Bloomberg/Bloomberg via Getty Images

Editor's note: Seeking Alpha is proud to welcome Matteo Sada, CFA as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Bloomberg/Bloomberg via Getty Images

Investment Thesis

PROS Holdings (NYSE:PRO) is a leader in revenue optimization, boasting impressive free cash flow growth in their last earnings report and consistent subscriptions revenue. However, they haven't achieved consistent profitability and remain heavily reliant on the airline industry. I believe that while diversification efforts and higher investment in AI related technology hold promise, consider waiting for evidence of sustained profitability and reduced industry dependence before investing.

Consequently, my investment thesis is neutral, as I believe the stock fairly valued in the $35-40 range.

Company Overview

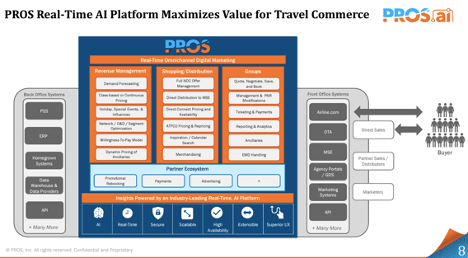

PROS is at the forefront of revenue optimization solutions, empowering businesses across industries with its Software as a Service (SAAS) offerings. Through leveraging a real time learning platform, PROS aids companies in enhancing their pricing strategies, streamlining quoting processes, optimizing configure price quote (CPQ) workflows, and refining revenue management practices as highlighted in their Q3 earnings presentation:

2023 3Q Earnings presentation slides (seekingalpha)

This technology goes beyond the traditional software offerings by continuously improving its capabilities based on real time data, leading to:

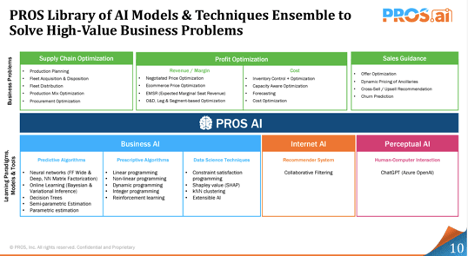

Leveraging this self-learning AI platform, it holds the potential to solve various business challenges across diverse industries including:

2023 3Q Earnings presentation slides (seekingalpha)

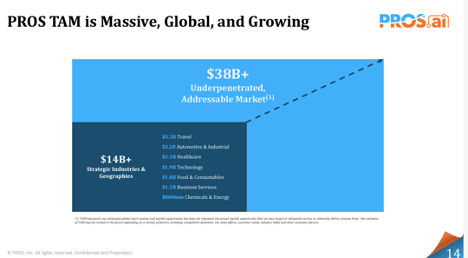

PROS has strategically chosen to make this platform flexible and industry-agnostic, allowing them to approach industries beyond the travel industry. This strategy unlocks significant shareholder value by tapping into a larger Total Addressable Value (TAM) spanning diverse industries, with particular focus on travel and automotive & industrial sectors.

2023 3Q Earnings presentation slides (seekingalpha)

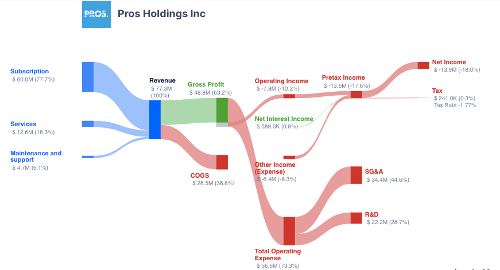

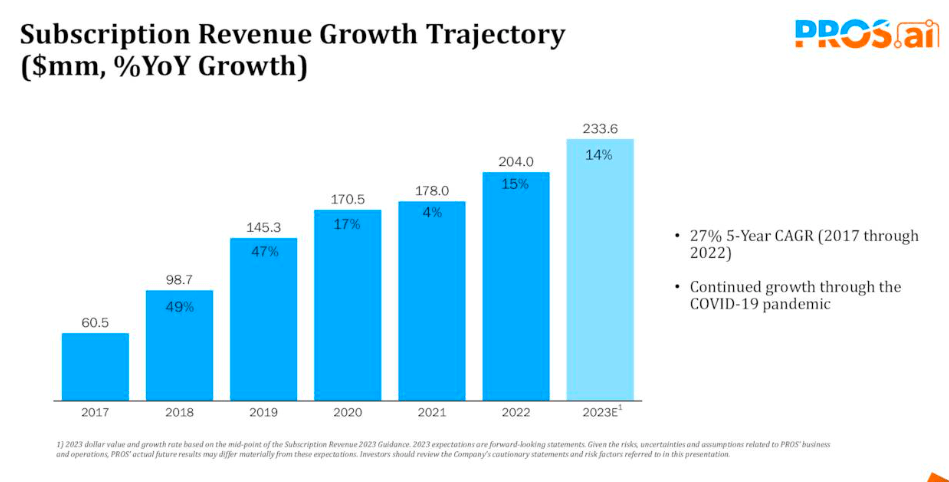

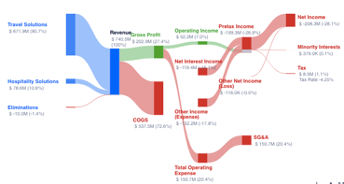

Its main source of revenue is from Annual Recurrent Revenue (ARR) or subscription revenue which tends to be steadier resulting in more steady cash flows but as we will read later this has not always translated into positive earnings.

PROS Income Statement Breakdown (gurufocus.com)

CEO Andre Reiner emphasized this strategic direction during the recent earnings reports, underlining the company's commitment to innovation and growth:

"The PROS value proposition has never been more relevant as businesses continue to lean into digitization, automation, and AI to fuel profitable growth. We continue to set the pace of AI innovation in our markets, and our platform strategy has made our AI innovations easier than ever to adopt. We enter 2024 well-positioned to capitalize on the incredible market opportunity in front of us."

Management Evaluation

PRO Holdings has a strong position in the airline industry and its evident that's increasing expansion into other sectors as part of the corporate strategy. New clients in the latest earnings report that included: Japan Airlines, BASF, and Hewlett Packard, among others.

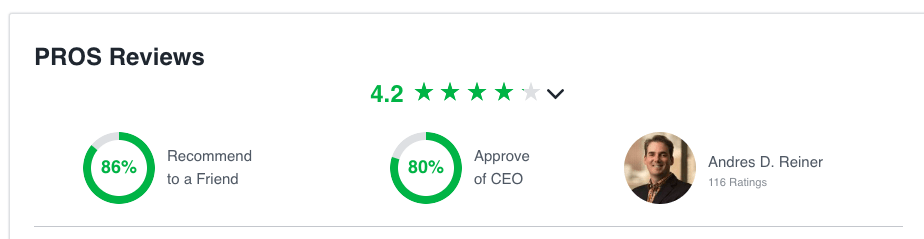

Having joined the company in 1999 before it went public in 2007, current CEO Andres Reiner knows the company inside out and has formed an experienced management team and a diverse board of directors. Their current Glassdoor rating reflects the direction that he has taken with the company:

Glassdoor Rating (Glassdoor.com)

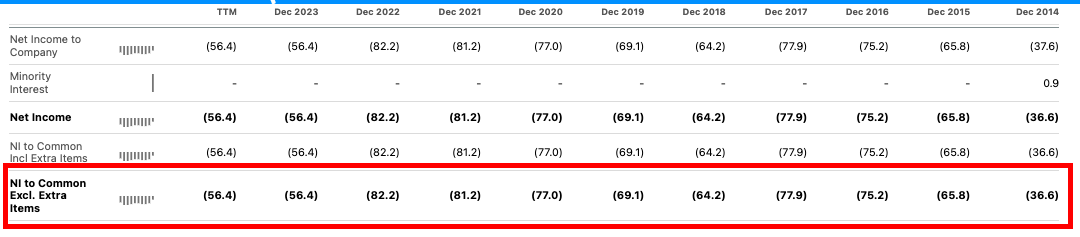

Steady cash flows but volatile earnings

PROS has beginning to penetrate new markets in manufacturing, distribution, and services, thereby augmenting its growth potential. They have also seen a benefit from a rebound in air travel post-Covid as observed in the improved cash flow from operations which has already surpassed pre-pandemic figures. I strongly believe that if they continue with this strategy, they should be able to achieve a full fiscal year with positive earnings in the future.

However, if their dependency in air travel persists, I believe their earnings will be volatile as shown on their annual earnings over the last couple of years.

Net Income Over time (seekingalpha)

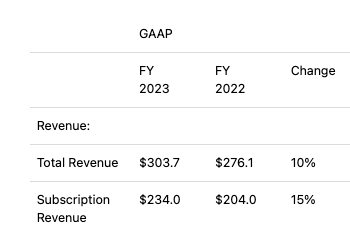

From their most recent earnings report, we can see:

Excerpt from the FY 2023 Earnings Report (seekingalpha) 2023 3Q Earnings Presentation (seekingalpha)

Valuation

Investors often utilize the rule of 40 as a benchmark to assess financial health of SaaS companies. Following McKinsey definition of this rule, I am using PROS Annual Recurring Revenue (ARR) growth rate and free cash flow margin that should be equal or close to a growth rate of 40%.

PROS full year 2023 earnings report:

Revenue $303.3M

Free Cash Flow $13.6M

Free Cash Flow Margin: 4.48%

+

ARR growth: 15%

Which means that their current growth rate sits around 20%.

That is, PROS falls below this 40% benchmark. I would consider reviewing the company again and potentially placing a higher value on the stock price once the company starts achieving results around 30%. For this to happen, a sustained growth rate exceeding 15% ARR for several quarters will be crucial to convince the markets of this potential.

Another metric I like to use is relative valuation. For a company like PROS Holdings this is hard to do as most of their direct competitors, including Zilliant and Vendavo have transitioned to private ownership.

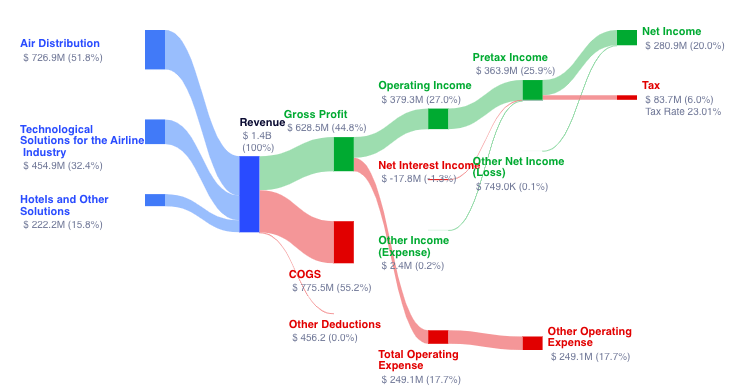

I consider their closest public competitors to be Sabre and Amadeus IT Group as they also offer services to PROS main clients; however, they operate more as technology providers with business models that diverge from PROS. That is both companies operate as intermediaries rather than offering direct software solutions like PRO. For context:

Sabre (SABR): through their travel solution segment they offer a platform for travel agencies to search and book flights, hotels, car rentals, and travel products. Through their hospitality segment they offer a full suite technology solution to assist hotels acquire new guests and improve guest experience.

SABR Income Statement Breakdown (gurufocus.com)

Amadeus IT Group (OTCPK:AMADF) has three business segments:

AMADF Income Statement Breakdown (gurufocus.com)

I consider both Sabre and Amadeus IT Group as indirect competitors, as they present potential competitive pressure for PROS, although their current offerings primarily focus on different areas. Both companies serve some of the same clients as PROS, and it's plausible to think that they could expand into revenue optimization in the future.

I also believe that as technology evolves, AI software implementation costs could decrease, making an entry into this space more accessible for established players like Amadeus IT Group.

For this analysis, I'm also adding software industry leaders, SAP and Oracle, as they could potentially offer similar services as part of a more holistic offering.

Further, I'm using EV/Sales as PROS haven't achieved a full 12 months of positive earnings.

Company Market Cap* CFO** EV/ Sales

PROS Holdings (PRO) | $1.71B | $9.88M | 6.14 |

Sabre (SABR) | $1.57B | ($1.47M) | 2.04 |

Amadeus IT Group (OTCPK:AMADF) | $30.35B | $1.92B | 5.89 |

SAP (SAP) | $211B | $6.97B | 6.09 |

Oracle (ORCL) | $320B | $17B | 7.77 |

Source: Seeking Alpha

*As of 2/12/2024

***Cash Flow from Operations

In comparison to other software companies, including SAP and Oracle, I find PROS to be adequately valued with a 6.14x EV/Sales ratio. On the other hand, Amadeus IT Group exhibits a lower ratio, reflecting its pricing more in line with a technology solutions provider rather than a software company. Sabre's lower EV/Sales ratio can be attributed to its stock price struggling to rebound following the pandemic downturn.

Additionally, just like PROS main competitors, Zilliant and Vendavo have gone private, PROS could potentially become the target of an acquisition. A Reuters article on September 27, 2023, hinted at this possibility as the reason for the stock jumping 13% that week to $36.18. However, the deal didn't materialize due to considerations of a low offer. Subsequently, as of the time of this writing, shares are trading hands at $36.75 as news about a potential sale have been quiet. This suggests to me that the stock is presently fairly priced.

Risks

On one side, the risk to my investment thesis, is PROS potential upside which would materialize if their revenue optimization and pricing solutions software indeed offer a competitive advantage to companies across different industries, and this materializes faster than I anticipate, and they manage to grow their ARR faster than 15% or that they secure an unexpected acquisition at a substantial premium.

On the other side, the potential risks to the downside, involves the risk that a larger competitor, as described above, begin integrating features like PROS as part of a more holistic software solution potentially impacting PROS growth prospects.

PROS Stock Chart (Tradigview)

Takeaway

The main takeaway is that PROS Holdings leverages self-learning AI software in its pricing and revenue management solutions, potentially creating opportunities for diverse industries and future revenue growth. However, consistent profitability that leads to 12 months of continuous positive earnings and exceeding their current growth rate of 20% are crucial to justify a higher valuation. Until concrete evidence of these strategies boosting profitability and growth emerges, a cautious approach is warranted.

Therefore, I consider PROS to be fairly valued in the $35-$40 range and staying on the sidelines. Any weakness below $32 should consider another review.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.