DisobeyArt/iStock via Getty Images

DisobeyArt/iStock via Getty Images

The purpose of this article is to evaluate the Schwab International Equity ETF (NYSEARCA:SCHF) as an investment option at its current market price. This fund is managed by the Charles Schwab Corporation (SCHW), and its objective is "to track as closely as possible, before fees and expenses, the total return of the FTSE Developed ex US Index".

I initiated coverage on SCHF over two and a half years ago when I had begun taking steps to diversify my portfolio. This was due to my US-centric nature which, over time, has led me to be concentrated towards a handful of large-cap US names. As a result, I had (and continue to) look beyond US borders and into other developed markets. I saw SCHF as a fund to keep on my radar, although its performance over time has been modest:

Fund Performance (Seeking Alpha)

As we begin the month of March, I am taking some time to reflect on broader equity performance in 2024. The S&P 500 - and Big US Tech by extension - have continued on their "alpha" path by dominating market discussions and returns. This has been rewarding for those who hold the NASDAQ 100, S&P 500, or the individual names, which most US investors probably have exposure to.

While I always welcome gains, the sheer level of disconnect between the "Mag 7" and the rest of the market has me concerned. This is leading me to consider non-US holdings for diversification. After review, I see SCHF as a great way to meet this objective, and I will explain why in detail below.

To begin this review, I want to touch on why I am looking outside US borders at the moment. As my followers know, I am a US-oriented investor who is overweight large-cap stocks. So the bull run in 2023 that has continued into 2024 is one I should be (and I am) celebrating. But that does not mean I celebrate in a vacuum. The overwhelming dominance of US stocks - led by just a handful of names - has got me concerned. But I don't want to be a net seller during this momentum. Rather, I want to look for ways to keep my portfolio diversified as the leaders continue to grow in their sizing within my portfolio.

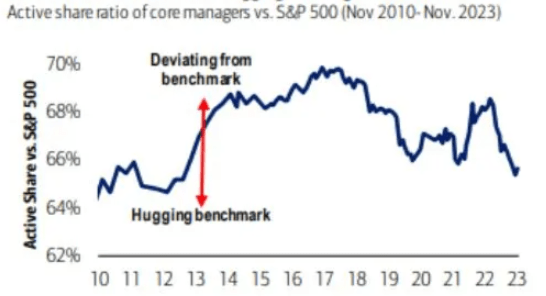

To understand why this is a concern, I am seeing a bit of a "fear of missing out" (known as "FOMO") playing out in the markets. There are a number of different ways to identify this, but one in particular that has caught my eye is the share of "active" money managers who are more closely mimicking the S&P 500. While I would expect those charging for their services would still have some S&P 500 allocation, they should not be simply copying the benchmark. They should be looking for individual stocks or themes to provide "alpha" beyond what the S&P 500 is going to give - that is the whole point of hiring them in the first place!

In fairness, most active money managers are certainly doing their share of stock picking. But the trend has started to turn towards heavier reliance on tracking the S&P 500. This has no doubt come about given the strong returns in the short-term from this index, which has coincided with a shift in money managers more closely resembling the index in their funds:

Asset Managers Mimicking S&P 500 (Bank of America)

My takeaway from this is that money managers have seen the rise and have been "fearing" missing out on further gains so are piling in at an accelerated clip. This is certainly helping short-term moves higher - but is it sustainable? How long can "active" managers demonstrate their worth if they are relying more and more on a passive index like the S&P 500? Probably not long, given what they charge for the privilege of managing your money.

The simple fact is when I see trends like this I get cautious. It tells me that gains - or at least out-sized gains - are not likely to last without a correction to wipe out the excess. I see that as a very real probability heading as we head into the second quarter, and want to maintain a proper level of diversification to protect myself.

It should be clear I favor keeping my portfolio balanced. This means leaning less of large-cap US stocks for the time being. But there are plenty of ways to approach this so, the question here is, why would one want to land on SCHF?

I see two key reasons right off the bat. One is the rock bottom expense ratio for the fund compared to other international ETFs (not to mention CEFs). Schwab charges a minimal fee for owning this product, which is great news for retail holders:

Expense Ratio (Schwab)

This is so low it is essentially negligible, and compares very favorably to the country-specific ETFs I have from iShares, which charge .50%.

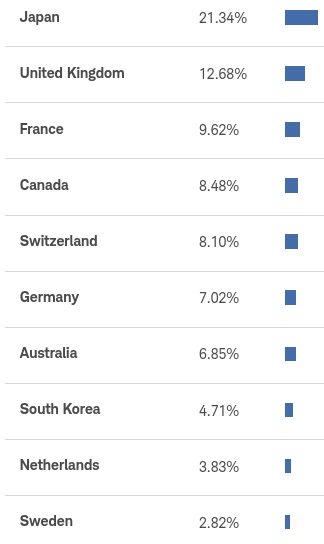

Low expenses are just one positive aspect. This fund is also quite diversified, offering investors exposure to a number of different countries around the globe. This makes the low expense fee all the more meaningful because you are paying a low price to get a large amount of exposure:

Country Breakdown (Schwab)

True, this fund is heavily allocated to Japan and the United Kingdom (I will get to why I like that below). So you are really only getting meaningful exposure (~5% or more) to about eight countries. But that is a pretty good number considering it offers US-based investors a "one stop shop" for getting developed world exposure. I think this can compliment - or even replace - a variety of strategies that would involve owning a lot more funds to get this type of balance. This supports my bullishness on this ETF.

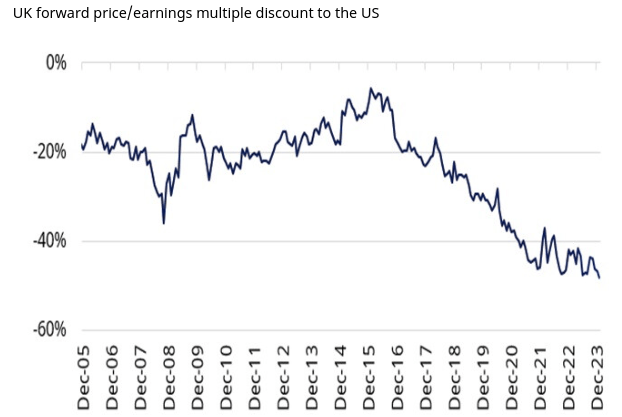

I will now shift to the underlying make-up of SCHF and why I like the prospects. Beginning with the British exposure, readers are likely aware of how cheap the UK has become relative to both the US and Europe. In fact, British stocks are considerably cheaper in both absolute and relative terms, particularly when it comes to smaller companies. While this has been the case for a while, the out-performance by US stocks in 2023 has pushed the relative valuation gap to an extreme:

UK vs US Equity Valuations (Schroders)

There are a number of valid reasons for this: Brexit, political uncertainty, a challenging consumer picture given rising mortgage expenses, among others. But my premise is these problems appear to be baked in. British stocks are exceptionally cheap, meaning they are pricing in a lot of downside and little upside. That is a scenario that offers a reasonable risk-reward in my view.

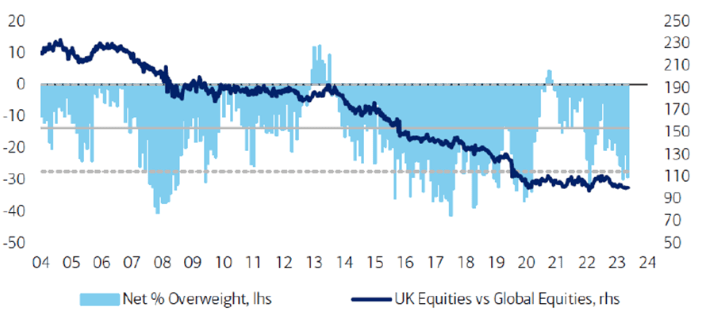

Simply put, this is a bit of a contrarian play. And I love those ideas. It makes sense to buy sectors or country exposure when others aren't. That is how you can get "alpha" if the timing is right. In this case, we see that fund managers are very under-weight the UK, to the point where I only see exposure rising in the future - as I'm not sure it can fall further!

Fund Manager's Exposure to British Stocks (Relative Global Exposure) (Bank of America)

The conclusion I draw here is British stocks are historically unloved and value-priced. That is a win-win in my book and I view SCHF's overweight exposure to this territory as a central reason for why I am a bull going forward.

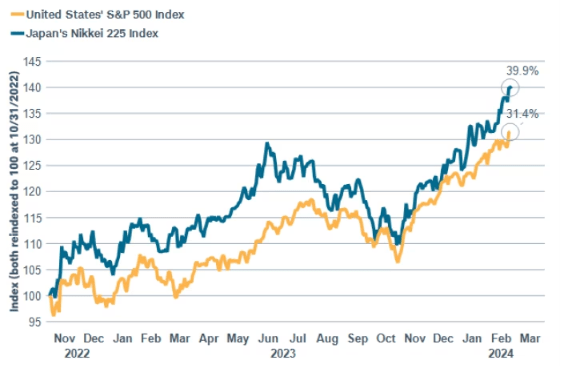

I just highlighted the British story, but what is actually more relevant to SCHF's outlook are Japanese equities. This fund has more than one-fifth of its total portfolio allocated to Japan - so one would want to have a very optimistic view of these equities before buying this particular product.

Fortunately, the inclusion of Japanese equities has been a net gain for SCHF over the past year - or even year and a half. In fact, the big story here at home has been the "Mag 7", which has kept Japan under the radar a bit. This shouldn't really be the case, since Japanese equities have actually out-performed the S&P 500 since the start of the current bull market:

Nikkei 225 vs. S&P 500 (S&P Global)

No doubt this has helped SCHF push higher, illustrating why this fund has had a pretty strong annual return:

SCHF's 1-Year Performance (Excluding Dividends) (Seeking Alpha)

There have been a number of reasons for this strength in Japanese shares. One is that the Bank of Japan (BoJ) kept current monetary policy in place, including negative interest rate policy, at its December meeting. This has been a stark contrast with the rest of the developed world - including the US, Canada, the UK, and Europe, which have seen their central banks hike rates aggressively over the past two years. Lower rates tend to be positive for equities - all other things being equal - so this is certainly helping to fuel Japan's strong performance. While that could change this year, a dramatic shift in monetary policy is not one I would forecast, so the positive tailwind remains in place for the time being.

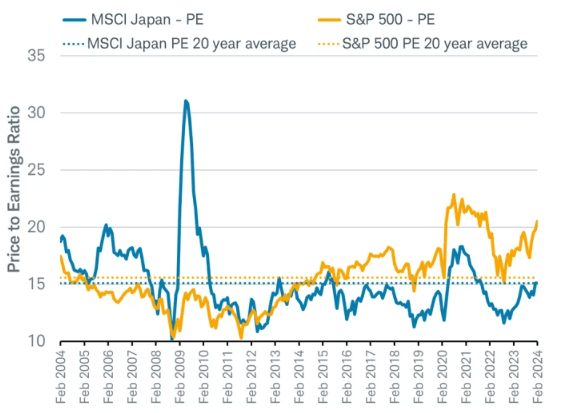

Expanding on the underlying story, valuation matters here too. While Japanese stocks are not enjoying the healthy discount relative to the world, the good news is that shares don't seem overly rich either. This is because while the broader index has been increasing, so too have corporate earnings. This has kept the index's P/E ratio in-line with longer term averages. The same cannot be said for domestic US stocks:

Relative Valuations (Japan vs. US) (FactSet)

For me this gives some comfort that SCHF can withstand some upcoming market volatility. The country exposure that dominates this fund (UK and Japan) is priced in a way that is either cheap or reasonable. There isn't a euphoric sense to these markets the way we are starting to see here at home. This suggests using this fund as a method for diversification has a lot of merit at these levels.

SCHF has had a good run and I see more gains continuing. This is a fund that will help me balance out my US holdings that have seen a metaphoric rise due to the Mag 7. Further, the income stream has been increasing, with the distribution level rising an impressive 22% year-over-year:

SCHF's Distribution History (Schwab)

While the yield is not "high" (at around 3%), I especially like the fact it is growing at such a strong clip. When I couple this with the value inherent in the underlying countries (namely the UK), I see this as a good buy here. Therefore, I am upgrading my outlook for this fund, and suggest my readers give the idea some consideration at this time.