ronstik/iStock via Getty Images

ronstik/iStock via Getty Images

Back in mid-December 2023, I wrote an article - 2 REITs That Are Likely To Have Alpha Performance In 2024 - on two REITs, which, in my opinion, were poised to outperform the market over 2024.

Safehold (NYSE:SAFE) was one of them due to the following aspects:

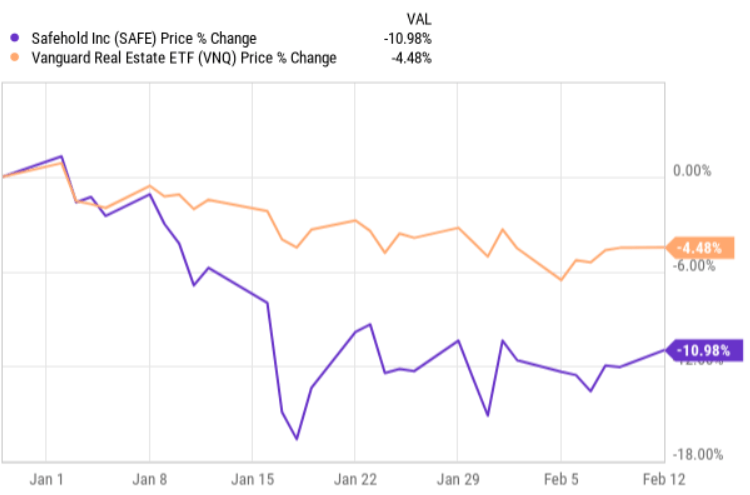

However, since the start of 2024, the thesis has not played out at all. In fact, SAFE has experienced further losses of ~11% that is more than 2x below the overall REIT market's performance.

YCharts

The key reason behind this negative movement in SAFE's share price has been the market repricing its expectations on the forthcoming interest rate cuts. As the SAFE embodies a massive exposure to the duration factor, even the slightest change to the upside in the SOFR dynamics renders a significant impact on SAFE's valuations (just as for the REIT market, but in a more considerable fashion).

Just recently, SAFE published its Q4 2023 results, which reveal a couple of interest elements that investors have to consider in the context of my initial thesis for going long SAFE's stock.

Let's now take a look at these figures and see whether the thesis still remains intact.

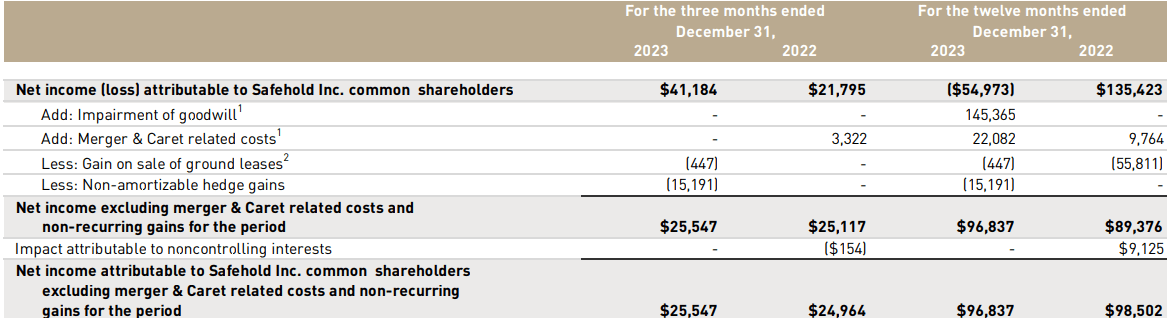

Despite the plunging share price, Q4 2023 results were actually solid and managed to beat the consensus expectations.

For example, Q4 2023 EPS figure landed at $0.36 (excluding non-recurring gains), which is slightly above the $0.35 average analyst estimate. Similarly, the top-line component came in at $103 million, that is massively above $86.6 million as per the consensus estimate.

In the table below, we can see a nice reconciliation of Q4 2023 EPS, which adjusts for the extraordinary items.

SAFE Q4 2023

So, the conclusion here is that financial performance-wise, SAFE continues to deliver stable results in the environment, which is currently extremely unfavorable for the business.

Moreover, if we assess the activity at the investment end, we will notice additional elements that should strengthen the buy thesis of SAFE.

The investment activity in Q4 was high, with decent statistics on both originations and fundings. During the quarter, SAFE registered three new originations amounting to $56 million, with the weighted average rent coverage and economic yield of 2.8x and 7.4%, respectively.

The most critical aspect here to underscore is the economic yield, which is above the current financing costs and the annualized economic yield that is currently embedded in SAFE's books. Namely, it signals that there is an active market in which SAFE can deploy its capital at yield that are sufficient to cover restrictive SOFR and leave a decent cushion for the value (spread) collection.

On the funding side (i.e., injected cash flows), the story is exactly the same, where new investments generate yields that enable value creation. For example, in Q4, SAFE funded several ground leases worth $46 million at 7.4% economic yield.

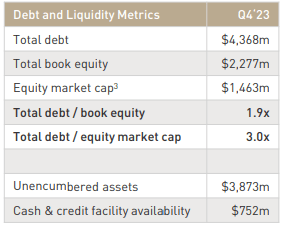

Now, let's take a look at SAFE's balance sheet, which is a significant driver for the overall buy thesis here.

SAFE Q4 2023

The debt to equity both if measures via book value and market capitalization levels remains in solid territory. In 2023, Moody's upgraded SAFE's credit rating from strong Baa1 to A3, which is a clear indicative of resilient cash flows and greatly mitigated financial risk.

However, the most important aspect / change is this:

Q4 2023 results prove that SAFE is able to deliver solid results above the consensus expectations even during an environment in which there are significant headwinds for sound cash generation.

Plus, the recent data indicate that SAFE has also managed to enhance its risk profile by back-end loading first maturities and accumulating ample liquidity that will come in extremely handy in the process of capturing high-yielding investment opportunities that seem to be already emerging.

I view the YTD drop in SAFE's share price as an opportunity for investors, who believe that interest rate will go down by 2026 when SAFE will have to roll over its first debt maturities. Once the SOFR starts to go down, SAFE should deliver outsized returns from the embedded duration factor and widening cash yield spreads.