well in order to reach a degree of normalization following a couple of years of elevated inventories that were built up to address supply chain issues. The EMEA (Europe, Middle East, and Africa) Industrial Packaging unit reported an even steeper decline of 11.1% from $1.57 billion to just under $1.40 billion. With the exception of corrugated boxes, which experienced higher sales prices year over year, all of the same factors that impacted the company’s North American operations impacted operations here as well.

The other segment that we need to look at is the Global Cellulose Fibers segment. Revenue for it totaled only $2.89 billion in 2023. That's 10.4% lower than the $3.23 billion generated one year earlier. A reduction in sales volume that was driven by customer inventory de-stocking was the primary culprit here. The company also dealt with, as part of this, higher maintenance and economic downtime that results in about 507,000 short tons of lower output being produced last year compared to the year prior.

With the drop in sales, profits and cash flows also took a hit. Net income plummeted from $1.74 billion to only $302 million. I would argue, however, that the earnings picture is rather deceptive. In 2023, for instance, the company's bottom line was negatively impacted to the tune of $412 million because of net special items charges. It also suffered to the tune of $41 million for non-operating pension costs. By comparison, in 2022, the company's bottom line benefited to the tune of $429 million from net special items income. This was on top of $144 million of non-operating pension income. A better metric to workout would be cash flow. When looking through the lens of cash flow, the picture for 2023 was still negative, but at least it was substantially better than when looking through the lens of profits. During 2023, International Paper generated operating cash flow of $1.83 billion. That was down from the $2.17 billion generated in 2022. If we adjust for changes in working capital, we would get a decline from $2.32 billion to $1.84 billion. And lastly, EBITDA for the company fell from $2.99 billion to $2.15 billion.

International Paper

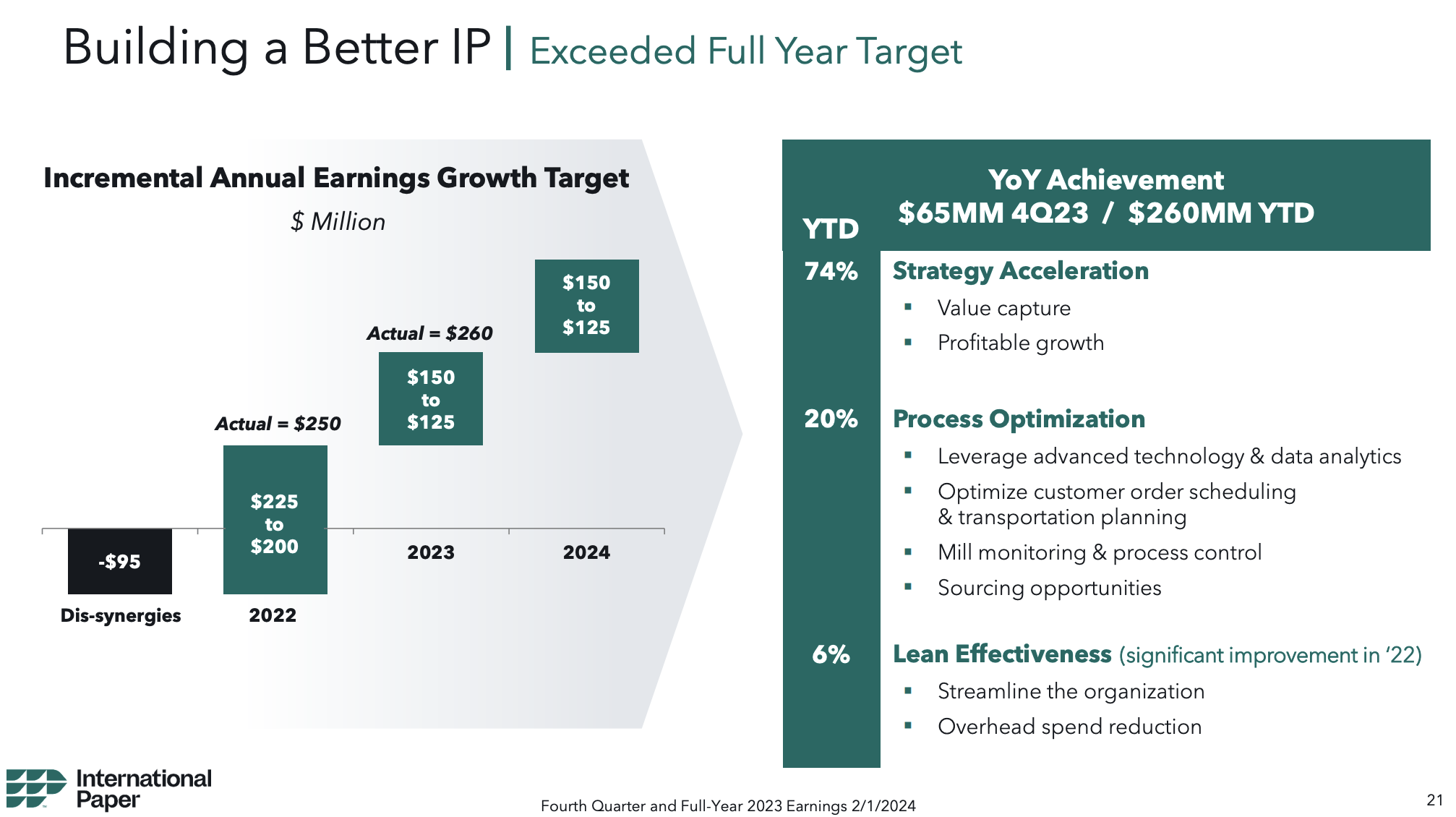

As I mentioned earlier, International Paper has been working hard to fix some of its issues. Some of these fixes have been focused on the cost side of the equation, while others have been focused on the revenue side. On the cost side, for instance, the business is attempting to boost annual earnings by investing more in technology and simplifying the complexity of the organization. Management is looking for various attractive sourcing opportunities and is attempting to optimize customer order scheduling and transportation planning. As part of its cost reduction plan, the firm has even focused on shutting down certain assets.

International Paper

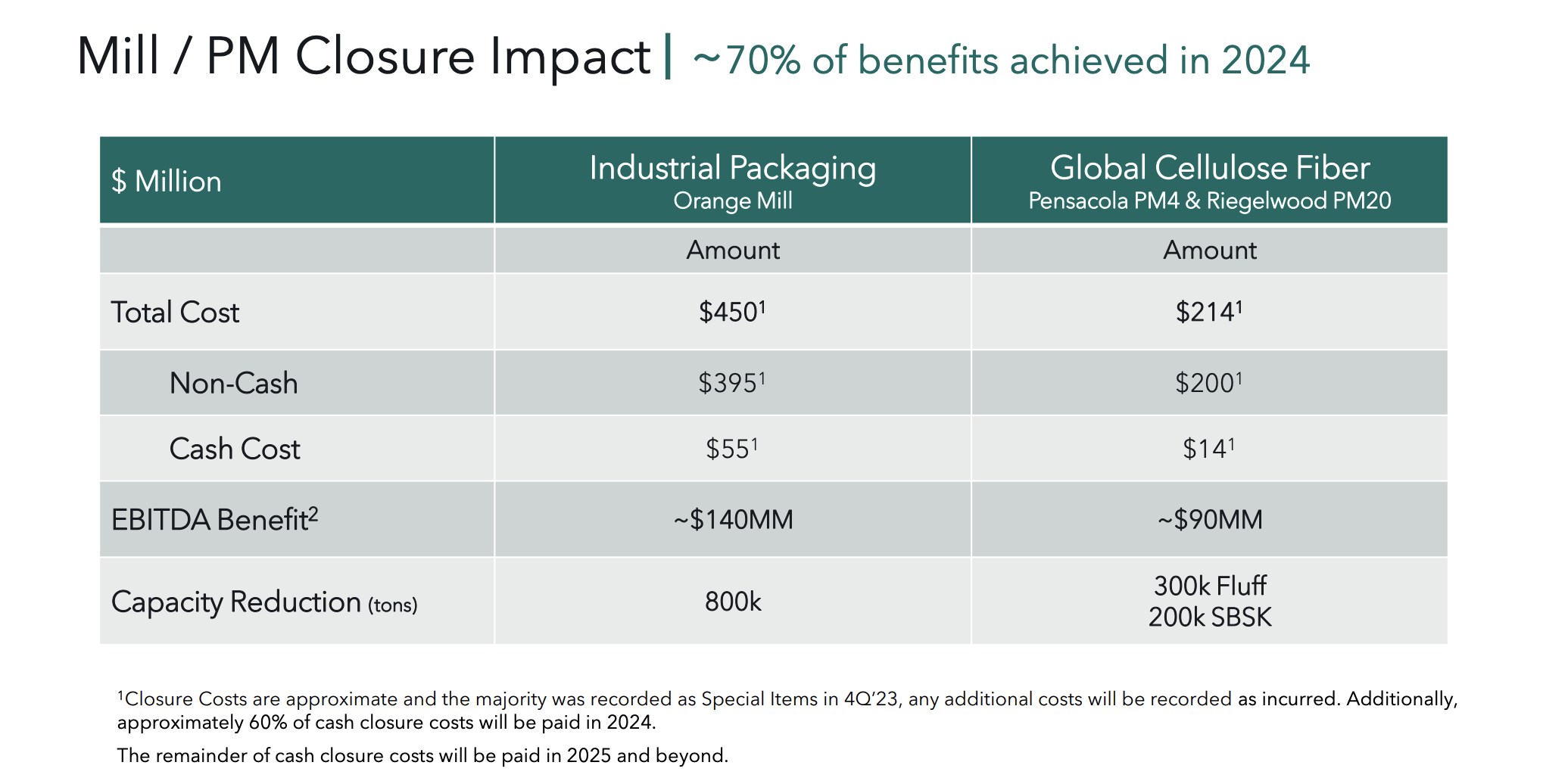

These are not without cost, however. Its Orange Mill Industrial Packaging facility will cause around $450 million worth of closure costs. The firm also is incurring costs of about $214 million associated with two facilities under the Global Cellulose Fiber segment. Most of the costs involved with these closures was booked in the final quarter of 2023, with the rest being recorded as they are incurred. About 60% of the cash closure costs, which will only represent a small portion of overall costs, will be paid out this year, with the rest paid out in 2025 and beyond. It's estimated that, while this will reduce production capacity, it will have an annualized EBITDA benefit to the business of $230 million.

International Paper

On the revenue side, the enterprise is looking to capture additional value by focusing on specific product lines. One example of this involves the Global Cellulose Fibers segment. In 2023, 55% of the revenue generated by that segment came from absorbance and specialty products. Management is hoping to increase this to 70% this year and, eventually, is hoping to grow it to about 80%. The specialty side of the business is also what management hopes to grow when it comes to the Industrial Packaging segment. This makes sense when you consider that, typically speaking, specialty products of any sort tend to have higher sales prices and more robust margins. More traditional offerings, meanwhile, are commoditized products that carry lower margins.

Author - SEC EDGAR Data

Irrespective of whether management deviates from this strategy or not, and irrespective of whether they are able to make the desired improvements planned, I would argue that shares are still fundamentally attractive. As you can see in the chart above, the stock looks to be trading on the cheap even on a forward basis. And in the table below, I compared it to five similar firms. When it came to the price to operating cash flow approach, only one of the five firms I compared it to were cheaper than it. And when it comes to the EV to EBITDA approach, it ended up being the cheapest of the group.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| International Paper | 7.2 | 8.3 |

| Amcor (AMCR) | 10.2 | 11.6 |

| Packaging Corporation of America (PKG) | 12.5 | 11.3 |

| Avery Dennison (AVY) | 21.1 | 18.3 |

| WestRock Company (WRK) | 6.9 | 63.9 |

| Sealed Air Corp (SEE) | 10.1 | 10.1 |

These are interesting times for International Paper. I rarely see shares of a business spike so much after a leadership change. But it's clear that the market is pleased with this maneuver. What this will mean in the long run is anybody's guess. But given the track record that Silvernail brings to the table, I suspect that the enterprise will be in good hands. Even if nothing changes, shares do look attractively priced at this point in time. And because of that, I believe that the ‘buy’ rating I assigned the stock previously should still hold.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.