gorodenkoff

gorodenkoff

I presented my bullish view on Roper Technologies (NASDAQ:ROP) in my initiation report in July 2023, highlighting their unique software portfolios in various niche markets. The stock price has surged by more than 16% since then. They finished FY23 with 7.8% organic revenue growth and 17% adj. EPS growth. I am impressed by their M&A pipelines, and long-term double-digit earnings growth track record. I reiterate the 'Buy' rating with a one-year target price of $633 per share.

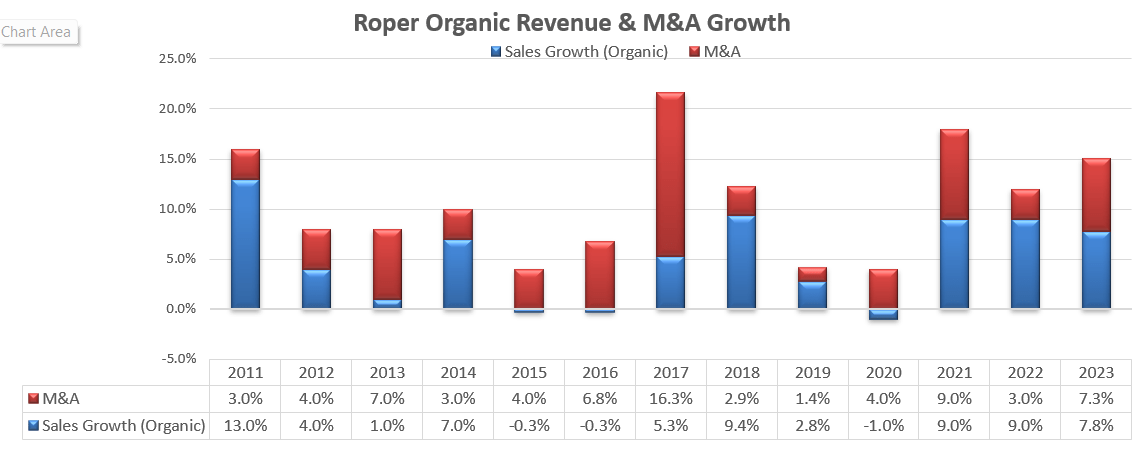

Over the past decade, Roper has consistently delivered robust organic revenue and M&A growth, as depicted in the chart below. In FY23, they sustained strong growth year with 7.8% organic revenue and 7.4% M&A growth.

Roper Technologies 10Ks

The strong and consistent growth is propelled by a variety of factors.

As highlighted in my initiation article, Roper possesses a diverse range of software portfolios tailored for defensive niche markets. Within these niche markets, Roper faces limited competition, granting the company strong pricing power over their customers. A substantial portion of Roper's software portfolios are SaaS-based, yielding highly recurring revenue. As disclosed by the company, recurring business accounts for more than 70% of total revenue.

M&A plays a crucial role in Roper's growth strategy, with a focus on actively acquiring small and medium-sized software companies specializing in vertical software solutions. Roper is operating as a decentralized organization, which makes it easier for these acquired businesses to be fully integrated into the organization. As shown in the slide below, Roper's portfolio encompasses entities of various sizes. The management delegates many decision-making authorities to these independent entities, empowering them to swiftly adjust their marketing, products, pricing, supply chain, and sales strategies.

Roper Technologies Investor Presentation

Roper allocated $2.1 billion toward vertical software acquisitions in FY23.

Roper completed the acquisition of Syntellis Performance Solutions for $1.25 billion in August 2023. Syntellis is a SaaS player specializing in performance management and data solutions for healthcare, education, and financial institutions. According to the release, Syntellis is expected to generate $185 million in revenue and $85 million in EBITDA in 2024. As such, the deal price represents around 15x EBITDA, a quite reasonable multiple for a software company.

In May 2023, Roper announced its plan to acquire Replicon, a provider of unified time-tracking solutions. The deal could enhance Roper's enterprise software and project management solutions, adding more than 2,500 customers to Roper's platform.

In January 2024, Roper announced a deal to acquire Procare Solutions for a net purchase price of $1.75 billion. The deal represented around 18x EV/EBITDA multiple. Procare is a leading SaaS vendor specializing in early childhood education centers.

Over the earnings call, their management expressed confidence in their M&A pipelines, and they will remain active in the acquisition market given their strong balance sheet. Their net debt leverage is around 2.4x EBITDA, and they have ample capacity for future M&A activities.

As evidenced by these deals, Roper prefers niche software players in defensive niche markets. With a more acquired vertical software portfolio, Roper would generate higher recurring revenues carrying higher gross margins. These deals make strategic sense for their multi-year portfolio transformation, in my view.

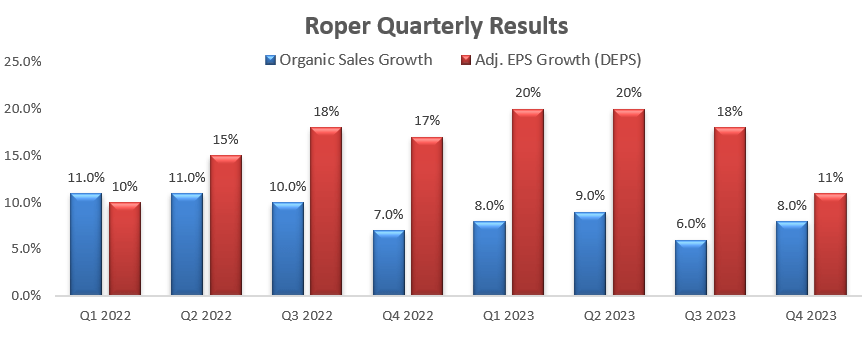

Roper released their Q4 FY23 result on January 31, and they delivered 8% organic revenue growth and 11% adjusted EPS growth, with strong margin expansion. Acquisitions contributed another 4% to the topline growth. Over the past few quarters, Roper has achieved strong EPS growth, as illustrated in the chart below.

Roper Technologies Quarterly Results

The margin expansion was propelled by strong growth in gross margin, primarily attributed to the expansion of high gross margin software businesses. I mentioned Roper's portfolio transformation over the past decade, noting that their increased focus on SaaS businesses contributed significantly to the margin expansion.

On the capital allocation, Roper generated $1.927 billion in free cash flow, and paid out $290 million in dividends, a consistent capital allocation policy.

For FY24, Roper guides 5%-6% organic revenue growth, approximately 6% acquisition growth and 7.7% adjusted EPS growth. Roper has delivered an average of 8.6% organic revenue growth over the past three years. Their FY24 is a bit lower than their historical average. The company is expecting two main growth headwinds. Firstly, there will be a continued subdued activity from large customers in their Application Software segment. Secondly, they expect weak growth in the freight-matching business within their Network segment.

I think the guidance is quite conservative, and the management might want to manage investors' expectations.

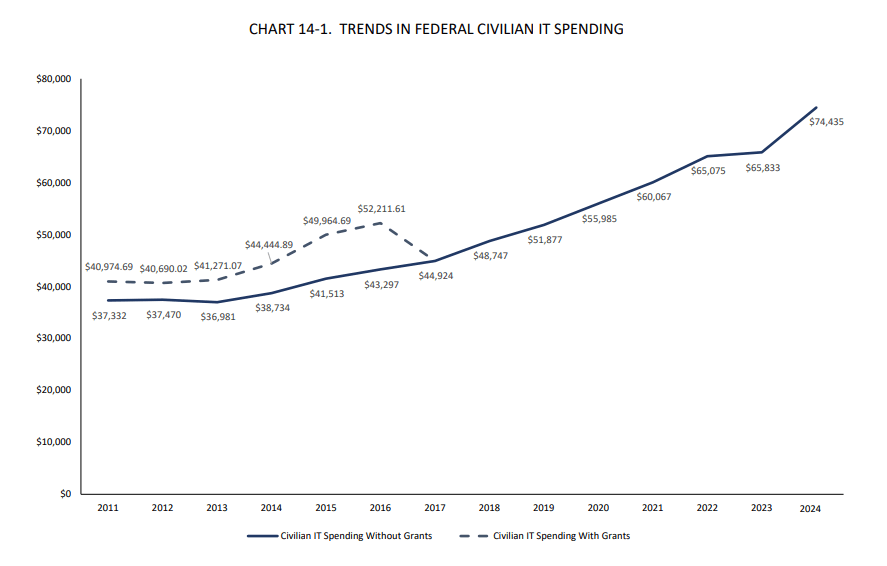

For the Application Software business, Roper has quite diversified end markets including law firms, K-12 education centers, government, hospitals, commodity producers, and insurance markets. For example, Deltek is providing software for government contractors, and it is one of the key businesses within the Application Software segment. Booz Allen Hamilton Holding Corporation (BAH), a leading IT contractor for the government sector, is guiding 14%-15% revenue growth for FY24, as disclosed in their latest earnings. The robust growth indicates a strong IT spending trend at the federal government level. According to the White House, the federal civilian IT spending is expected to increase from $65.8 billion in 2023 to $74.4 billion in 2024, as shown in the chart below. Therefore, the government end-market will remain strong in FY24, in my view.

White House

The outlook for freight matching business might be reasonable, and I will discuss more in the risk section. Overall, I think Roper's end-market is quite diversified and stable in FY24, and I don't expect there to be any material changes in the new fiscal year.

With a strong portfolio transformation towards more SaaS vertical software, Roper is likely to sustain their 8%-9% organic revenue growth in the near future, as discussed previously. The growth forecast assumes 3%-4% pricing growth as the company offers vertical software in niche markets and possesses strong pricing power over their customers, as evidenced by their historical results.

Most of their software is mission-critical to their customers; therefore, an annual price adjustment of 3%-4% in their software subscription fee is quite reasonable, in my opinion.

Therefore, I assume 8% organic revenue growth in the model. Assuming the company allocates 20% of total revenue towards M&A, the acquisitions would contribute 3.7% growth to the topline. Over the decade, Roper has generated an average of 5.7% acquisition growth; therefore, my assumption is quite conservative in the model.

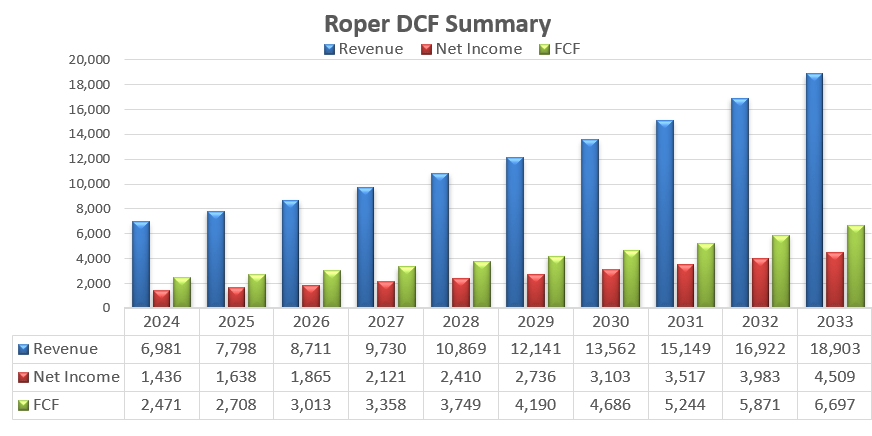

Roper's margin expansion is driven by the increasing revenue mix of high-margin vertical SaaS software. More specifically, their gross margin has expanded from 59.4% in FY14 to today's 69.7%. Thanks to their strong M&A pipelines and strategic focus on vertical software, I anticipate their gross margin expansion will continue in the future. In the model, I assume a 20bps gross margin improvement and 10bps margin expansion due to efficiency improvements from SG&A. Therefore, according to my calculation, the operating expenses will grow by 11% YoY, resulting in a 30bps margin expansion annually in the model. Based on these parameters, I have projected revenue, net income and FCF for the next ten years below.

Roper Technologies DCF - Author's Calculation

I calculate their free cash flow to equity (FCFE) by adjusting their net income, depreciation & amortization, change in working capital and net borrowings.

Roper Technologies DCF

The cost of equity is calculated to be 9.6% in the model, by assuming:

-risk-free rate: 4.32%, US 10-Y Treasury Yield

-Beta: 0.96, SA 24-month data

-Equity Market Risk Premium: 5.5%

Applying the cost of equity, the present value of all FCFE is estimated to be $67.9 billion, thus the one-year target price is calculated to be $633 per share in the model.

As discussed above, Roper has been actively seeking acquisitions; therefore, the company carries the risk of failed M&A integration. Additionally, for investors who are not comfortable with acquisitions, Roper may not be a good investment candidate. Roper does not repurchase any stocks. Though they pay some dividends, the majority of their free cash flow is used for M&A. Having said that, Roper has a longstanding track record of successful M&A executions.

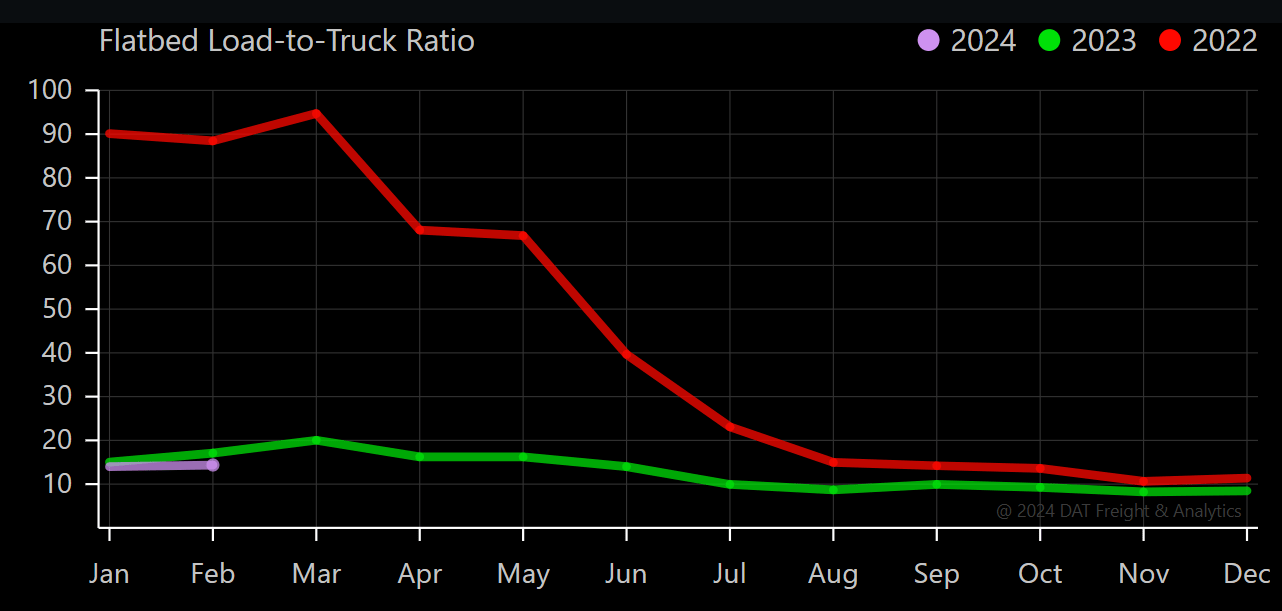

Roper owns both DAT and Loadlink businesses, both cater to serve the freight market by providing electronic marketplace connecting trucks in North America. DAT is providing DAT ONE subscription services to logistic carriers, enabling them to manage their freight loads and conduct data analysis. Loadlink provides similar services as well. Logistic carriers/brokers and other long-haul operators can subscribe to these services and pay the fee on a monthly basis. While the business growth is not solely tied to the overall freight market, DAT/Loadlink may face higher churn rate, or may not be able to raise the subscription fees amid a weak freight market. In other words, the freight market has some indirect impacts on Roper's business growth.

The chart below illustrates the flatbed load-to-truck ratio, an indicator of the spot market demand and capacity balance. The freight market was quite strong in 2022 due to increased consumer spending on physical goods, then the market began to normalize in 2023, as depicted in the chart. Given the current high interest rate, I don't expect a material recovery in consumer spending on physical goods in 2024. As such, I anticipate Roper's DAT and Loadlink will deliver a weak growth in FY24.

DAT Website

Furthermore, Roper's products/software are widely used in various niche end-markets, and most of their competitors are small regional players. It would be impossible to track their competitors. However, in most vertical markets, Roper holds the leading position, and their M&A preference is to acquire software leaders in niche markets.

After years of portfolio transformation, Roper Technologies has emerged as a defensive software company in niche markets. Despite consistently delivering double-digit earnings growth, the stock often remains under-covered by investors. I reiterate the 'Buy' rating on Roper with a one-year target price of $633 per share.