BlackJack3D

BlackJack3D

Royalty Pharma plc (NASDAQ:RPRX) released its Q4 results yesterday. The company delivered outstanding results in 2023 and deployed capital in key value-enhancing transactions for a total consideration of $4 billion.

Royalty Pharma is one of the few companies rated as a Strong Buy. As a reminder, at September-end, we started a long position backed by 1) its unique diversified portfolio, 2) lower execution risks compared to traditional pharma players, 3) a compelling valuation versus royalties companies, and 4) a sound management team with supportive capital allocation priorities.

For a complete overview, here is our initiation of coverage and the Q3 results analysis.

Before commenting on the Q4 results, it is vital to comment on the two latest updates:

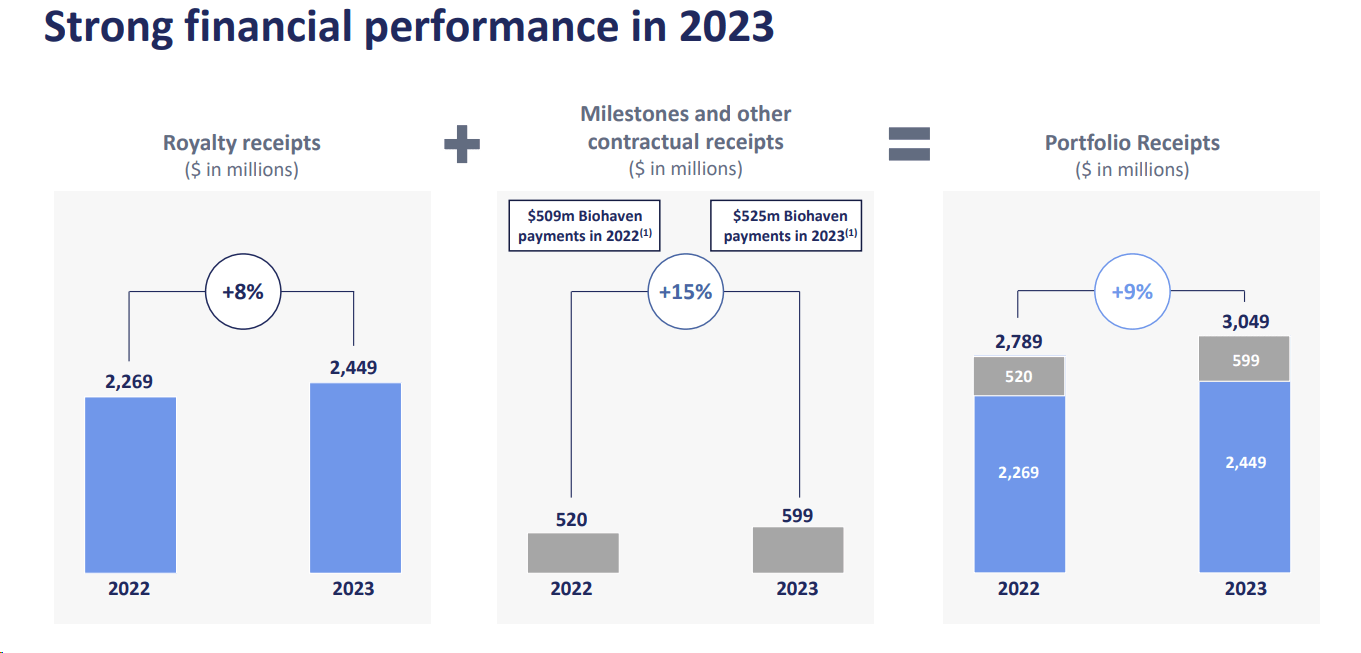

Looking at the results, the company's portfolio receipts reached $736 million in Q4 2023 with a total yearly results of approximately $3.05 billion. The adjusted cash receipt outlook was increased twice in 2023 and exceeded the company's internal expectations set between $2.95 and $3 billion. With this performance, the company reached an underlying growth of 9%. That said, in Q4, the portfolio receipts decreased by 31% compared to last year's results. For our readers and new investors, this decrease is attributable to the accelerated redemption of Biohaven Preferred Shares. Last year, Biohaven was acquired by Pfizer. If we exclude this development, royalty receipts were up by double-digit rates at 10%. This growth was primarily supported by 1) the cystic fibrosis franchise, 2) Evrysdi and Trelegy, and new royalties of Spinraza.

Royalty Pharma 2023 results in a Snap

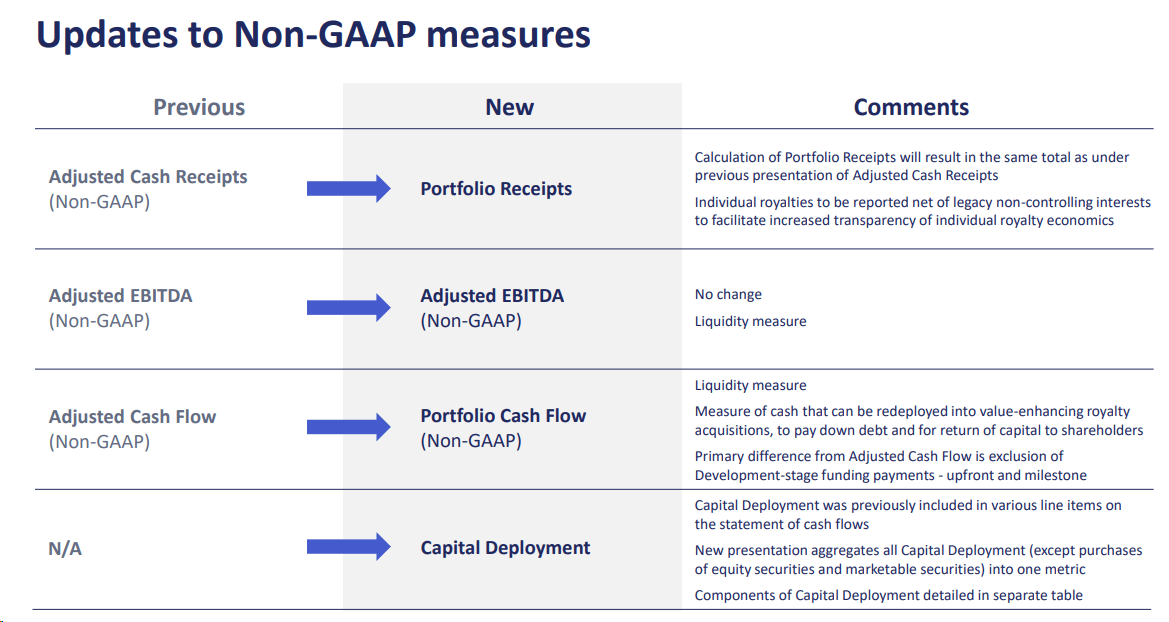

In Q4, the company reported an Adjusted EBITDA of $682 million. This metric is calculated by subtracting payments for operating and professional costs from Portfolio Receipts. For transparency, Royalty Pharma has provided a reconciliation of each non-GAAP measure to the most directly comparable GAAP financial measure. Net cash delivered by operating activities reached $773 million.

Royalty Pharma Accounting Transparency

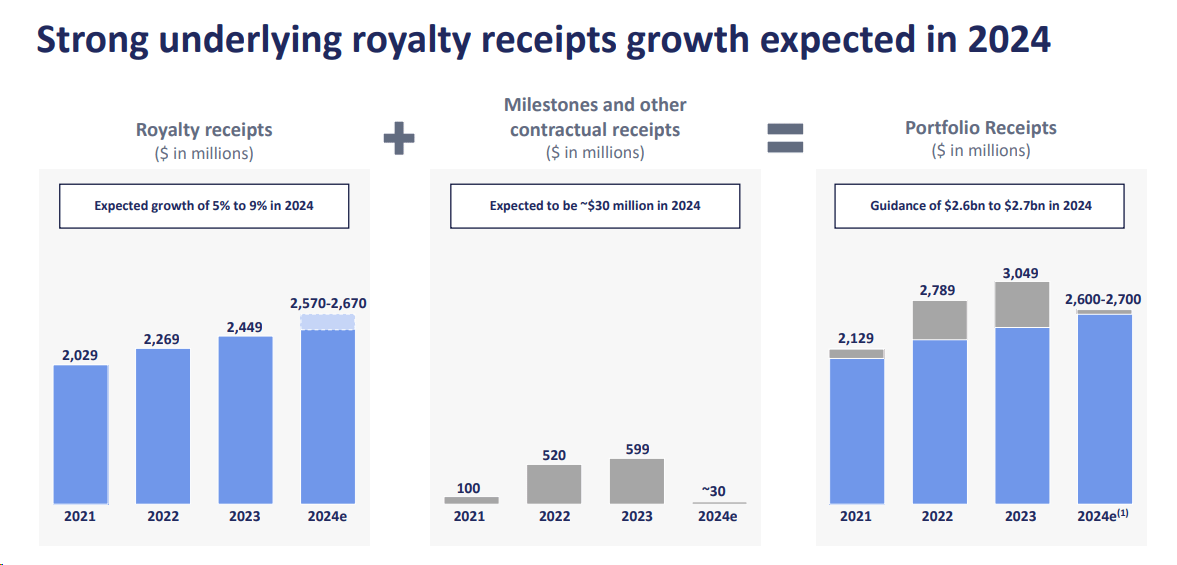

The company provided the new full-year 2024 guidance, which excludes future transactions. Royalty Pharma now anticipates portfolio receipts between $2.6 and $2.7 billion, with a growth in the 5% and 9% range (Fig 3). The company forecast 8/9% of operating & professional costs with an interest expense cost of $160 million. Following Royalty Pharma numbers, we arrived at an adjusted EBITDA of $2.41 billion and net earnings of $2.25 billion. Our 2024 EPS is set at $3.65.

After having listened to the analyst call, there were no updates on any potential dispute with Vertex. As reported by the CEO, the company outlined different scenarios related to the CF franchise development. Downside sensitivity showed a possible impact of a hundred million dollars on RP's sales. RP's patent will expire in 2037.

In addition, the company has repurchased about $300 million of the $1 billion total buyback. With a 5% dividend increase, we are satisfied with the remuneration policy. In our estimates, we now project $363 million in dividend payments. Assuming a $300 million buyback (as happened in 2023) and $1 additional billion of capital deployment to finance new royalties, we arrive at a year-end net debt of approximately $5 billion.

Royalty Pharma 2024 target

The company trades at a P/E and EV/EBITDA of 8.5x and 9.62, respectively. Here at the Lab, we decided to confirm our buy rating status; however, leaving our 12x EV/EBITDA multiple unchanged, we reduced our target price from $42 to $38 per share.

Downside risks include 1) 2026 sales impact from IRA price concessions, 2) Vertex potential dispute, 3) Xtandi royalty that has 1.5 years of exposure to price concessions due to loss of exclusivity, 4) Imbruvica sales erosion on biosimilar competition, and 5) Trelegy's further price cut.

For the above reasons, our buy rating is confirmed.