Matt Porteous

Matt Porteous

In this article on Sandstorm Gold (NYSE:SAND), I will:

1) Provide an in-depth analysis of the company's assets, financial position, and outlook, focusing on strengths and identifying weaknesses.

2) Show how SAND is substantially undervalued on both a relative and absolute basis.

Investors can then decide if they agree or disagree with the bullish thesis.

I will not waste any more "ink" on an intro, so without further ado, let's dive in.

Sandstorm is a precious metals streaming and royalty company that got its start back in the late 2000s.

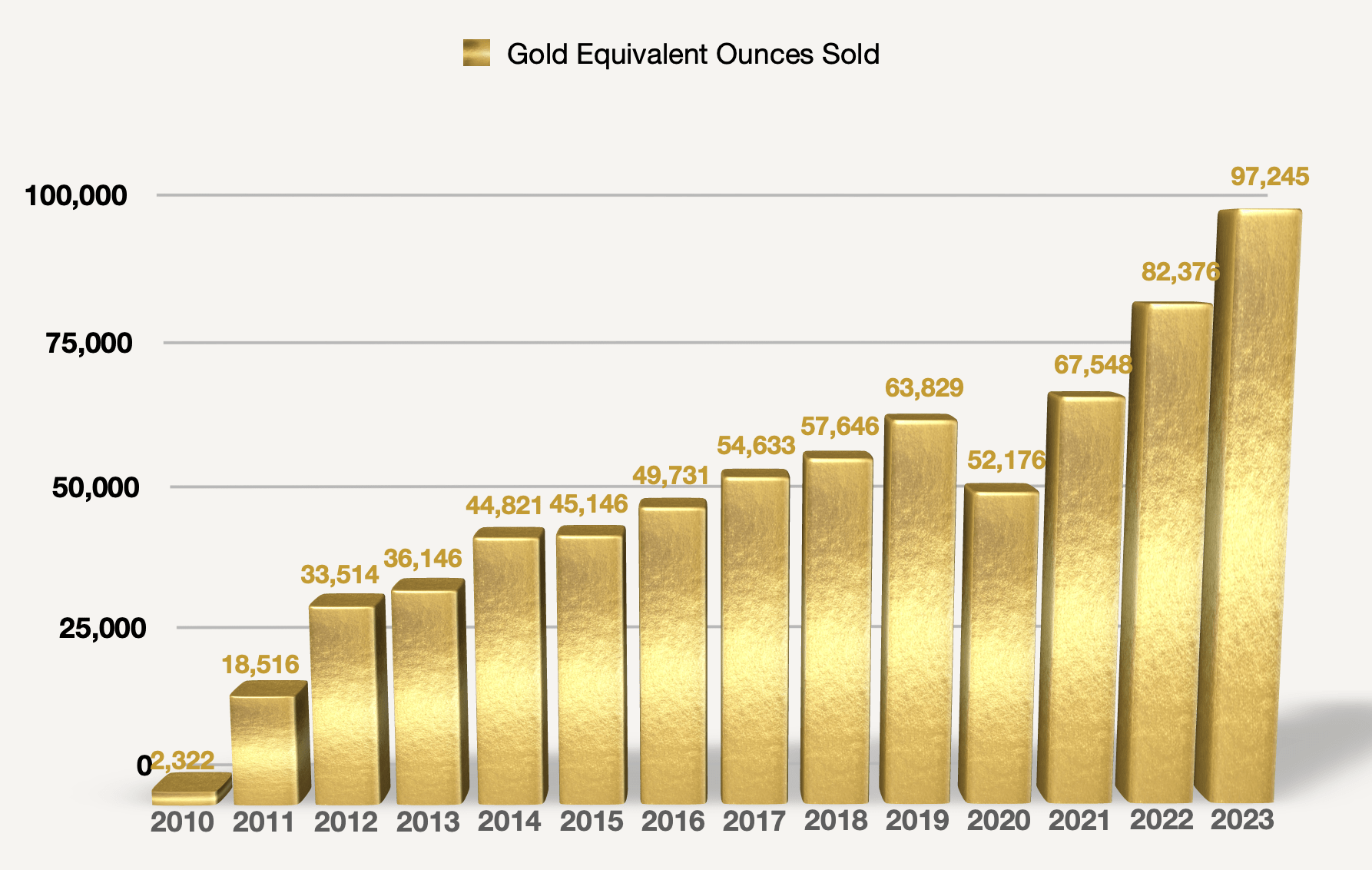

2010 was the first year the company realized gold equivalent ounces (GEOs) sold, with three streaming assets producing 2,322 GEOs for the company at the time and five streams/royalties in total. SAND today looks nothing like it did ~15 years ago, as the company now owns ~250 streams and royalties at various stages — including over 40 producing assets — and had another record year in 2023 with 97,245 GEOs sold. Sandstorm has a long track record of continually growing its portfolio and production. 2020 was the only year where SAND didn't see a YoY increase in GEOs sold, as COVID-19 disrupted many mines in the sector.

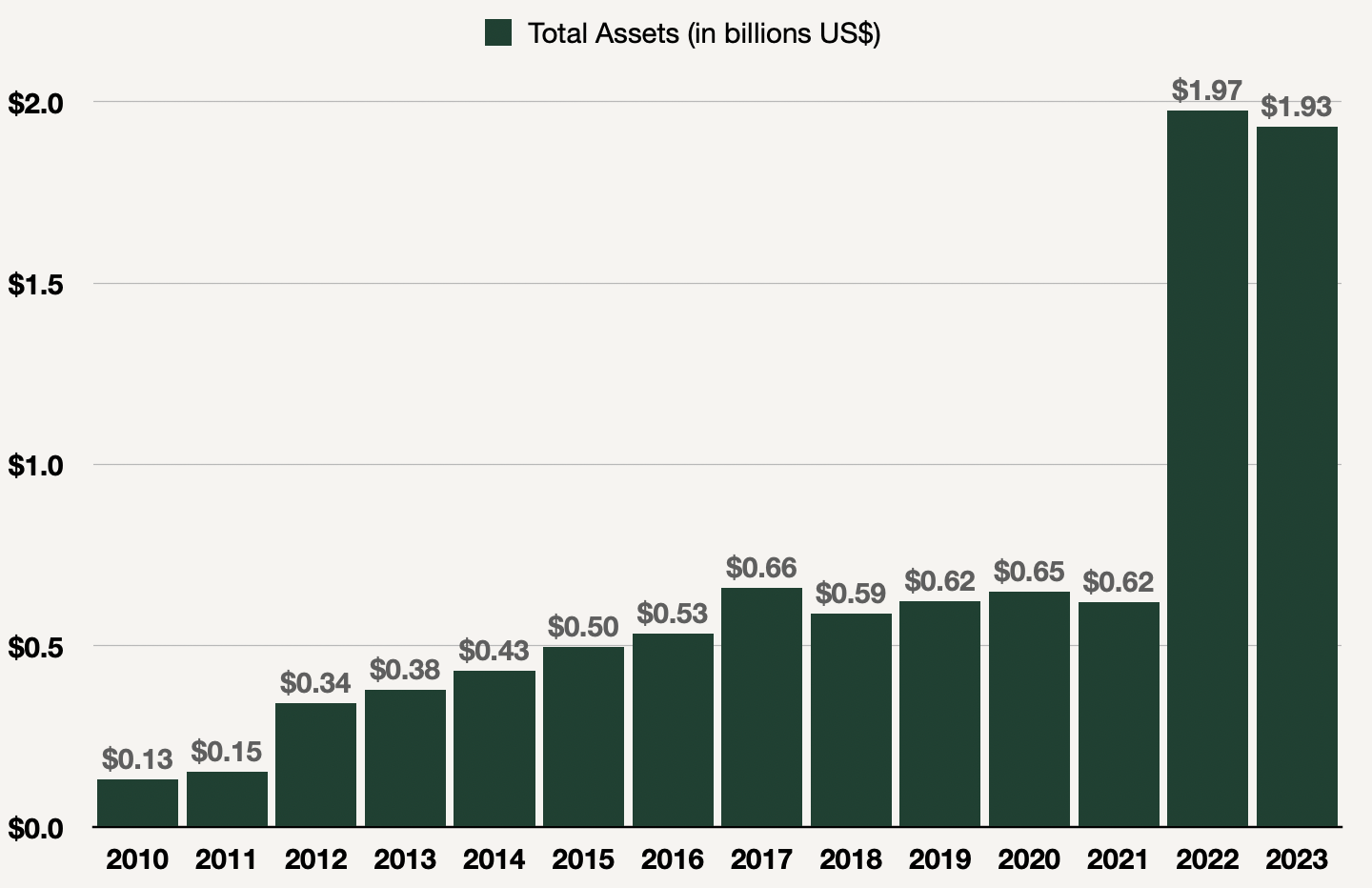

2022 was the most transformational year for the company, as it acquired $1.1 billion of assets via the Nomad Royalty and BaseCore Metals acquisitions. The chart below perfectly visualizes how impactful these two transactions were for Sandstorm, with its total assets increasing by over 200% to almost $2 billion after it closed the deals.

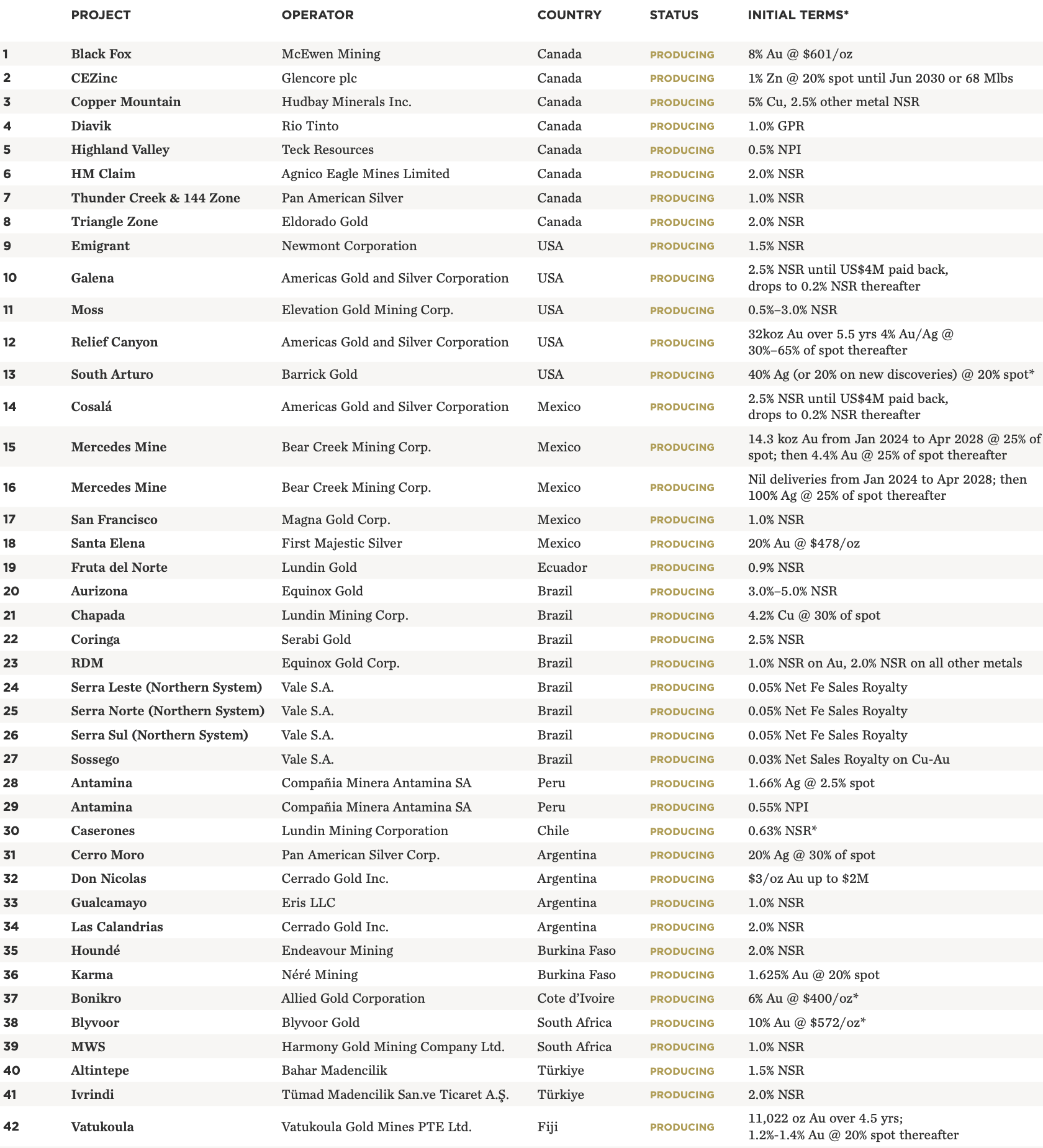

Below is a list of Sandstorm's producing streams and royalties, which I believe also provides a good visual for the number of cash-generating assets and the diversification of the company's portfolio. It drives the point home without needing to review every single one. However, later in this article, I will provide a deeper analysis of the key assets, as I believe it's important to show that this story is much more than just Hod Maden. I will also identify any critical risk there is for any asset.

In addition to the above producing streams and royalties, SAND has over 200 other royalties at various stages, including 30 assets that are in development, most of which are gold-producing.

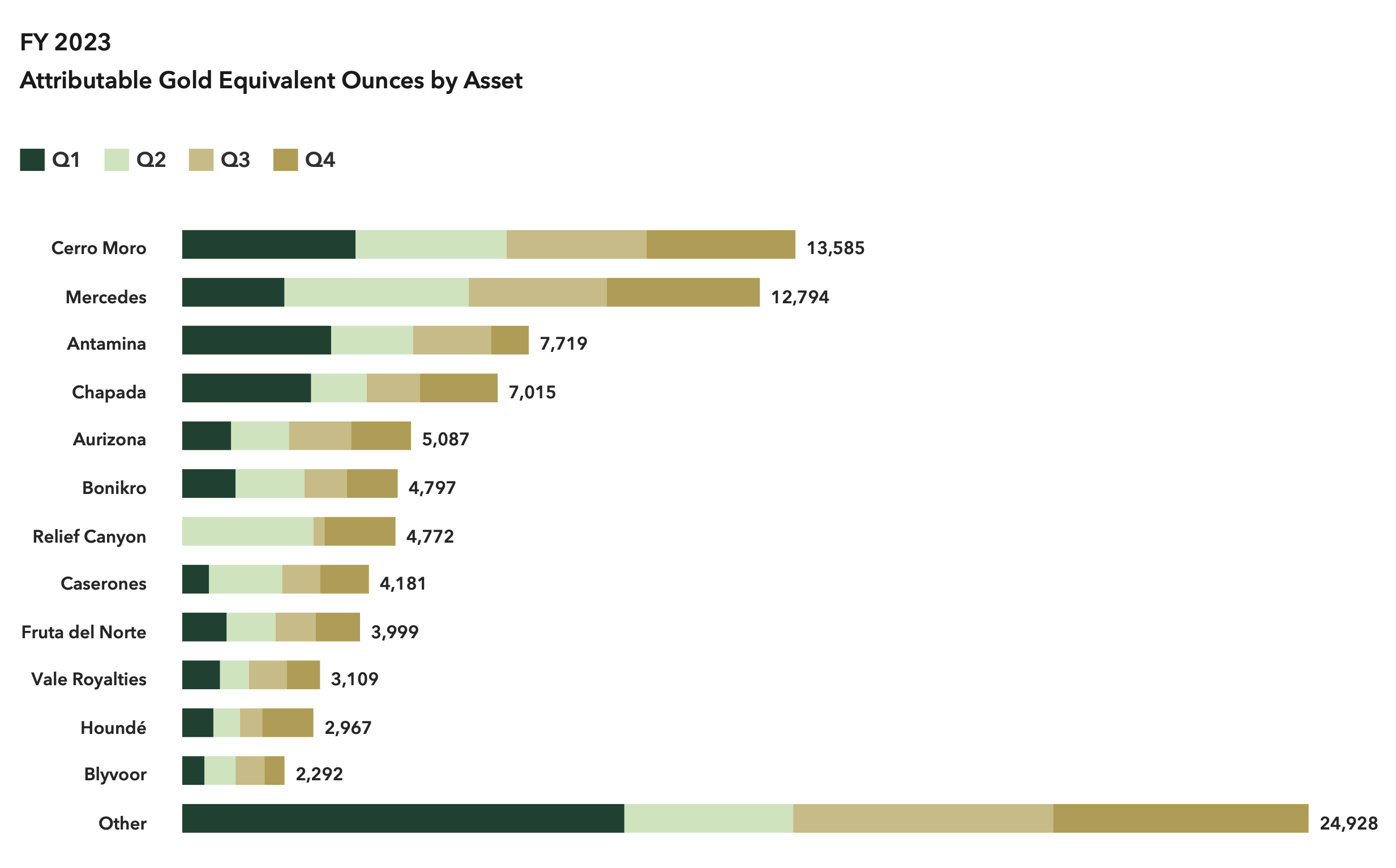

In 2023, the largest contributors to GEOs sold were the Cerro Moro silver stream and the Mercedes gold and silver streams. However, these won't be the two top GEO assets in 2024, and they aren't even the most valuable streams in the portfolio. The Mercedes streams were restructured at the beginning of this year, and there will be a notable drop-off in contribution from Mercedes in 2024. Cerro Moro has limited reserves remaining, and the stream is quickly approaching a step-down next year, as SAND currently receives 20% of all silver production from Cerro Moro up to a maximum of 1.2 million ounces of silver annually until 7.0 Mozs are delivered. After that threshold is hit — which will likely occur in 2025 — SAND will receive 9% of the silver produced for the life of the mine. Cerro Moro could still vie for the top spot this year, but Mercedes won't be there with it, and next year, Cerro Moro will drop down.

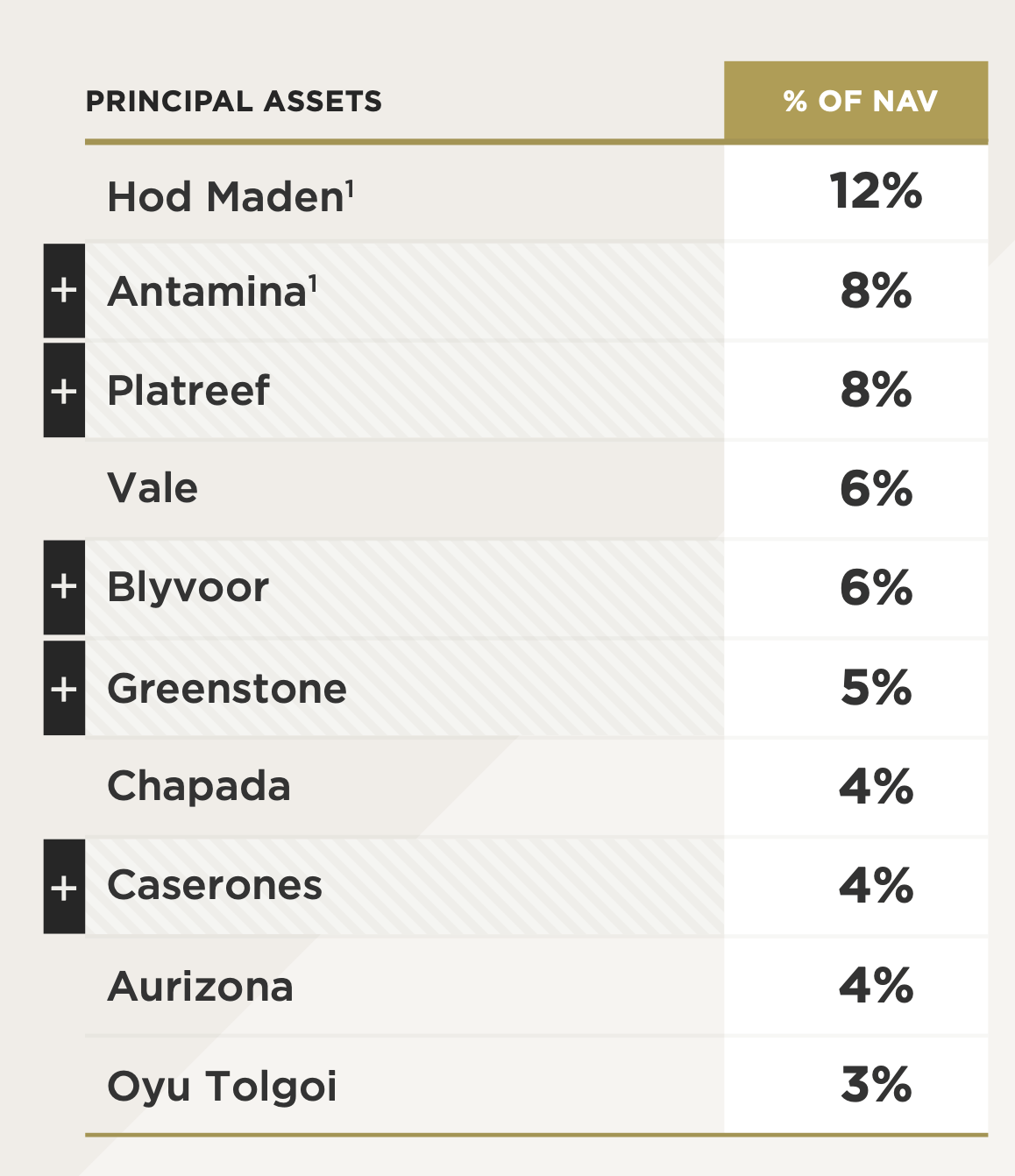

The most valuable assets in Sandstorm's portfolio are listed below, and several aren't even in production yet, including Hod Maden, Platreef, and Greenstone. The "plus" sign next to a name signifies it's a recent acquisition and reflects the upgrades to the portfolio as a result of the Nomad and BaseCore transactions. Also, notice the diversification and how one asset doesn't account for a substantial portion of the company's Net Asset Value. SAND is the most diversified out of all of its mid and large-cap peers, with just over 40% of its NAV coming from its top 5 assets vs. 60-65% for Franco-Nevada (FNV), Osisko Gold Royalties (OR), Royal Gold (RGLD), and Wheaton Precious Metals (WPM). In fact, Sandstorm's next five assets only account for an additional 20% of the company's value, which means its top 10 assets are ~60-65% of its NAV, or equal to the aforementioned companies' exposure to their top 5 streams/royalties. Having risks spread out among dozens of assets instead of just a handful is one aspect that makes SAND appealing.

Let's now review the key producing, development, and exploration assets in Sandstorm's comprehensive portfolio. I want to leave Hod Maden for last, as there is more to discuss with this asset. I also want to note that the royalty ounces discussed below are based on reserves and resources from mid-2023 or prior, and don't reflect end-of-2023 estimates. Most are based on 2022 reserves/resources.

Gold price assumption = $2,000

Terms:

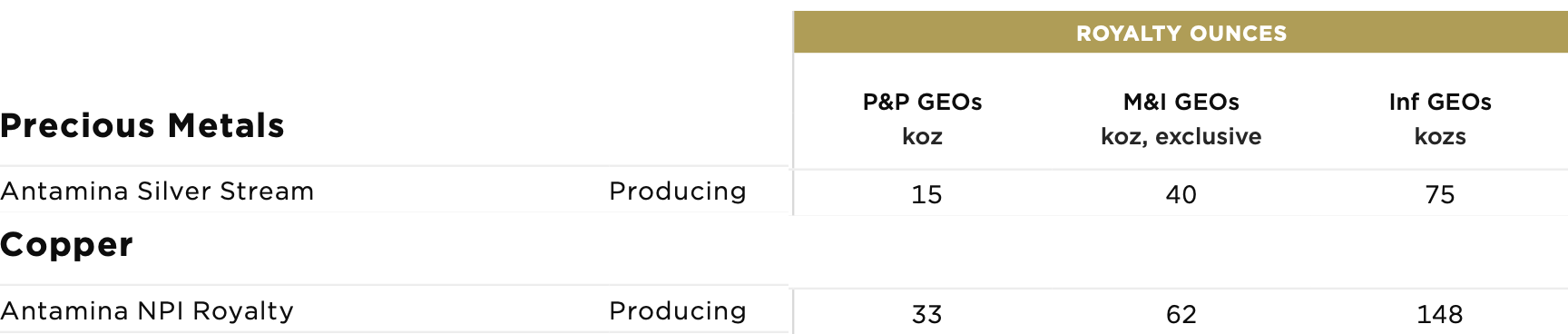

Antamina is an open-pit copper mine in the Andes and was the third-largest copper mine in the world on a copper equivalent basis in 2022. Antamina also produces a substantial amount of zinc and silver and is one of the top five largest silver mines, even though Ag is not the primary metal.

The operation has been in production since 2001 and has enough resources to extend the mine life by another ~30 years. The mine is operated through a joint venture between Glencore (33.75%), BHP Billiton (33.75%), Teck Resources (22.5%), and Mitsubishi Corporation (10%).

Two weeks ago, Peru granted Antamina a long-awaited permit that allows for a US$2 billion expansion project to proceed that will extend the mine life from 2028 to 2036. The modified EIA includes the approval to widen and deepen the pit and increase the throughput by ~20%. Other aspects of the project include, replacing the primary ore crusher with a new rock crusher and increasing the tailing dam storage capacity.

Sandstorm's 1.66% Ag stream and 0.55% NPI on Antamina give the company and its shareholders appreciable and long-life exposure to one of the largest mining operations on the planet.

The combined silver stream and copper royalty equate to SAND receiving 48,000 Gold Equivalent Ounces of Antamina's mineral reserves, or ~$100 million of revenue at the current gold price, and that's at an almost 100% margin. Including all of the M&I Resources (exclusive of reserves) is an additional 102,000 GEOs or over $200 million of revenue. All the Inferred Resources amount to 223,000 GEOs or almost $450 million of revenue.

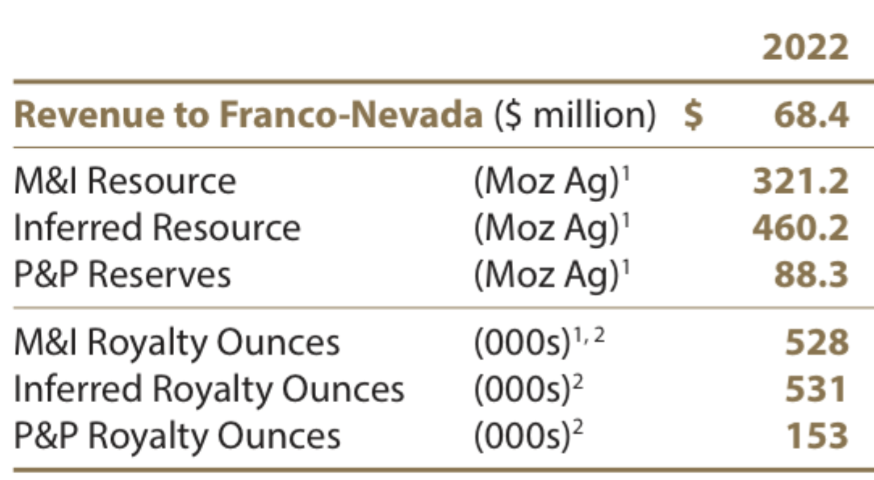

These figures are supported by Franco-Nevada's figures, as FNV owns a 22.5% Ag stream on Antamina. FNV realized $68.4 million of revenue from its stream on Antamina in 2022 and estimates its portion of silver reserves amount to 153,000 GEOs. Please note, there is an eventual 33% step-down in FNV's silver stream, and the company also includes its per-ounce payments in its stream interest.

Franco Nevada

Depending on grade variation for any given year, I would estimate Sandstorm will receive between 2,000 to 3,500 gold equivalent ounces from its Antamina silver stream, and that doesn't include the additional GEOs from the 0.55% NPI.

Sandstorm is also receiving additional annual cash flow from Horizon Copper's (OTCPK:RYTTF) NPI on Antamina. Sandstorm sold a portion of its original 1.66% NPI on Antamina to Horizon Copper, converting it into a silver stream and lower NPI. SAND also received a debenture with a face value of US$149.1 million as of June 2023, and according to the terms: "The principal repayments are subject to a cash sweep of the excess cash flow Horizon Copper receives from the 1.66% Antamina NPI after the Antamina silver stream and Antamina residual royalty obligations are paid." Effectively, SAND will receive 1) the 1.66% silver stream and 0.55% NPI, and 2) all of the excess cash that Horizon receives from the rest of the NPI as part of the repayment of the debenture (until it's repaid in full). Plus, SAND gets 3% interest on top of that. To put it another way, Sandstorm sold the 1.66% NPI on Antamina, but it will receive all of the cash flow from this NPI — plus interest — until the debt that Horizon owes is extinguished.

The NPI (or Net Profits Interest) royalties that Sandstorm and Horizon hold will realize less revenue over the next few years because of reduced profits during the expansion of the mine, but will ultimately generate much more cash flow as the expansion unlocks many more reserves.

NPV (5%) = US$200-$250 million (range is based on how much of the Inferred Resources are ultimately mined)

Terms:

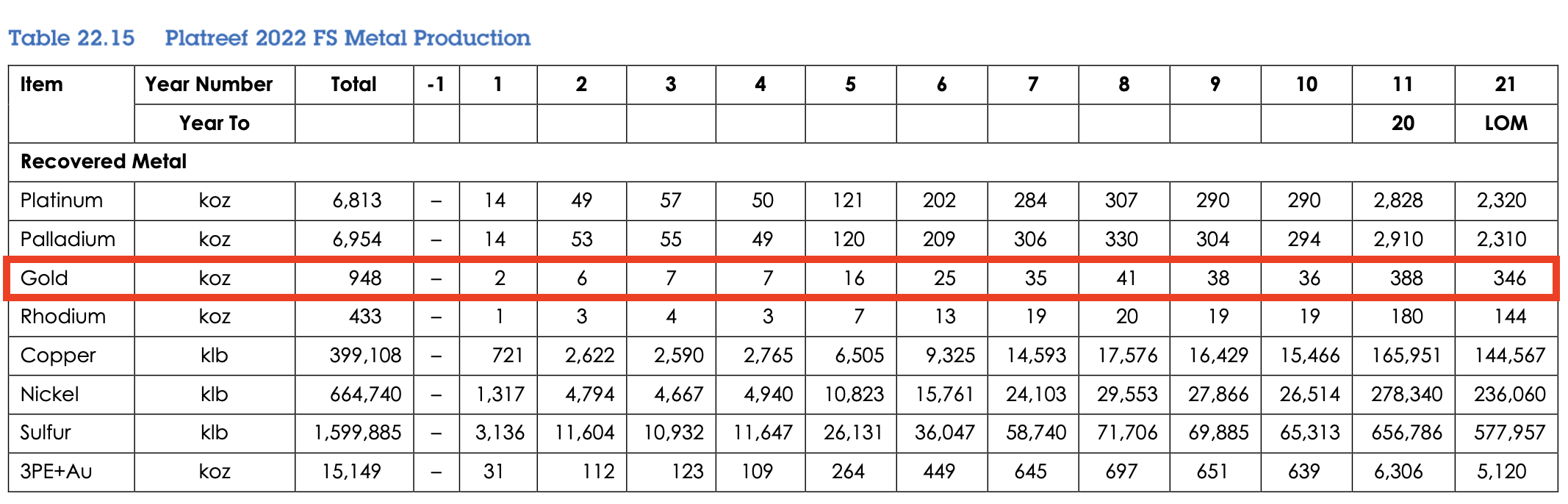

Platreef is a platinum group metals and nickel/gold/copper deposit that is majority owned by Ivanhoe Mines (OTCQX:IVPAF). Currently under development, with Phase 1 commissioning expected in the second half of this year, Platreef is one of the largest mines in the world under construction. The underground deposit is characterized by thick, high-grade mineralization, and it will be one of the largest and lowest-cost primary PGM mines in the industry.

Slated for the end of this decade, Phase 2 will result in a dramatic 5-fold increase in output, with over 500,000 ounces of 3PE+Au production annually. It is during this phase that gold production will average ~35,000 ounces per year.

Platreef is a near-term bullish catalyst for Sandstorm, as the mine will begin contributing to GEO production later this year. While the next 4-5 years will see minimal gold production, Sandstorm's 37.5% Au stream still equates to 2,000-2,500 GEOs per annum during Phase 1.

In Phase 2, Sandstorm will receive ~13,000 GEOs annually from the Platreef stream, which will make it one of the largest cash-flowing streams in the portfolio.

Sandstorm's royalty ounces from its portion of reserves amount to 252,000 GEOs, and the NPV (5%) of this stream just based on the next 20 years of mine life is ~US$250 million, which is ~20% of the company's current market cap.

Sandstorm Gold

There are a few notable risks for Platreef.

Ongoing power outages in South Africa due to inadequate maintenance of facilities and other factors are threatening platinum and palladium supplies in the country, as loadshedding is disrupting mining operations in SA.

Continued labor unrest and rail transportation disruptions are also plaguing the industry.

While Platreef should overcome the challenges and move on to Phase 2, there could still be disruptions from year to year, and the mine might underperform expectations. Even in that scenario, I would still expect at least 8,000-10,000 GEOs per annum on average during Phase 2.

Terms:

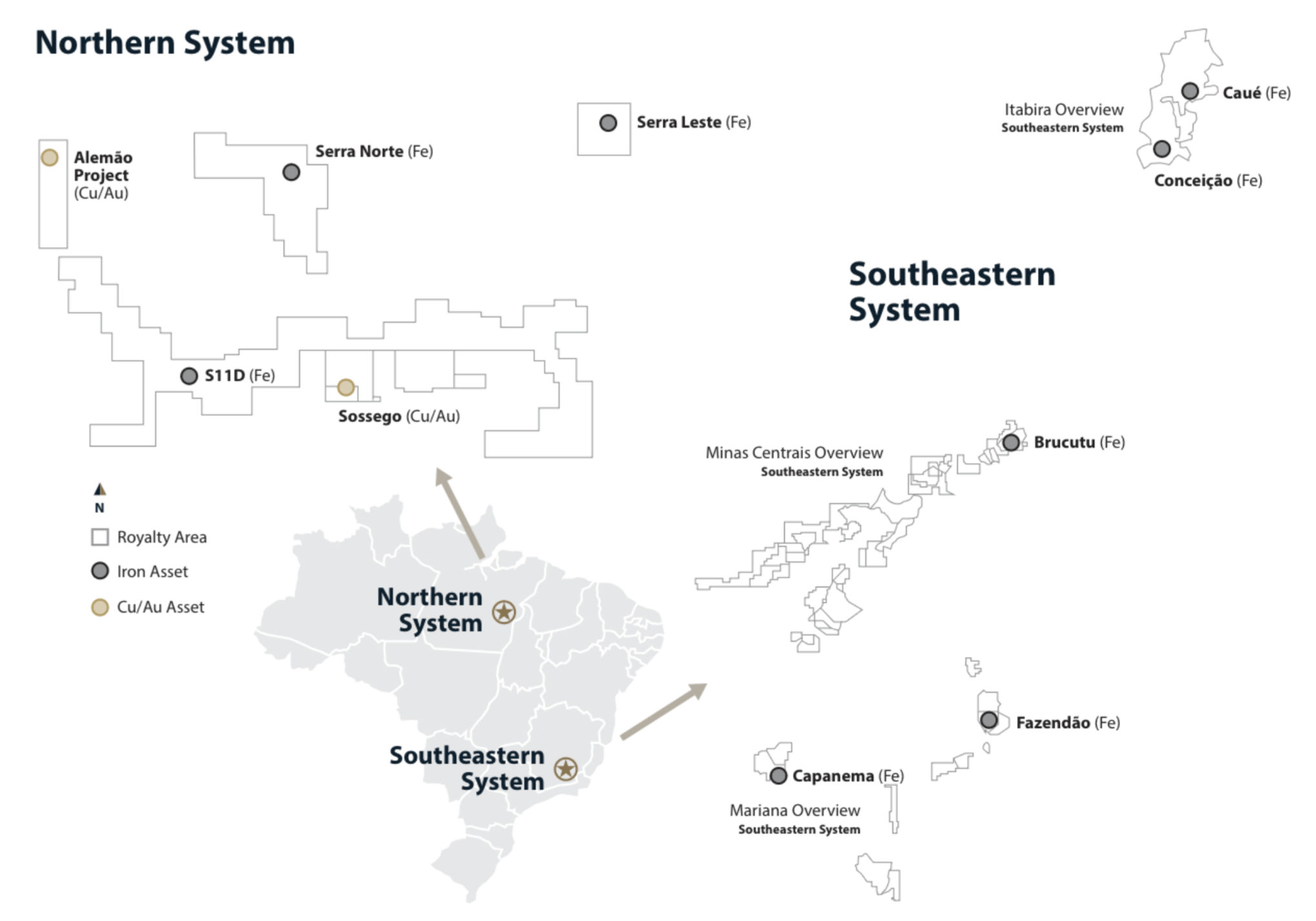

0.05% net sales royalty on iron ore sales from a portion of the Southeastern System

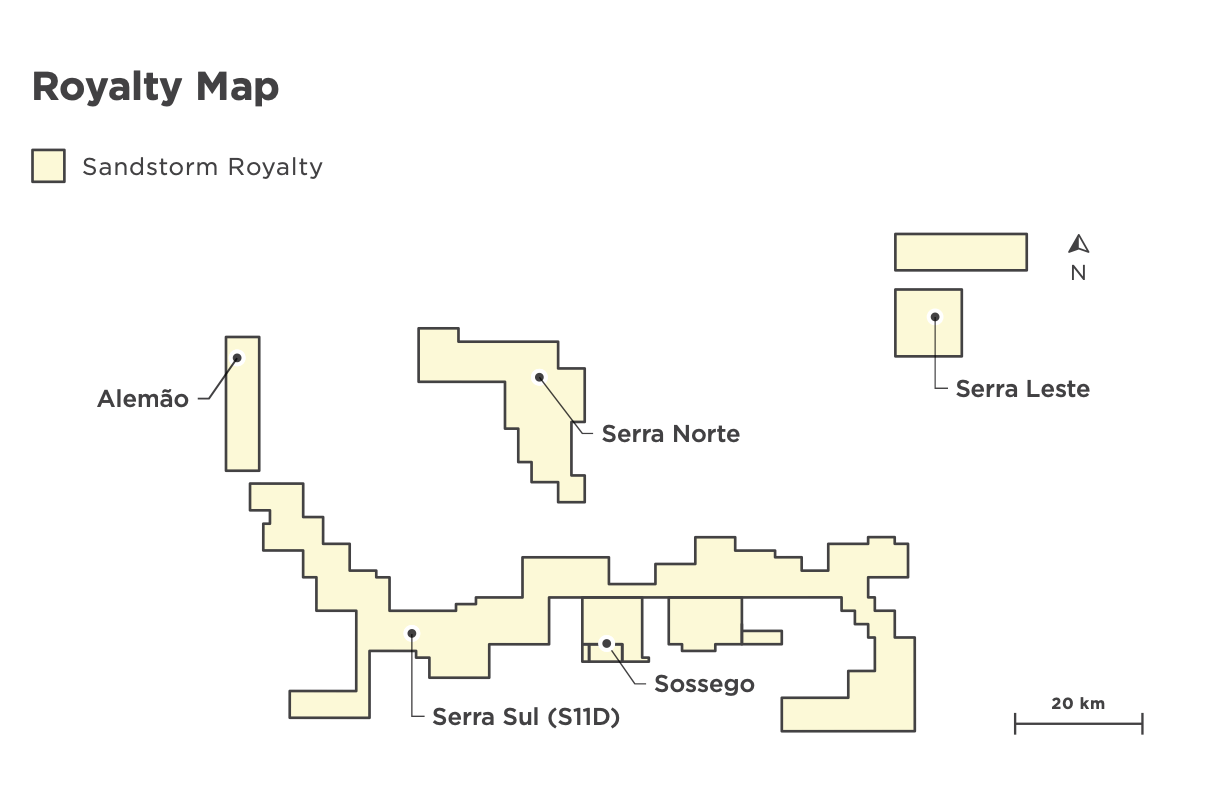

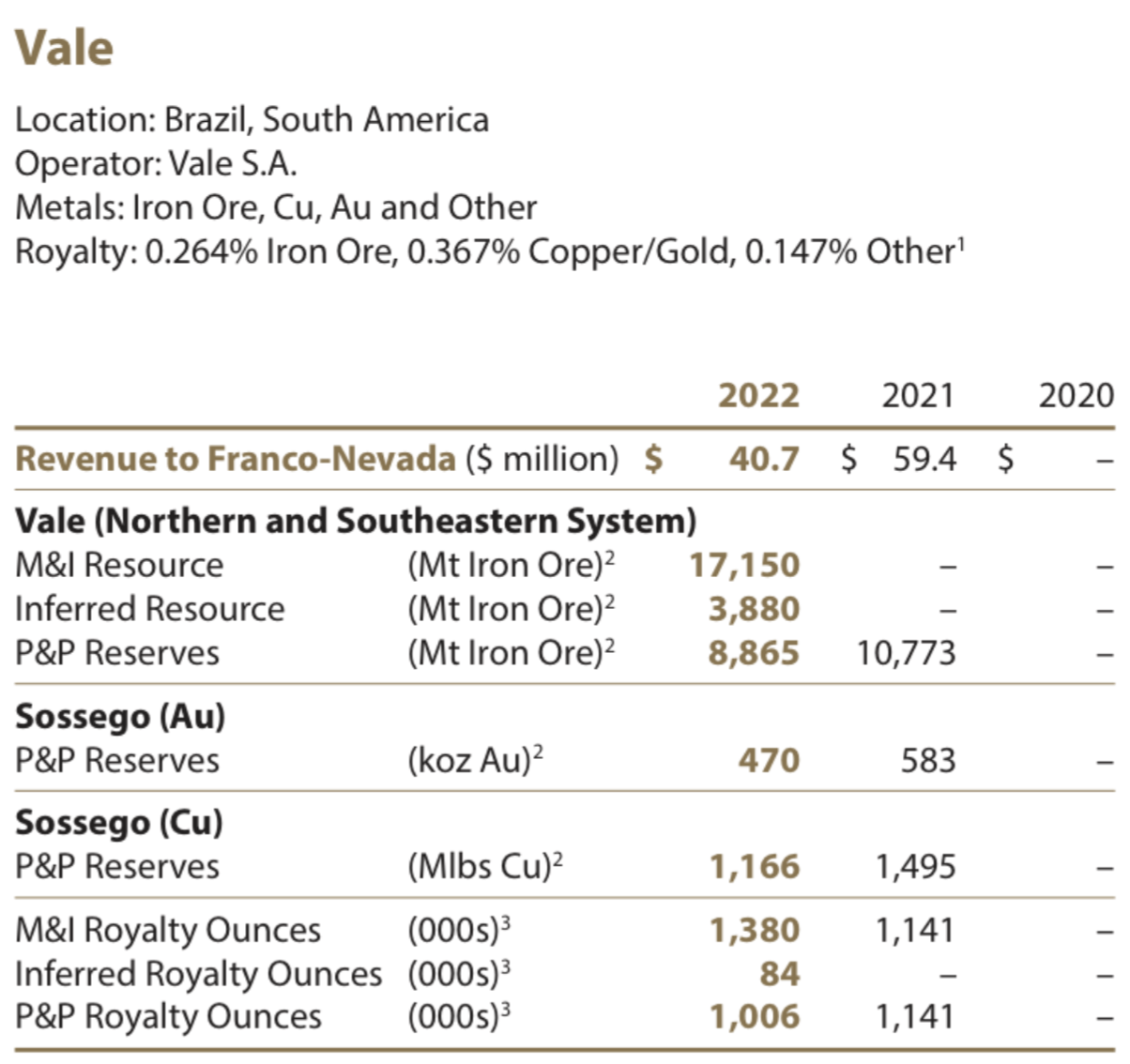

Vale (VALE) is the sixth largest mining company in the world (all metals) and produces ~15% of the global supply of iron ore, with cost in the first quartile of the cost curve. Sandstorm owns several net sales royalties on Vale's assets in Brazil.

The Northern System consists of the Serra Sul, Serra Norte, and Serra Leste iron ore mines. Serra Norte began production in 1984 and, based on reserves, has a mine life of ~15 years (late 2030s). Production at Serra Leste began in 2014 and will continue into 2049, while Serra Sul will produce into the late 2050s. Vale is looking to expand Serra Sul and has other growth projects planned that could increase Sandstorm's royalty production. SAND also holds a royalty on the Sossego copper-gold mine in the Northern System, and net sales royalties on other assets on the property.

In addition, Sandstorm holds royalties on a portion of the Southeastern System, which includes three mining complexes: Itabira, Minas Centrais, and Mariana, with the latter two expected to produce through the mid to late 2050s. This asset won't begin to contribute to Sandstorm's production until a certain sales threshold is met, which is expected to occur next year.

Franco Nevada also owns royalties on the same Vale assets, as in 2021, FNV gobbled up 14.7% of the total 1997-issued royalty debentures by Vale, paying $538 million for these royalties. Again, these are the same royalties that SAND owns, but just at a greater exposure (5-6x that of Sandstorm).

The Vale royalties currently contribute around 3,000-3,500 GEOs annually to Sandstorm. That figure will increase over the next few years and through later this decade once the Southern System royalties begin contributing and expansion projects are complete.

Sandstorm's royalty ounces from its portion of reserves amount to 170,000 GEOs. NPV (5%) = US$140 million

Again, using FNV as a reference, we can see over 1 million ounces of "Reserve Royalty Ounces" from its Vale royalties, or 5-6x Sandstorm's estimate. As a side note, Franco Nevada's M&I Royalty Ounces are inclusive of reserves, while Sandstorm's are exclusive. If you compare M&I Resources on an apples-to-apples basis, FNV has 374,000 M&I Royalty ounces or 5-6x what SAND lists above.

Terms:

The Blyvoor underground gold mine is located in one of the most prolific gold camps in South Africa. The mine first entered production in 1942 and, at one point in the 1950s, was the most profitable mine and largest gold producer in the world.

By the 2000s, its best days were behind it, and the asset was purchased out of bankruptcy in the mid-2010s.

Privately owned, fresh money was put into the asset, and in June 2021, an updated technical report was filed, which estimated 5.5 million ounces of high-grade gold reserves and 242,000 ounces of annual production over a 22-year mine life.

When Nomad owned the stream, the company estimated it would receive ~20,000 gold ounces per year.

I was skeptical of the assumptions put forth on the asset by Nomad, and so I wasn't surprised that when Sandstorm purchased the stream, it reset expectations to 60,000 to 80,000 ounces of gold production per annum, or 1/4 to 1/3 of the previous estimate. That would still equate to 6,000-8,000 GEOs per year for Sandstorm, a healthy stream.

However, the mine doesn't appear to be hitting even those much lower targets, as SAND only recognized a little over 2,000 GEOs from Blyvoor in 2023.

Bloomberg reported last December that Blyvoor was in talks to combine with a New York-based SPAC in a deal valued at $425 million, which would be a positive outcome and could help the mine if it's underfunded.

It's difficult to value Blyvoor and estimate potential annual GEOs to Sandstorm. Sandstorm's stream ounces from its portion of reserves amount to 295,000 GEOs, but at this stage, we can't assume anything close to that estimate. I would value Blyvoor at about 1/3 of the NAV Sandstorm estimates.

Terms:

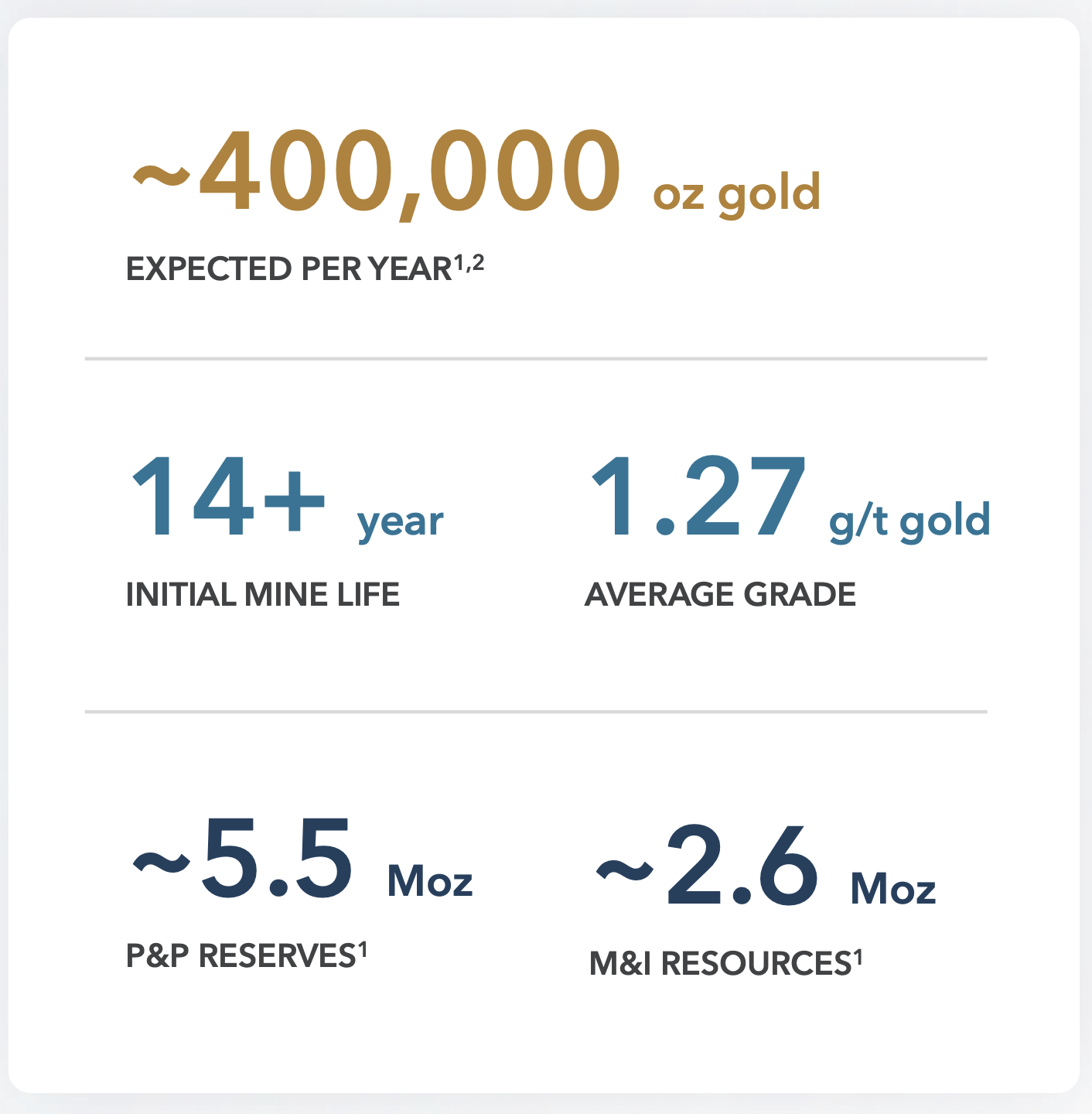

Scheduled for completion in the first half of this year, the Greenstone project — owned jointly by Equinox Gold (60%) and Orion Mine Finance (40%) — is a significant growth asset for Sandstorm.

~400,000 ounces of gold production are expected per year during the first five years of mine life, which equates to ~10,000 GEOs to Sandstorm per year, and Greenstone has a 14+ year mine life in total. It's an asset that could generate substantial free cash flow for Sandstorm.

However, I do have a concern about Greenstone.

Premier Gold and Centerra Gold (CGAU) were 50/50 partners on the project. But in 2019, Premier released an updated resource and technical study on Greenstone, which saw the grade of the open pit resource jump considerably and made the project far more economical. Centerra's team, though, had significant concerns about the use of certain technical parameters and cost assumptions in the resource estimate.

Centerra sold its stake in Greenstone to Orion in 2020, and then Premier was bought by Equinox Gold (EQX) in 2021.

It's unclear whether Centerra's concerns were valid, or if those concerns have been addressed since then. But having two partners disagree like this on a technical report is unusual. For me, it means there is a cloud of uncertainty hovering over Greenstone until we see at least 3 to 4 quarters of production figures.

Sandstorm's stream ounces from its portion of reserves amount to 120,000 GEOs. NPV (5%) = ~US$140 million (based only on reserves)

Terms:

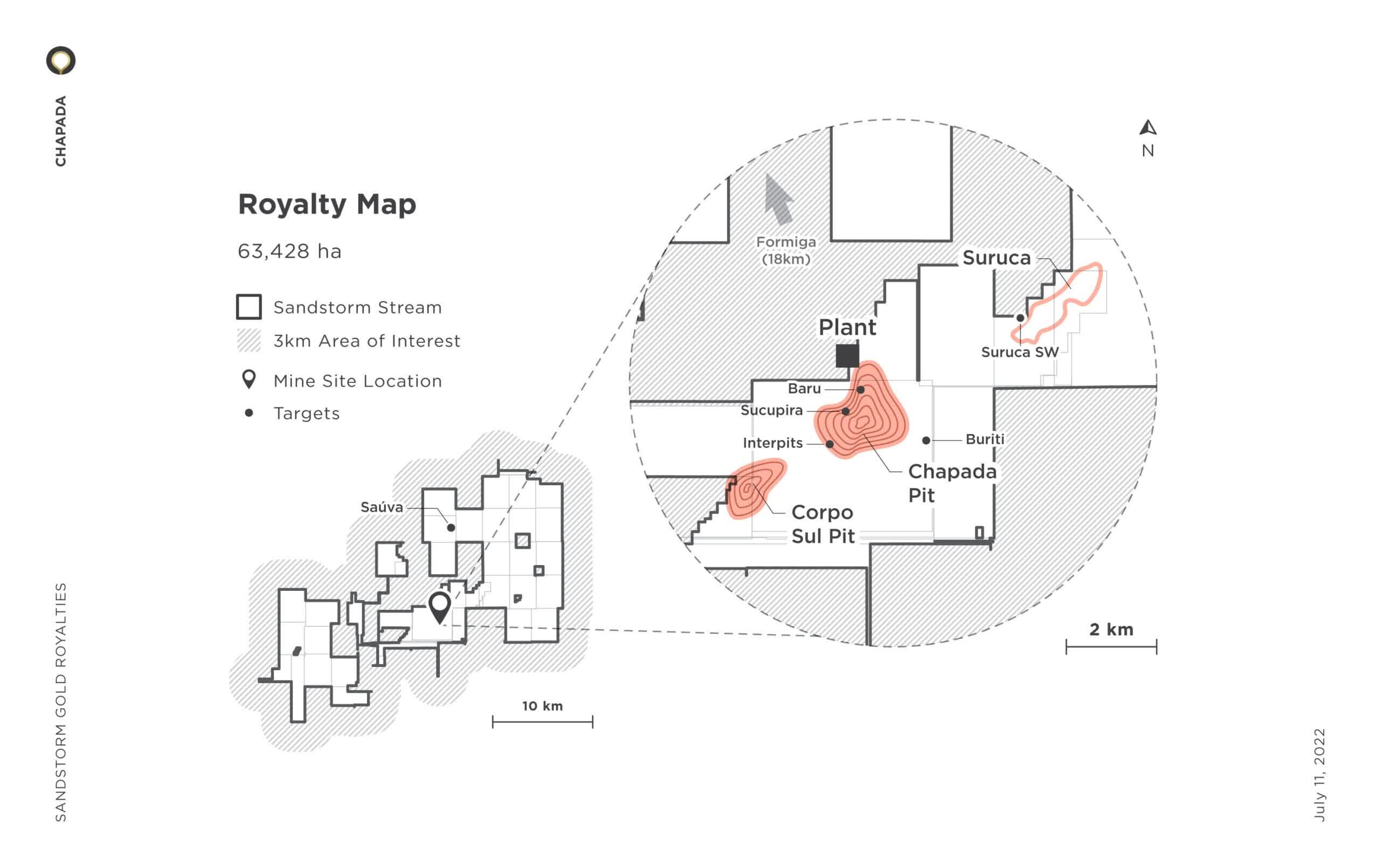

Chapada is a top 5 asset for Sandstorm. An open-pit copper-gold mine that began production in 2007, Chapada — which is owned by Lundin Mining (OTCPK:LUNMF) — has over 3 billion pounds of copper reserves and a ~30-year mine life. Current production is from the Chapada and Corpo Sul pits, but the discovery at the higher-grade Saúva target ~10-15 Km north has resulted in another long-life source of open-pit production.

Sandstorm Gold

Drill results from Saúva released in early 2022 showed extremely wide intercepts at grades that are multiples of the current reserve grade at Chapada, and mineralization started just below the surface. Highlights included:

Saúva, which is located within the Sandstorm's stream boundary, now contains over 1.5 billion pounds of copper resources, and Lundin is looking to potentially incorporate Saúva into the current mine plan at Chapada.

SAND also owns a 2% NSR royalty on the Suruca deposit, but that's still a development project, and given that it's low-grade gold, Saúva and other targets are higher priority.

Chapada has produced a consistent 7,000-9,000 GEOs for Sandstorm since it acquired the stream (not including 2020 when Covid shut down mines across the world).

There will be a 28% step-down in a few years to 3.0%, but the original terms of the stream didn't mention a maximum annual delivery during this phase of the stream, and throughput expansion or increased production because of higher grade Saúva ore could mean the stream continues to produce at around current levels.

Eventually, in ~5 years or so, it will drop to a 1.5% stream, or ~3,000 GEOs per year for SAND.

Barring an unforeseen event, Chapada should remain a dependable, high-cash-flow-generating asset for decades to come.

While most of the other streams and royalties discussed earlier contain more royalty ounces in the reserve category than Chapada, when you include the M&I royalty ounces, Chapada is near the top. NPV (5%) = ~US$80 million (reserves only)

Terms:

In 2023, Lundin Mining paid almost US$1 billion for 51% of the Caserones open pit copper mine in Chile, with JX Nippon Mining & Metals retaining the remaining 49%.

Caserones is a large mine with a low strip ratio and has been in production since 2014, historically producing between ~220 to 270 million pounds of copper annually. $4.2 billion of capital has been spent on infrastructure at Caserones over its mine life, and it's expected to produce substantial volumes of copper (and molybdenum) for likely decades to come.

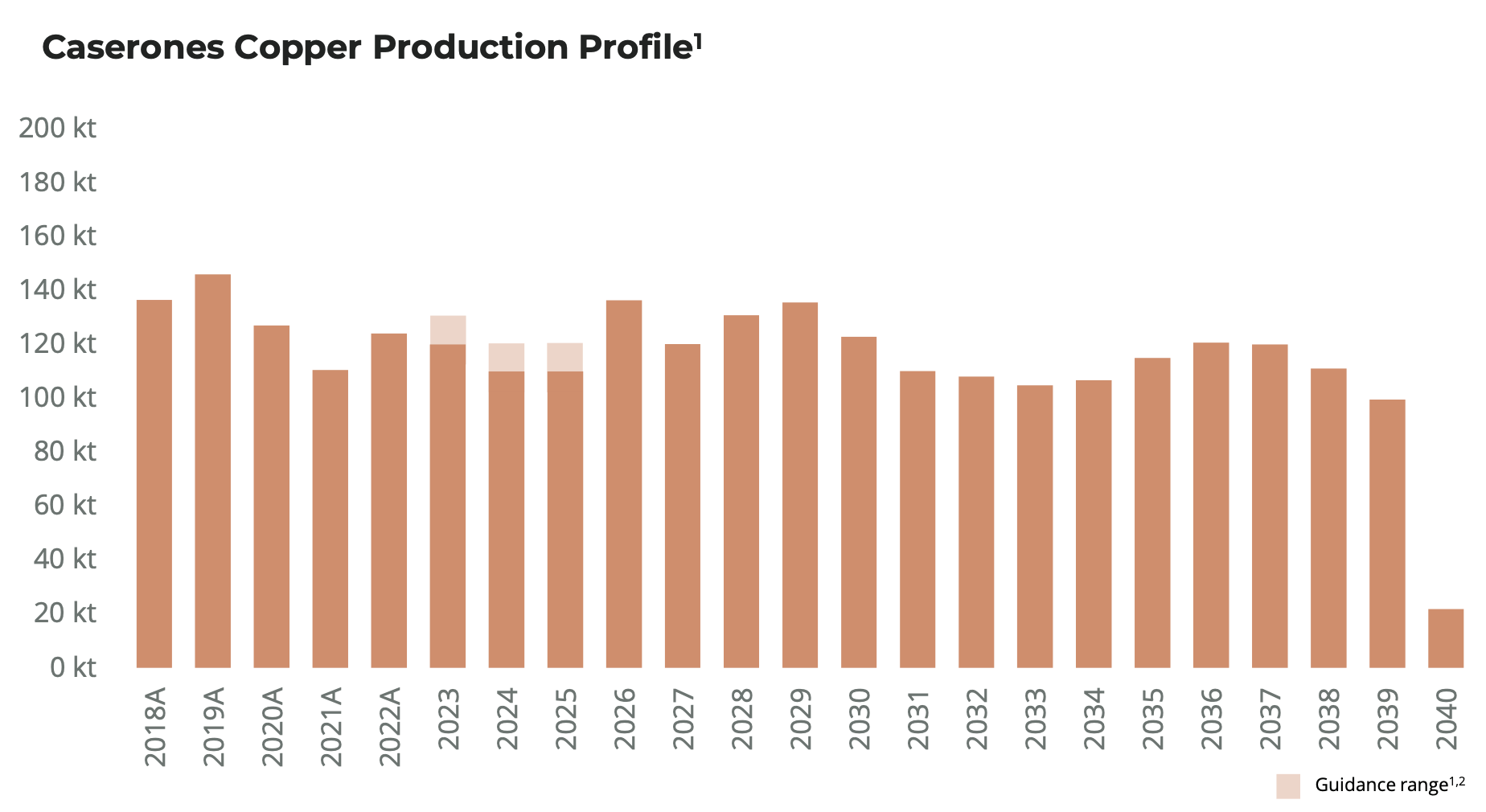

An updated technical report released by Lundin after the close of the acquisition last summer estimated a remaining mine life of 16 years for Caserones, or extending through 2039. During this time, copper production will remain relatively stable and within the historical range. During the next seven years (or through the rest of this decade), copper production will be above that average, or ~270 to 300 million pounds (~130,000 tonnes) per year. Sandstorm received just over 4,000 GEOs from its 0.63% NSR royalty in 2023, and given that it's unlikely that copper will ever drop below $1.25 per pound again, the Caserones royalty should result in an average of ~4,000 GEOs per year (including molybdenum production) to Sandstorm for years and years to come.

The Reserve royalty ounces support this assumption (4,000 GEOs per year x 16-year mine life = 64,000 GEOs). While there aren't as many M&I and Inferred GEOs, there are a host of targets at Caserones that will likely extend the current mine life by at least another 10-20 years. NPV (5%) = ~US$90 million (reserves only)

Terms:

The Aurizona mine is a higher-grade open-pit gold operation owned by Equinox Gold. Equinox brought the mine back into production in 2019, and since then, Aurizona has produced on average more than 125,000 ounces of gold per year. SAND owns a sliding-scale NSR royalty on Aurizona that has consistently paid out 4,000-5,000 GEOs per year.

EQX is currently mining the Piaba open pit, which is part of a 4-km long, continuous gold zone. However, encouraging exploration results beneath the Piaba pit and at nearby targets has resulted in Equinox embarking on an expansion project at Aurizona.

A 2021 Prefeasibility Study envisioned mining the Piaba open-pit, Piaba underground, and open-pit satellite deposits concurrently, which almost doubled the mine life to 11 years and increased annual gold production, with a total output of 1.5 million ounces of gold during the LOM.

The PFS estimated an average annual production of 137,000 ounces of gold, with peak production at more than 160,000 ounces of gold per year. All of these ounces are subject to Sandstorm's 3%–5% sliding scale NSR. At the current gold price of just over $2,000 per ounce, the royalty will generate close to 7,000 GEOs per year for Sandstorm (a substantial increase compared to past years) and over 8,000 GEOs at its peak year (which is double the 2023 GEOs realized from this royalty).

Equinox has the permits in place for three portal locations and plans to start portal development in the second half of this year. The company is also advancing a Feasibility Study on the expansion project.

Using an estimated gold price of $1,700, which equates to a 4% NSR over the life of the mine, Sandstorm estimates that it owns 60,000 royalty ounces in the Reserve category (1.5 million ounces x 0.04 = 60,000 GEOs). I'm using a $2,000 gold assumption for valuation, so I will assume 75,000 GEOs to keep everything congruent. However, I believe there are higher risks to these ounces compared to many of the streams/royalties discussed above. The FS will give more data and an updated mine plan. Costs will likely be much higher than what the 2021 PFS envisioned, and it's not clear if that will negatively impact some of the reserves, which could result in a lower production profile. I would rather be more conservative with Aurizona. I believe that it will continue to operate at least at the current production run rate, but I'm skeptical that the mine will hit 160,000 ounces. As a result, either applying a heavier discount on the Aurizona stream or assuming lower production is warranted. Still, for the foreseeable future (~3-5 years), Aurizona should be a solid cash-generating asset for SAND, with potentially the highest realized GEOs ahead if gold remains above $2,000. NPV (5%) = ~US$85 million

Terms:

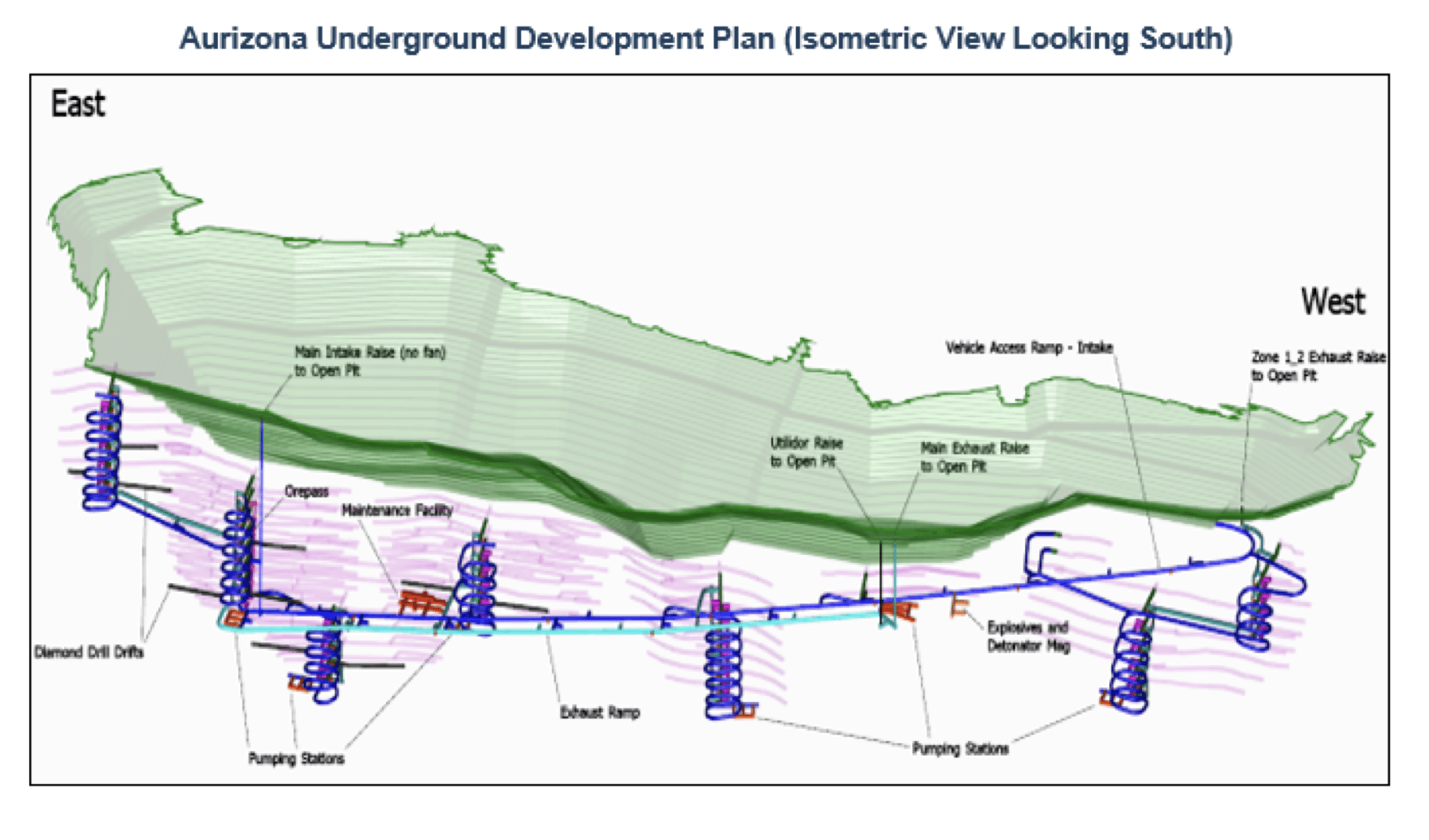

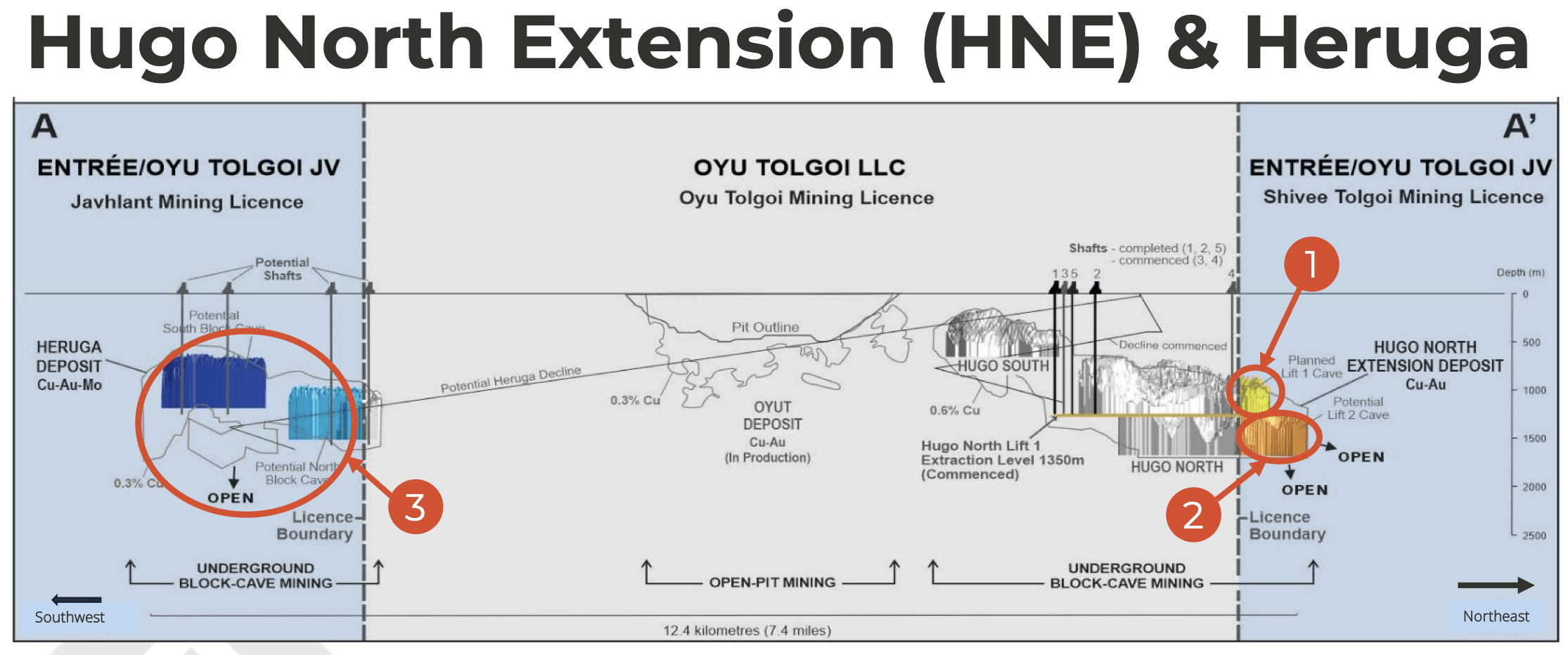

Hugo North Extension

Heruga

The Oyu Tolgoi copper mine in Mongolia is one of the largest and most modern mines in the world. Rio Tinto owns a 66% direct interest in the Oyu Tolgoi project with the remaining 34% owned by the Government of Mongolia.

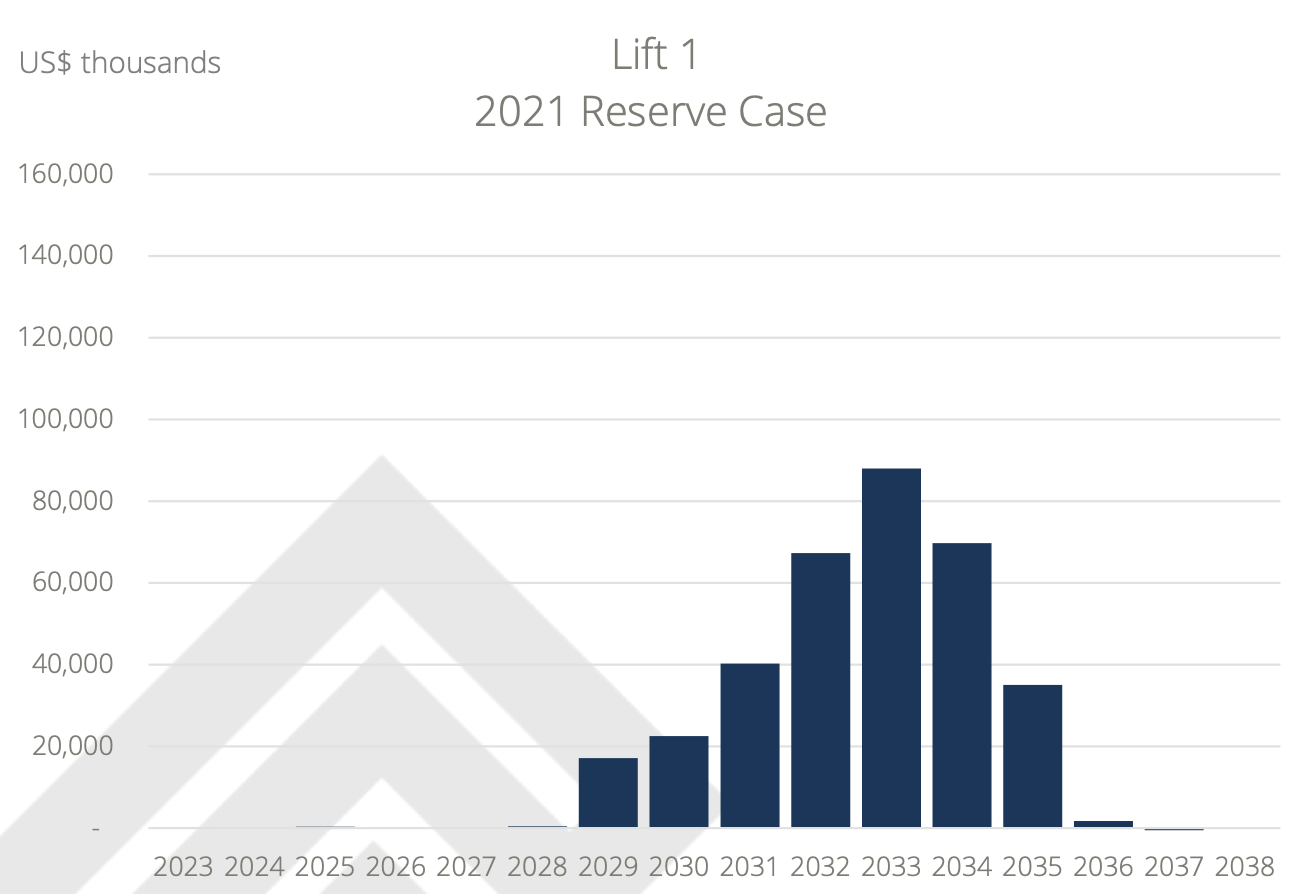

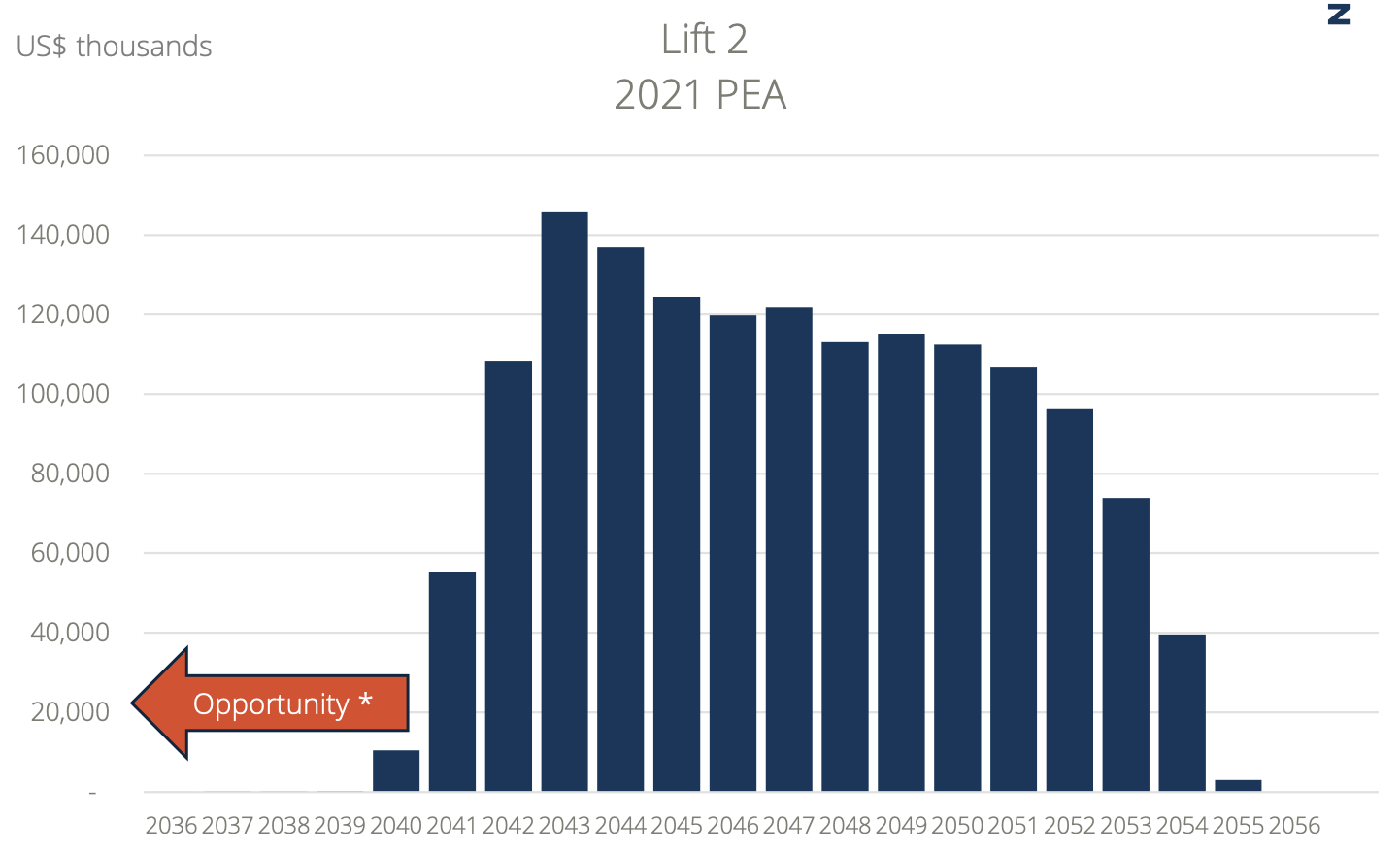

The main ore source since commercial production has been from the Oyut open pit, but now the operation has also moved underground. In the development pipeline for more than a decade, and maybe even considered a "pipe dream" by many, the Hugo North block cave is now in production. Sandstorm owns Au, Ag, and Cu streams on the extension at Hugo North — within the Entrée/Oyu Tolgoi JV boundary. The Hugo North Lift 1 extension won't be mined until later this decade, but it represents solid future growth for SAND.

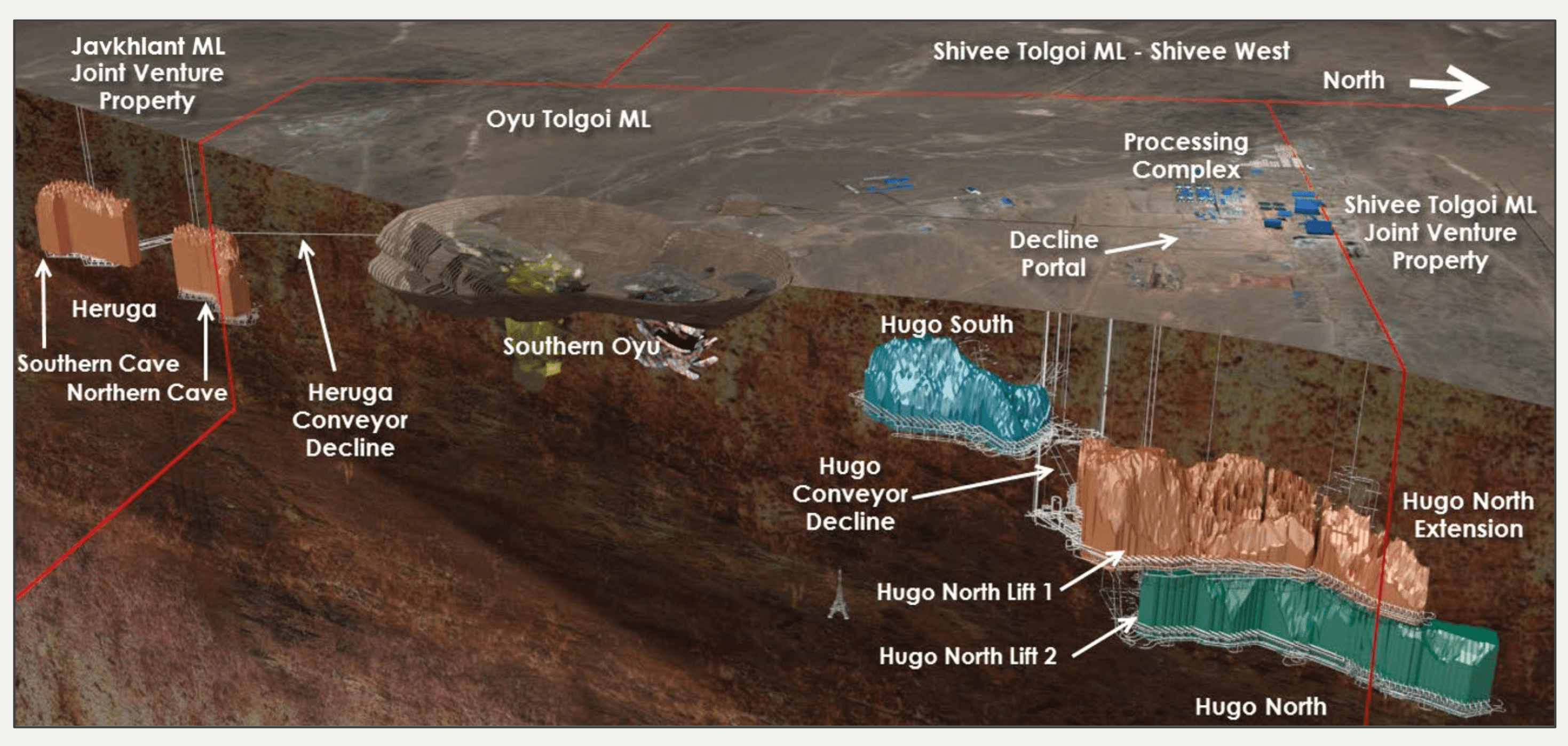

It's difficult to grasp the size of Oyu Tolgoi from the diagram above. The one below provides a 3D model, with the Eiffel Tower also included, to show the scale of all the deposits and the entire Oyu Tolgoi complex. It takes a workforce of 21,000 people (or that of a large town) to run the mine.

By 2030, Oyu Tolgoi will be the fourth-largest copper mine in the world as Hugo North Lift 1 production ramps up over the coming years. It will also be one of the lowest costs, operating in the first quartile of the CuEq cost curve.

Entrée Resources (OTCQB:ERLFF) provides the following graphs, which show its portion of cash flow from Lift 1 and 2 and give SAND investors an idea of when the streams will begin to pay out.

Entree Resources Entree Resources

Just based on royalty ounces in reserves at Lift 1, there are 43,000 GEOs. If you include all of the resources from the Hugo North extension, which includes Lift 2, it's an additional 200,000+ GEOs. NPV (5) = ~US$80 million (Lift 1 and Lift 2 only)

While Sandstorm also holds streams on Heruga, it's not part of the mine plan yet and is decades out. Therefore, I'm not assigning any valuation.

While the above assets are some of the highest valued in Sandstorm's portfolio and have a combined NPV of just over US$1 billion, there are many other streams and royalties worth discussing.

Terms:

Bayan Khundii is one of the highest-grade open-pit gold projects in the world. The mine is currently under development, with first production expected in 2025.

While the reserve/resource base is modest in size at just over half a million ounces of gold, the open-pit grade is ~4 g/t, and there is multi-million-ounce exploration potential.

The jurisdiction might seem challenging, but Erdene Resource (OTCPK:ERDCF) formed an alliance with Mongolia's leading — and largest publically traded — mining company, which is backed by one of Mongolia's largest conglomerates.

Sandstorm's 1% NSR equates to just under 1,000 GEOs per year during steady-state production starting in 2026, with 600-700 GEOs next year. The six-year mine life is short, but the optionality that comes with this NSR and the other 1% NSRs that Sandstorm owns on the surrounding land package (including Ulaan) should not be overlooked. As a side note, Erdene also received a 5% NSR when it formed the alliance on the project. It's not clear if that royalty is up for grabs, but it's possible SAND could increase its NSR royalty.

Terms:

While currently not a principal asset because of its minimal reserves (571,000 ounces of gold as of December 31, 2023), Bonikro is one of the top contributing GEO streams in Sandstorm's portfolio. The mine accounted for ~4,800 GEOs in 2023 and was the company's sixth-highest contributing asset. It will likely remain in the top 10 for the foreseeable future.

Bonikro is a high-grade, open-pit gold and silver mine that has produced over 1 million ounces of gold since 2008. The operation is owned by Allied Gold (OTCPK:AAUCF), which is now led by the former Yamana Gold team, who raised US$267 million last year to fund the growth of its West African assets. In other words, there is a lot of money and seasoned mining professionals backing Allied Gold.

The company is aggressively drilling at Bonikro — a $10+ million exploration program is planned this year — and using its cash pile to improve the operation's outlook.

The mine produced 100,000 ounces of gold in 2023 and is expected to have similar output this year. A waste stripping phase is planned for 2024, but it will open up higher-grade sections of the pits that will be mined in 2025 and 2026.

There are also over 1.5 million ounces of resources at 1.3 g/t, and the goal is to extend the mine life to over 10 years, although not all of these are within the stream boundary.

Still, the 6% stream on Bonikro means that Sandstorm will receive a healthy gold stream from this asset for at least the next several years and will participate in a good portion of the upside potential of the asset.

Sandstorm Gold

Terms:

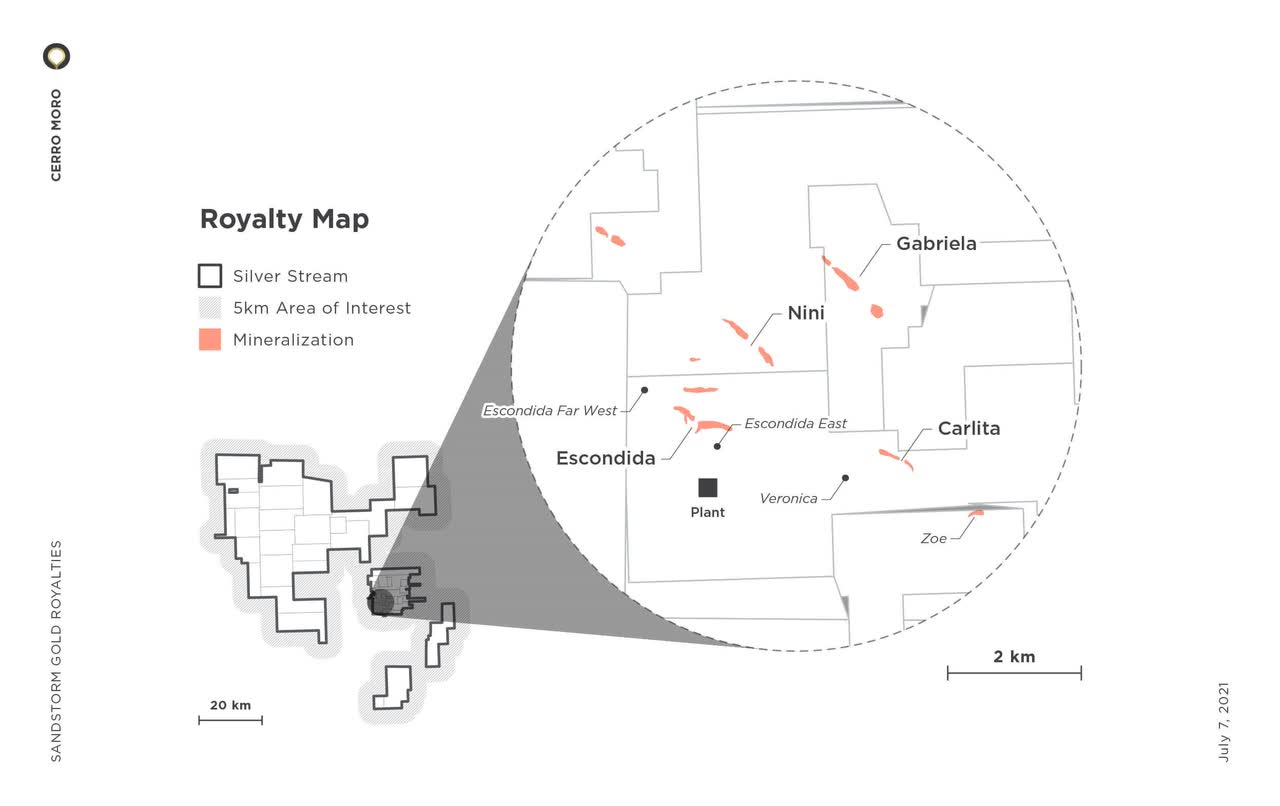

Cerro Moro isn't considered a top asset because of the step-down occurring next year and limited reserves remaining. However, I believe the mine gives Sandstorm considerable optionality.

Cerro Moro contains extremely high-grade gold and silver mineralization, and there are numerous veins on the land package. There are significant upside opportunities on the exploration front that could result in many more GEOs for Sandstorm than what's currently estimated.

Sandstorm Gold

When Yamana owned the mine, the company was contemplating constructing a heap leach operation to process lower-grade ore in conjunction with the high-grade mill feed. It was targeting over 200,000 GEOs per year and a 10 year mine life. Since Pan American Silver (PAAS) took over the asset last year, it's been tight-lipped on plans for Cerro Moro, but it still doesn't change the optionality the asset offers.

Sandstorm Gold

Terms:

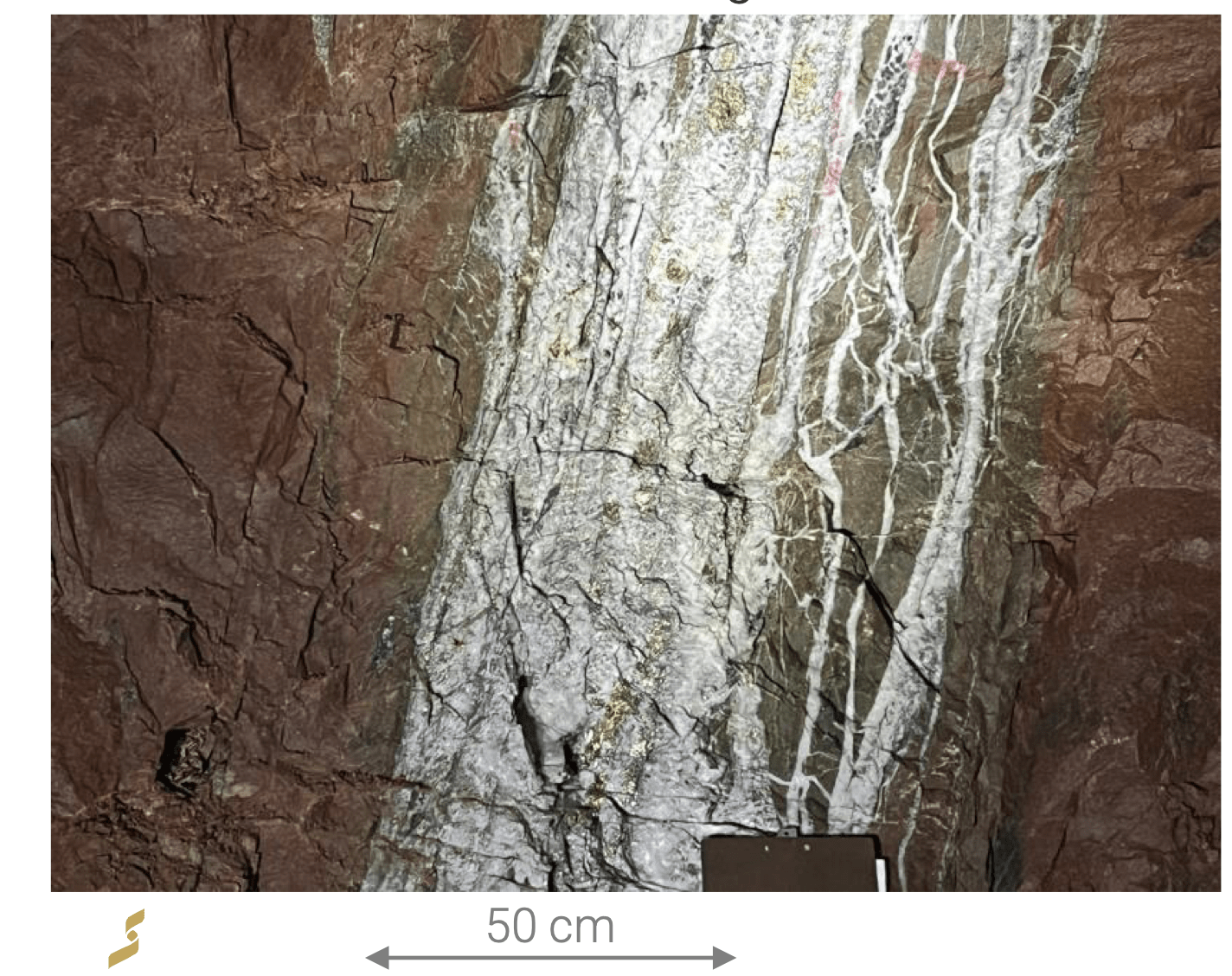

Coringa is a small-scale underground mine and not normally an asset I would highlight, but I'm intrigued by its potential, and it is in production (albeit only trial mining).

While the mine is only expected to produce 38,000 ounces of gold per year due to its limited reserves, it's a high-grade (8+ g/t) deposit performing the exact opposite of what one would expect from a mine of this size, as "The Coringa orebody continues to exceed expectations with payability of the development significantly better than forecast." I've also included a photo of one of the well-defined mineralized veins. At this stage, Coringa only generates ~250 GEOs for SAND, but it will be a nice little royalty (~1,000 GEOs per year) for the company when it reaches full production.

Coringa

Terms:

Fruta del Norte is a high-grade underground gold mine that continues to outperform. The operation produced just under 500,000 ounces of gold in 2023, and it could produce up to 525,000 ounces starting next year. With over 5 million ounces of reserves and some tremendous exploration potential, it's a mine that will be in production for at least the next decade.

Lundin Gold

While SAND only owns a 0.9% NSR on the asset, given the amount of production, it results in a sizable annual GEO contribution. Fruta del Norte should produce ~4,000 ounces of GEOs per year for SAND over the next decade.

Sandstorm Gold

Fruta del Norte has higher jurisdictional risk than other assets in the portfolio.

Terms:

Highland Valley Copper is owned by Teck and has been in production since 1962. The mine produces over 100,000 tonnes of copper per year as well as a molybdenum concentrate. Teck is forecasting higher copper production over the next several years and is currently evaluating the Highland Valley Copper 2040 Project, which will extend the mine life to at least 2040 and produce an additional 1.95 million tonnes of copper over the life of the mine. The current mine life is estimated to end in 2028, but the proposed project will allow it to operate for an additional 14 years.

Since it's an NPI royalty (i.e., based on profits), the GEOs to Sandstorm will vary depending on the level of profitability, not production. But HVC is a profitable mine, and if the mine-life extension project is approved, it will be a high cash-flowing asset for SAND for years to come.

Terms:

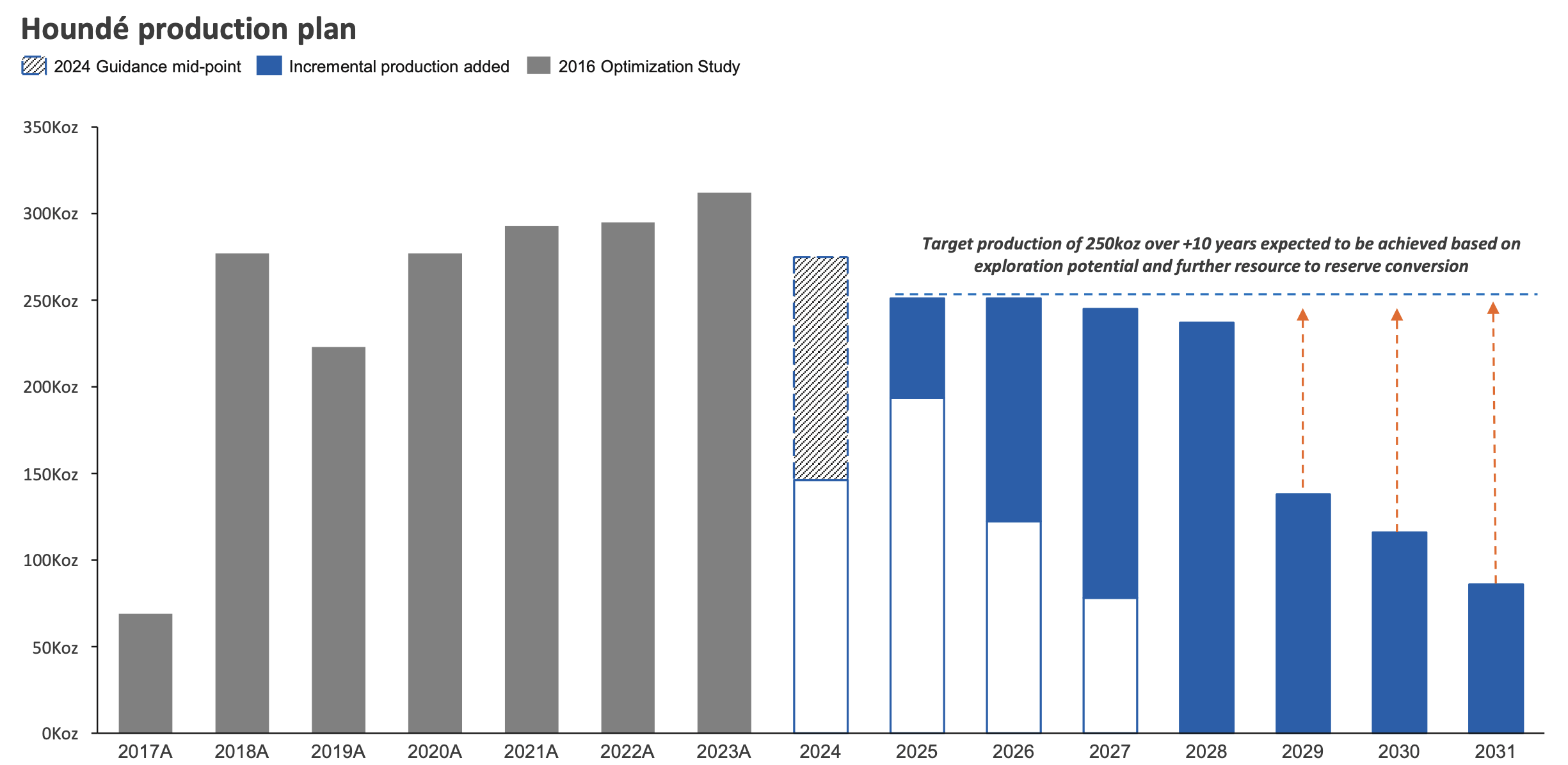

Houndé is a high-grade open-pit gold mine that produces ~300,000 ounces per year. It's been a dependable source of GEOs and cash flow for Sandstorm since the mine entered production in 2017. Successful exploration has resulted in incremental production added, with the mine expected to produce ~250,000 ounces of gold over the next five years on average, and further resource conversion will increase the mine life to 10+ years at that production level.

Endeavour Mining

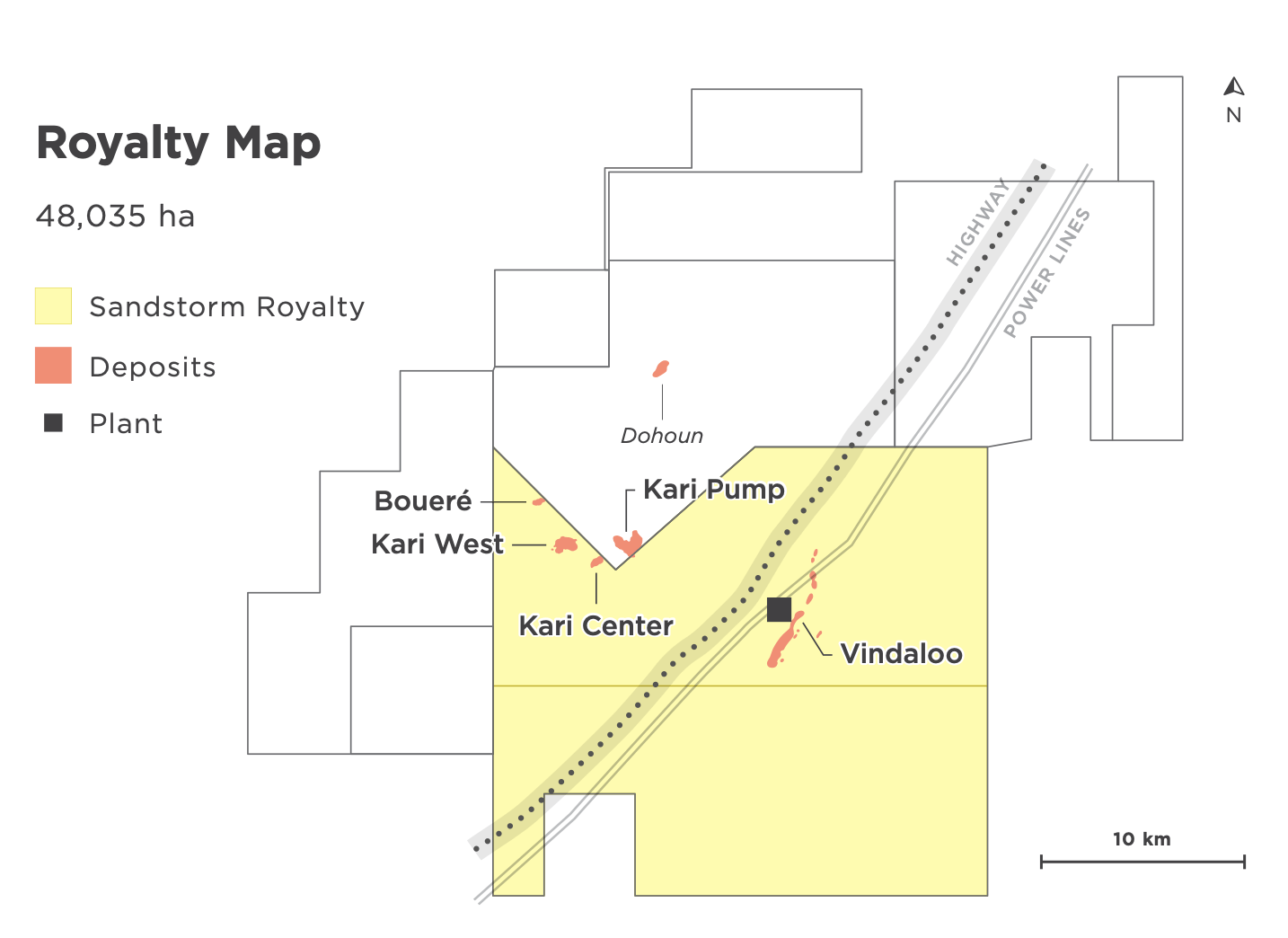

The Sandstorm royalty does not cover the entire mining operation, as current mining activities focus on the Vindaloo Main, Kari Pump, and Kari West pits, and the vast majority of Kari Pump is outside of the royalty boundary. However, the 2% NSR resulted in ~3,000 GEOs flowing Sandstorm's way in 2023. Exploration is focused on prospective areas both inside (just south of Vindaloo and around Kari West) and outside (Kari Pump and targets to the north) the royalty boundary, and I expect Sandstorm will continue to realize solid gold production and cash flow from this royalty for the foreseeable future.

Sandstorm Gold

Like with some of the other royalties/streams in the portfolio, the main risk for the 2% NSR on Houndé is jurisdictional related, as Burkina Faso is a hotbed of extremist activity. However, the highest-risk areas are in the north and east of the country, while Houndé lies in the southwest.

Terms:

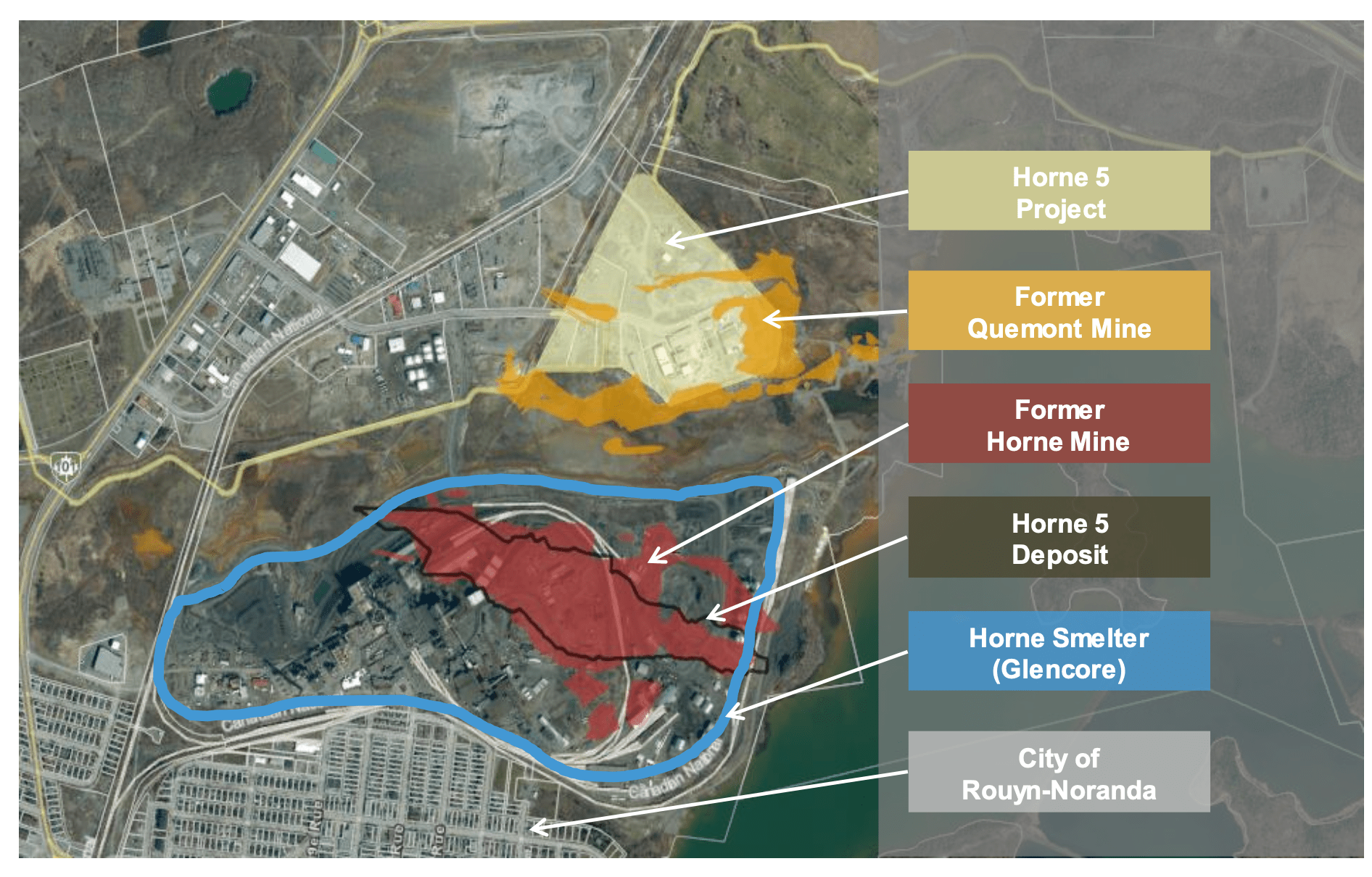

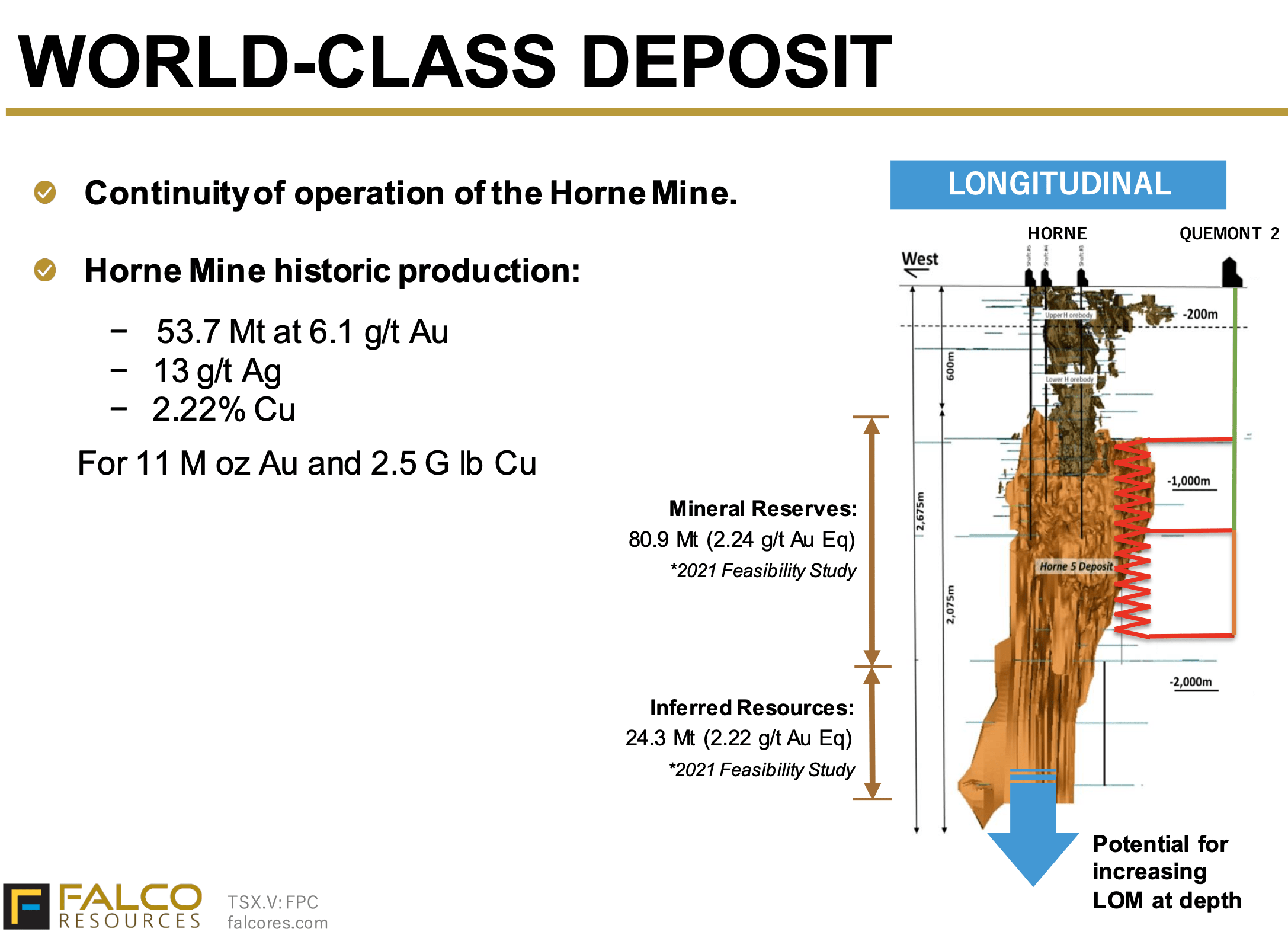

In the advanced development stage for many years without much progress, the Horne 5 gold project now has a clear pathway to commercial production, thanks to the recent signing of an operating license and indemnity agreement with Glencore.

The Horne 5 deposit resides beneath the Horne smelter and below the old Horne Mine, operated by Noranda from 1926 to 1976. Glencore owns the smelter, and this agreement sets the rules so that the Horne 5 operation doesn't interfere with its operation.

Falco Resources

Falco Resources owns the Horne 5 project and will now be able to focus on permitting and project financing.

Horne 5 is a massive deposit with over 6 million AuEq ounces in reserves. The gold grade is low, but like the historic Horne mine, Horne 5 also contains silver and base metals, which will be used as by-product credits. A 2021 Feasibility on Horne 5 estimated 220,000 ounces of gold production over a 15-year mine life with AISC at only $587 per ounce thanks to substantial Ag, Cu, and Zn by-product credits. The cost assumption is out-of-date, but that likely won't have any bearing on the production and, therefore, the amount of GEOs from Sandstorm's 2% royalty.

Falco Resources

The following statement was made about Horne 5 in Sandstorm's Q4 2023 conference call a few weeks ago:

Our 2% NSR on this massive deposit has the potential to cash flow for a generation or more, but has yet to be worked into our future production guidance. However, with the recent development, it gets closer and closer to a definitive timeline.

Terms:

I've highlighted for years the value of Sandstorm's option to convert its NSR on MARA into a 20% gold stream. SAND was receiving zero value for this stream option before and still is today, yet MARA will deliver substantial production and cash flow and could contribute more total GEOs than any other asset in the company's portfolio.

The MARA project is a porphyry deposit that contains 11.8 billion pounds of copper and 7.4 million ounces of gold, along with other metals.

Glencore recently acquired Pan American Silver's majority stake in MARA, which means the project is clearly moving forward, and Sandstorm believes quicker than the market expects.

The 2020 Pre-Feasibility Study projected a mine life of 27 years at an average annual production level over the first 10 years of approximately 556 million pounds of copper equivalent, including 107,000 ounces of gold, as well as silver and molybdenum. The stream would be worth ~20,000 GEOs per year to Sandstorm during the peak production years, with high levels of GEO production continuing well past that point.

It will cost Sandstorm US$225 million to exercise this option, but restructured terms of the deal allow SAND to forgo making payments until construction begins, which is still a few years out.

MARA doesn't account for much of Sandstorm's NAV as the company hasn't exercised the stream option on it yet. When it does, MARA will be the top asset in the portfolio.

Later in this article, I will show production estimates that highlight the impact of MARA.

Terms:

While Mercedes was a top GEO contributor for Sandstorm last year, the stream was restructured starting in 2024 to give the operation and its owner, Bear Creek Mining (OTCQX:BCEKF), a better chance of success.

Mercedes is a work in progress, which has been hampered by Bear Creek's weak financial position. By substantially reducing the monthly stream burden and also restructuring its debt obligations, Bear Creek will realize more free cash flow from Mercedes, which will allow it to invest more in exploration, development, and mine upgrades.

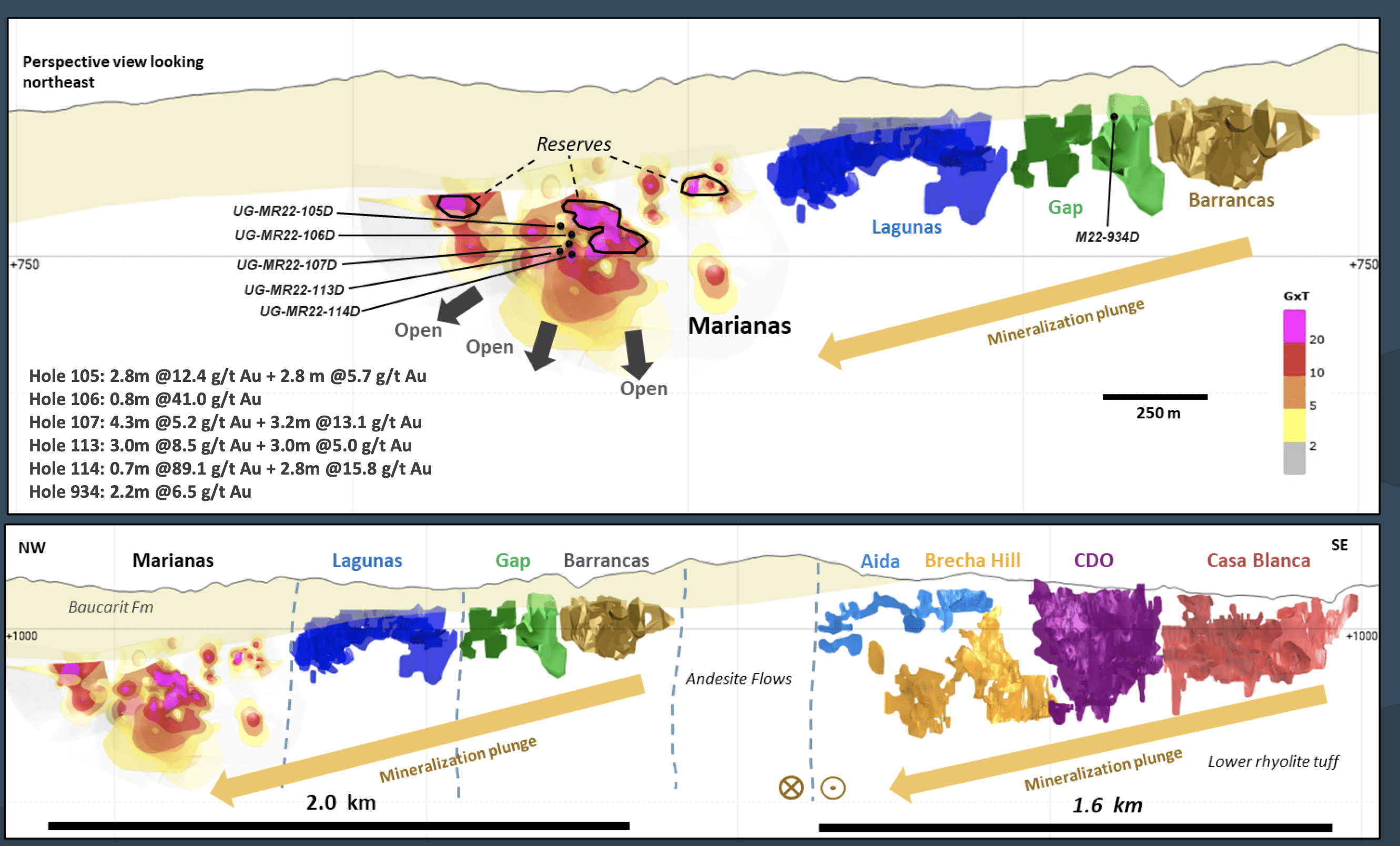

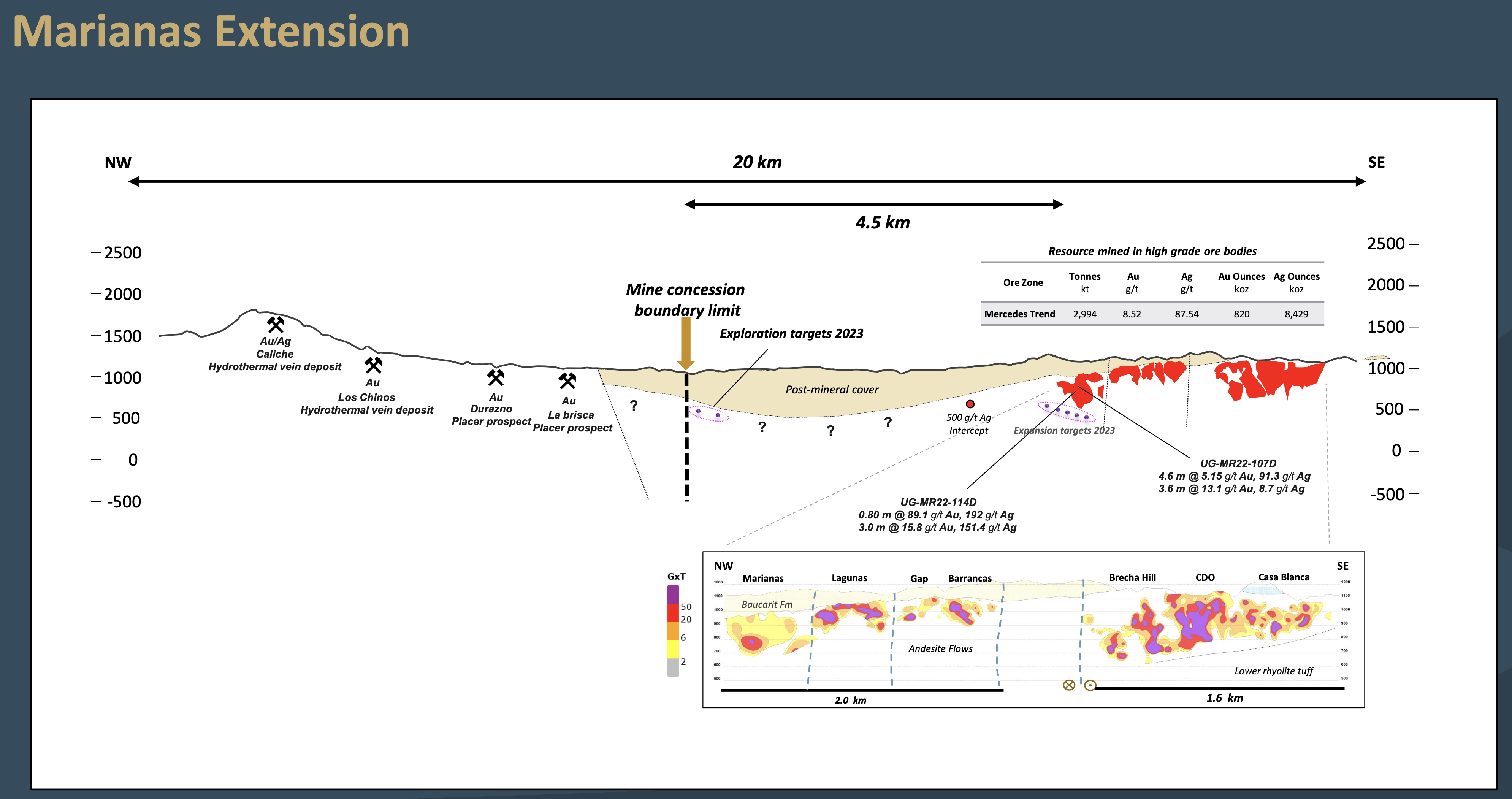

Mercedes has intriguing exploration potential.

Drill results near the current reserves at the Marianas deposit released last year intersected mineralization that was ~2-5x the reserve grade and at solid widths. These are new vein discoveries and also close to the current infrastructure, and this ore could be introduced into the mine plan in the short term, positively impacting production and costs. BCEKF stated that these "new discoveries confirm our thesis that bonanza grades exist within reach of our infrastructure."

Bear Creek Mining

Marianas could potentially extend much further, and there is another 4.5km before it hits the concession boundary limit. There are also a host of deposits on this trend that extend past the land package and might indicate it's one long continuous system.

Bear Creek Mining

Numerous other targets at Mercedes have never been drilled.

There is significant long-term optionality from Sandstorm's gold and silver stream on Mercedes. Having said that, Bear Creek still isn't on solid financial footing, and it's possible that the mine will continue to struggle and remain underfunded over the short term.

Terms:

The Minyari Dome project at North Telfer has grown considerably over the last several years and now contains 1.8 million ounces of gold at 1.4 g/t and over 140 million pounds of copper. A 2022 scoping study estimated a total initial gold output of 975,000, with an average of 168,000 ounces over the first five years. CapEx was under US$200 million.

Another drill program is planned for this year at Minyari Dome, and will likely result in further mineral resource growth.

If Minyari Dome enters production, Sandstorm's 1% NSR would result in ~2,000 GEOs annually.

Assets in Sandstorm's portfolio, like North Telfer, receive little or no attention and aren't included in the company's forward guidance, but there are many interesting development projects that could begin to provide annual GEOs to SAND before the end of this decade. North Telfer is only one example.

Terms:

1.0%–2.25% NSR (1.0% NSR below $1,200 gold, an increase of 0.25% for every $200 increase in the price of gold, and 2.25% NSR above $2,000 gold)

Located at the north end of the Cortez District (10km east of the Pipeline/Cortez Mine Complex) and in one of the most mineralized areas in Nevada, the Robertson project is a key growth asset for the Nevada Gold Mines JV owned by Barrick (GOLD) and Newmont (NEM).

Robertson is an emerging tier-two gold asset in the eyes of Barrick (i.e., one that has the potential to produce 250,000 ounces of gold per year over at least a 10-year mine life and has total cash costs per ounce in the lower half of the industry cost curve).

Roberston is an oxide deposit that contained 1.6 million ounces of gold reserves at the end of 2022 and 2.2 million ounces of M&I resources (inclusive of reserves), and the resource is growing. It's a key long-term source of oxide mill feed for the Cortez Complex.

As Mark Bristow, CEO of Barrick, said in the company's Q2 2023 conference call:

Strong drilling results, staying with Cortez Complex, from Robertson, which show its potential to grow into a multimillion ounce asset. And this is -- it's very important, Robertson. It's still got to be permitted. We are in the process of permitting it, but it's a multimillion ounce oxide deposit. And that's important for Nevada, because we've got capacity in our oxide mills...this is a very key asset. And we're still looking to expand this footprint. It's been a very successful exploration project.

The timeline for first production at Robertson was pushed back from 2025 to 2027, but everything indicates that the mine will contribute 3,000-5,000 GEOs per year to Sandstorm within a few years.

I wanted to highlight Sandstorm's other key assets first, as most investors believe that this story is all about Hod Maden when, in actuality, the project now only accounts for 12% of the company's NAV (and even less if one assumes SAND exercises the option on MARA).

By reviewing all of the streams and royalties above (and I only covered half of the producing assets), my goal was to drive the point home that Sandstorm is much more than just Hod Maden. Hod Maden is one of many quality assets in the portfolio, not the only one.

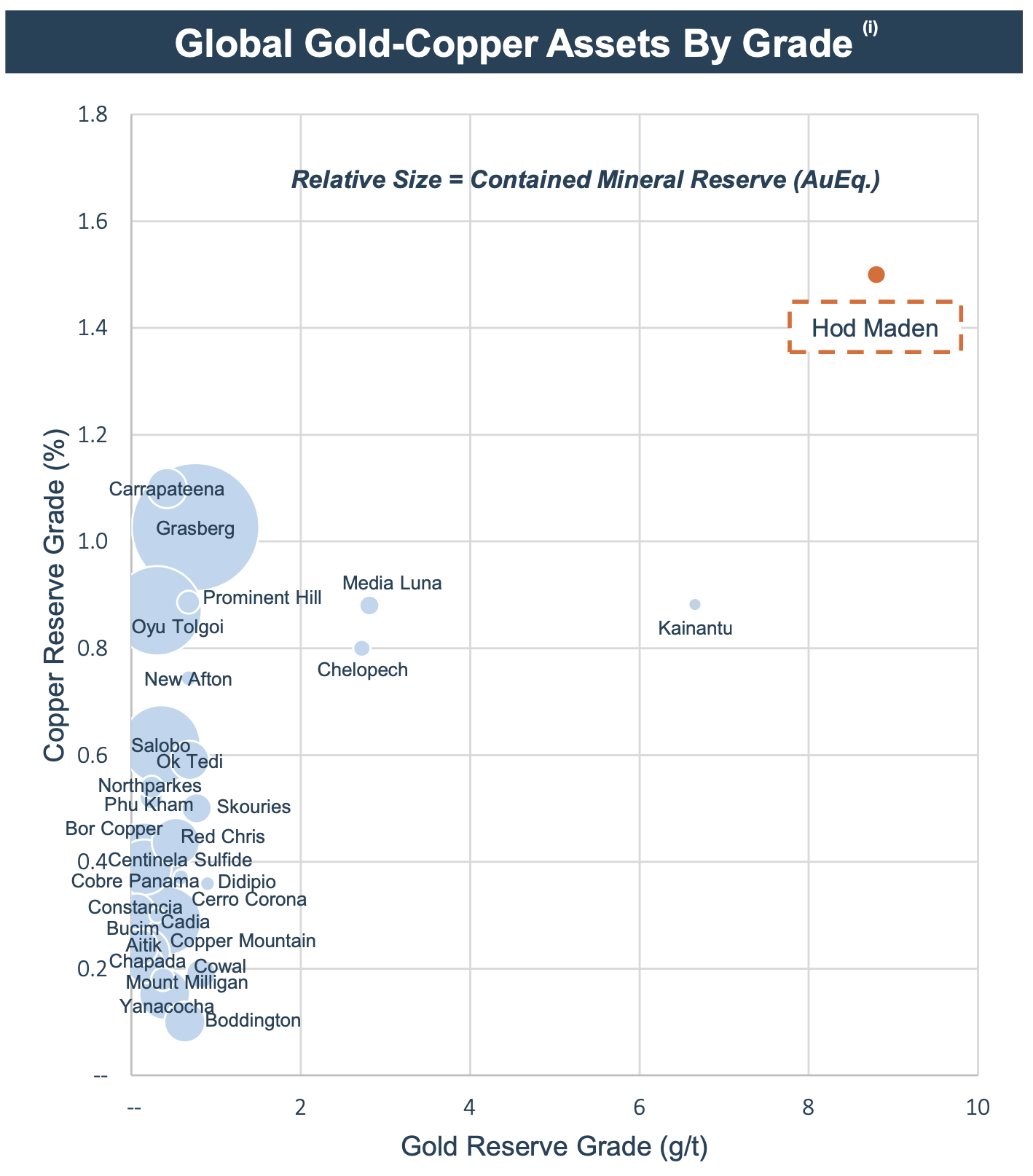

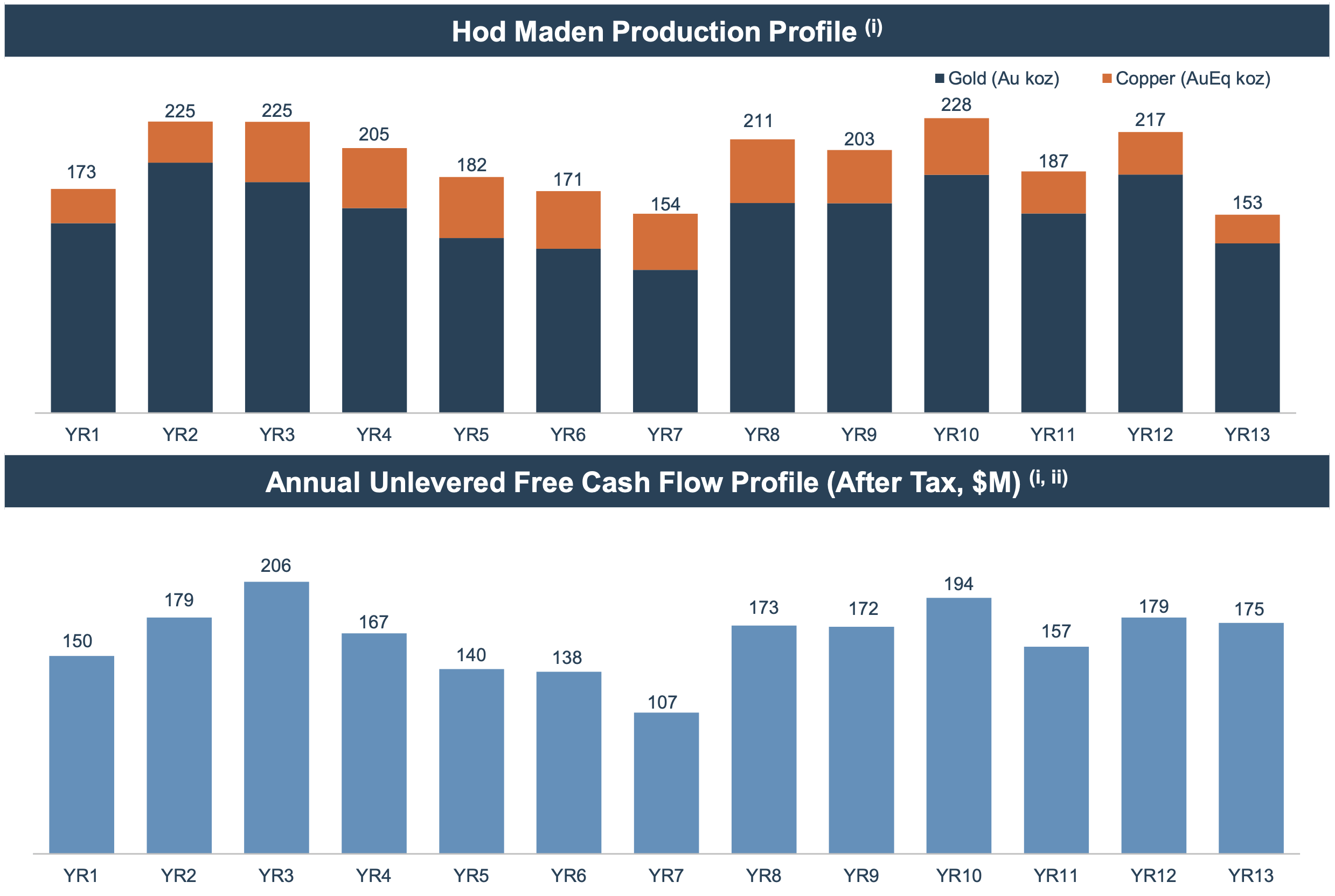

Hod Maden is a top gold/copper project as it's extremely high grade and low-CapEx intensity. There are almost 2.5 million ounces of gold reserves at 8.8 g/t Au and 287 million pounds of copper reserves at a very high grade of 1.5% Cu. Hod Maden is smaller in scale, but it's a clear standout when comparing the grade to other gold/copper mines.

SSR Mining

Gold accounts for 80% of the estimated total metal content produced, with copper production accounting for the remaining 20%. The 2021 Feasibility Study estimated a 13-year mine life with 195,000 AuEq ounces and an AISC on a co-product basis of $588 per ounce. AISC drops to $334 per ounce with copper used as a by-product credit.

SSR Mining

Hod Maden is an incredible asset, but unfortunately, it's acted as a bearish catalyst on Sandstorm's share price for many years.

Most of this is due to the exposure level that Sandstorm previously had to the asset and the countless delays in production over the last 5+ years.

Sandstorm originally purchased a 30% equity interest in Hod Maden eight years ago. This was during a time when SAND was much smaller than it is today, resulting in Hod Maden accounting for an outsized portion (30-40%) of the company's overall NAV. The equity stake — instead of a stream — was also something that investors balked at.

If Hod Maden came online within the time expected, it would generate huge free cash flow for Sandstorm, which is why the company took the risk. But construction kept getting pushed back year after year, and Hod Maden was built into Sandstorm's future production forecast, forcing the company to continually adjust (i.e., lower) its GEO guidance. This had a dramatically negative impact on the share price performance compared to its peers, to the point where Hod Maden was eventually completely priced out of the stock.

In 2021-2022, the outlook brightened for Hod Maden as 1) it received EIA approval, which would finally allow construction to commence, and 2) then Sandstorm sold its 30% equity stake in the project to Horizon Copper in exchange for a 20% gold stream on 100% of Hod Maden (paid for by Horizon's stake in the project).

While this was bullish news, it ultimately didn't do anything for Sandstorm's stock price. In other words, there was zero re-rating, and Hod Maden remained effectively priced out.

Then, in May 2023, another positive piece of news on Hod Maden was delivered, as SSR Mining (SSRM) announced that it had purchased 10% of the Hod Maden project from Lidya Mines for a US$120 million upfront cash payment, followed by $150 million in earn-in structured milestone payments to acquire an additional 30% interest (payable between the start of construction and the first anniversary of commercial production).

SSRM had taken over as operator of Hod Maden, and the project will be managed "under a tri-party ownership structure" between SSR Mining (up to 40% of the project), Lidya Mines (30%) and Horizon Copper (no change to its current 30% position).

Having SSRM step in as a JV partner would not only finally fast-track the project but also result in more information on the progress of Hod Maden and the asset in general. SSR Mining also owns the Copler mine in Türkiye.

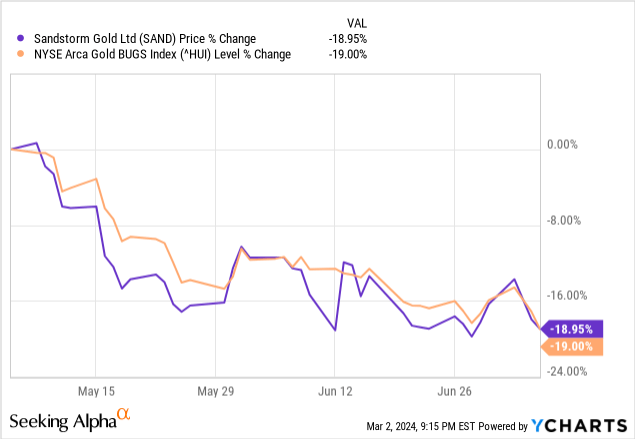

However, the news still did nothing for Sandstorm's stock, as the shares continued to trend lower with the sector over the following months, underperforming during most of that time.

YCharts

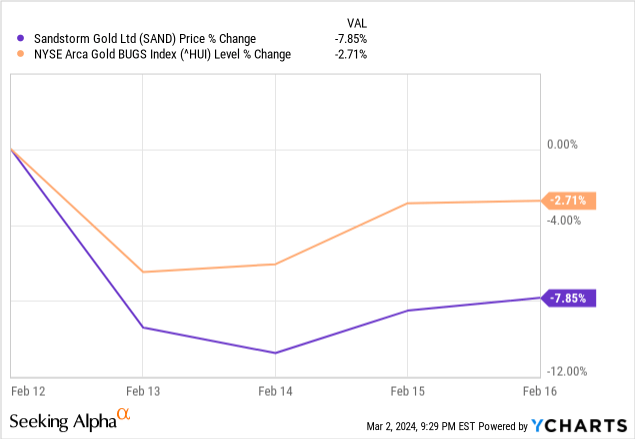

A terrible tragedy hit SSR Mining's Copler mine last month, as a portion of the heap leach collapsed. Lives were lost, and there are many uncertainties about the environmental damage and clean-up cost. Unsurprisingly, the government has canceled Copler's permits.

Even though Hod Maden has been more than priced out, SAND still took a hit when the news on Copler reached the market.

YCharts

Every bit of negative news on the project results in more selling pressure on SAND.

Let me put this another way: SAND's market cap is the same as the amount it spent in 2022 on acquisitions, and SAND's legacy portfolio was already producing 70,000 ounces at the time. Effectively, an asset that accounts for 12% of SAND's NAV, has likely contributed to a 30-40% performance hit (maybe more).

The tragedy at Copler, the extensive cleanup cost, and the view towards SSRM in the country do bring about uncertainty with the development timeline for Hod Maden (and maybe even who will develop it), but again, that's more than priced in.

Nolan Watson, Sandstorm's CEO, said something similar in his comments in the company's Q4 2023 conference call:

On the day this Copler event was announced, Sandstorm stock price dropped 10%. And I think like candidly, it's a crazy overreaction by people who don't understand. Sandstorm was already trading at a discount to our inherent value because of Hod Maden. There is only 12% of earn out. And it isn't our only growth asset, as we have the MARA started to come into the picture. And MARA will eventually be a much bigger part of our now that of Hod Maden because it has a 30-year mine life already. So I believe the market reaction was to take the entire value of Hod Maden out of a market cap again, even though it was already mostly out of our value.

I believe that most investors aren't familiar with Sandstorm's portfolio, and all they know is Hod Maden and a few other streams/royalties, which is likely why Hod Maden gets more attention than it deserves.

It's certainly possible that SSRM will either delay Hod Maden by another year or won't be able to build it at all (as it might lose its social license in the country). However, it doesn't mean Hod Maden can't and won't be built by another company.

Copler and Hod Maden are two entirely different assets. Copler is an open-pit heap leach operation that uses cyanide. Hod Maden is an underground mine (i.e., there is no heap leach), and as Nolan Watson stated during the last conference call, it was: "specifically designed to have no cyanide, so it'd be environmentally friendly. So if there is some reverberation in the mining industry for this incident, these technical issues are not applicable to Hod Maden."

If Hod Maden were in production today, SAND would likely be 50% higher, as the above and beyond discount would need to be removed, and then an in-production Hod Maden would need to be priced in.

Another point on Hod Maden has to do with the value of the stream ounces vs. other assets in Sandstorm's portfolio. Hod Maden stands out as there are 465,000 royalty ounces in reserves, which is almost 2x the amount of royalty ounces of Platreef. However, SAND pays 50% of spot for the first 405,000 ounces of gold on the Hod Maden stream and then 60% for all ounces above that threshold, and only $100 per ounce for all gold reserves received from its stream on Platreef. At $2,000 gold, the Platreef stream will generate more cash flow than the Hod Maden stream because the former is ~2x the margin.

Sandstorm also owns a 2% NSR on Hod Maden, which ultimately puts that asset over the top of Platreef. The point is, though, when you look at the other quality streams and royalties in the portfolio and analyze the margin of the ounces and total ounces produced, Hod Maden doesn't stand head and shoulders above the rest. In fact, it's MARA that will — once the option is exercised.

With the substantial transactions made over the last few years and MARA advancing, Sandstorm doesn't need Hod Maden, but I still believe the asset will eventually reach commercial production.

NPV (5%) = ~US$250–$300 million (depending on the timeline to production)

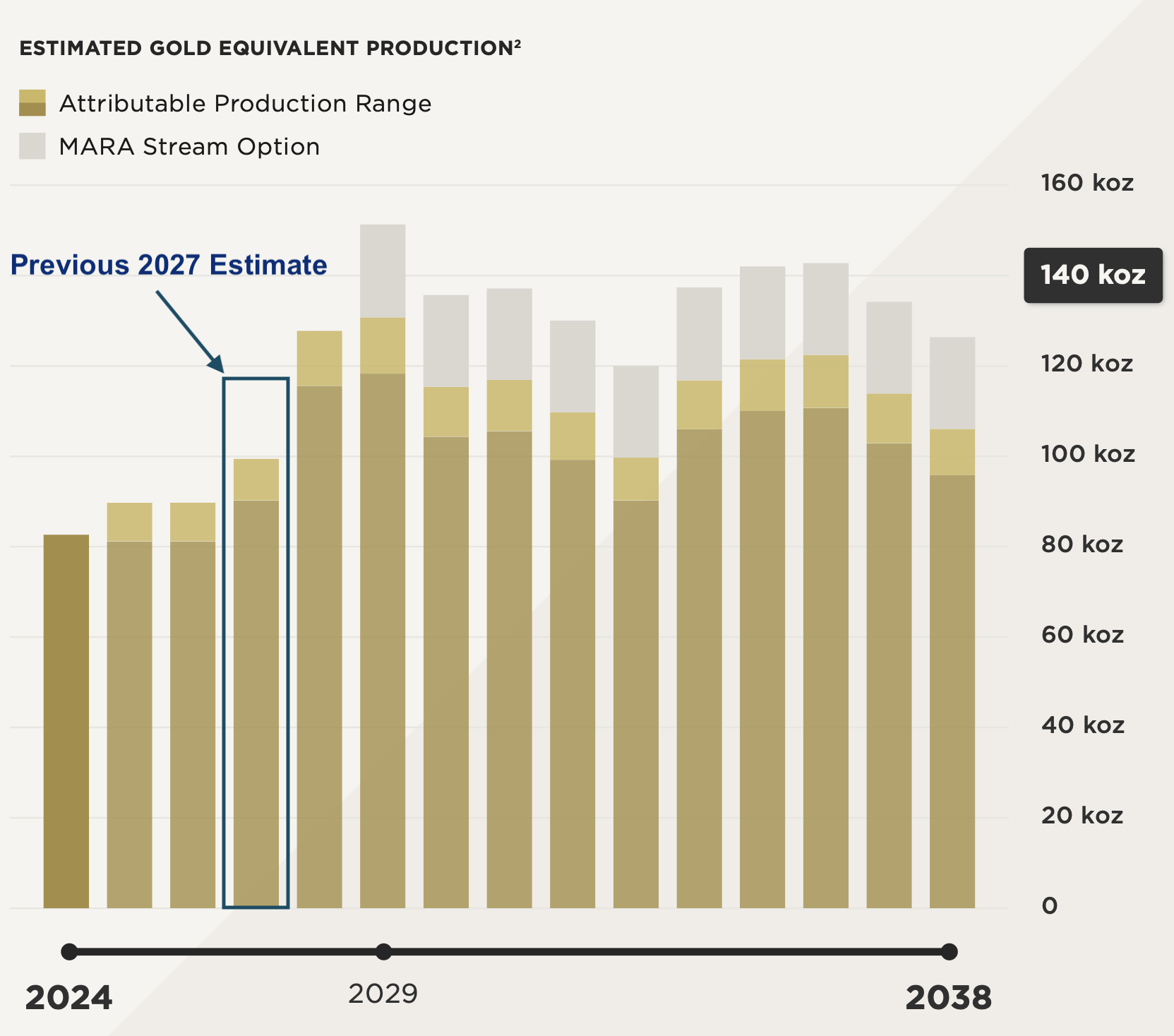

Sandstorm released updated long-term production guidance last month. 2024 GEO production will be ~15,000 ounces less than last year, mostly due to the restructuring of the Mercedes stream (which will result in 10,000 fewer ounces). SAND had already previously guided for this decline in production and estimated ~80,000 ounces for this year in presentations leading up to the new guidance. The only significant difference I noticed was with the 2027 estimate, as the previous forecast called for almost 120,000 GEOs that year, while the latest forecast for 2027 is much lower at ~100,000 GEOs. This reduction is because of SSR Mining's updated construction schedule for Hod Maden. However, this forecast also doesn't reflect the potential further delay in the project due to the incident at Copler. Sandstorm has stated that if MARA is built but Hod Maden is delayed, production will be closer to 110,000 ounces per year later this decade and then ramp up from there. Even if you remove both Hod Maden and MARA from the equation, there would still be 90,000-100,000 GEOs annually from Sandstorm's other streams and royalties over the next 14 years. That doesn't include GEO production from Horne 5, other development assets, or optionality from assets like Cerro Moro. I believe that speaks to the quality and diversification of Sandstorm's portfolio.

Sandstorm Gold

This year, 70% of Sandstorm's revenue will come from gold and silver (56% Au and 14% Ag), with 22% from copper and the remaining 8% mostly from base metals. The copper streams and royalties are a bonus as they give Sandstorm and its shareholders just the right amount (not too little; not too much) of exposure to the metal during a time when there is a global copper shortage.

By 2028, gold streams and royalties will account for 76% of revenue if you include Hod Maden.

A hallmark of Sandstorm over the years was the company always maintained a pristine balance sheet with little to no long-term debt. It used cash flow to fund the purchase of new streams/royalties, allowing the cash to build first. Wash, rinse, repeat.

For example, at the end of Q1 2021, the company's cash position had increased to US$142.5 million, while total liabilities were just US$15.8 million (with no debt). The next quarter, Sandstorm acquired US$138 million of new streams and royalties, including US$108 million on the Vale royalty package, and it didn't need to take on any debt to complete those transactions.

Sandstorm Gold

However, to fund the 2022 acquisitions, SAND took on US$500+ million of debt. The company went from typically having zero debt to half a billion dollars worth.

The much weaker balance sheet has likely put additional pressure on SAND, especially since it limits the company's ability to acquire new streams and royalties.

There isn't much cash on the balance sheet either, as SAND has maintained less than $10 million. It's focused on keeping a minimum cash balance as everything goes towards paying down debt.

Effectively, SAND is on the sidelines for any competitive bidding on new deals.

The company is making progress, as Sandstorm has steadily reduced its debt each quarter since Q3 2022. Debt only dropped by US$21 million last quarter to US$435 million despite the strong operating cash flow in Q4 and the $10 million of proceeds from Sandbox for the sale of the company's El Pilar and Blackwater royalties, but there was also a higher interest payment made and other payables. However, Sandstorm provided an updated debt position when it released Q4 results last month, which showed that its current bank debt declined by $16 million since the close of last quarter, and that was when SAND was only halfway through the current quarter. The company remains on track to hit its $350 million debt target by the end of this year. I also believe SAND is being conservative on the end of 2024 estimated debt level, as the net cash flow using $1,800 gold and factoring in another $20-$25 million of non-core asset sales puts net debt below $350 million. The pace of debt repayment should quicken post-2024; it's only a matter of time before debt is fully extinguished and Sandstorm's balance sheet is pristine again.

Sandstorm Gold

The company does have US$57.6 million of investments in associates, which includes a 34% stake in each of Sandbox Royalties and Horizon Copper.

Sandstorm Gold

SAND also holds US$258.9 million of other investments, mainly in the form of convertible debt instruments. If you include all of the company's investments, net debt will be close to zero by the end of this year. However, these aren't liquid investments, and they are high-risk companies. I believe it's prudent not to include Sandstorm's investments in any net debt calculation, but that doesn't mean they have zero value. Case in point, a good portion of the convertible debt held by SAND is on Horizon Copper, and Horizon is repaying this debt via cash flow from its Antamina NPI.

Sandstorm Gold

Once Sandstorm's debt is fully repaid, these investments will add to the strength of the company's balance sheet.

In 2019, I wrote an article on Wheaton Precious Metals (WPM), discussing how I felt the stock would be aggressively re-rated.

WPM had been under pressure for several years prior as the company had an unresolved tax dispute with the Canada Revenue Agency, and net debt stood at $1.2 billion at the end of 2018 as Wheaton took on a mountain of debt to fund major stream acquisitions.

By the spring of 2019, the company was able to resolve its tax dispute favorably, and net debt was starting to drop sharply. It was clear the trend in declining net debt would continue, if not quicken, which would act as a bullish catalyst for the stock price and further supported the re-rating thesis.

It took less than two years for WPM to extinguish most of this debt and get net debt back to $0 (which then moved into negative territory, or, to put it another way, positive net cash).

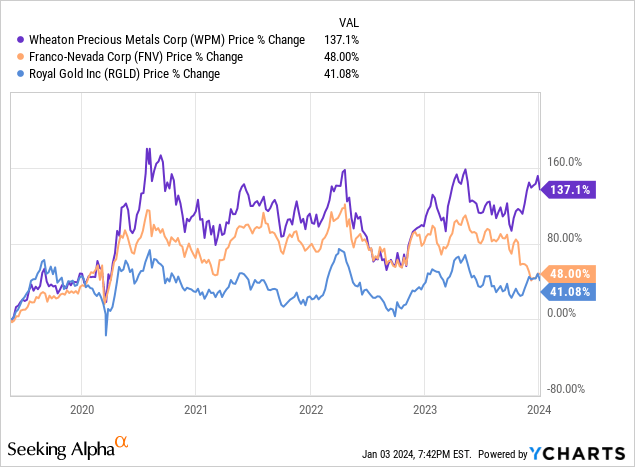

YCharts

By mid-2020, WPM had increased by more than 160%, substantially outperforming FNV and RGLD, as well as the HUI.

YCharts

I see SAND in a similar position as WPM was five years ago, and I expect a re-rating as Sandstorm pays down its debt.

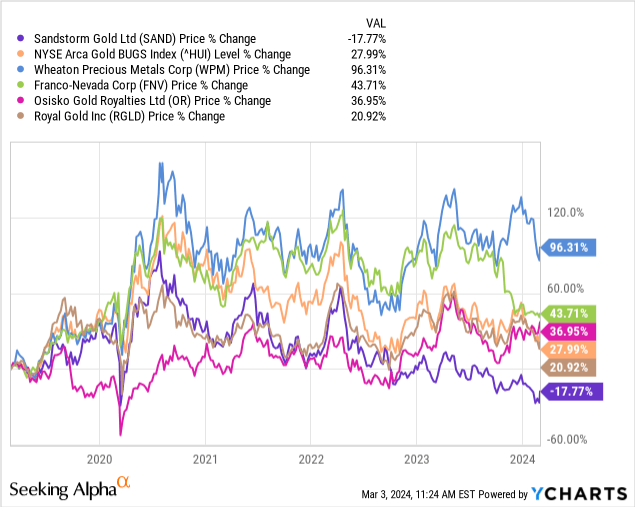

SAND has underperformed the sector by a wide margin over the last five years. The stock is down 18% during that time, while the HUI is higher by 28%, and most of the company's peers have posted even stronger gains, with WPM up by almost 100%.

YCharts

While Sandstorm's valuation has contracted, its portfolio has dramatically strengthened. The company's EV is US$1.8 billion, which is lower today than at its peak valuation in 2020 (before SAND acquired another ~$1.3 billion of assets). In fact, SAND has recently traded at a market cap that is equal to the amount it spent on acquisitions in 2022.

Assuming a ramp-up to 140,000 GEOs over the next several years, SAND is trading at around 0.8x NAV using an $1,800 gold price, and ~0.7x NAV at $2,000. That valuation adjusts for the higher risk of some assets, and it doesn't include the significant optionality of the company's portfolio. Precious metal streaming and royalty companies typically trade at a premium to NAV because of the inherent, risk-free optionality, as well as their fixed cost structures (which aren't negatively impacted by inflation) and diversification.

On an absolute basis, SAND is undervalued, and on a relative valuation basis, the stock trades at a far deeper discount.

The large-cap streaming and royalty companies are trading at close to 2x NAV. Sandstorm's mid-cap peer group (i.e., Osisko Gold Royalties and Triple Flag) are around 1.2x NAV.

I created the following graph that shows the long-term GEO production outlook for the mid and large-cap gold/silver streaming and royalty companies. I also included the enterprise values and respective EV/GEOs multiple. I adjusted Sandstorm's EV higher by $225 million to reflect the cost of the MARA option (which I also did above in my absolute valuation model). As you can see, the 3-5-year outlook for SAND is similar to OR and TRPF, yet SAND trades at a much lower multiple. WPM and FNV are trading at even higher valuations based on their enterprise value and long-term outlook for GEOs.

SomaBull

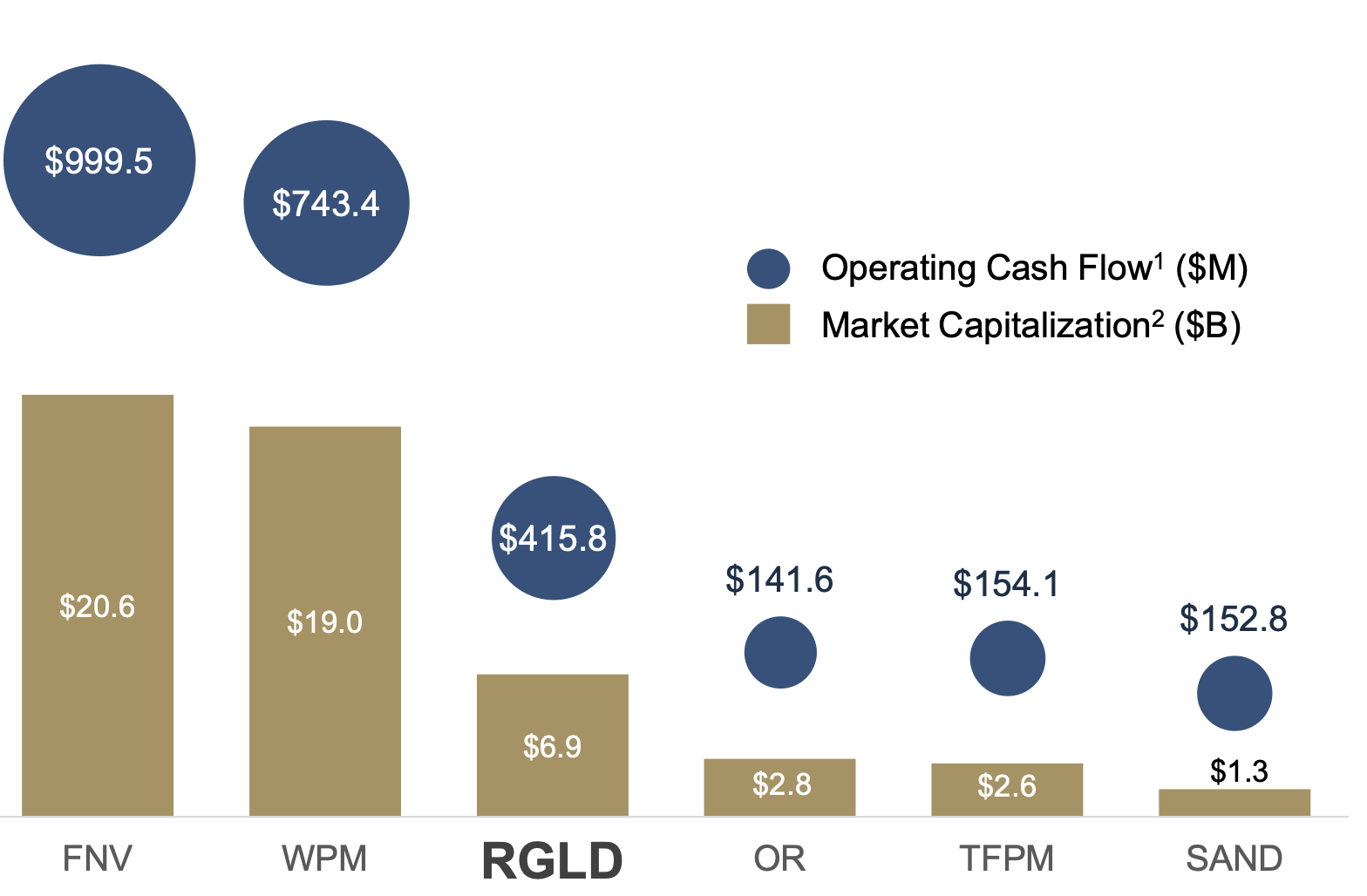

Even Sandstorm's peers don't shy away from showing how cheap SAND is compared to the rest of the group (the graph below is from Royal Gold's recent presentation).

Royal Gold

Let's look closer at Sandstorm vs. Osisko Gold Royalties, as that gap is quite excessive.

To recap, OR has an enterprise value of $2.9 billion vs. $2.0 billion for SAND, factoring in the $225 million cost of the MARA stream option.

I've already discussed Sandstorm's assets and production outlook in great detail. Osisko's 2024 guidance is similar to Sandstorm's, as is the 2028 outlook for both companies. In terms of diversification and overall portfolio quality, Sandstorm comes out ahead. Osisko has an outsized exposure to Canadian Malartic, and I'm skeptical of some of its growth prospects. Osisko also just lost the Renard stream. The only advantage OR has over SAND is on the margin side, but even then, SAND is generating more cash flow from its portfolio. Given the almost $1 billion valuation gap between the two, there is no compelling reason to own OR over SAND, especially when you begin to dig into the assets.

Osisko Gold Royalties

Sandstorm owns a diverse portfolio of quality streams and royalties; Hod Maden is only one piece of a much larger puzzle.

The company's producing assets are generating robust free cash flow each quarter, allowing SAND to continue reducing its debt.

New assets are also coming online that will result in further growth and record GEOs over the next several years, as Sandstorm has a robust long-term production outlook even without Hod Maden.

Sandstorm is trading below fair value on an absolute basis and at a dramatic discount relative to its peers.

I view SAND as the best value and opportunity in the streaming and royalty space.