HalimLotos

HalimLotos

Shoe Carnival (NASDAQ:SCVL) is an American footwear retailer with 430 stores.

The company showed consistent growth and margins for over 30 years since going public in 1993. After the pandemic, growth accelerated, coupled with operational leverage and lower promotions, which led to double operating margins.

Margins are currently deleveraging as store productivity decreases. An analysis of several margin scenarios over today's business base (including the announced acquisition of Rogan's) shows that the stock price is high. Shoe Carnival is not an opportunity.

Suburban emporium: Shoe Carnival had 400 stores up to FY23, concentrated in the US Midwest and southeast. Texas, Florida, Illinois, Indiana, and Georgia are among its most prominent states.

The company has stores in large cities but with a more suburban focus, maybe except Chicago. For example, of 47 stores in Texas, only 10 are in the main cities (Dallas-Fort Worth, Austin, San Antonio, or Houston). Of the 26 stores in Indiana (its home state), only five are in Indianapolis.

With the recent acquisition of Rogan's Shoes (announced this week), Shoe Carnival will add 30 stores in Wisconsin, Minnesota, and Illinois.

Assortment and value for the family: The company's value proposition is being the single place to buy shoes for all the family, for different occasions, from renowned brands, at value-conscious price points. The stores are well assorted, with around 30 thousand units and large, covering 11 thousand square feet on average.

The Shoe Carnival customers are low- to middle-class, with approximately 25% making less than $30 thousand per year, another 25% making over $75 thousand, and the rest in the middle (according to the 3Q23 earnings call).

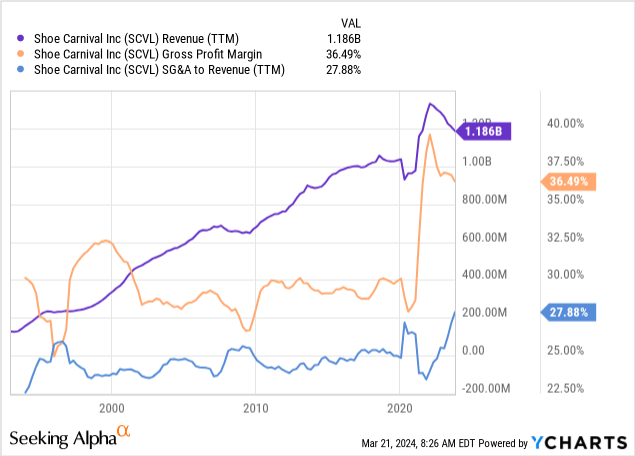

Consistent profitable growth: Shoe Carnival prides itself in having been profitable for all years but one since going public in 1993. The company grew at a pretty steady pace for the past 30 years, maintaining average gross margins in the 27.5/30% range and operating margins in the 4/5% range. This has been remarkably stable until the pandemic (more on this later).

Strong culture: The company has a strong employee culture. Most of the company's executives have been with the company for over 15 years, with the average district or store manager posting the same or higher tenures. 90% of district or store managers are promoted from within. The company's Chairman (age 88) has been with the company since 1988 and owns about 35% of the stock.

Iconic store concept: The carnival concept is portrayed in the stores via spinning wheels, bright screens with advertising, and flash promotions. I find the store interiors pretty dull and unappealing, looking like giant warehouses with little space for showing the shoes, but most footwear stores have the same concept (like recently covered Caleres). The company emphasizes B&M stores, with only 10% of sales generated online in FY22.

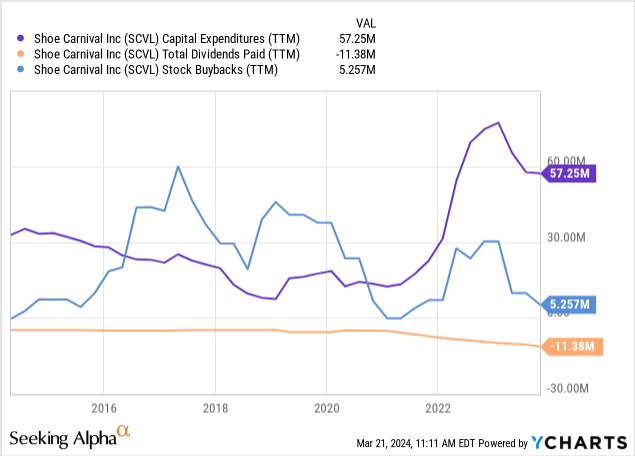

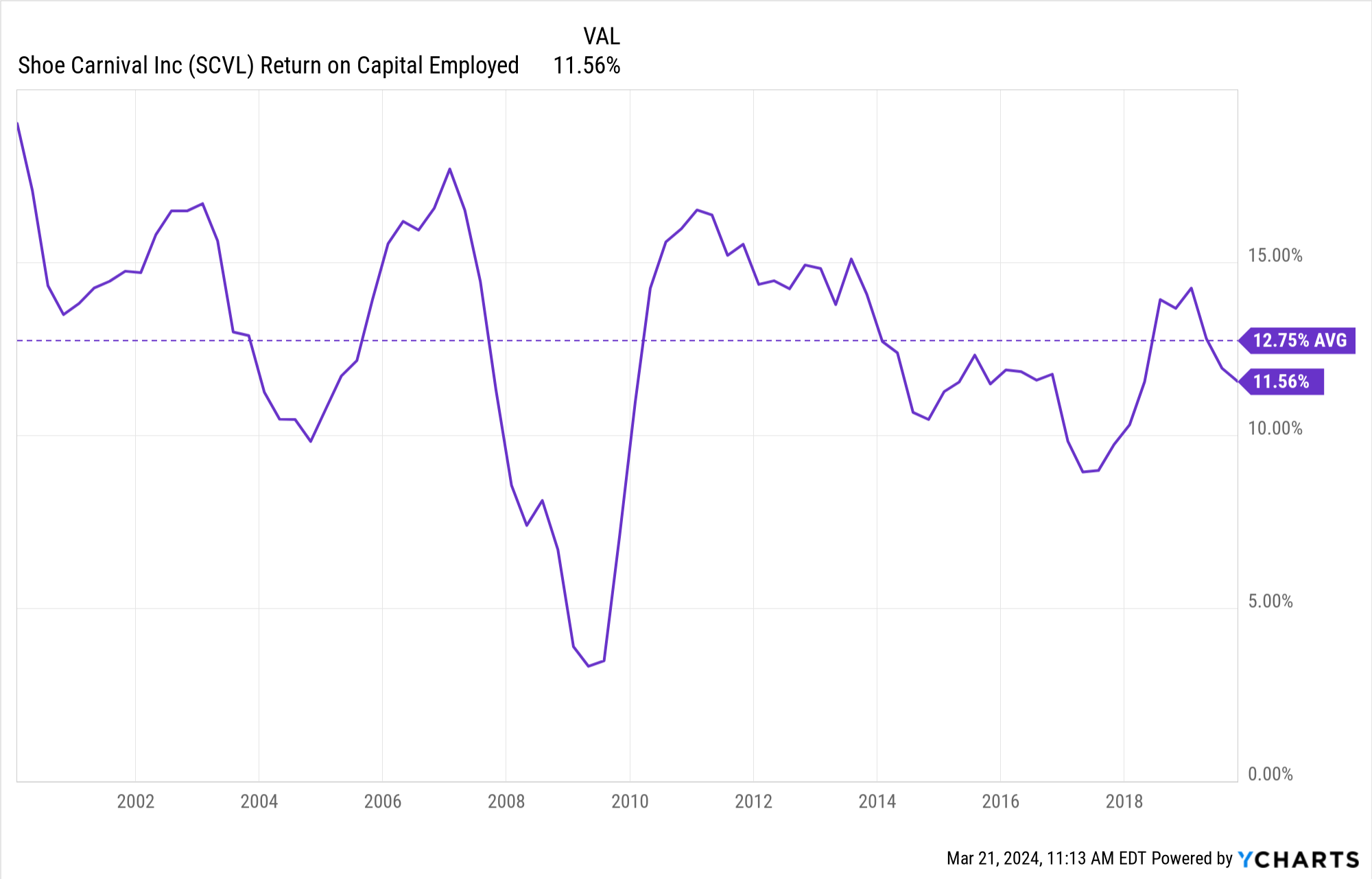

Conservative capital allocation: Pre-pandemic, the company was not investing too much in the business, concentrating more on returning capital to shareholders via buybacks and dividends. Despite this, the company was growing while maintaining a consistent (albeit slightly down-trending) return on capital employed.

Cost-competition category: Shoe Carnival's negatives come mainly from its positioning. Most of what Shoe Carnival sells can be found in other stores or online. This puts a lot of pressure on margins as the customers can try the shoes and then search for a better price online. Unless the differential is small, they will not purchase in the store. Of course, having stores in less populated areas with lower B&M competition helps. Still, it is difficult to gain premium pricing in this market, with costs being more important.

After close to 30 years of stable margin growth, something changed for Shoe Carnival in the post-pandemic period.

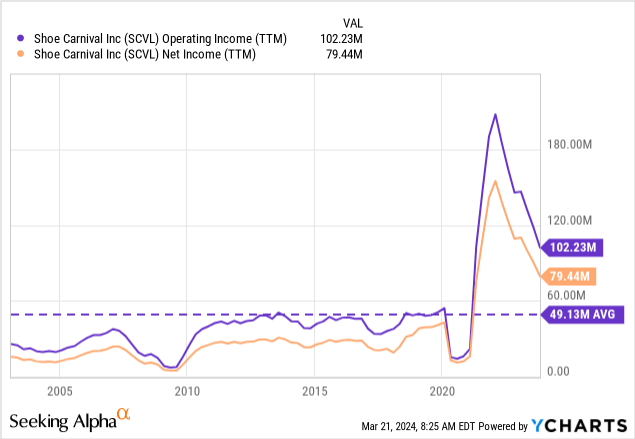

The company's sales took a completely different and ballistic upward trend, and gross margins expanded close to 1000 bps. This led to a 400% increase in operating profits and net income. Even today, with a more moderated effect, the company is generating twice the profits it generated pre-pandemic.

The company has commented that most of that improvement has come from running fewer promotions. I believe this is, in part, the case, like most retailers, and also explains why margins are more pressured now.

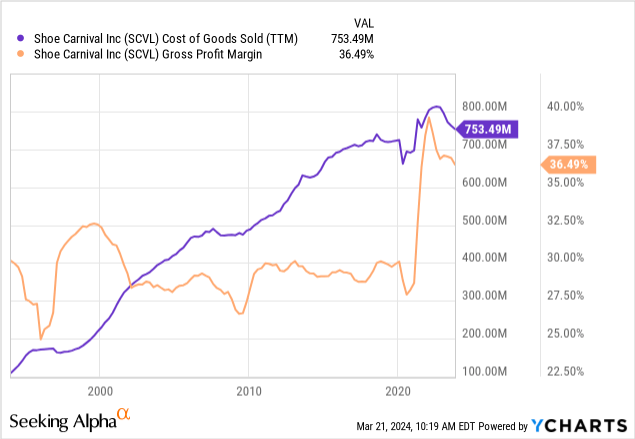

Another critical aspect, in my opinion, but not commented directly by the company, is how operating leverage plays in the company's gross margins (which include occupancy costs of approximately 10% of CoGS). We can see that when the CoGS figure deviates from the trend below (like in the GFC, the pandemic, or the post-pandemic period), margins tend to move more violently than when CoGS is trending.

I cannot find intrinsic reasons for Shoe Carnival's higher margins. I believe that external factors generated the expansion, so the margins could potentially revert to their historical levels.

However, we do not need to pinpoint future margins to evaluate Shoe Carnival's stock as an opportunity today. Instead, comparing the company's multiples under different scenarios will show that they are generally high, except for the most optimistic scenarios.

We start with Shoe Carnival's current CoGs, which approximate the company's current volume sales independently of the margin applied to them.

The historical scenario would have gross margins of about 30% (a little optimistic still, given this was the upper range historically). A bullish scenario would have gross margins at the current 37%, and a more mixed scenario would have gross margins at about 33%.

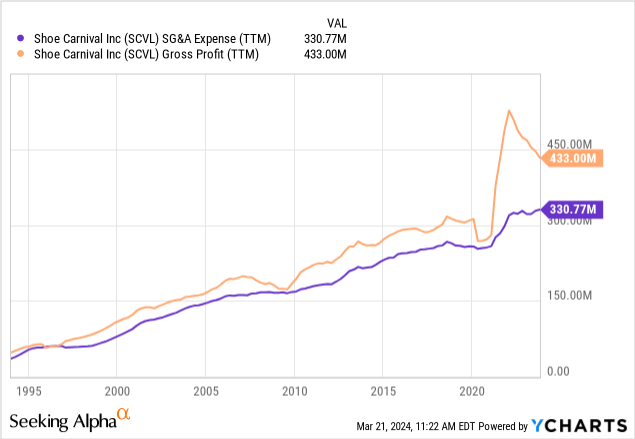

From those scenarios, we should remove SG&A, a more fixed expense. As the chart below shows, SG&A has been growing despite the recent deceleration in gross profitability. For the lower gross margin scenarios, SG&A expenses that fail to adapt would imply a lower operating margin than what was historically the norm.

Still, for the sake of simplicity, we can assume that even in the scenario of lower gross margins, SG&A expenses would adjust to maintain historical operating margins. Further, in optimistic scenarios, SG&A would not change so that operating margins would be higher. This represents an optimistic bias.

In that case, our historical scenario has gross and operating margins of 30% and 5%, with the optimistic scenario at 37% and 10% and the mixed at 33% and 7%, approximately.

Again, starting with CoGS of $750 million and applying a tax rate of 30% on the proceeds, the scenarios result in the NOPATs in the table below. These are compared to the company's 4Q23 EV of $800 million, considering no debt and $100 million in cash.

| Scenario | Historic (30/5%) | Mid (33/7%) | Optimistic (37/10%) |

| Revenue | $1,071M | $1,120M | $1,190M |

| NOPAT | $37M | $55M | $83M |

| EV/NOPAT | 21x | 14.5x | 9.6x |

Given the relatively undesirable characteristics of Shoe Carnival's industry and position, which are not fully offset by its positive intrinsical characteristics, a 10x multiple on the mid-scenario earnings would be fair but not an opportunity. In this case, the company's current EV would only be fair under the most positive scenario, which is clearly not in the current margin compression trend that has continued into 4Q23 earnings.

The company is overvalued in both the mid-scenario and the (in my opinion, most likely) historical scenario. Further, these margin-shrinking scenarios already embed the optimistic assumption that Shoe Carnival can promptly adjust its SG&A expenses to keep its operating margins high. This might not be the case.

Therefore, I believe Shoe Carnival's stock is not an opportunity at these prices. I would be more interested in the stock at half the current prices. In the future, I will follow the company's gross margins with attention, for signs of their durability at these historically-elevated levels.