phuttaphat tipsana/iStock via Getty Images

phuttaphat tipsana/iStock via Getty Images

Schrodinger (NASDAQ:SDGR) reported strong results in the fourth quarter of 2023 but guidance for 2024 was weak, causing the share price to drop. The demand environment continues to impact the software business, with growth amongst smaller customers particularly soft. Schrodinger's software business is growing at a reasonably healthy pace considering the challenging macro environment, and the drug discovery business continues to demonstrate its value.

Investors appear to be valuing Schrodinger based on software revenue and drug discovery losses. These are separate businesses, with separate value drivers, and should be treated as such. Schrodinger's software business largely justifies the company's current market capitalization, with the drug discovery business providing a large amount of upside.

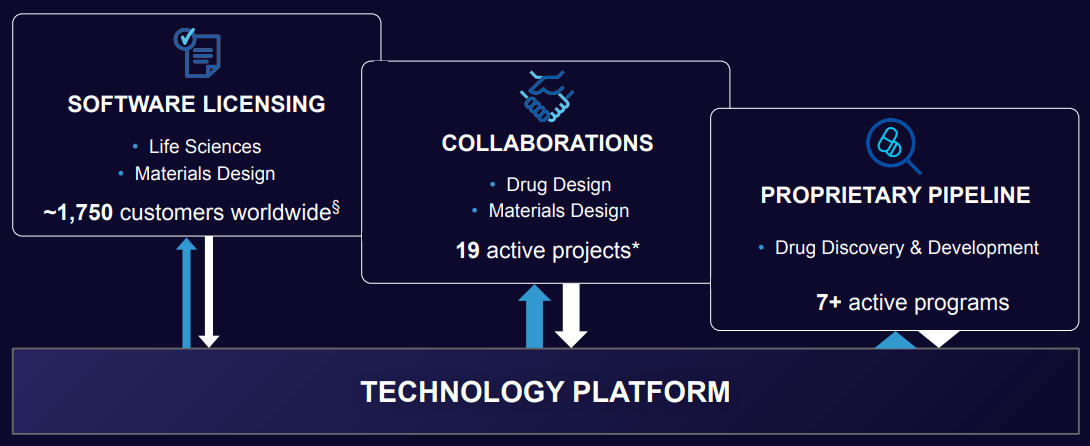

Figure 1: Schrodinger Platform Monetization Strategy (source: Schrodinger)

While Schrodinger's software business had a reasonably solid year in 2023, the demand environment remains challenging and guidance for 2024 is weak. Schrodinger had a number of multi-year on-prem software deals towards the end of 2023 that pulled revenue forward, setting the company up for difficult comps going forward. For example, Schrodinger recently announced an expanded 3-year software agreement with Eli Lilly to accelerate all stages of drug discovery.

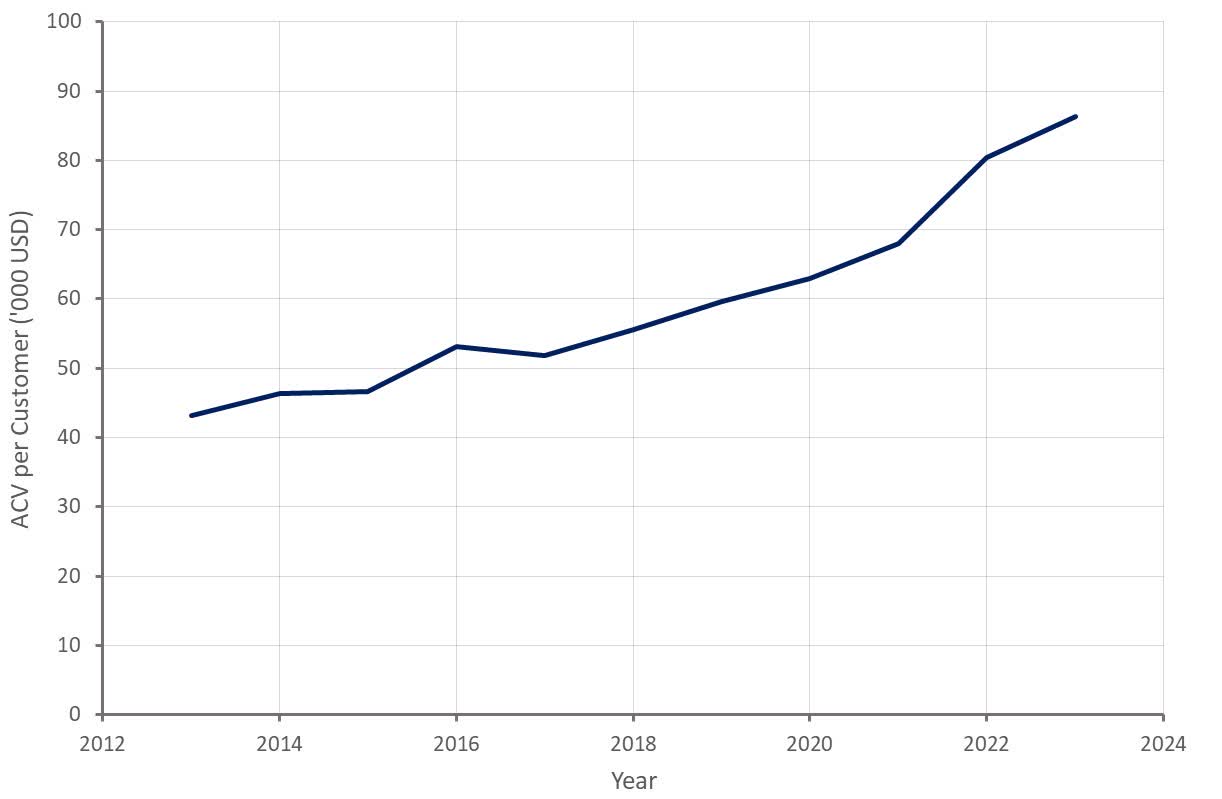

Growth amongst larger customers still appears to be solid but has softened amongst smaller customers. The average contract value for customers with ACV greater than 5 million USD increased to 6.7 million USD in 2023.

Figure 2: Schrodinger ACV per Customer (source: Created by author using data from Schrodinger)

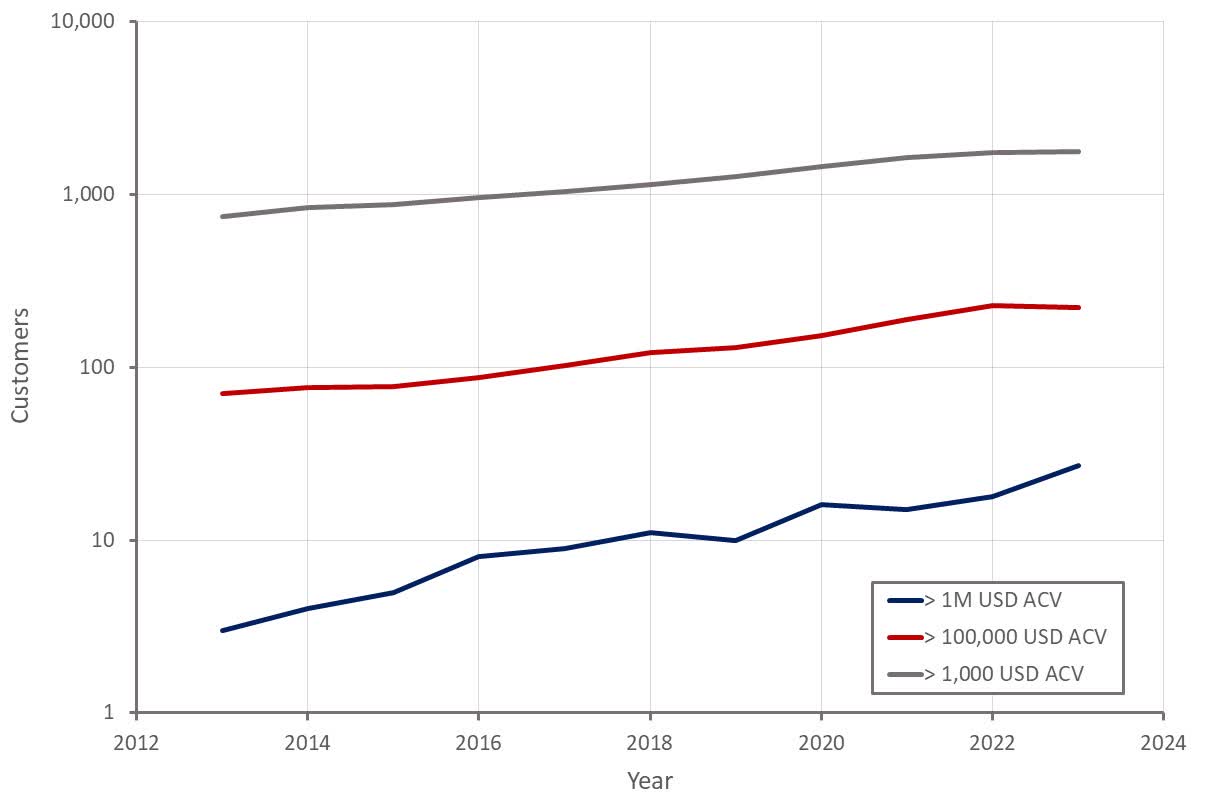

Schrodinger’s gross retention rate in the 100,000+ USD ACV cohort declined from around 96% to 92% over the past year. The decrease was attributed to consolidation and discontinuation of R&D efforts by some biotech customers.

Figure 3: Schrodinger Software Customers (source: Created by author using data from Schrodinger)

Longer term, Schrodinger expects to see increased adoption of its software within existing customers. Schrodinger has stated that the interest in computationally driven drug discovery has never been greater, but that a shortage of knowledge workers could limit near-term adoption.

The company is also trying to drive adoption amongst emerging biotech companies. In support of this, Schrodinger continues to advance its software capabilities relevant to biologic drug discovery.

Schrodinger is also enabling the refinement of machine learning generated protein structures, which is expanding the number of targets for structure-based discovery.

Schrodinger is increasing its focus on internal programs as a result of the difficult macro environment and its growing conviction in its drug discovery platform. As a result, drug discovery revenue in 2024 is expected to be similar to or lower than 2022.

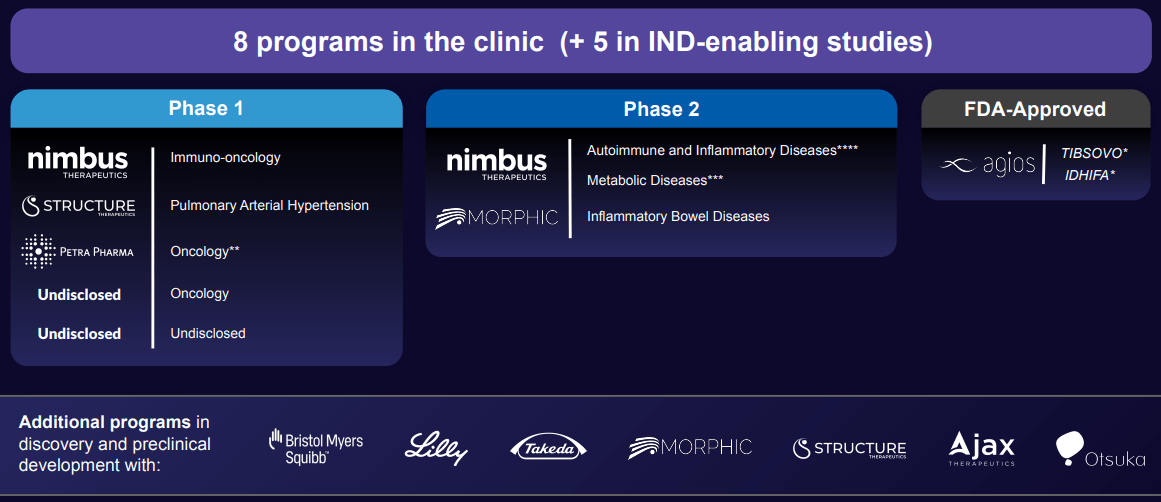

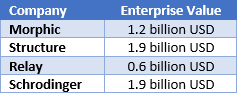

While Schrodinger is pulling back on collaboration programs, these have already demonstrated the value of Schrodinger’s approach to structure-based design. Schrodinger co-founded and has equity stakes in Nimbus Therapeutics, Morphic Therapeutic and Structure Therapeutics. Morphic and Structure are both multi-billion-dollar companies, and Nimbus sold a molecule to Takeda in 2023 which resulted in a 147 million USD distribution to Schrodinger.

Figure 4: Schrodinger Partner Programs (source: Schrodinger)

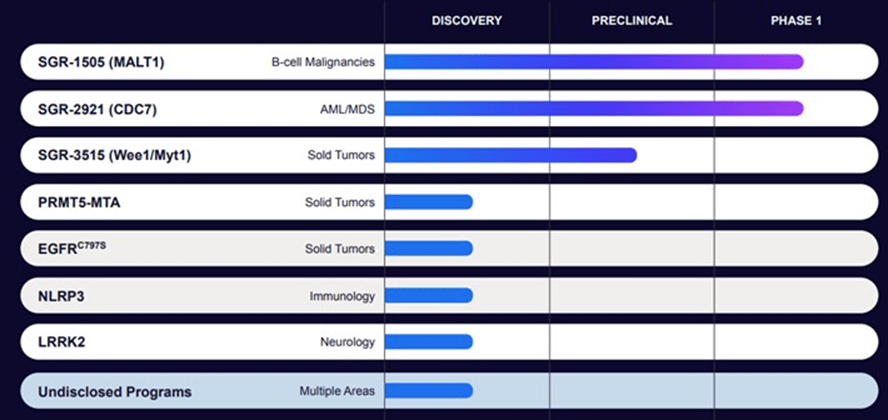

Schrodinger expects data from its first two studies in late 2024 or 2025 and is on track to progress a third program into the clinic this year. Schrodinger also expects to submit an IND from its discovery portfolio in 2025.

Figure 5: Schrodinger's Proprietary Pipeline (source: Schrodinger)

SGR-1505

Phase 1 data confirms target engagement and indicates that SGR-1505 is well tolerated. The data supports ongoing evaluation of SGR-1505 in patients with relapsed or refractory B-cell malignancies. Initial data from the phase 1 study is expected in late 2024 or 2025.

SGR-2921

Schrodinger has a Phase 1 study of SGR-2921 in patients with acute myeloid leukemia or myelodysplastic syndrome. Initial data from the phase 1 study is expected in late 2024 or 2025.

SGR-3515

Schrodinger expects to submit an IND for SGR-3515 in the first half of 2024 and initiate a phase 1 study during the year.

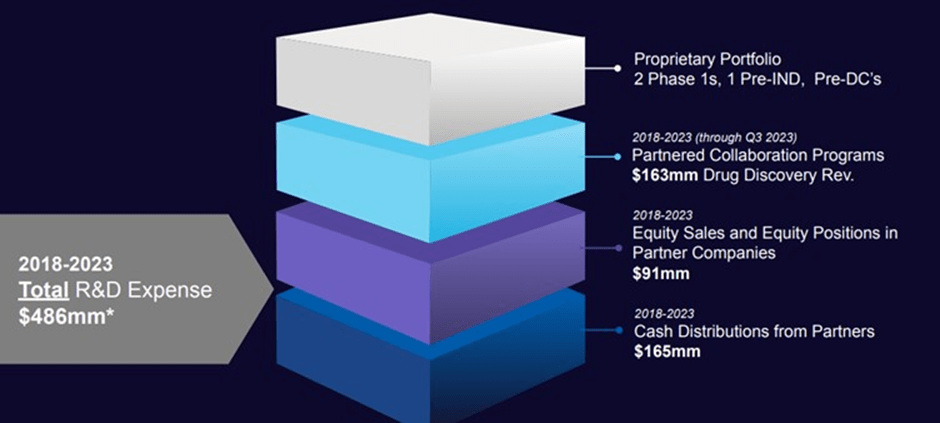

Schrodinger's investment in drug discovery has been rising since 2018 and could be contributing to the company's undervaluation. Companies with large losses have been punished over the past few years, and Schrodinger appears to have fallen into this basket.

Losses are largely related to drug discovery R&D though, a business that shouldn't be valued based on current cash flows. While programs are beginning to advance through clinical trials, it is still early days for Schrodinger’s drug discovery efforts. It should also be noted that the value created by collaborations has largely offset Schrodinger's R&D investments.

Schrodinger's software business would likely be profitable on a standalone basis, particularly in a healthier demand environment, and should be valued as such.

Figure 6: Schrodinger R&D Investment and Drug Discovery Returns (source: Schrodinger)

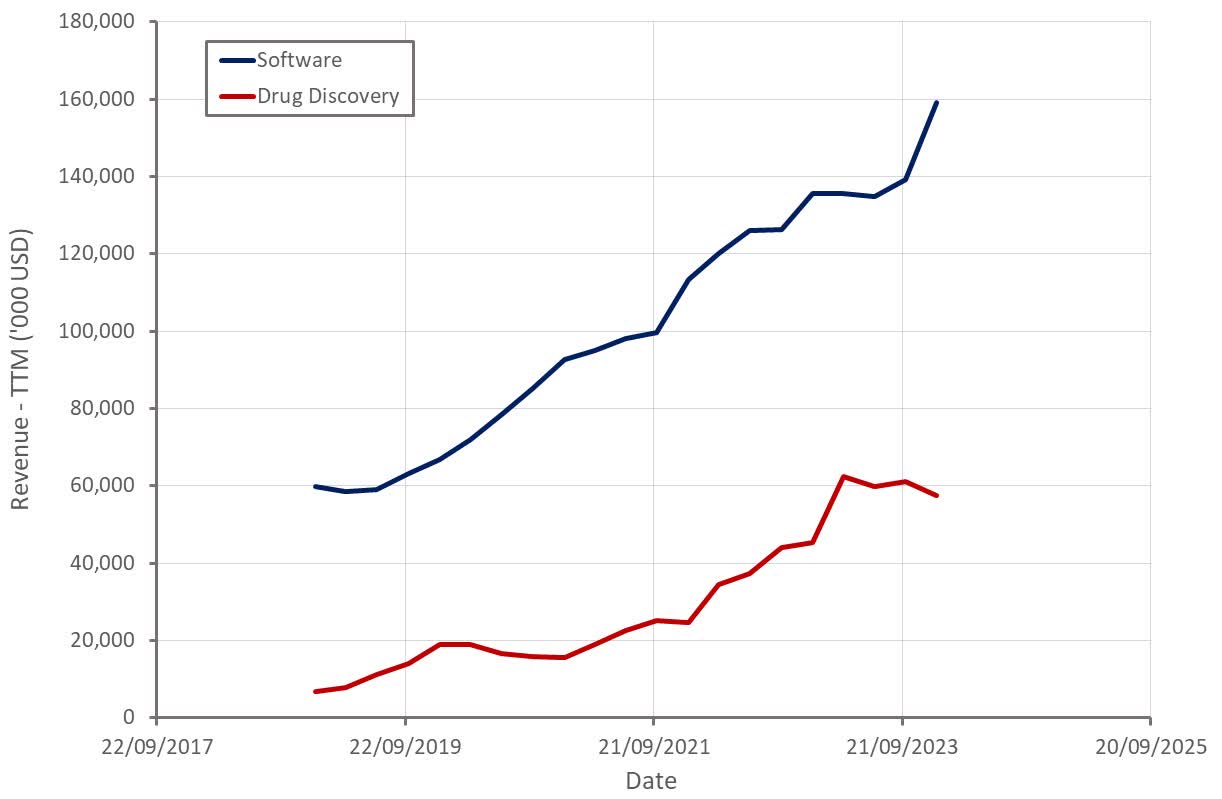

Schrodinger’s revenue increased 30.4% YoY in the fourth quarter, to 74.1 million USD. Software revenue was up 43.6% YoY, to 68.7 million USD. Multi-year on-prem agreements contributed significantly to revenue in the quarter, which sets Schrodinger up for difficult comps going forward.

Software revenue growth is expected to be in the 6-13% range in 2024. Schrodinger does see opportunities for growth from renewals in 2024, but this is likely to be less than in 2023. Drug discovery revenue is expected to be 30-35 million USD, down over 40% YoY. Schrodinger is not including any potential milestones or business development transactions in this guidance though, due to their unpredictable nature. As a result, there could be substantial upside to the drug discovery guidance.

Figure 7: Schrodinger Revenue (source: Created by author using data from Schrodinger)

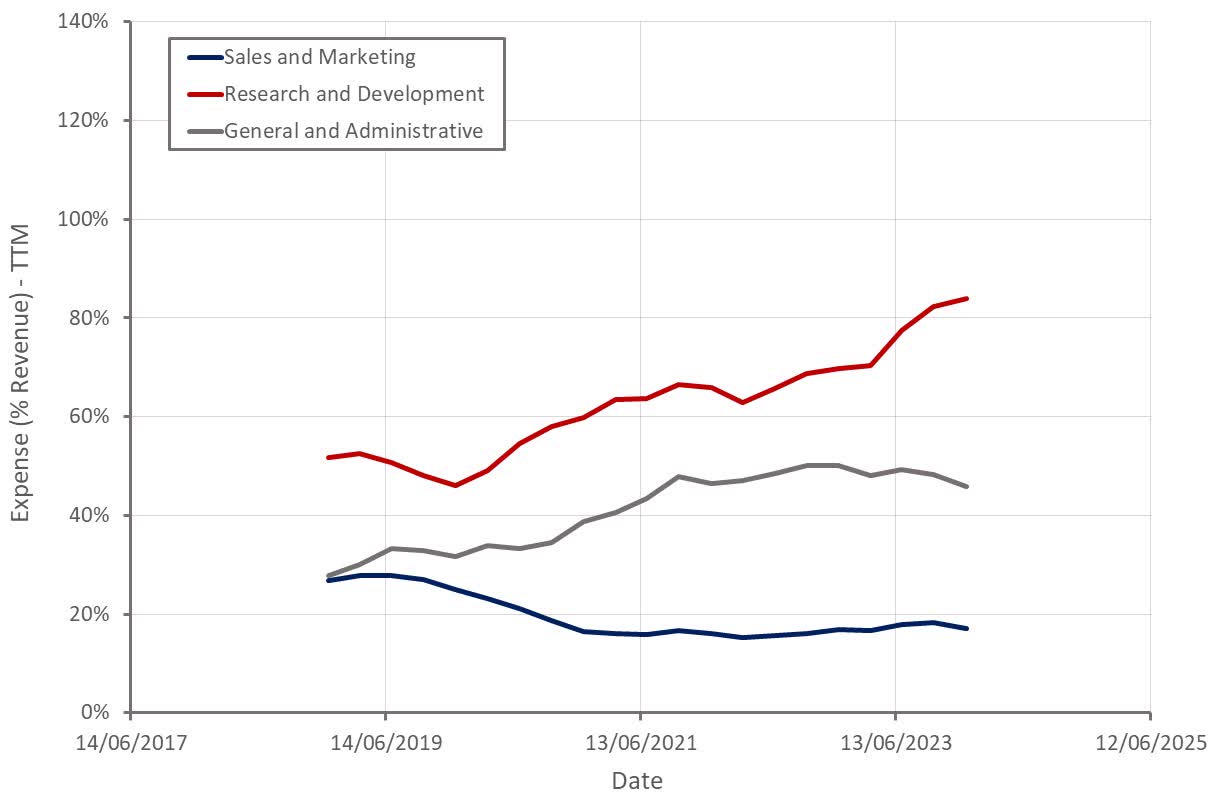

Schrodinger's R&D expenses were 52 million USD in the fourth quarter of 2023, up nearly 50% YoY. The increase was driven by headcount, CRO expenses and technology expenses. Schrodinger's prioritization of internal programs has also seen costs shift from COGS to R&D.

Operating expense growth is expected to be in the 8-12% range in 2024 and cash used for operating expenses is also expected to increase. While this may be received poorly by investors in the near-term, it is an inevitable outcome of Schrodinger's shift in focus.

Figure 8: Schrodinger Operating Expenses (source: Created by author using data from Schrodinger)

Valuing Schrodinger is difficult as it is monetizing its technology platform through a combination software licensing, collaborations and a proprietary pipeline of drugs.

Schrodinger is eligible for billions of dollars in milestones from its collaboration programs and also has 12 programs which are eligible for a royalty on sales. While these involve high risk, hundreds of millions of dollars of value will likely accrue to Schrodinger, although this will probably be used to finance Schrodinger's own drug discovery efforts.

Schrodinger's drug discovery efforts are still fairly nascent, and hence the market appears to be attributing little value to this part of the business. Schrodinger will likely need to advance programs towards approval before the market takes this business seriously.

Table 1: Structure-Based Drug Design Company Valuations (source: Created by author using data from Seeking Alpha)

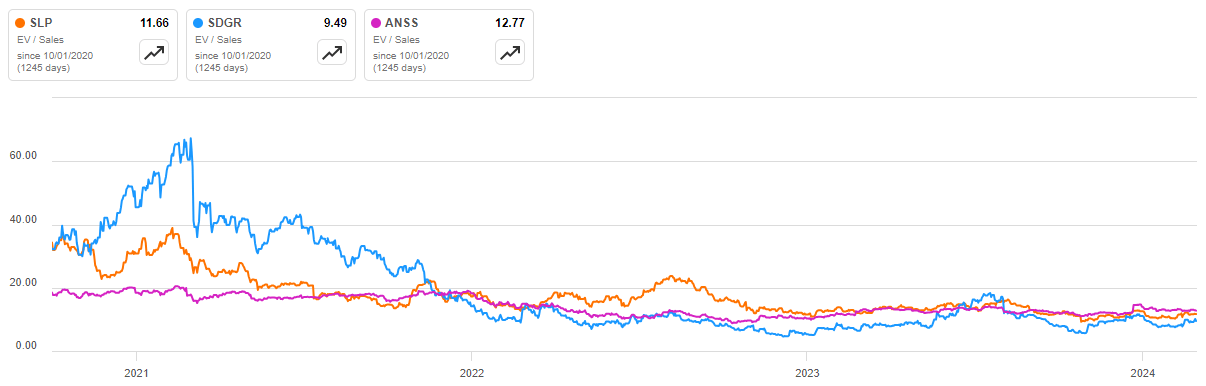

Schrodinger's software business operates in a niche with growing demand and relatively limited competition. The market appears to be undervaluing this part of the business because its potential is being hidden by losses associated with drug discovery. If Schrodinger's software was a profitable standalone business, it could potentially be valued higher than Schrodinger's entire business.

Figure 9: Schrodinger EV/S Multiple (source: Seeking Alpha)

The near-term is likely to remain volatile for Schrodinger's stock, due to the uncertainty associated with milestones, collaborations and clinical trials. In addition, the demand environment is likely to remain soft, which will continue to weigh on Schrodinger's software growth. Over a longer time frame the value of the company's various activities is likely to be recognized though.