years/iStock via Getty Images

years/iStock via Getty Images

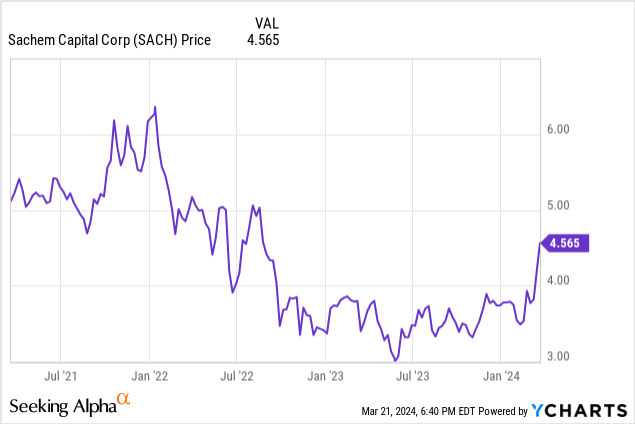

Sachem Capital (NYSE:SACH) still has to report its financial results for the fourth quarter of 2023 next week but I don’t necessarily want to wait that long before boosting my exposure to the fixed income securities issued by Sachem. As the Federal Reserve recently hinted at three rate cuts this year, I am continuing to look into increasing my exposure to fixed income. I own several different baby bonds issued by Sachem Capital as I like the debt securities more than the common shares. This article is meant as an update to my previous coverage of Sachem Capital and its securities and I would recommend you to read the older articles here.

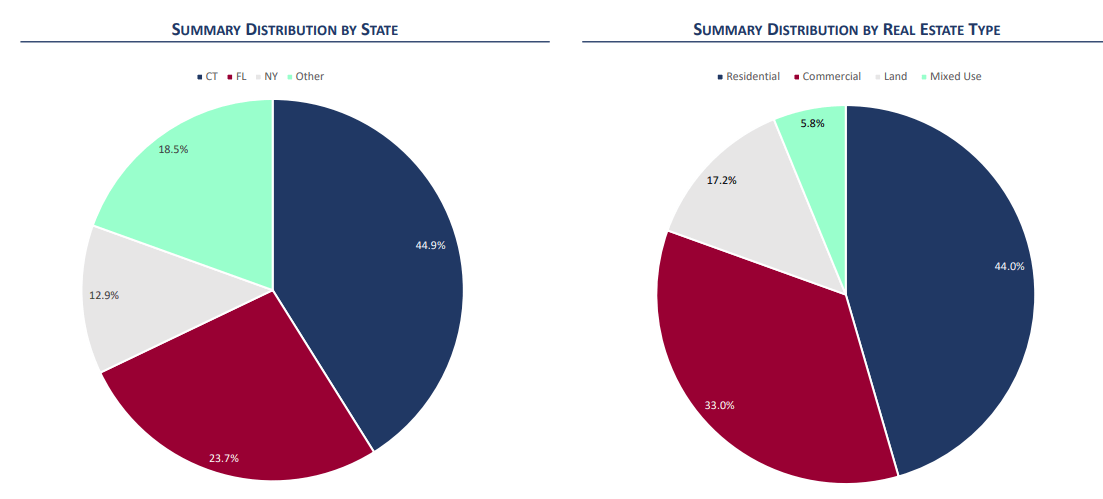

As I’m mainly focusing on the REIT’s publicly traded debt, I am focusing on two things: how well are the interest payments covered and how robust is the balance sheet. As you can see below, Sachem’s loan book mainly focuses on residential and commercial real estate with Connecticut and Florida accounting for the majority of the loan book.

Sachem Investor Relations

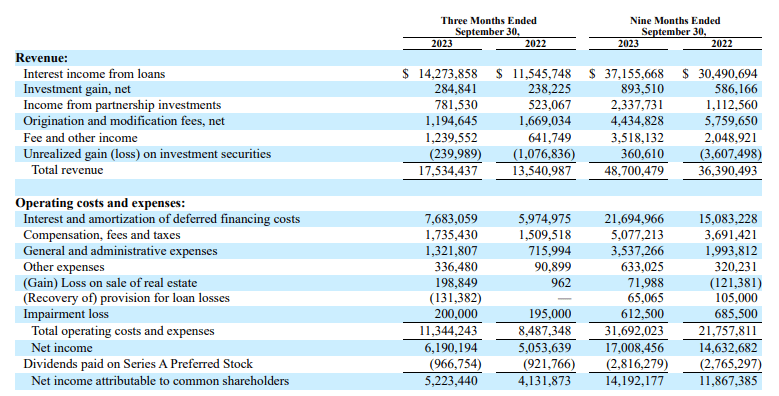

Looking at the income statement of the third quarter and the first nine months of 2023, the interest payments were very well covered. As you can see below, the REIT made approximately $17M in net profit in the first nine months of the year, and this includes $0.7M in non-cash impairment charges and provisions for loan losses. It also included a $0.07M loss on the sale of real estate.

Sachem Investor Relations

This means the interest expenses of $21.7M were well-covered in the first nine months of the year. And looking at the Q3 results, we see a similar result with $6.2M in net income (including a net $0.25M impairment loss & loss on the sale of real estate partially offset by a provision recovery).

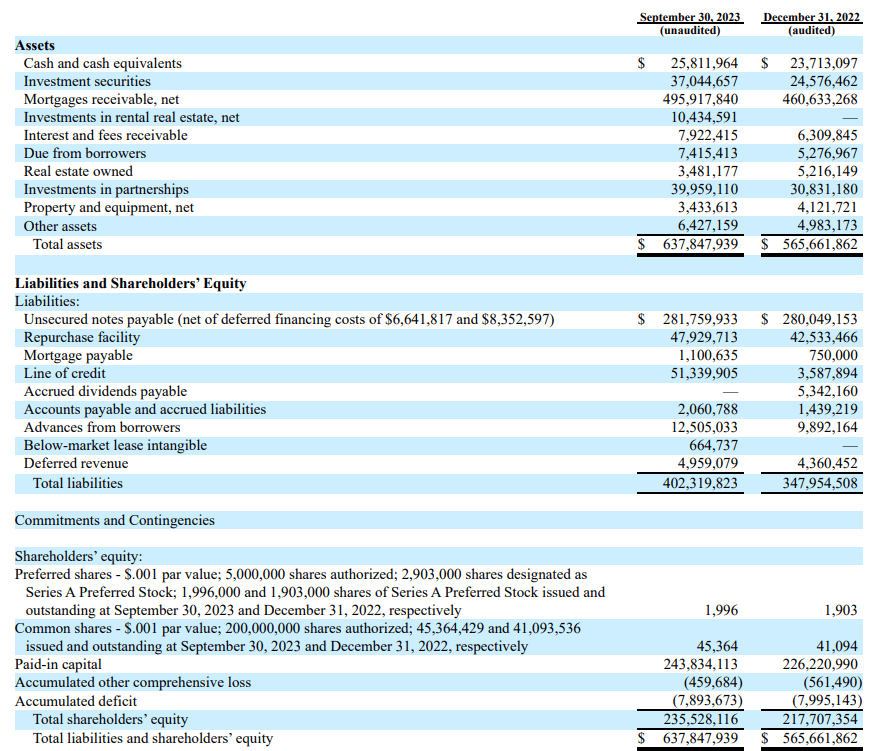

Secondly, the balance sheet has to make sense. As of the end of Q3 2023, Sachem’s balance sheet contained almost $638M in assets, of which $235.5M was equity. That is a nice cushion to have. All baby bonds are included in the ‘unsecured notes payable’, which totalled almost $282M at the end of September (the total face value is approximately $288M). This indeed means the $112M in order debt ranks senior to the unsecured notes.

Sachem Investor Relations

Fortunately the REIT also has approximately $63M in cash and investment securities which means the net financial debt ranking senior to the unsecured notes is approximately $49M. Considering there are $496M in mortgages receivable on the balance sheet as well as $50M in investments in partnerships and real estate as well as $20M in owned real estate and receivables, you could argue the more senior financial liabilities are taken care of the assets excluding the $496M in mortgages receivable.

This also indicates that even if the REIT recovers just 60 cents on the dollars from its loan book, all baby bond holders can be made whole. This means I’m not too worried about the position of the creditors.

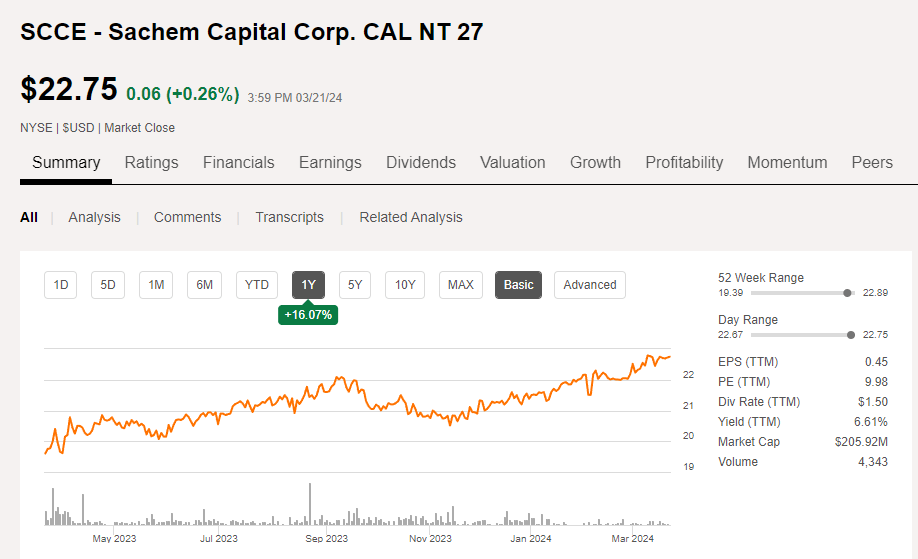

As mentioned in the introduction, I own several issues of the baby bonds that were issued by Sachem Capital. The very first baby bond I bought was the 2027 baby bond which is trading with (NYSE:SCCE) as ticker symbol. These securities are currently callable at any given moment and have a maturity date of March 30th, 2027 (so almost exactly three years from now). Sachem issued approximately $52M of this series of baby bonds.

Seeking Alpha

The baby bonds have a 6% coupon and the $1.50 in annual interest payments is payable in four equal quarterly tranches of $0.375 per note. As the baby bond is currently trading at 91% of the redemption value of $25 per share, the yield to maturity is approximately 9% which I think offers excellent value for money.

One of the main ‘issues’ with this series of baby bonds is that there are several other issues that will mature before the March 2027 maturity date of SCCE so the main risk I see is ‘seniority by maturity’. Debentures with an earlier maturity date have a better chance to be fully repaid versus baby bonds that are still years away from the maturity date.

This is only a small element. There are also other issues that mature after SCCE. SCCF and SCCG for instance both have maturity dates that are further out than SCCE. And as Sachem’s notes maturing in September 2025 have a yield to maturity of 7.8%, I expect Sachem to have no issues refinancing the existing notes. The first litmus test will come in June when Sachem will have to refinance the 7.125% notes which are maturing in June 2024. These notes are currently trading slightly below par so the market doesn’t appear to be too worried about Sachem’s refinancing process.

While I certainly understand the appeal of the common shares of Sachem, I will stick with the baby bonds for now as they add two layers of safety. Both the common equity and the preferred equity are the layers that rank junior to the debt and should thus provide a safety net.

I am looking forward to seeing Sachem Capital’s results next week and I am more specifically interested in hearing the management comments on the default rate and refinancing options for borrowers. At this point, I am avoiding the common shares of Sachem Capital given the 10% premium to the book value. The preferred shares are likely okay but I prefer a 9% yielding debt security over an 8% yielding equity security (although the main difference is of course the perpetual nature of the preferred shares while SCCE has a maximal remaining useful life of 3 years).