D-Keine/E+ via Getty Images

D-Keine/E+ via Getty Images

I recently sold my shares in New York Community Bancorp, Inc. (NYSE:NYCB), one of my best and one of my worst investments ever. In this article, I will recap my euphoric and depressing experiences holding this stock and the lessons I learned in the process.

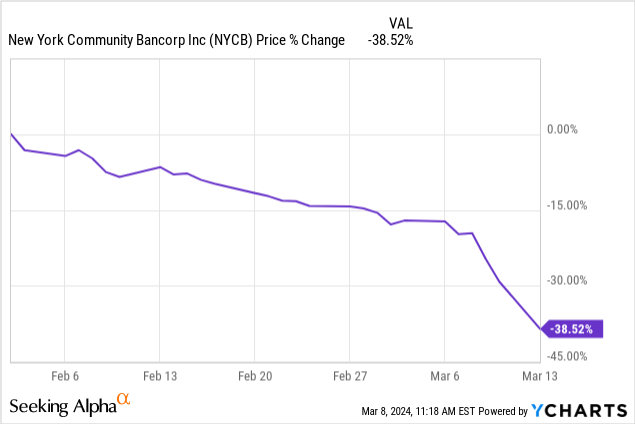

Just over one year ago, the NYCB stock price crashed by nearly 40% during the regional banking (KRE) crisis:

However, while a few other banks were failing and there was concern that panic and bank runs would spread like wildfire across the industry, NYCB seemed to be on solid footing due to its strong branch relationships with clients and its very high percentage of insured deposits. Moreover, I had a chance to interview senior leadership at the company during that period and was able to get answers to my questions. Confident in the solvency of the bank, I took the plunge and timed my buying of the dip almost perfectly, buying the stock at $6.50 on March, 14th 2023.

Within a matter of days, word broke that NYCB was buying up assets from failed Signature Bank (OTC:SBNY) for pennies on the dollar, sending the stock price soaring and making NYCB one of the few winners of the regional banking crisis.

This bullish outcome and a subsequent easing of fears that the banking crisis would spread further caused NYCB stock to deliver exceptional performance in the coming months. Eventually, my fair value target was hit, and I made very large profits in a very short period of time, making it one of my best investments ever, with nearly 400% annualized gains.

However, while I may have made off like a bandit in March 2023 and the months that followed, the monster came back for me this year to take back what was his. With NYCB stock falling significantly from its mid-year highs at the end of last year, I finally succumbed to the temptation to go back for round two with NYCB, making the fateful decision to buy back into the stock on December 22, 2023, at around $10 per share.

This time, once again, I accidentally timed my purchase almost perfectly ahead of a major move in the stock price. Unfortunately, this time it was in the opposite direction. At the very end of January, the company reported a massive GAAP loss for Q4 as NYCB took on enormous loan loss reserves and slashed its dividend.

In the wake of this shock report - which blindsided many, including apparently renowned investors like George Soros who bought shares in the company during Q4 like we did - more negative reports came out, including a slew of negative analysts' reports, credit rating downgrades, and a flurry of headlines that almost seemed to be a coordinated attack on the company's solvency. As a result, the stock continued to plummet with seemingly no bottom in sight.

Then, just when the bottom seemed to be in, management reported material weakness in its internal accounting protocols, pushed back the timing of its 10-K filling, and wrote off its goodwill, while also getting rid of its longtime CEO. But that still wasn't all. On March 6th, the stock tanked even further on news that it was going to investors to raise additional capital. As a result, in less than a month and a half, the stock had dropped from over $10 to $1.76 per share.

Fortunately, the stock bounced back a bit when news broke that a group of investors were injecting $1 billion in equity capital into the company, led by former Treasury Secretary Steven Mnuchin. The fact that his firm was putting roughly 15% of its portfolio into NYCB equity - even if it was at a price of pennies on the dollar - signaled a strong vote of confidence in the company's prospects, causing the stock to quickly recover. Given that the dividend was all but eliminated in the wake of this announcement, massive shareholder dilution took place, and the distressed terms of the deal were unforeseeable by investors, I exited my position at $4 per share yesterday, suffering a brutal ~60% loss of my original investment in a matter of two-and-a-half months.

The market giveth and the market taketh away. The same stock that gave me extremely handsome returns in a matter of days, gave me a precipitous drop in a similarly short period of time. This experience reminded me of the truth laid out by people such as Warren Buffett that a stock has no idea and does not care if you own it or not and that anything can happen to any stock in the short term.

Heading into this past month and a half's drama, NYCB was viewed as a bit of a boring stock. With mediocre growth prospects, conservatively underwritten loans to defensive assets, a high percentage of insured deposits, and a pretty conservative underwriting track record and balance sheet relative to other regional banks, NYCB was supposed to be a low-drama holding. Moreover, with its attractive and well-covered dividend payout that was sustained through COVID-19, it appeared to be a stable income stock.

However, this experience taught me that banks in general - and regional banks in particular - can never be viewed as "sleep well at night" income stocks. This is because the sector is too beholden to news headlines and regulators to make for a sound long-term investment. Ultimately, even otherwise investment-grade banks with conservative underwriting standards, lengthy track records of success (even of weathering the Great Financial Crisis), well-covered dividends, low default rates, and a very high percentage of insured deposits are not immune to a spiraling situation where regulators are strict, and then the media spins the story out of control, forcing management to make decisions that hurt shareholders in a permanent fashion.

While some may criticize Bitcoin USD (BTC-USD) (and not without reason) for being backed by nothing but emotion, banks are ultimately products of emotion as well. The moment confidence in them is gone, they go under. Without confidence, the banking business model cannot succeed.

My investments in NYCB are among the very best and very worst results that I have had in any investment to date, especially on an annualized return/loss basis. That being said, it is hard to pinpoint a true error in my analysis of the losing trade given that I could only work with the information that was publicly provided, and even the likes of George Soros bought the stock shortly before it crashed. It is a case of bad luck compounded with a series of events coming out of seemingly nowhere to amplify the risks to the thesis, leading to a rapid and permanent loss of capital for us as shareholders.

This is the risk that comes with investing, and inevitably even the best of investors like Warren Buffett have big losers (for example, his purchase of the original Berkshire Hathaway eventually went to zero as the business eventually failed). That is why diversification is so important, and, fortunately, this was never a large position for us.

Moreover, an important takeaway for me is that banks - especially regional banks - are not low-risk investments and can end up being quite speculative.

Moving ahead, I view New York Community Bancorp, Inc. as a high-risk investment, and I am steering clear of it as it no longer offers a high enough dividend to fit in with my investment approach - and I also plan to steer clear of the banking sector in general.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.