undefined undefined

undefined undefined

Sea Limited (NYSE:SE) is reaching an inflection point in its business in 2024.

The company exceeded market expectations in the Q4'23 earnings report, as management is increasingly sounding more optimistic about future growth and profitability prospects.

Not only did Sea Limited achieve an incredible milestone by having its first ever profitable year since its IPO, the management team also guided for the company to continue to be profitable in the next year in 2024.

Sea Limited ended 2023 with $8.5 billion in cash on its balance sheet, which increased about $566 million sequentially, highlight a strong liquidity position despite investing more aggressively in its business to achieve market leadership.

I have published several articles on Sea Limited in Seeking Alpha, which can be found here. In the earlier article, I suggested that the sell-off in Sea Limited stock that was driven by the company's communications that it was going to invest in its business was creating an attractive opportunity for long-term investors. In this article, I will share why this is even more so the case after the recent events and the fourth quarter results.

Shopee has had an interesting year, but it really ended off on a positive note.

The company began to invest in Shopee in July of 2023, as it saw competitive pressures intensify.

I think it is positive that investors can see the positive impact of these investments made earlier in 2023, as management shared that Shopee gained meaningful market share from the start to the end of 2023.

The intention in 2024 will be to maintain this higher market share that it managed to grow in 2023.

As such, management guided for the full year GMV growth for Shopee to be in the high-teens range.

Perhaps more positively, the management team also guided for Shopee to return back to positive adjusted EBITDA in the second half of 2024.

This is positive because there has been uncertainty surrounding how long Shopee will be in this investment phase as it fends off competitive pressures.

The investments made since July 2023 have helped Shopee to gain market share through improving monetization, increasing cost efficiencies and grow scale for the company.

For Q4'23, after investing into the business, the company saw improvement not just on the top line, but also the bottom line.

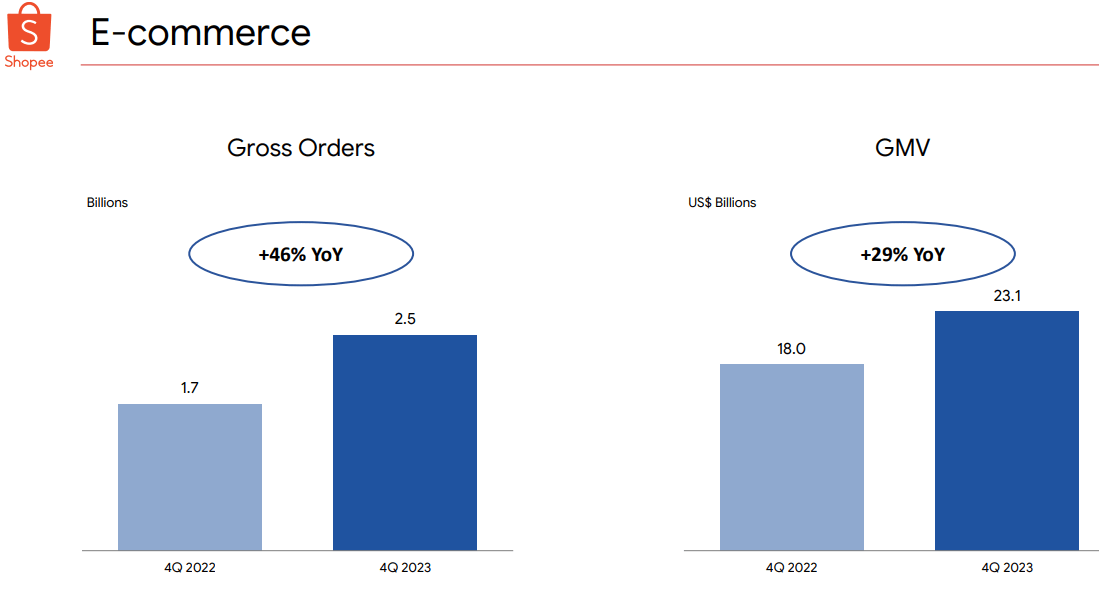

GMV for Shopee grew 29% from the prior year while the gross orders grew 46% from the prior year, which led to solid gains in market share across its markets.

E-commerce gross orders and GMV for 4Q23 (Shopee)

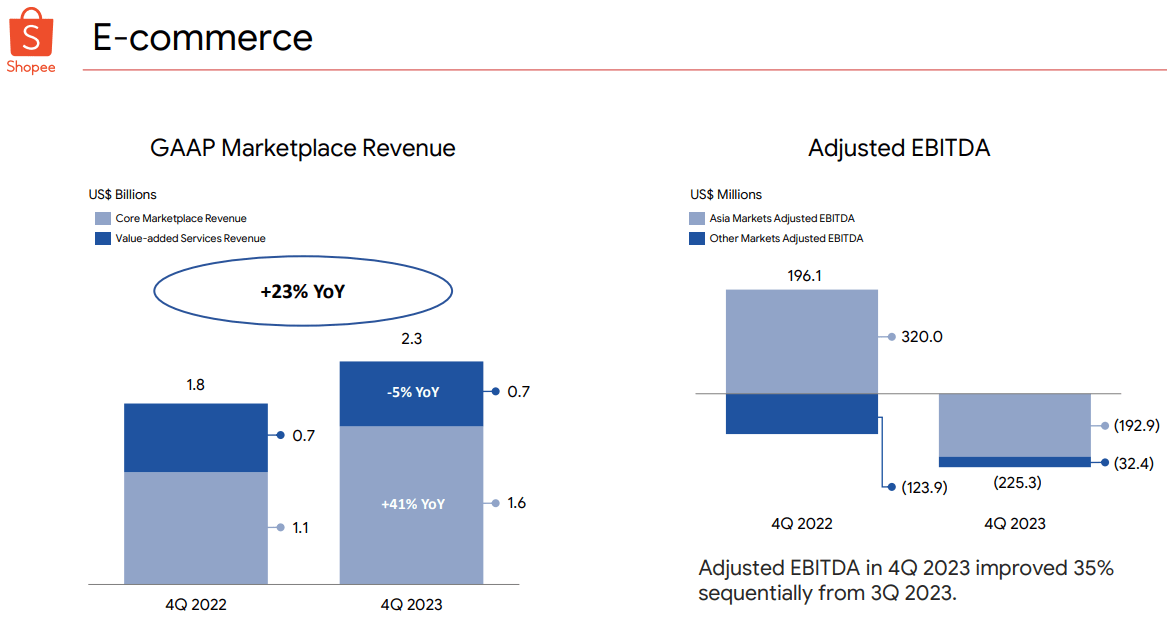

Revenues grew 23% from the prior year, driven by strong core marketplace revenue growth of 41%.

The profitability financial metrics also look good from a sequential basis, with adjusted EBITDA loss improving 35% from the prior quarter and adjusted EBITDA loss per order improving 43% from the prior quarter.

Financial metrics of Shopee (Shopee)

I think for many investors, there were many uncertainties going into this round of investments in Shopee since July 2023 although I had confidence in the management team's experience and execution.

This Q4'23 report does highlight to investors once again that the management team is executing really well despite the intense competition it is experiencing.

With the market share gains that Shopee has gained in 2023, it is clear that the strategy it is employing is working well in its core markets. The goal to maintain market share in 2024 and return Shopee to positive adjusted EBITDA in the second half of 2024 highlights that the Shopee's market leadership is where it needs to be and continues to improve.

Shopee continued to invest in its business and grow its moat in Q4'23.

Firstly, the company focused on growing its e-commerce logistics network in the quarter, making Shopee's e-commerce logistics network one of the most extensive and also most efficient in the key markets in which it operates in.

I think that this brings huge competitive advantages to Shopee, because it helps to improve on delivery speed and consistency, which in turn leads to a better experience for buyers.

In the last quarter, Shopee not only opened five new sorting centers, but also 385 new first and last mile hubs across its markets in Asia, significantly increasing its logistics network and coverage.

This leads to tangible, observable improvements as Shopee's platform logistics cost per order in Asia fell 12% from the prior year in Q4'23, which was driven by Shopee's own logistics network cost per order falling 20% from the prior year.

As such, we can see that developing and growing this logistics network will lead to lower costs and higher efficiency in the long-term.

This increasing of the delivery coverage also helps to improve delivery speed for Shopee, where more than half of the orders from buyers in Java, Indonesia were delivered in two days.

For 2024, improvement of its logistics capabilities will remain a key focus for Shopee as it looks to improve the buyer experience and bring a better service quality to the end users.

Another area in which management has been focused on in 2023 and will continue to invest in 2024 is in growing the content ecosystem. Specifically, Shopee has focused on quickly growing and ramping up its live streaming e-commerce business.

As of end December 2023, live streaming e-commerce makes up 15% of its total physical order volume in the Southeast Asia markets.

After ramping it for some time since July last year, the live streaming e-commerce business has gained enough scale and leadership for the unit economics of the business to improve meaningfully sequentially, according to management.

I think the direction that management is taking to invest and strengthen its content ecosystem is the right one. The initial concern was whether this will require significant investment that might dampen near-term profitability.

That said, the very fast ramp in the live streaming e-commerce business has meant that the unit economics has also improved meaningfully, highlighting strong execution from the management team.

In 2024, management will likely continue to invest in this area. I think the focus for 2024 will be to improve the engagement between creators, sellers and partners across the content ecosystem. Another area of focus will be to enable a more seamless integration of the live streaming feature with the shopping experience.

The Digital Financial Services segment has had a strong 2023 as this was the first full year in which SeaMoney was profitable, generating $550 million adjusted EBITDA in the quarter.

The strong 2023 was largely due to the consumer and SME credit business.

The consumer and SME loans principal outstanding grew 27% from the prior year to $3.1 billion, highlighting robust demand for its credit business.

I think that there continues to be meaningful upside in the SeaMoney business. In 2024, SeaMoney will continue to scale up its business by investing in user acquisition for its credit business while remaining prudent on risk management.

On top of the credit business, another focus for SeaMoney is to grow its digital banking and insurance services that will bring the next leg of growth for SeaMoney in 2024.

Within the digital entertainment segment, things are starting to look good for the company.

Free Fire's user acquisition and retention trends have been improving in 2023 and looks encouraging.

For 2023, Sensor Tower reported that Free Fire was the most downloaded mobile game in the world.

I think that it is highly encouraging that this positive trend is continuing into 2024.

In fact, Free Fire has more than 100 million peak daily active users in February, which highlights how the efforts to improve game experiences and bring more localized content is increasing engagement with users.

With these positive trends and metrics, the cherry on top of the cake is the positive guidance that management gave for Free Fire in 2024.

Management is guiding for Free Fire to grow user base and bookings by double-digits from the prior year in 2024.

I do think that this is a bold call by the management team given the inherent volatility and uncertainty in the Garena numbers, but it does suggest that management is rather confident that we are seeing a stabilizing trend for Free Fire.

With the guidance of high teens GMV growth for Shopee, positive adjusted EBITDA in the second half of 2024, and the double digits growth of the user base and bookings for Free Fire, this makes the forecasting of 2024 numbers much easier.

There is a caveat of course, and that is whether management can actually meet this guidance provided. Over the earnings call, it does seem like management is quite confident in being able to deliver the full year guidance for 2024.

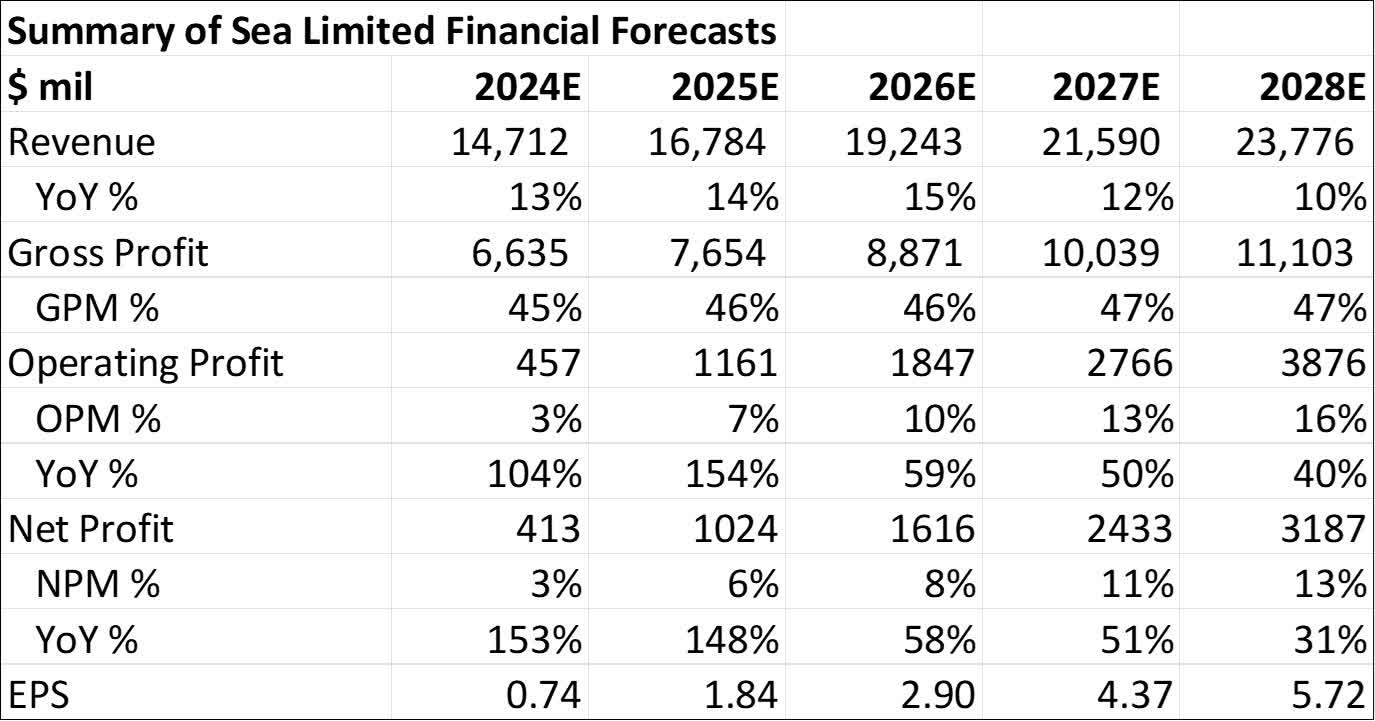

Summary of 5-year financial forecasts (Author generated)

The intrinsic value goes up to $60 given the increased certainty of profitability outlook. Again, the assumptions include a conservative 20x 2024 P/E and 14% cost of equity.

The 1-year and 3-year price targets also goes up marginally to $65 and $101.

This was certainly positive quarter after a difficult few investment quarters for Sea Limited's Shopee.

The commentary surrounding around market share gains in 2023 and the goal to maintain this market share in 2024 shows that the strategies employed in 2023 worked, and that we will likely see less aggressive investments in 2024 than in 2023.

With the less aggressive investments to be made in Shopee, this then brings about the possibility of Shopee returning to positive adjusted EBITDA in the second half of 2024.

The digital entertainment segment is also starting to see the light at the end of the tunnel, with management guiding double digits growth of the user base and bookings for Free Fire.

Lastly, for the digital financial services segment, this segment is still in the early stages of growth with potential for upside in the years to come, as management is focused on user acquisition in the near-term.