Joe Raedle

Joe Raedle

In a surprise move, JetBlue Airways (NASDAQ:JBLU) and Spirit Airlines (NYSE:SAVE) announced plans to mutually terminated their merger agreement. The move isn't shocking after the judge originally blocked the merger, but the airlines had announced plans to pursue an appeal with a hearing in June. My investment thesis remains ultra bullish on both airlines following the weakness in both stocks over the last year.

Before the market opened, the airlines announced the mutual agreement to terminate the merger agreement. Both companies discussed issues with the timing of completing the merger with JetBlue highlight the July 24 timeline.

Either way, the termination agreement includes JetBlue paying Spirit Airlines a $69 million fee. In total, JetBlue has already paid Spirit shareholders $425 million, pushing the total payments to $494 million.

JetBlue has paid a hefty price not getting the merger approved. Despite this price, JetBlue has traded up on the news while Spirit Airlines is down substantially with the removal of a potential windfall approval with the merger price still at nearly $30.

JetBlue avoids the $3 billion-plus in net debt in cash payments to Spirit Airlines shareholders from closing the deal along with trying to turnaround the combined business that struggled during 2023. Either way, one can make a bull case for both airlines with the stocks trading at the merger lows.

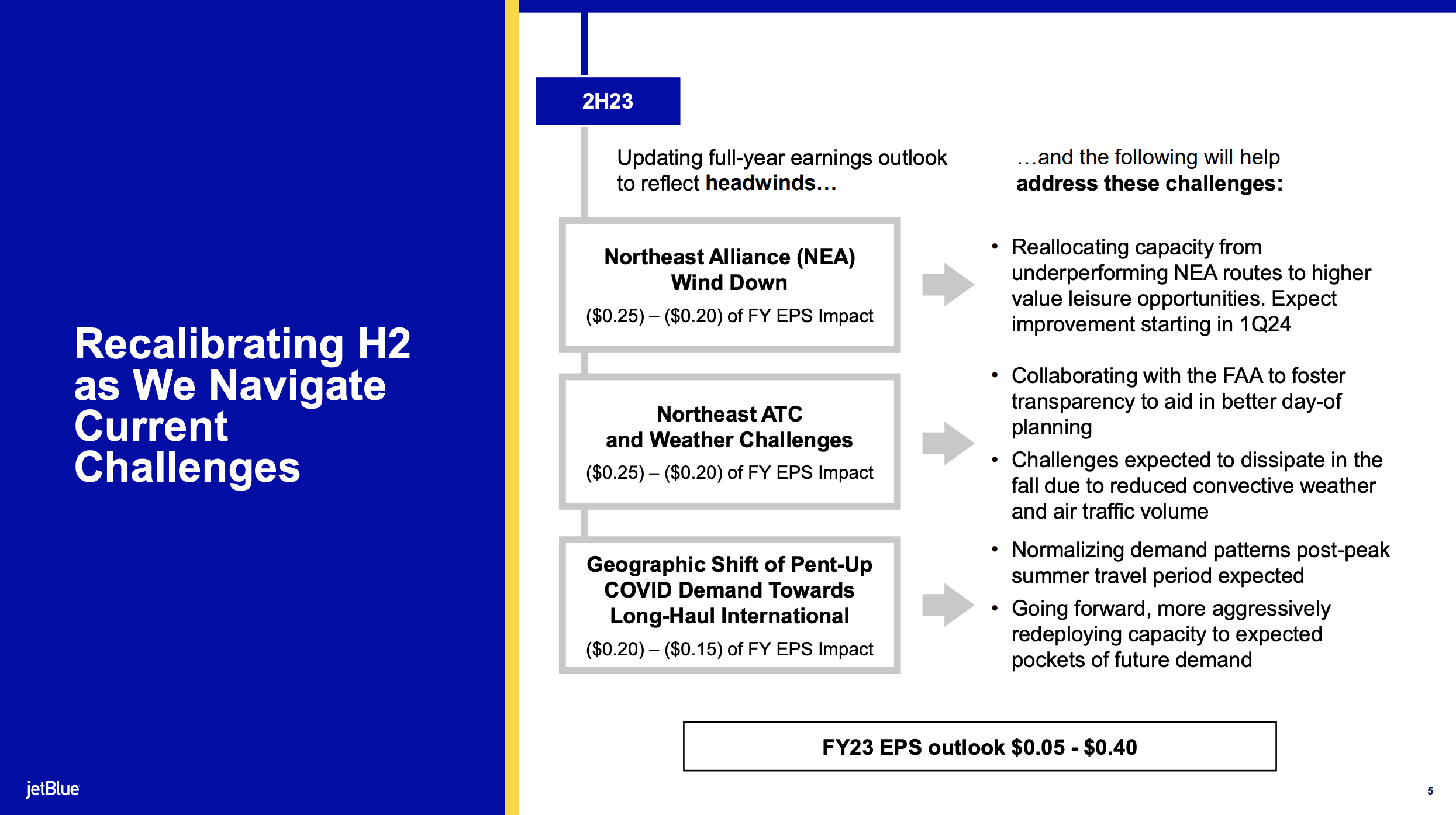

The airline stocks haven't had a great few years despite returning to producing billions in profits and operating cash flows. The cruise line stocks continue surging despite facing more shutdowns due to COVID while airlines like JetBlue faced a multitude of issues in 2023 that hit earnings and shouldn't repeat going forward.

Source: JetBlue Q2'23 presentation

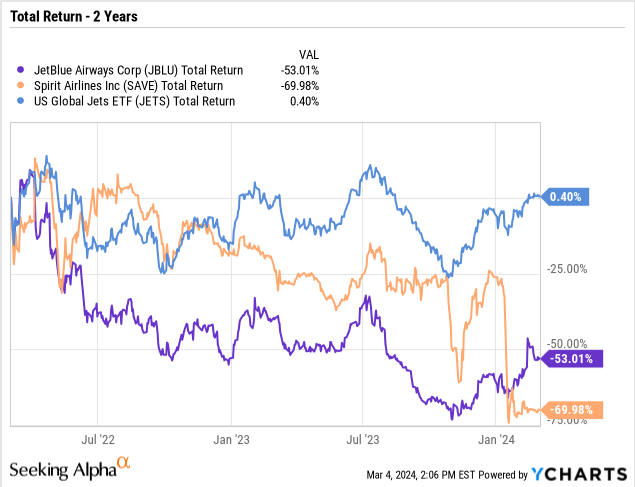

The only issue with the airline sector is that domestic traffic faced more pressure during 2023 in part due to two strong participants focused on domestic traffic not making necessary business adjustments due to a focus on the merger. In the last two years, JetBlue is down 53% and Spirit Airlines has fallen 70% while US Global Jets ETF (JETS) is basically flat.

JetBlue has now adjusted the business to reduce capacity in 2024 and defer a large amount of capex out beyond 2028. The plans immediately reshape the airline's path to profitability that JetBlue had lost during the focus on the merger.

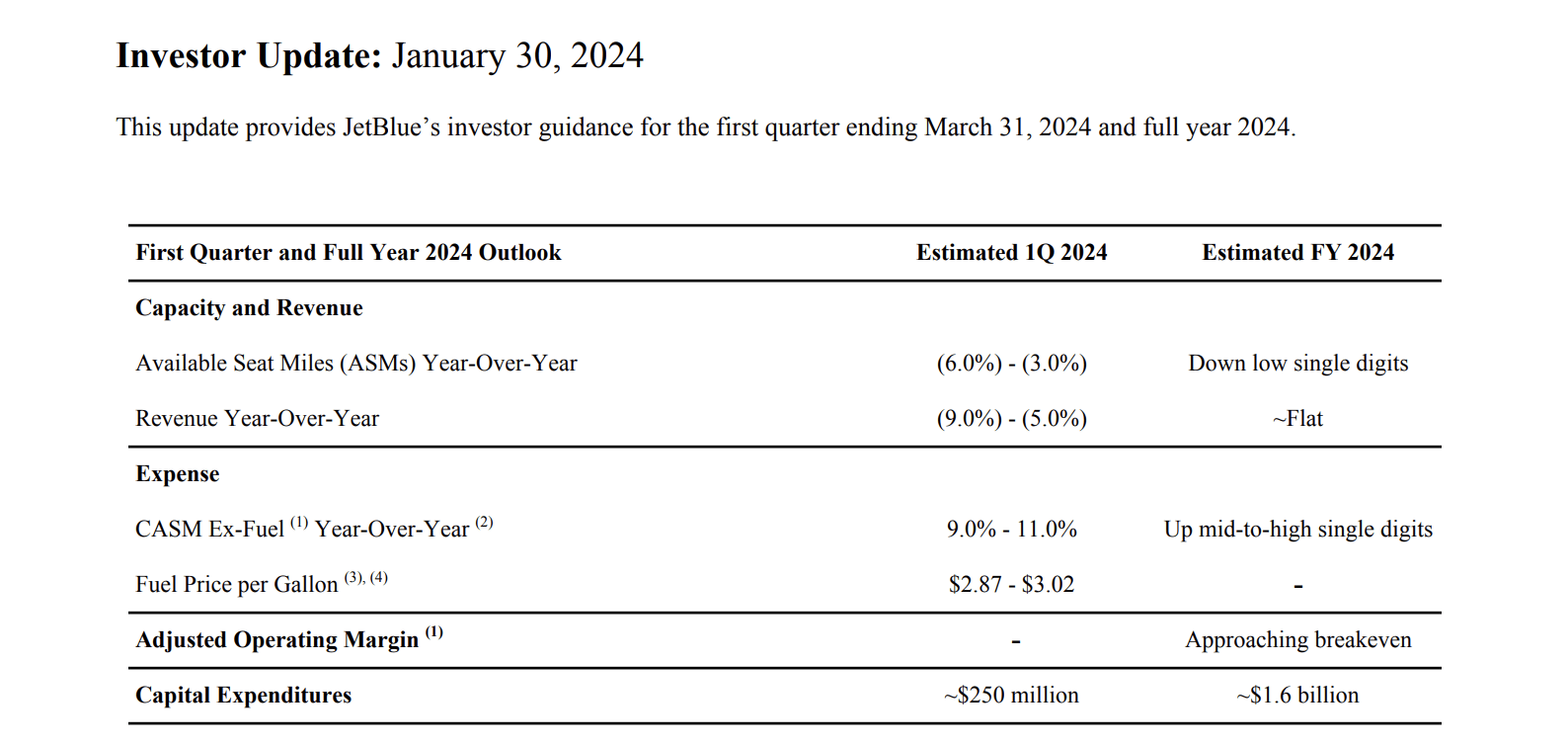

Source: JetBlue Q4'23 investor update

The airline is now guiding to ASMs down low single digits in 2024 with revenue nearly flat due to higher yields. At the same time, the cost trajectory has been adjusted to lower the cost increases this year with fuel prices a major unknown. JetBlue guided to fuel averaging $2.95 per gallon with prices currently at $2.62/gallon in North America.

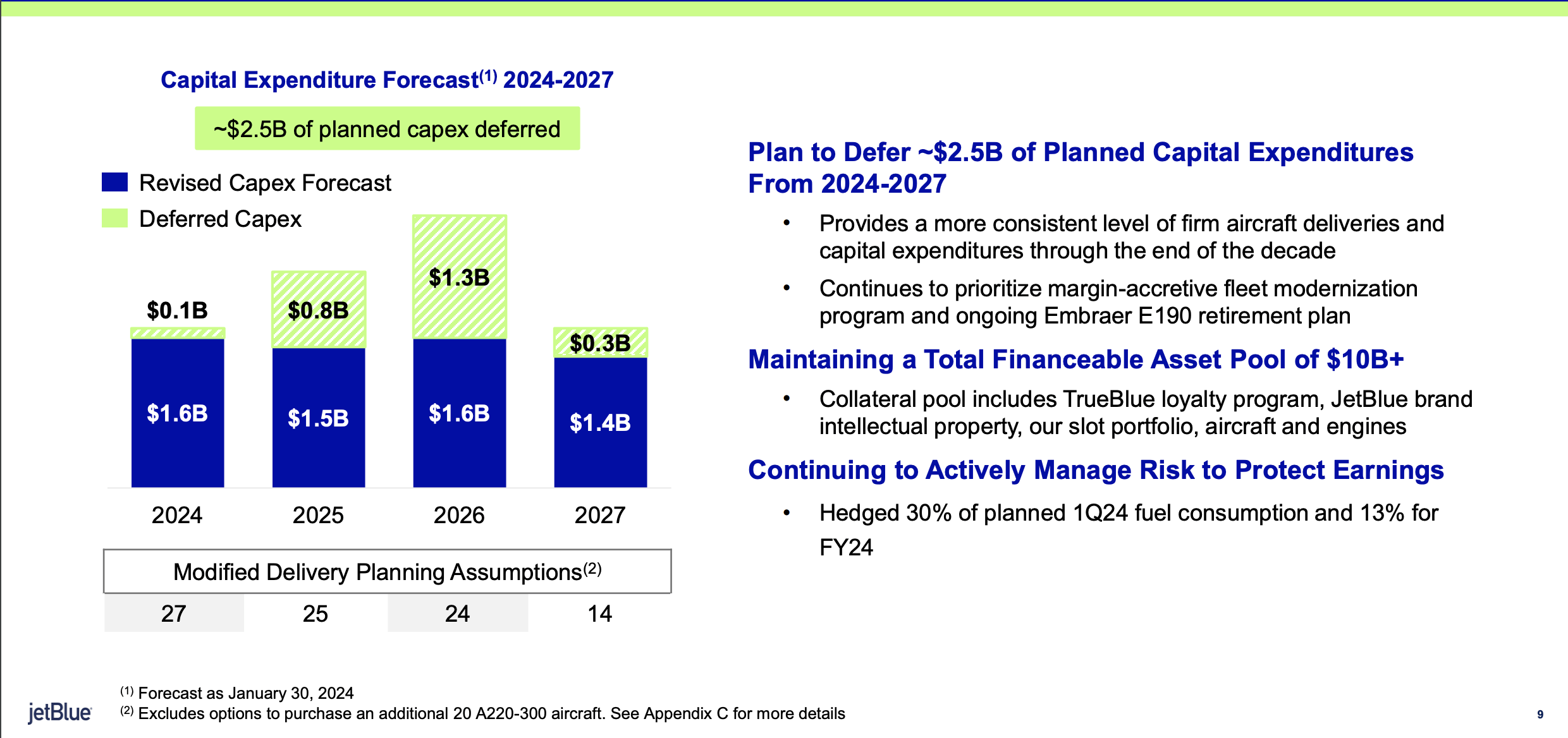

JetBlue is deferring ~$2.5 billion in capex until beyond 2028. The airline is now targeting annual spend in the $1.5 to $1.6 billion range through 2027 in a surprise move considering the court case focused highly on the airline needing the Spirit merger in order to acquire more aircraft.

Source: JetBlue Q3'24 presentation

With depreciation costs only topping $600 million annually, JetBlue is still spending more on aircraft than the hit to profits. The airline already has net debt of $3.6 billion leading to the concerns regarding the additional debt from Spirit Airlines combined with the large order book leading to the capex spend.

The investment picture is a lot more clear without the additional debt coming onto the books. Analysts still forecast JetBlue to lose money in 2024, though the airline forecasts a breakeven operating margin and limited net interest expenses should reduce any loss far below the projections for a $0.70 loss.

Carl Icahn bought 9.91% of the outstanding shares of JetBlue Airways. He now controls 33.6 million shares and bought the shares when the stock was in the $5s in another sign the investment picture is more solid with the stock still in the $6s.

The odd part about the whole merger block by the DoJ was that Spirit Airlines was seen at bankruptcy risk while JetBlue wasn't identified as having the same risk. Both airlines were unprofitable with net debt levels, but only Spirit Airlines collapsed due to bankruptcy fears.

Certain aspects of the merger case weren't supportive of the airlines reporting large profits as confirmed by Judge Young when discussing the risk of Spirit Airlines going bankrupt would make a DoJ win a moot point. Both airlines have spent time since the merger close adjusting operations to improve cash flows and the profit outlook.

In the Q4'23 earnings release, Ted Christie, Spirit's President and Chief Executive Officer, seemed to confirm the airline needed only minor adjustments to the business model to greatly improve financials going forward:

As we enter 2024, we are beginning to see benefits from the tactical and strategic changes we implemented in 2023. In addition, current booking trends further our confidence that the domestic environment is beginning to rebound. Together with the changes we have made, we estimate this will result in an unprecedented sequential improvement in total revenue per available seat mile (TRASM) from fourth quarter 2023 to first quarter 2024, which supports our view of a domestic recovery in 2024.

The CFO went on to discuss a path to being cash flow positive already as follows:

Regarding liquidity, we believe our $1.3 billion in total liquidity at year end 2023 should be more than adequate to get us to our primary goal of getting the business to generate cash. This is a milestone we think we will cross as we enter March. We believe we will be operating cash flow positive in the second quarter 2024 and beyond.

One reason for Spirit Airlines to agree to this mutual termination is the airline hitting this positive cash flow target in March as outlined during Q4 earnings on Feb. 8. Management might see the benefit of just moving on and taking the $69 million termination fee while an airline still struggling financially would likely cling onto the merger, though this is just pure speculation.

Of course, an airline can capture advanced ticket sales cash and cut capex below depreciation costs to boost cash flows while still reporting operating losses. Spirit Airlines isn't predicting any massive growth in revenues, so advanced ticket sales aren't likely a great source of cash going forward.

The company forecast 2024 capex of $235 million and depreciation and amortization costs in 2023 were $321 million. At an equal capex level in 2024, Spirit Airlines would save ~$86 million in cash from the lower capex than reported expenses.

The airline actually reported a solid profit in Q2'23 and Spirit Airlines generated a $4 to $5 EPS pre-COVID. The investor community probably shouldn't fret so much on whether this management team can get the domestic airline back to producing profits in a more normalized market in 2024.

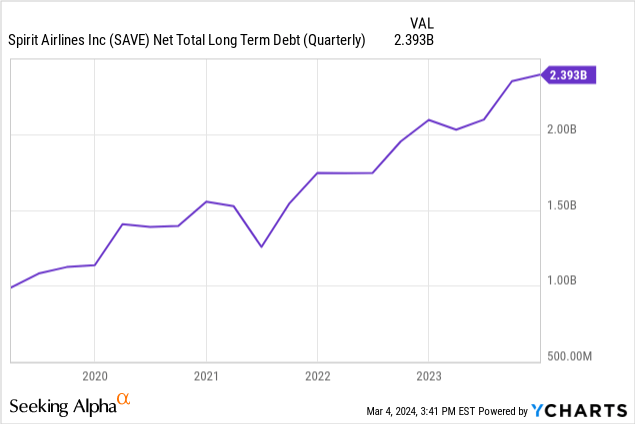

The airline has higher net debt now, but Spirit Airlines doesn't face anything daunting considering the revenue base has soared far beyond 2020 levels. The forecast for limited capacity growth in 2024, due partly to the engine issue, should contribute to the airline fixing the operational issues with lower yields leading to the suddenly drastic losses last year.

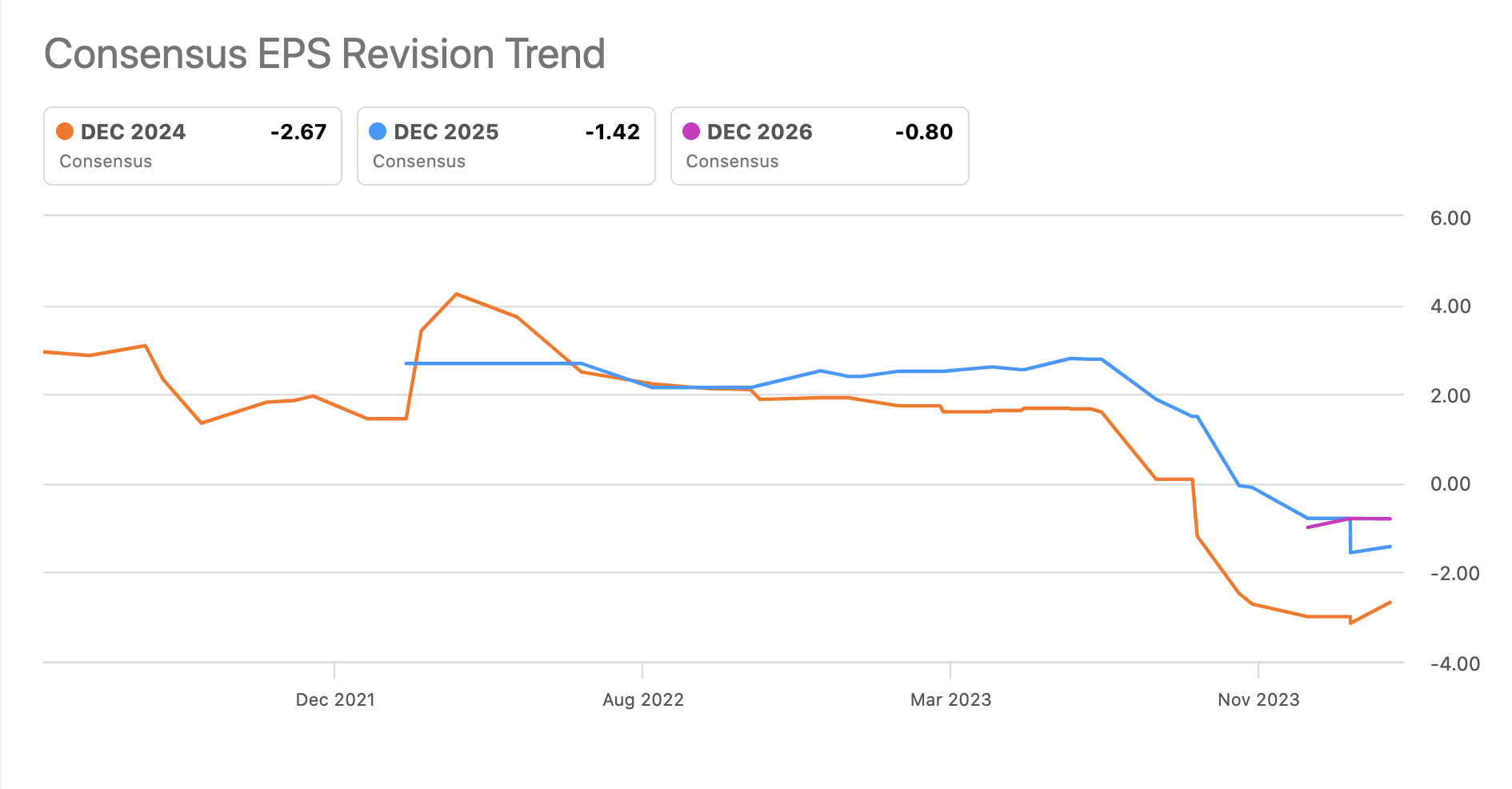

Just going back to mid 2023, the consensus estimate was for Spirit Airlines to produce a $2+ EPS for 2024 and into 2025. Now, the consensus estimates still forecast the airline loses $1.42 per share in 2025 despite bold predictions for the business turning cash flow positive in March, not years from now.

Source: Seeking Alpha

The market is likely smart to be skeptical considering Spirit Airlines just reported a quarter where the operating margin was (12.4)%. The airline did exceed the original estimate for a margin of (17.0)% in a partial indication of how quickly the metrics can turn.

Spirit Airlines was very profitable heading into COVID and turned profitable following COVID suggesting management knows how to operate in the competitive domestic travel market. The big unknown is how far the airline can return the business to generating profits after becoming cash flow positive. The stock appears exceptionally cheap trading below $6 considering the business prospects over the long term haven't likely changed.

The key investor takeaway is that JetBlue is probably the more conservative play while Spirit Airlines has more risk. Both airlines struggled over the course of the last year with the pressure on domestic airfares. As the sector adjusts led by changes at both JetBlue and Spirit Airlines, the operations should improve leading to a rally in the stocks, which both traded in the $15 to $20 range pre-COVID with further upside potential. Naturally, both stocks face very unfavorable outcomes, if the airlines aren't able to return to positive cash flows and profits.