bjdlzx

bjdlzx

Chesapeake Energy (NASDAQ:CHK) announced the acquisition of Southwestern Energy (SWN). At the time, management was not real specific about exactly how this was going to be accretive. More importantly, management was in the process of dumping the Eagle Ford properties. At least one buyer, SilverBow Resources (SBOW) was thrilled with the sales price. So maybe it is time to review the whole transaction to get an idea as to how much this is costing shareholders.

Chesapeake Energy stated that they would exchange .0867 shares of stock for each Southwestern Share of stock. That would make the current Southwestern stock worth roughly $7.17 using $82.81 as the value of the share of Chesapeake stock currently. Note that the price could vary by the time you read this.

Southwestern is showing roughly 1.103 billion shares outstanding in the latest quarterly press release. that makes the value of the shares needed for the acquisition roughly $8 billion in very round numbers. Southwestern also reported roughly $4 billion of debt to make the enterprise value $12 billion (without worrying about adjusting for things like cash to keep it simple).

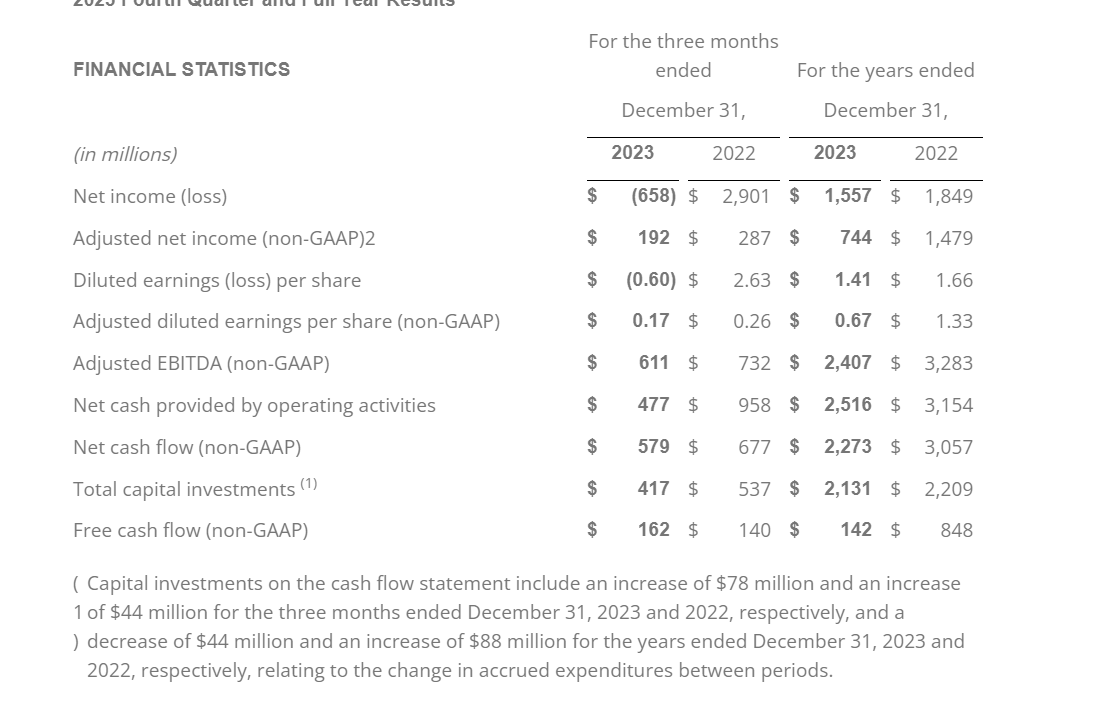

Southwestern Fourth Quarter 2023 Summary Results (Southwestern Earnings Press Release Fourth Quarter 2023)

When that roughly $12 billion is compared to the reported adjusted EBITDA shown above, this transaction has one of the highest valuations compared to EBITDA that I am likely to report for years to come. I have been reporting deals around 3 times EBITDA for a couple of years now. That is before you mention that Chesapeake paid primarily for natural gas production because the Southwestern average price received is only slightly modified by the more valuable liquids produced.

This covers the Eagle Ford properties sold to SilverBow (SBOW). There were other sales not covered here as well. The purchase price of these properties was $700 million, which is no small amount for SilverBow and definitely significant for Chesapeake Energy.

Compare this to the SilverBow acquisition of the Eagle Ford properties, where SilverBow management claimed that the sales price to EBITDA ratio was 2.3 on a far more valuable production mix.

Note that the SilverBow announcement used a lot of numbers to back up the claim that this was a bargain, whereas the Chesapeake announcement used a lot of words like accretive.

More to the point, SilverBow is now going to drill on those acquired lands to increase its production of liquids and likely its profitability during this period of low natural gas prices.

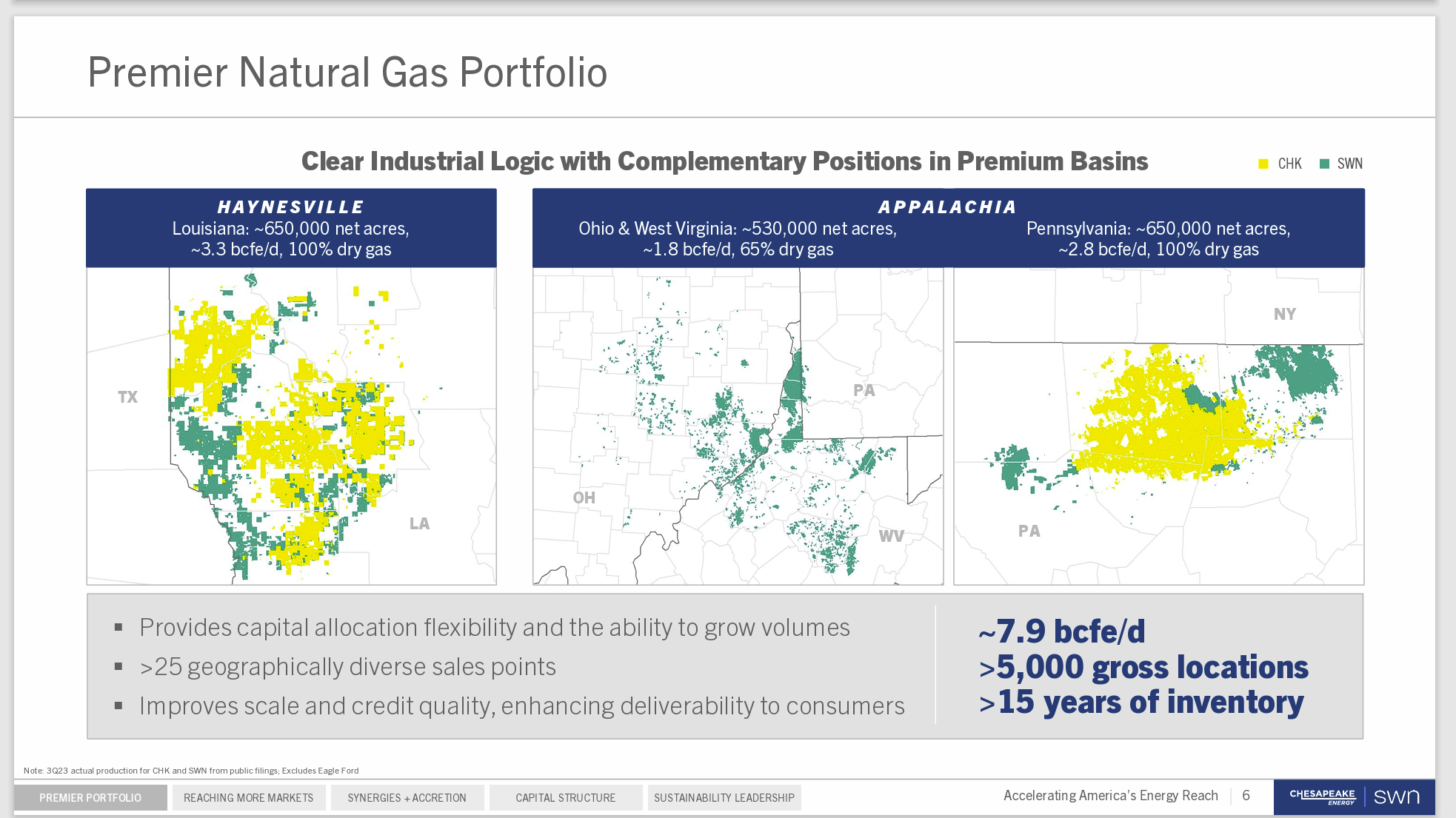

Chesapeake Energy is paying for essentially "bolt-on" acreage in both the Marcellus and the Haynesville as shown below:

Chesapeake Energy Map Of Post Combination Operations (Chesapeake Energy Southwestern Acquisition Announcement Corporate Presentation)

The combined company will have operations in both the Marcellus and the Haynesville dry gas areas. Management is transitioning to a dry gas producer at a time when many in the industry are picking up rich natural gas production to "help out" during times like right now when natural gas prices are low.

The Marcellus is a known low-cost dry gas basin.

The Haynesville, on the other hand, is definitely not low cost because it has swing basin status.

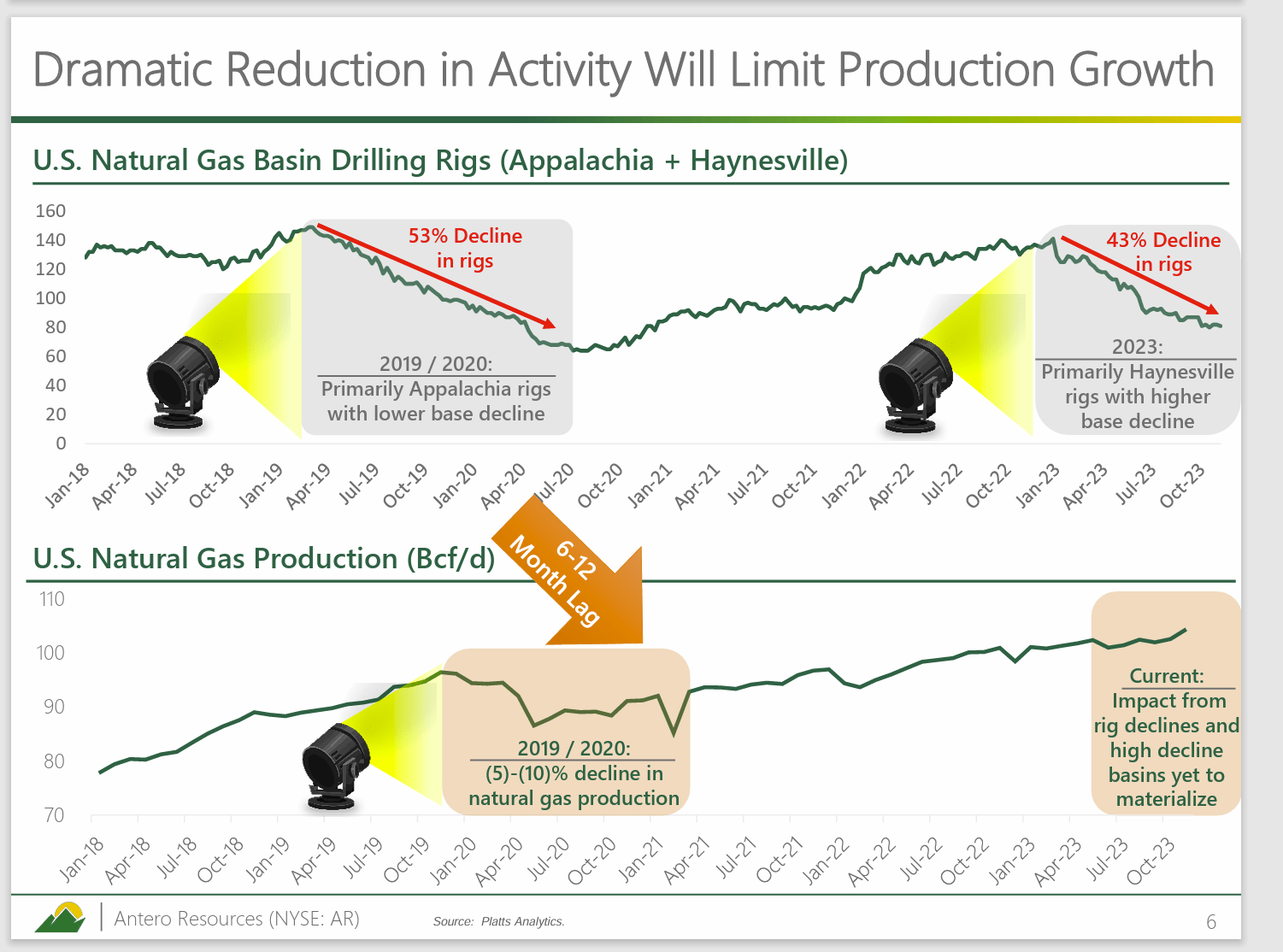

The last time that Antero Resources (AR) gave an update on the situation, this was the status as shown below:

Antero Resources Rig Count Response To Low Natural Gas Prices (Antero Resources Natural Gas Fundamentals Update November 2023)

Clearly, the dry natural gas producers are bearing the brunt of the currently weak natural gas pricing. There is something to be said for purchasing assets at a cyclical low. But given that selling prices in general are about 3 times EBITDA (on average), Chesapeake clearly did not get a bargain for the privilege of idling rigs until natural gas prices improve.

We are probably getting near to the maximum of idled rigs. But natural gas prices have not yet began a pricing recovery. With winter nearing an end, it becomes less likely that natural gas prices would stage any significant pricing recovery without the aid of a hot La Nina summer.

There is pricing hope in that more exporting capability is coming online through the next two years. But very few acquirers value that hope as much as this company did with the acquisition offer.

The last consideration is that Antero Resources often receives the best sales prices (and terms) in the Marcellus Basin. Rarely has Chesapeake management ever discussed sales prices past a general overview. Naturally, the overall average price received is in the quarterly and annual reports. But it is probably important to investors to know that management is getting every last possible extra penny for any production.

Generally, the companies doing the best job tend to communicate that accomplishment, as shown below.

Antero Resources Natural Gas Pricing Advantage (Antero Resources Natural Gas Fundamentals Update November 2023)

Chesapeake does maintain low debt ratios as a general rule. That does take some of the risk out of the investment. But as Antero Resources points out, every extra penny pretty much heads to the bottom line (with only a few subtractions) because the expenses largely remain unchanged.

Therefore, the better the selling price, then the more profitable the company. This is something that Chesapeake needs to discuss in more depth in the future.

Chesapeake does send some production to export. But how is the natural gas sales price doing in each basin compared to competitors?

For me, the valuation of Southwestern Energy compared to the latest sales price of the Eagle Ford acreage makes this stock (of Chesapeake Energy) a clear sell. It is bad enough to dump noncore holdings at a bargain price. But that "bad enough" was compounded with a very rich purchase price for the latest acquisition. Frankly as a shareholder I do not need that as there is far too much money being left "on the table" for others to pick up.

This may work out for shareholders in that the stock price could still appreciate from current levels due to the likelihood of North American natural gas prices joining the usually far stronger world natural gas pricing market as the ability of North America to export natural gas increases.

However, for me, it works out even better if darn good Eagle Ford acreage was not dumped at a bargain price. The shareholders of SilverBow are likely to benefit from that sale (and benefit big time in the future). That is a somewhat foregone opportunity for Chesapeake shareholders.

Right now, dry gas producers are idling rigs because it is not worth it to drill for dry gas at current natural gas prices. As a contrarian opportunity, the current deal has some merit. But the execution could have been far better.