morfous

morfous

One of the companies that I have been the most bullish on over the past several months, but do not own shares of, is telecommunications firm Crown Castle (NYSE:CCI). For those not familiar with the company, it owns and operates telecommunications towers and other related assets such as fiber and small cell operations. Since I initially rated it a 'strong buy' back in October of last year, shares have seen an upside of 21.9% compared to the 17.3% rise seen by the S&P 500. But more recently, performance has lagged. Near the end of November of 2023, I reiterated the 'strong buy' rating I had on the stock because of news that came out involving activist investment firm Elliott Investment Management stepping into the picture and proposing a significant change to the operation. I lauded their approach, even though I felt as though the strategy to create the value they saw was not necessary. But since then, shares have lagged the broader market, seeing an upside of only 1.2% compared to the 11.8% rise generated by the broader market.

Fast forward to today, and we do have some additional data to work with. In addition to the drama going on at the upper echelons of the business, there's also additional fundamental data that covers through the end of 2023. Management has also provided guidance for 2024. While the picture could be better and it's clear that there are some weaknesses for the enterprise, all of this, in the aggregate, shows just how cheap the stock remains. This, in turn, underscores just how valuable the company truly is and makes me feel confident that the 'strong buy' rating I assigned the stock still makes sense even in light of some underperformance recently.

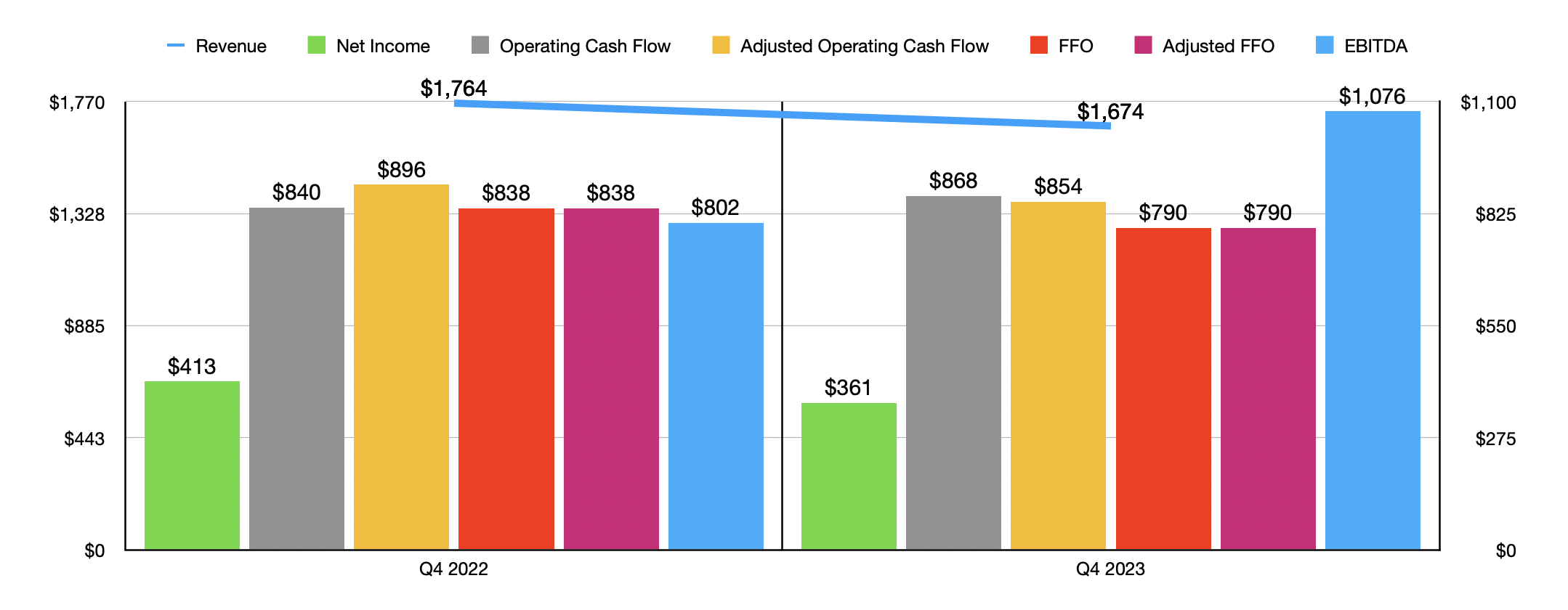

Financially speaking, things could be a bit better for Crown Castle. I say this after looking at financial results covering the end of the 2023 fiscal year. Revenue for that time, for instance, came in at $1.67 billion. That represents a decline of 5.1% compared to the $1.76 billion generated one year earlier. This decline came even as revenue associated with the company's Fiber segment managed to climb by 7.1% from $495 million to $530 million. If you recall, this is a segment of the company that provides capacity to the 115,000 small cells that the firm has in operation and the 90,000 route miles of fiber that supports said small cells and other fiber-related solutions that the firm provides customers. This kind of growth does not surprise me. I say this because revenue had grown for that segment as a whole for the year. Management has invested heavily in this part of the business in recent years, which helps to explain some of the increase in revenue.

Author - SEC EDGAR Data

The weakness for the company, then, came from the Towers segment. Revenue actually fell from $1.27 billion to $1.14 billion. The vast majority of that decline, however, was driven by a plunge in what the firm calls segment services and other revenues from $183 million to $65 million. Management chalked this up to lower volume of activity from 'carriers' network enhancements' and to a reduction in the volume and the mix of services associated with other miscellaneous work.

On the bottom line, Crown Castle has also been hit. Net profits went from $413 million in the final quarter of 2022 to $361 million in the final quarter of 2023. This was driven by pain across both operating segments. Towers operating profits, for instance, took a $40 million hit that came about because of margin and contraction associated with the aforementioned drop in sales. Fiber also declined, thanks largely to site abandonment fees associated with cancellations from Sprint. Other profitability metrics were mixed but mostly negative. The one that was positive was operating cash flow. It ticked up from $840 million to $868 million. But if you adjust for changes in working capital, you get a decline from $896 million to $854 million. As the first chart in this article shows, other profitability metrics also took a hit. These include FFO, or funds from operations, adjusted FFO, and EBITDA.

Author - SEC EDGAR Data

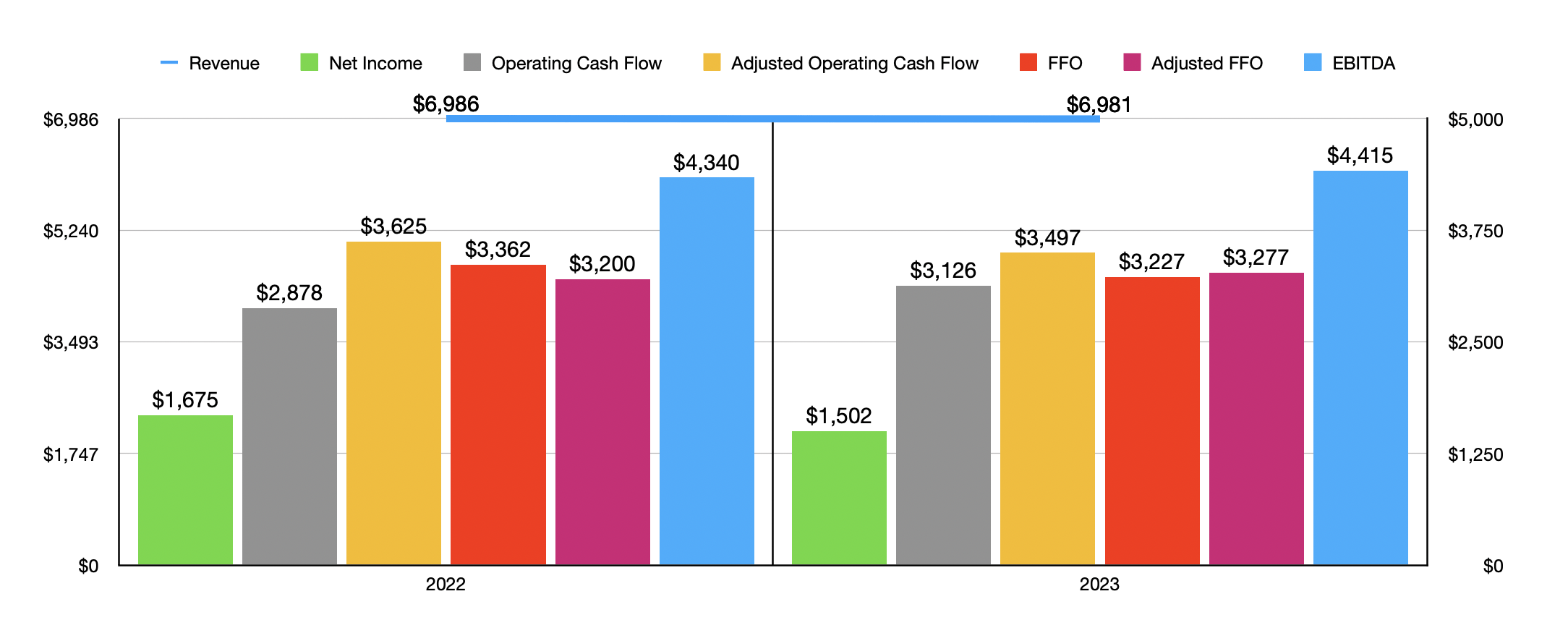

As the chart above illustrates, the final quarter of the year was instrumental in negatively affecting 2023 as a whole relative to 2022. Without those bad results, revenue for the company would have increased year over year. And while there were some profitability metrics that were down even without the final quarter, some of them managed to still improve. As an example, adjusted FFO rose from $3.20 billion to $3.28 billion. Meanwhile, EBITDA for the company managed to climb from $4.34 billion to $4.42 billion.

Unfortunately, this year is probably going to look a bit different. Management has provided guidance when it comes to three very important profitability metrics. The first of these is adjusted FFO. It's forecasted to be around $3.01 billion. That's down from the $3.28 billion generated last year. This likely means that FFO will fall to somewhere around $2.96 billion. Meanwhile, EBITDA is now expected to come in at around $4.16 billion. That represents a decline from the $4.42 billion generated in 2023. Net profits have also been forecasted to be around $1.25 billion. That's a drop from the $1.50 billion generated last year. If we assume that adjusted operating cash flow will change at the same rate that EBITDA is forecasted to, we can expect a reading for the company then of $3.30 billion.

Author - SEC EDGAR Data

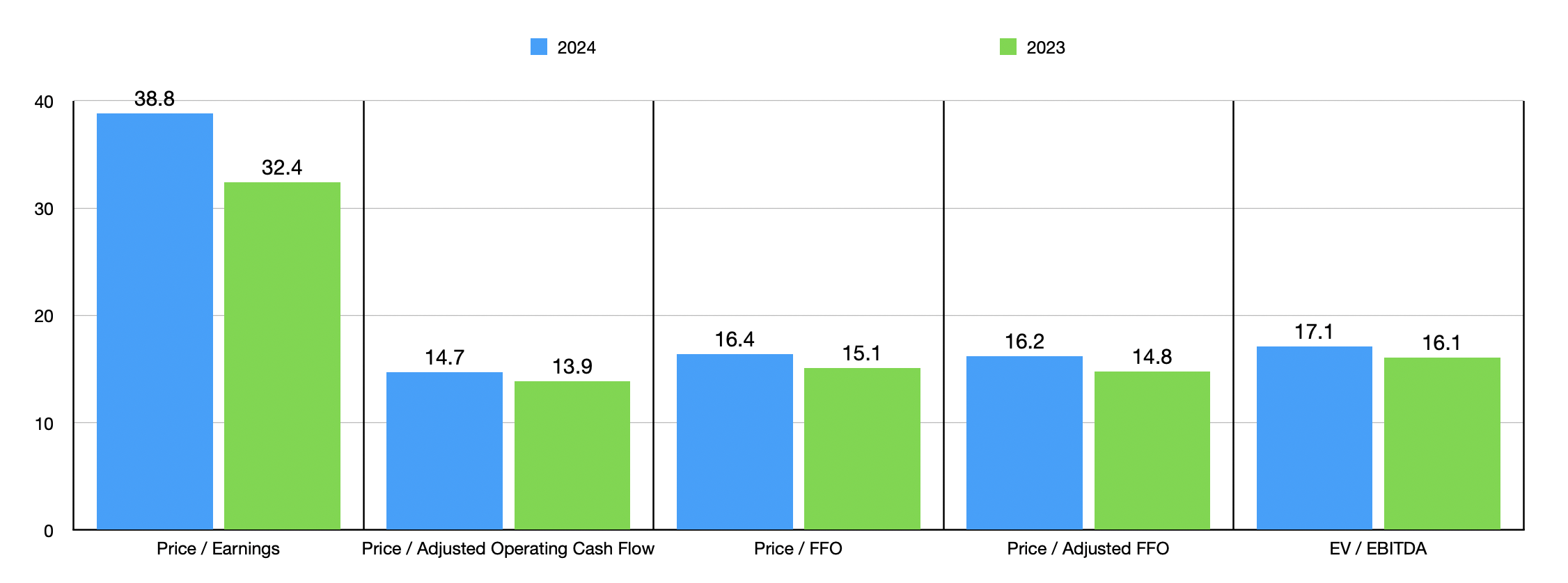

By taking these estimates, it's easy to value the company. As shown in the chart above, the stock looks very expensive relative to earnings. But when it comes to the other profitability metrics, it's not so bad. Generally speaking, multiples like these would fit the company into the fair value category in my book. But I do make exceptions for certain types of businesses. The fact of the matter is that Crown Castle is a true cash cow with robust margins. It also operates in an industry that should, over the long run, see steady growth. This stability and cash generation warrants a higher trading multiple than your typical retailer or shipping company or shoe manufacturer. What's also important to point out is that, relative to similar firms, shares of Crown Castle are cheap. In the table below, you can see the company compared to two similar firms. Using both the price to operating cash flow approach and the EV to EBITDA approach, shares do look attractively priced.

| Company | Price/Operating Cash Flow | EV/EBITDA |

| Crown Castle | 14.7 | 17.1 |

| American Tower (AMT) | 20.4 | 23.4 |

| SBA Communications (SBAC) | 15.8 | 21.4 |

What I did next was to see what kind of upside potential, if any, might be achievable should shares of Crown Castle come to trade at or near where those two rivals are. In the table below, you can see two different scenarios. The first covers what the picture would look like if the company were to trade at either the price to operating cash flow multiple of the cheaper of the two competitors, or at the EV to EBITDA multiple of the cheapest. In this case, we are looking at an upside of between 7.5% and 36.7%. In the second scenario, I did the same thing but by averaging out the two firms. In this case, an upside would be between 23.1% and 45.3%.

Author - SEC EDGAR Data

Those who disagree with my assessment will argue that there are some key differentiators between the businesses. I agree wholeheartedly. A great example that does not work in Crown Castle's favor is the fact that, because of its years of massive investments in small cells and the slower growth rate that space has seen compared to expectations, the firm has failed to keep up with the other two in terms of expansion. However, that's why I'm excited about the activist investor angle here. The fact of the matter is that management is exploring its options and has even gone so far as to rebuff the efforts of its former executive to step back into the picture after more than two decades away. In all likelihood, change will be coming in the not-too-distant future.

Author - SEC EDGAR Data

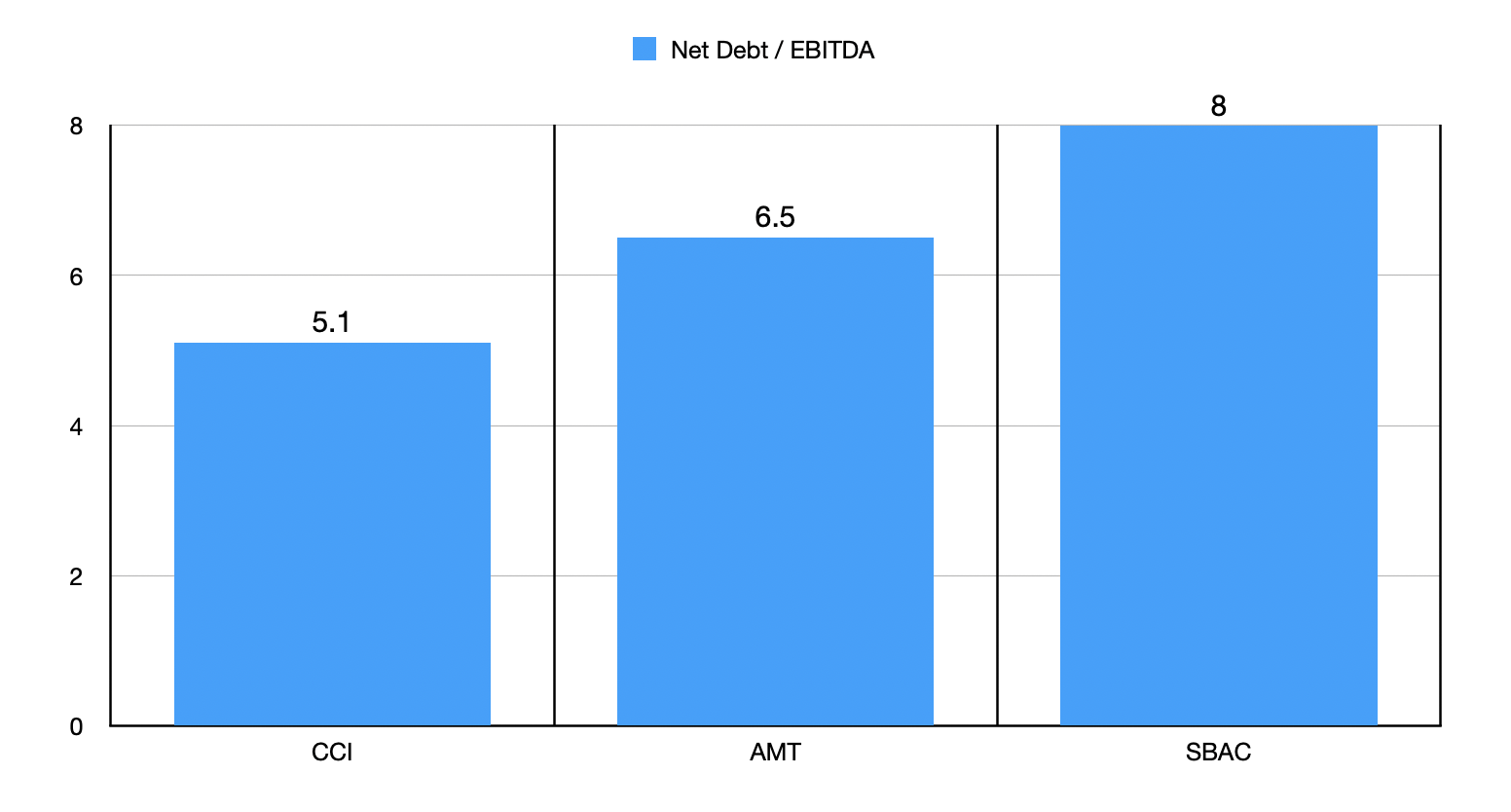

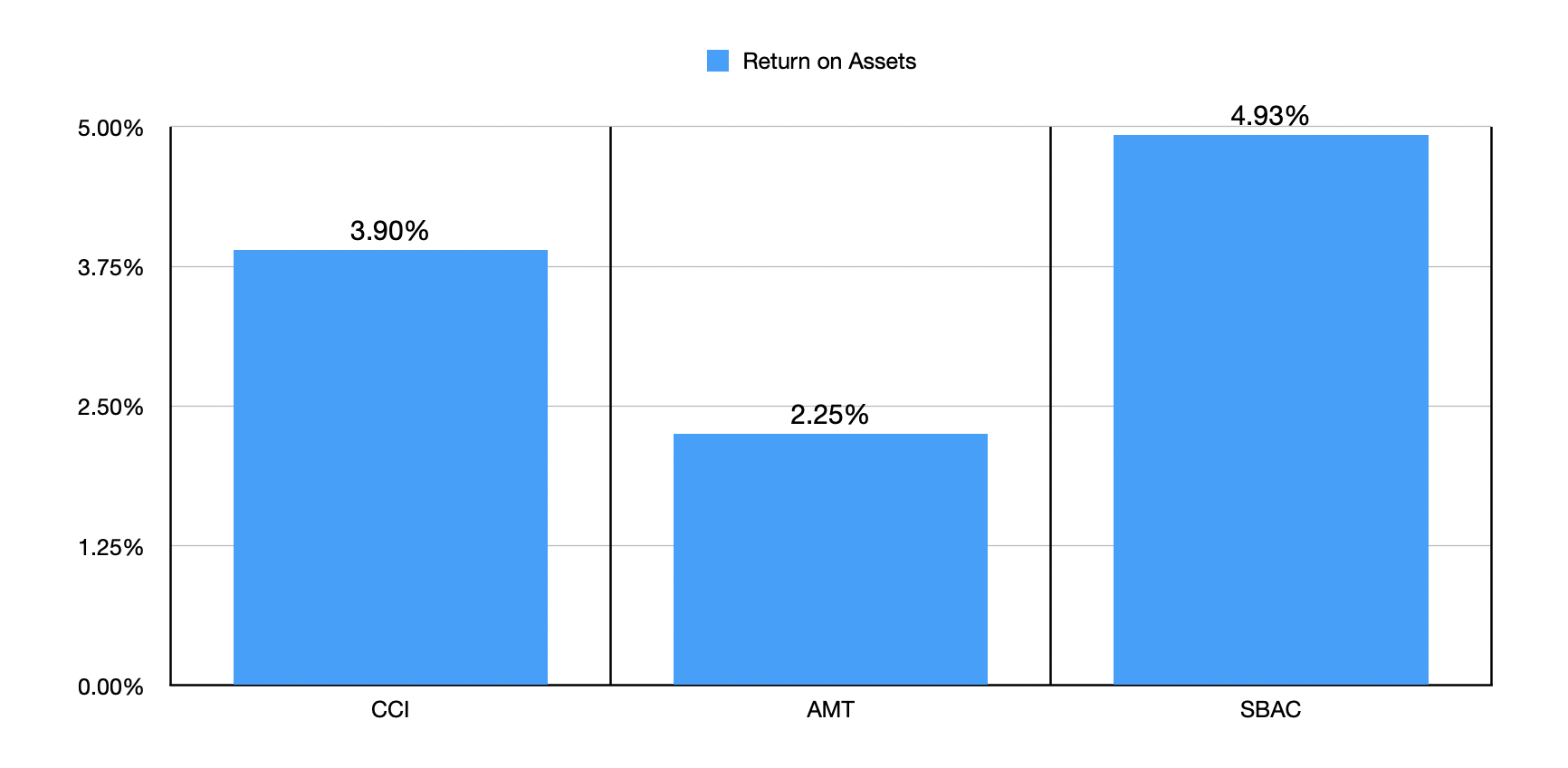

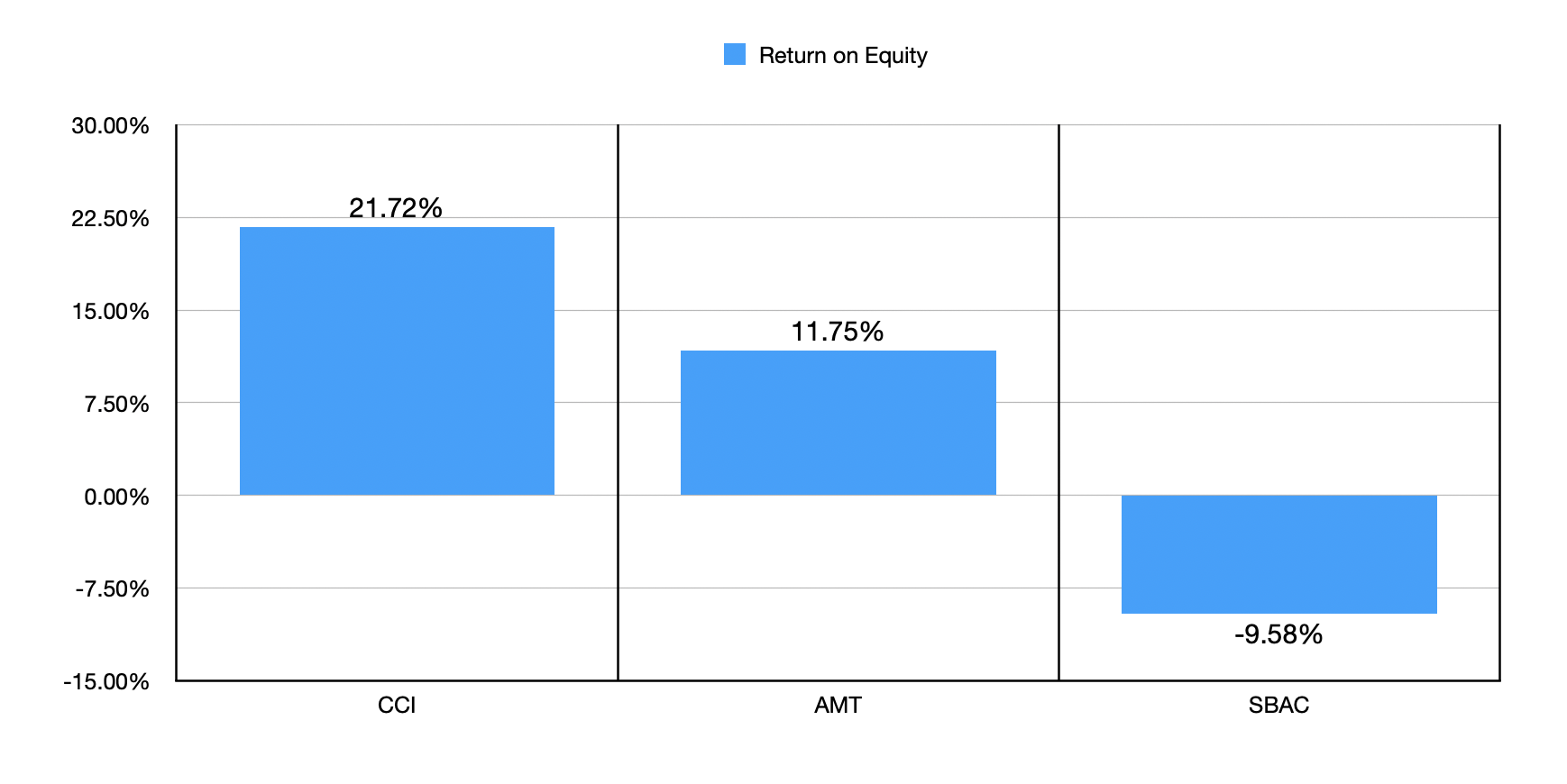

In the event that significant change does take place, shares of Crown Castle stand to skyrocket higher. If the company can get back on track from a growth strategy perspective, I would argue that it might even deserve to trade at a premium to the two aforementioned rivals. This is for multiple reasons. For starters, although the net leverage ratio has increased recently, it stands at 5.1. As you can see in the chart above, this is lower than either of the peers. But then there's also the topic of asset quality. In the first chart below, you can see the return on assets for all three players. Instead of being at the bottom of the group, Crown Castle is in the middle. But when it comes to return on equity, which is shown in the subsequent chart, our prospect is at the top of the list.

Author - SEC EDGAR Data Author - SEC EDGAR Data

Based on the data provided, Crown Castle is a high-quality company that has had some issues. If those issues do get resolved as I discussed in the article that I wrote about the firm late last year, I believe that upside potential could be very significant. Relative to similar firms, shares are cheap and leverage is in check. Of course, it would be nice to see leverage come down even more. Absent something catastrophic happening, I would argue that the 'strong buy' rating I assigned the stock previously should hold until the stock rises nicely from this point.