sandsun/iStock via Getty Images

sandsun/iStock via Getty Images

Note: I previously covered Star Bulk Carriers (NASDAQ:SBLK). My previous article discussed the company’s strengths, such as excellent solvency and liquidity metrics, revenue structure utilizing time charters and voyage charters, and fleet quality. I also pointed out supply chain disruptions and rising major bulk demand as tailwinds for dry bulk shipping. This article dissects SBLK fleet changes, FY23 financial results, and updates company's valuation.

Star Bulk Carriers remains an excellent option for gaining exposure to bulk carriers. The company benefits significantly from the rising demand for major bulks. SBLK's OPEX falls into the industry's lowest quartile, providing the company with a solid margin of safety. SBLK retains excellent financials, with 45.2% Total Debt/Equity and 45.2% Total Liabilities/Total Assets. Compared to Golden Ocean (GOGL) and Himalaya Shipping (HSHP), SBLK trades at reasonable prices. I expect the bulk carriers market to remain strong with a growing demand for iron ore, bauxite, and coal. SBLK is a great way to play that theme. My verdict remains the same—a buy rating.

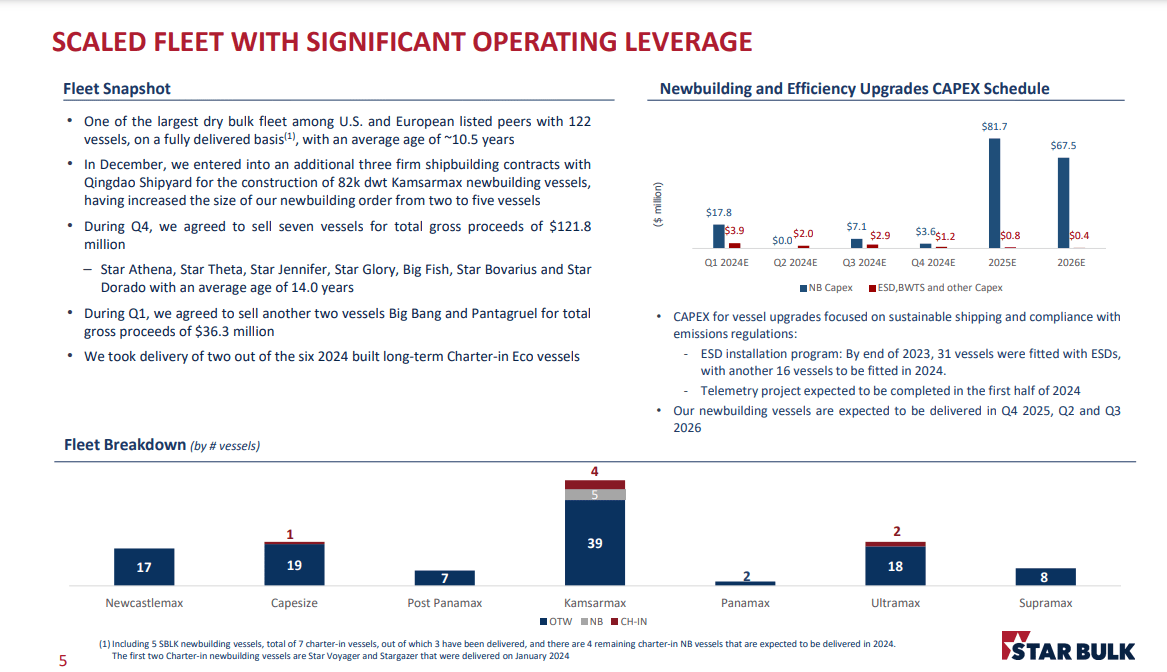

SBLK owns one of the largest bulk carrier fleets globally, consisting of 122 vessels with an average fleet age of 10.5 years. 94% of the ships are scrubber equipped. The table below from the last presentation provides information on the current status of the SBLK fleet.

SBLK presentation

The company owns 36 large bulk carriers: 19 Capesize and 17 Newcastlemax. In the midsize segment, SBLK owns 7 Post Panamax, 39 Kamsarmax, and 2 Panamax. SBLK has 21 smaller vessels, 18 Ultramax and 8 Supramax ships.

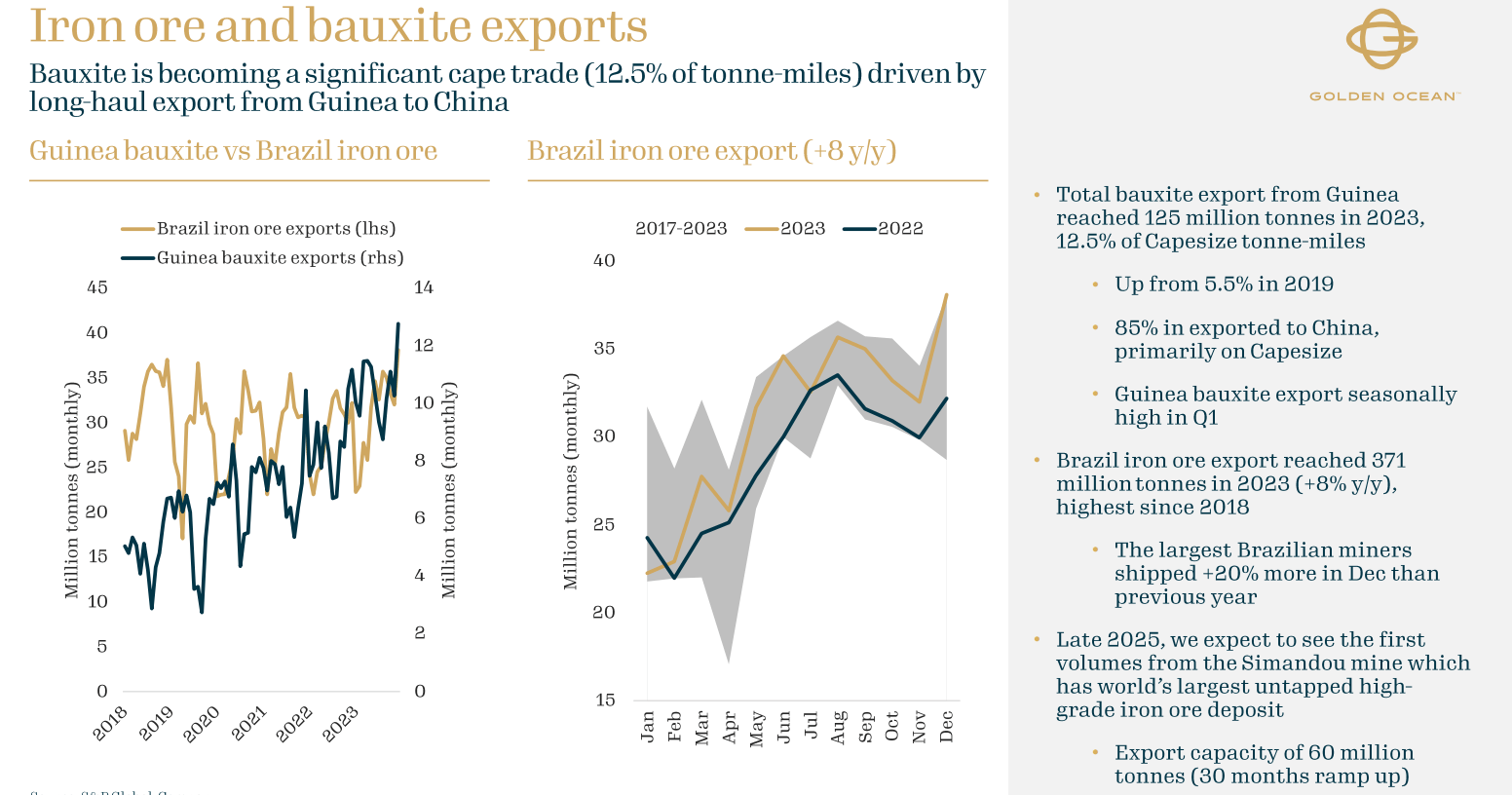

The company is one of the leading players in the Capesize/Newcastle segment, which is, in my opinion, the hottest niche in the bulk market. Those ships carry major bulks such as bauxite, iron ore, and coal. The table below shows the increase in iron exports from Brazil and bauxite exports from Guinea.

GOGL presentation

Iron ore and bauxite exports have risen over the last few quarters, driven by Chinese fiscal stimulus to boost the economy. Besides that, Australian coal exports are growing, again driven by Asian economies.

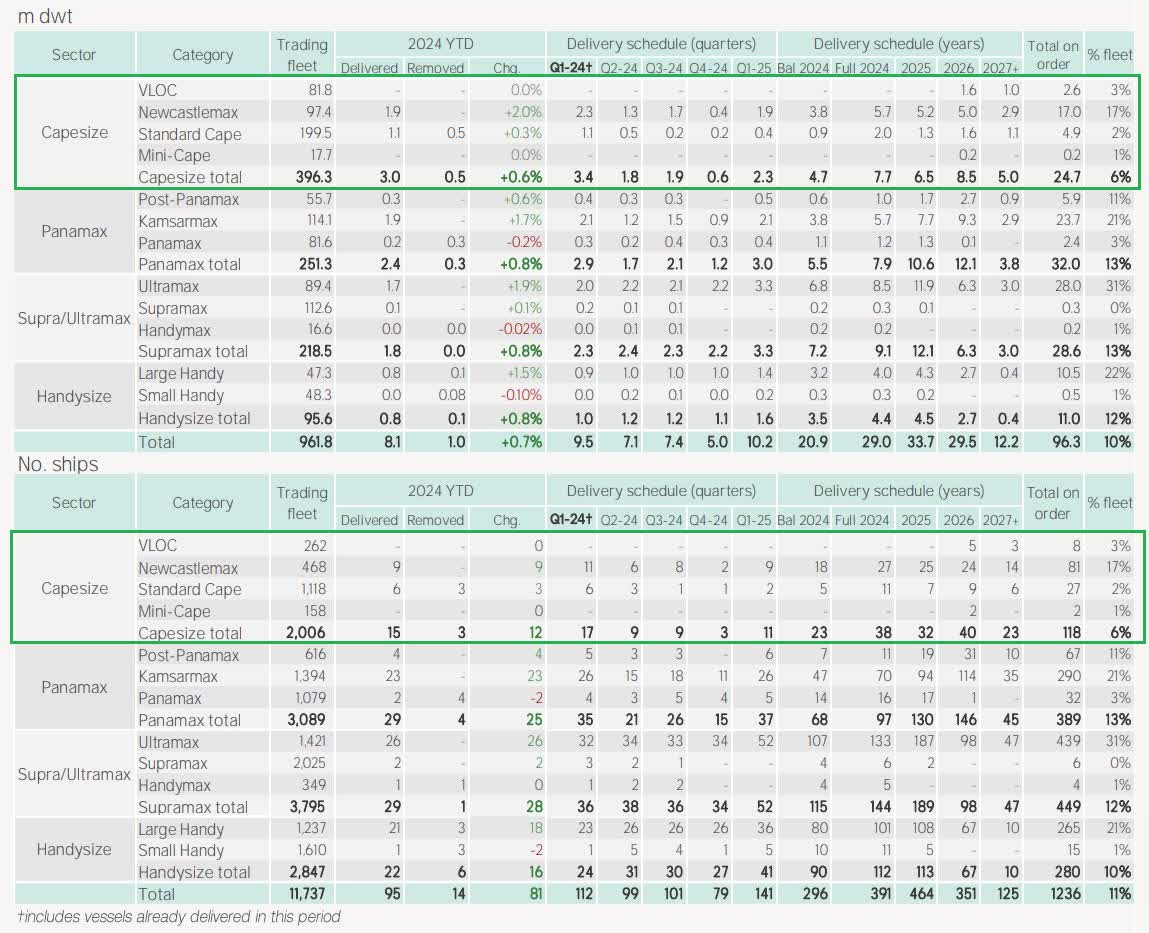

Capes/Newcatlemaxes are the most constrained segment due to well-known factors such as an aging fleet, low order book, and limited shipyard capacity. The chart below from Braemar shows bulk carriers' supply for the next three years.

Braemar/Twitter

The table is divided into two sections. The top shows the global fleet as total dwt, while the bottom shows the number of ships. As seen in the right column, named ''% fleet'' Capesize segment has the lowest order book, 6%, as a percentage of the current fleet. For reference, Panamax, Supramax, and Handysize have order books in the low teens.

The 2024-2027 delivery schedule gets more interesting. For the next 24 months, the deliveries of new Capesize ships measured in dwt are way lower than those of mid-size ships like Panamax and Supramax/Ultramax. Nevertheless, the Handysize segment expects the lowest delivery figures.

SBLK updated its fleet in 2023. Three ships (Athena, Theta, and Jenifer) were delivered to their new owners in November 2023, and Star Glory delivered in January 2024. In addition, SBLK agreed to sell five more vessels over the last three months. For 1Q24, SBLK expects $112 million in proceeds from vessel sales. The plan is to fully repay the outstanding debt on those vessels ($38.7 million) and fully prepay its bridge loan facility with ING.

The company expects two new Japan-built Kamsarmax vessels in 2Q24. In 4Q24, two more ships, one Kamsarmax and one Ultramax, are anticipated. SBLK also entered an agreement with Quingdao Shipyard for five Kamsarmax ships with 82,000 dwt. The delivery is scheduled for 2025/2026.

In 1Q24, SBLK took a delivery of a few vessels: two Kamsarmax and one Ultramax.

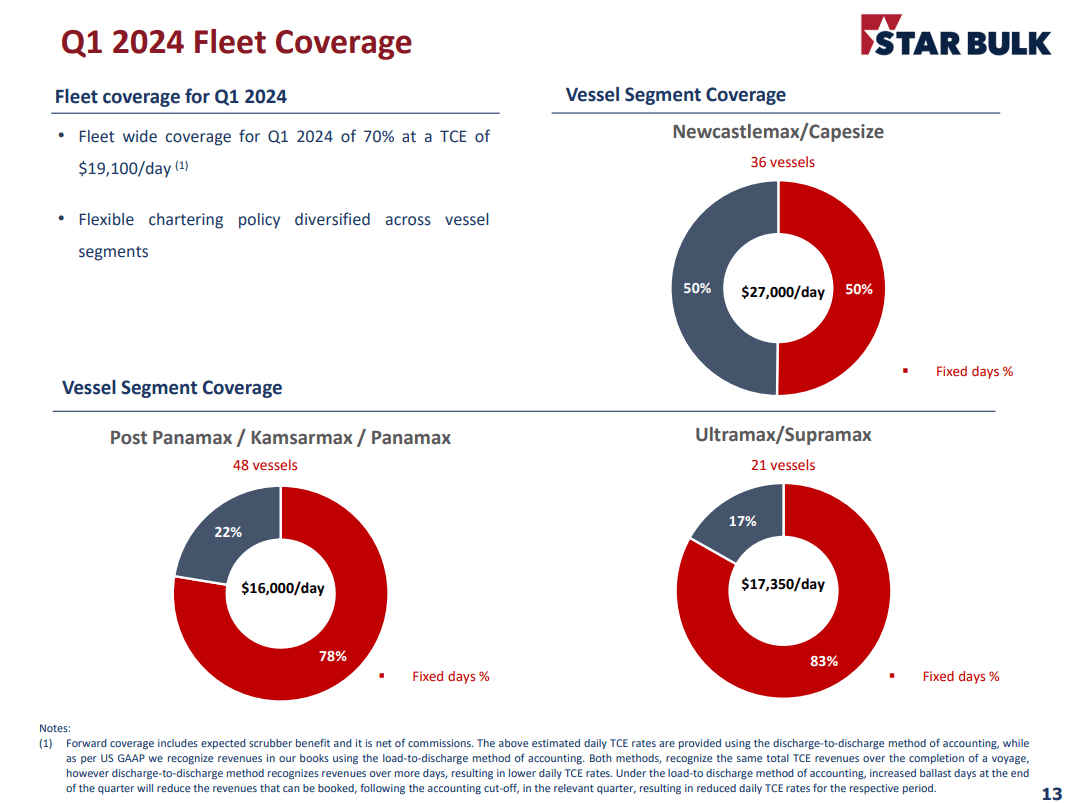

The chart below shows 1Q244 fleet coverage.

SBLK presentation

The pie charts show the ship's 1Q24 employment by vessel segment and average TCE. Capesize/Newcastlemax have 50% fixed days, while mid-size and small-size segments have 78% and 83%, respectively. Fleet-wide TCE is $19,100/day, higher than FY23 ($15,824) and 4Q23 figures ($18,296). On the other hand, the daily OPEX remained stable YoY. FY23 SBLK had daily OPEX per ship of $4,919, compared to $4,893 FY22. G&A expenses were relatively stable, too. FY23 was $1,059, and FY22 was $1,000.

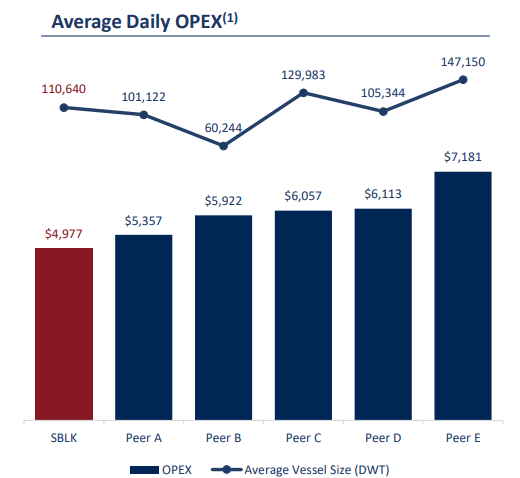

SBLK maintains the lowest daily OPEX compared to its peers, as seen on the chart below:

SBLK presentation

The shipping business is highly volatile. I believe we are just before the middle of the expansion phase of the dry bulk shipping cycle, so there is a lot of upside potential. However, the market might prove me wrong. The day rates may fall abruptly approaching daily OPEX, thus endangering shipping companies' liquidity and, at one point, solvency. Simply put, SBLK’s low OPEX provides the company with a robust margin of safety.

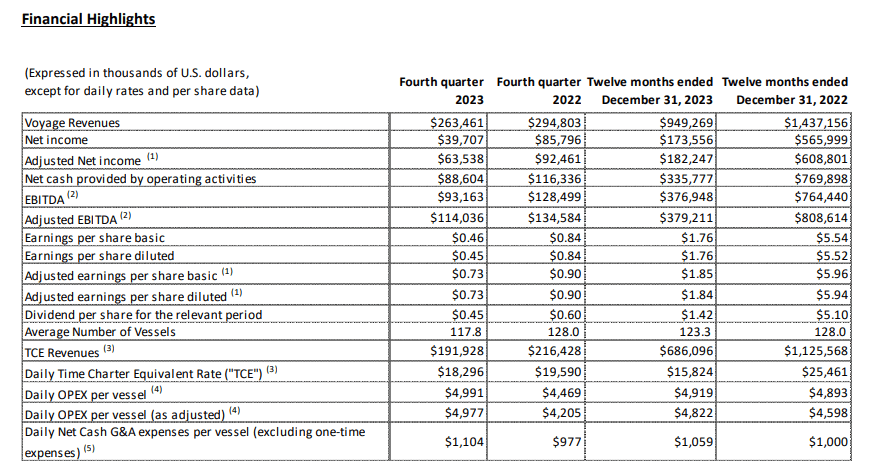

This chapter discusses the company’s financial performance in FY23 and 4Q23. The table below shows SLBK's financial highlights.

SBLK 4Q23 report

SBLK had a good fourth quarter of 2023. The company achieved a composite $18,296/day TCE. It is lower by 6.6% than 4Q22, although it is 15% higher than the FY23 average TCE. Daily OPEX per ship increased by 11% YoY, reaching $4,991 in 4Q23. 4Q23 the company delivered $263 million in voyage revenues, $31 million lower than in 4Q22. The net income for 4Q23 dropped by 54% YoY, resulting in 4Q23 EPS of $0.45. SBLK realized $114 million adj. EBITDA in 4Q23 and $134 million in 4Q22.

Looking at the big picture, SBLK achieved lower TCE figures in FY23 than in FY22, resulting in 34% lower voyage revenues. In FY23, the company delivered $379 million in EBITDA compared to $808 million in FY22. EPS per share dropped from $5.52 to $1.76. On an annual basis, the OPEX increased by 5%, reaching $4,919 in FY23.

The primary driver behind the lower profits was the weaker TCE rates compared to 2022. The expenses remained relatively stable annually and quarterly.

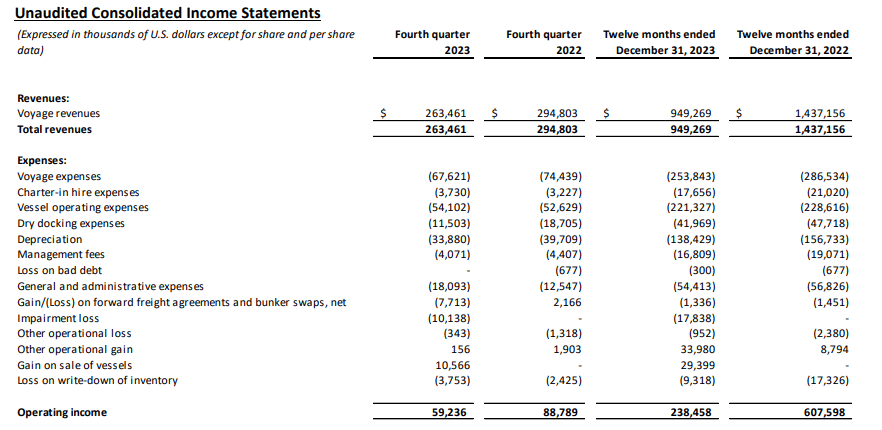

SBLK 4Q23 report

SBLK operates its vessels under spot and time charter contracts, so the company has voyage expenses (bunker costs, canal transit dues, and port fees), too. FY23, the company incurred $253 million in voyage expenses, which was 8.5% lower than FY22. Daily OPEX per ship, as seen above, remained stable. YoY total OPEX declined by $7 million, reaching $221 million.

The only significant change is in the impairment loss. FY23, SBLK recorded a loss of $17.38 million. $10.1 million is related to two vessels (Big Fish and Big Bang) that were agreed to be sold. Another $6.2 million in losses was caused by inventory write-downs because of their lower value than their historical cost.

In the last report, SBLK declared $227 million in cash (ex. restricted cash), $970 million in long-term debt, and $1,368 million in total liabilities. The company maintains a prudent capital structure with 45.2% Total Liabilities/Total Assets and 76.2% Total Debt/Equity. SBLK has adequate liquidity, too. In FY23, the company delivered $335 million in operating cash flow and $196 in operating income. Over the same period, the company paid $58 million in net interest expenses.

In November 2023, SBLK entered into an agreement with the National Banks of Greece for a $151.1 million loan (NBG $151 million facility). The funds were used to refinance a $81.1 million loan under NBG's $125 million facility and to repurchase its shares from Oaktree Capital. The NBG facility is payable in 12 consecutive quarter installments, and one balloon payment is due in November 2026.

The big corporate event in FY23 was the merger between SBLK and Eagle Bulk Shipping (EGLE), announced on December 11, 2023. Below is an excerpt from my previous article on SBLK, discussing the merits of SBLK/EGLE merger.

The new fleet structure will improve SBLK's exposure to the smaller bulkers (Ultramax and Supramax). EGLE owns 52 vessels (22 Supramax and 30 Ultramax), at an average age of 10 years. More than 90% of the ships have scrubbers. Both companies have 169 vessels and 97% of the pro-forma fleet has scrubbers.

The "new" SBLK will have liquidity of $420 million and net leverage of 37%. $50 million are the expected synergies between the EGLE and SBLK.

The deal is expected to close in 2Q24 or 3Q24. The next step is the EGLE special meeting, during which the company’s shareholders will vote on the deal's completion.

SBLK declared a $0.45 quarterly cash dividend. The TTM dividend yield is 5.88%, while the FWD yield is 7.45%. In 4Q23, the company repurchased 20 million shares, valued at $380.0 million, from Oaktree Capital Management.

To estimate SBLK's value, I use P/NAV and relative valuation. To calculate fleet replacement cost, I use the last Compass Maritime weekly. The quoted prices are for five- and ten-year-old vessels. Given SBLK`s average fleet age of eleven years, I use 5% annual depreciation to estimate the price discounting the price of a ten-year-old ship.

The inputs for the NAV equation are as follows:

SBLK’s fleet replacement value is $3,289 million.

NAV input figures are:

SBLK NAV = $2,375 million

SBLK Market Cap = $1,980 million

P/NAV = 83%

I picked Golden Ocean Group (GOGL), Himalaya Shipping (HSHP), and Genco Shipping (GNK) for comparative valuation. The reason is simple: those companies have high exposure to the Capesize segment.

GOGL has 95 ships, 52 Capesize vessels with an average age of 8.0Y, and 31 Panamax with an average age of 6.0Y. Genco owns 18 Capesize ships and 27 Ultramax/Supramax vessels. 67% of GOGL’s Capes fleet has scrubbers. GNK’s fleet average age is 11.7Y, and 37% of the ships are scrubber-equipped. HSHP has a Newcastlemax-only fleet of 12 ships with an average age of 1Y. All HSHP ships have dual-fuel LNG propulsion plus scrubbers.

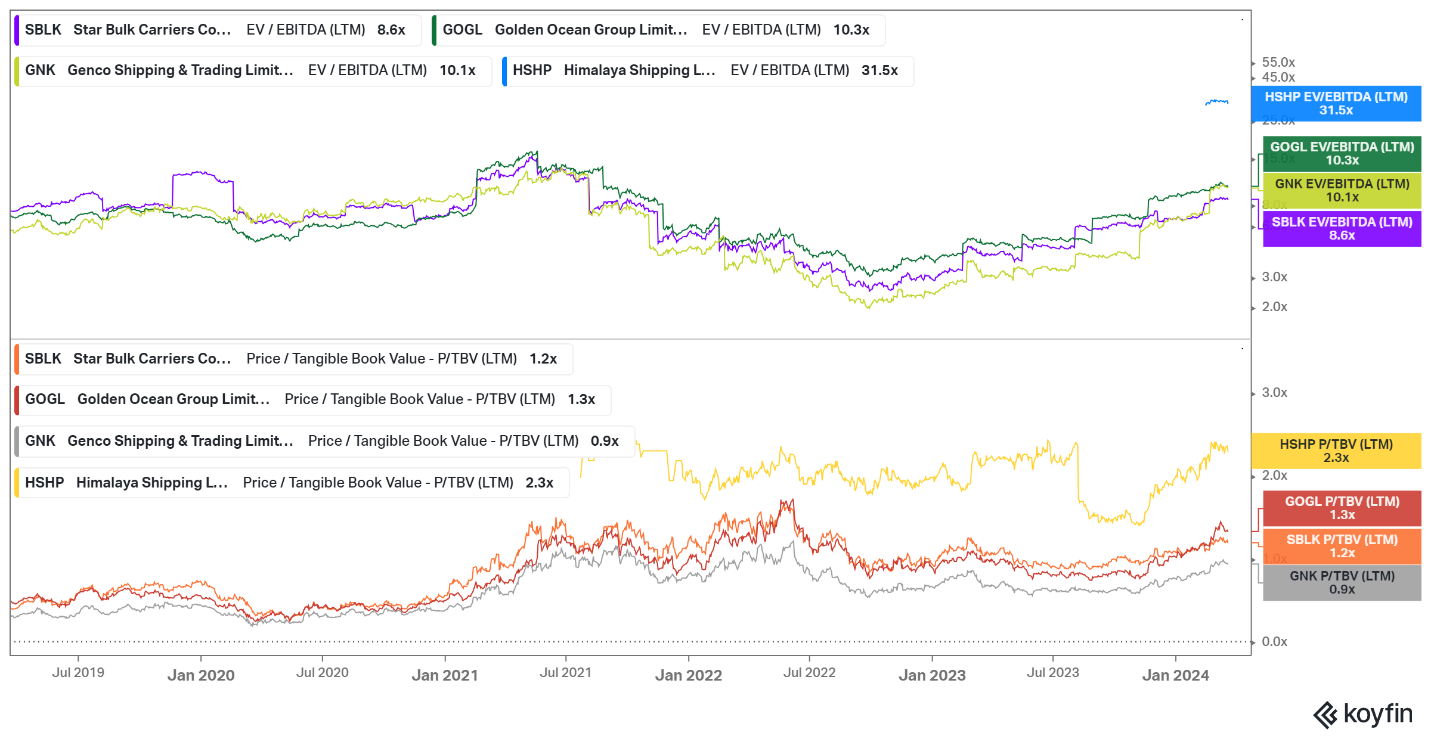

Koyfin

SBLK trades at the lowest EV/EBITDA. Besides that, the company is the second cheapest with its 1.2 P/TBV, next to GNK. HSHP commands the highest multiples; however, we must consider its brand-new Newcastle-only fleet with dual-fuel engines. It is a formidable advantage at that stage of the cycle. GNK, on the other hand, has the oldest fleet, with less than half of the ships having scrubbers.

SBLK offers a diversified fleet at a reasonable price. I prefer companies with a focus on one ship segment. Prime examples are DHT Holdings (DHT) with its VLCC fleet and HSHP with its Newcastle-only fleet. However, the concentrated approach has its disadvantages. The top one is the quality of our thesis. Forecasting a general growth in demand for one broad shipping theme is more straightforward than forecasts for only one segment. Hence, as investors, we are prone to fewer mistakes. Diversified companies like SBLK, yet not conglomerates like Navios Maritime (NMM) or Tsakos (TNP), are great for exposure to a broader theme, such as growing dry bulk transportation demand.

SBLK is an excellent option for playing the dry bulk cycle. The company has a large, diversified fleet with an average age of 10.5Y. 94% of the ships are equipped with scrubbers. SBLK is financially sound, with robust solvency and liquidity metrics. It also pays dividends with adequate yield at 5.88%.

SBLK's primary risk is the Chinese economy. If the fiscal stimulus is unsuccessful, the demand for major bulks may fall, resulting in decreased demand for bulk carriers. At least for now, the figures affirm that the fiscal measures are working, boosting the demand for iron ore, bauxite, and coal.

An idiosyncratic risk is an aging fleet. SBLK's fleet is older than its major competitors, like GOGL. Older ships mean higher maintenance and unplanned repairs costs, plus extended downtimes, which reduces the company`s profitability. One of SBLK's strengths is the best-in-class OPEX. It provides a wide margin of safety in case of declining day rates and rising operating expenses due to maintenance and repairs.

SBLK maintains a prudent capital structure and ample liquidity. The company has spare dry powder to survive a crisis even in the worst-case scenario, shrinking Chinese economy and global recession. Besides that, having a conservative balance sheet allows the company to expand and renew its fleet.

I own SBLK shares, so my verdict remains unchanged. I give the company a buy rating.