babyrhino

babyrhino

I last covered Roivant Sciences Ltd. (NASDAQ:ROIV) in a note for Seeking Alpha back in May last year, giving the company a buy recommendation, based on an intriguing and differentiated drug development pipeline targeting multi-billion dollar indications, with multiple significant data catalysts in play.

10 months on, Roivant stock has made a slight gain of ~10%, and shown minimal volatility, despite some significant developments at the company. I covered Roivant's business model in my last note, but as a reminder, it is focused on "accelerating the development and commercialization of medicines that matter," according to its latest quarterly report / fiscal Q3 2023 10Q submission, which also explains:

We advance our pipeline by creating nimble subsidiaries or "Vants" to develop and commercialize our medicines and technologies. Beyond therapeutics, Roivant also incubates discovery-stage companies and health technology startups complementary to its biopharmaceutical business.

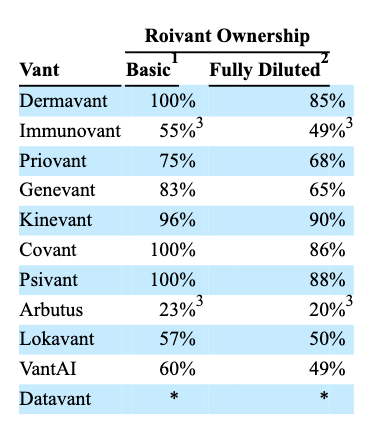

Roivant subsidiaries as of fiscal Q323 (10Q submission)

The above table - taken from Roivant's latest 10Q - covers all of the various "Vants," and eagle-eyed readers will notice there are three less Vants than when I last shared this table in my last note, 10 months ago.

Proteovant, focused on cutting-edge "protein degradation" science and technology, has been sold to SK Biopharmaceuticals in exchange for $47.5m. Hemavant is no more, after its lead candidate, RVT-2001, an SF3B1 modulator indicated for transfusion-dependent anemia for low-risk MDS patients, missed endpoints in a Phase 1/2 clinical study, and in the words of Roivant's CEO, Matt Gline, speaking on the Q3 earnings call, "did not meet our bar for progress."

Affivant is no longer mentioned in the latest quarterly report, although AFVT-2101, a preclinical candidate being developed to treat solid tumor cancers, being a "tetravalent bispecific antibody" binding to CD16A and FRα is mentioned as a pipeline asset on the website of Affimed N.V. (AFMD), a <$100m market cap biotech based in Heidelberg, Germany.

VantAI is an intriguing new addition that "uses machine learning to build computational models to generate new molecular entities for targets of interest", and is part-owned by SK Biopharmaceuticals. The biggest change at Roivant, however, undoubtedly relates to RVT-3101-Vant, since renamed Telavant.

RVT-3101 is an anti-TL1A antibody in development for ulcerative colitis ("UC") and Crohn's disease, that Roivant was developing alongside Pfizer Inc. (PFE), who out-licensed the asset to the company. As I wrote in May last year:

The consensus among some market watchers is that Roivant made an excellent deal by securing development rights for RVT-1301, which has demonstrated a safety and efficacy profile that looks approvable in markets that offer double-digit billion revenue opportunities for a best-in-class performer.

Recently, the Pharma giant Merck & Co., Inc. (MRK) acquired Prometheus Biosciences in a deal worth $10.8bn in order to gain access to its lead candidate PRA023, which has a similar mechanism of action ("MoA") to RVT-1301. It seems incredible that while Merck is paying double-digit billions to gain access to one TL1A inhibitor, Pfizer is almost giving one away to its partner!

In October last year, the Swiss Pharma giant Roche Holding AG (OTCQX:RHHBY), completed the acquisition of Telavant for a payment of $7.1bn upfront, plus a $150m milestone payment.

The deal seems to confirm that Roivant did indeed make an excellent deal with Pfizer, who retains rights to develop, market, and sell the drug outside of the U.S. and Japan.

Data from RVT-3101's TUSCANY-2 study showed 36% clinical remission at 56 weeks, and endoscopic improvement of 50%, leading Roche CEO Teresa Graham to comment that "we strongly believe in the first-in-class and best-in-disease potential of this late-stage antibody to treat people living with Inflammatory Bowel Syndrome ("IBD")".

With the deal completed, Roivant was able to report a cash position of $6.7bn as of fiscal Q3 2023, versus total liabilities of $245m.

Across the first nine months of 2023, Roivant reported $56m of product revenues, $40m of license and milestone revenue, R&D expenses of $381m, SG&A expense of $518m, and $5.35bn gain on the sale of Televant, resulting in net income of $4.5bn, versus a loss of $(941m) in the prior year period.

For a company whose market cap valuation is $8bn at the time of writing, with shares trading at a value of ~$10 - more or less the exact same price they traded at when Roivant joined the Nasdaq via a merger with the Special Purpose Acquisition Company ("SPAC") Montes Archimedes Acquisition Corp back in May 2021 - we could certainly make the argument that Roivant is somewhat undervalued, but ultimately, it all depends on how Roivant deploys its cash.

In its latest earnings presentation, Roivant compares its R&D productivity with that of "the top global pharma companies," given its seven Phase 2 & 3 data readouts this year, but also points out that its R&D spending of $0.6bn is a fraction of what the "Big Pharma" sector spends.

The implication is presumably that Roivant is more efficient compared to its Big Pharma rivals, but while that may be the case, Roivant has only secured a single commercial approval - for its Vtama cream to treat psoriasis - which earned only $21m of revenues in Q3 2023 - to date, hence, comparisons with the "Big Pharma" are some way wide of the mark.

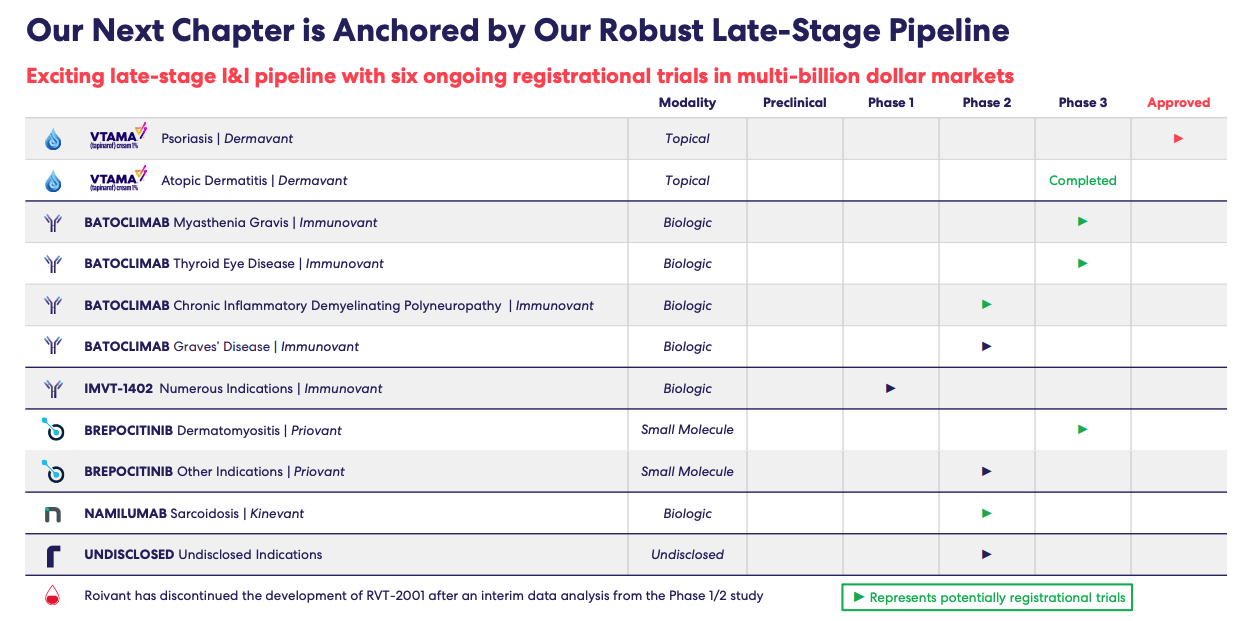

Nevertheless, Roivant's pipeline, shown below, has several assets that may one day generate revenues in the billions of dollars.

Roivant pipeline (Roivant corporate presentation)

Beginning with Vtama, the topical cream to treat psoriasis appears to be a strong proposition, although the product is yet to take off commercially, and slow sales to date have prompted some Wall Street analysts to cut peak revenue expectations from ~$1.4bn to just ~$400m.

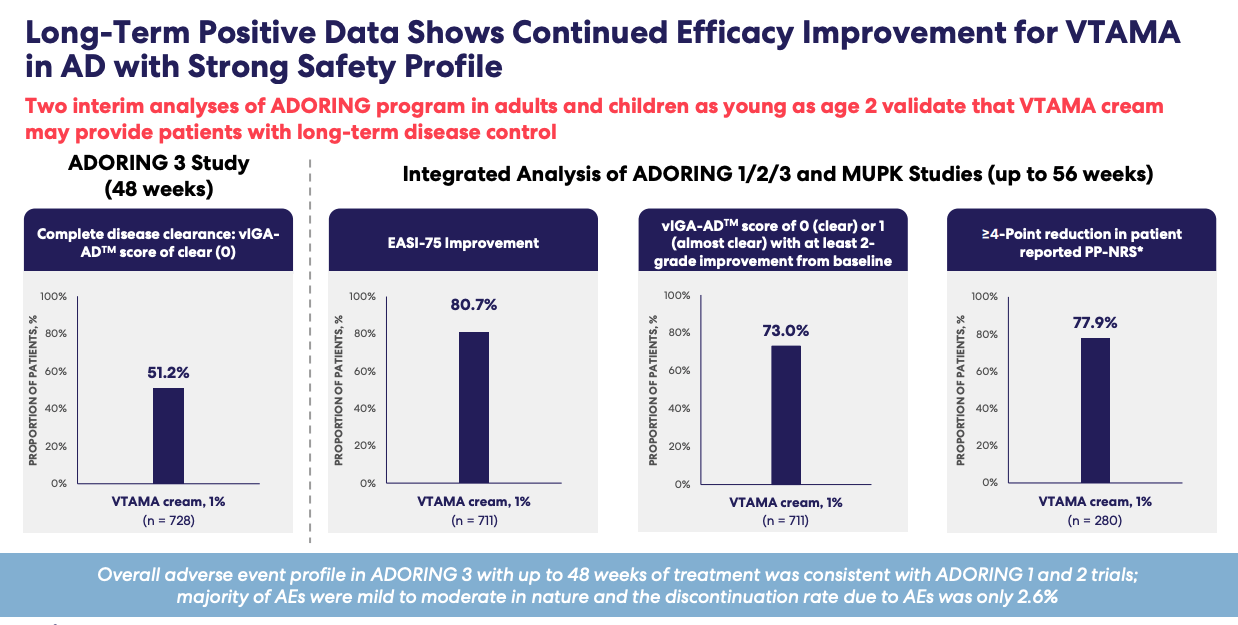

On the plus side, Roivant expects to submit its supplemental New Drug Application ("sNDA") for VTAMA in atopic dermatitis ("AD") this quarter, and from an efficacy and safety perspective, the product looks to be competitive, able to offer long-term disease control to patients, as we can see below based on results ADORING Phase 3 studies.

VTAMA long-term efficacy / safety data (earnings presentation)

An approval in AD would substantially increase VTAMA's addressable market, from a 100k prescription market, to a ~450k prescription market, Roivant estimates - a fourfold increase, which could persuade analysts to revise their peak sales estimates again, although Roivant faces intense competition in both the AD space, and the topical creams space.

For example, AbbVie Inc.'s (ABBV) Rinvoq, Sanofi's (SNY) Dupixent, and Pfizer's Cibinqo all have multi-billion dollar peak revenue expectations in this indication, and are of critical importance to their 'Big Pharma" owners, who have substantial marketing budgets to deploy.

There are at least two other topical creams - Incyte Corporation's (INCY) Opzelura, and Arcutis Biotherapeutics, Inc. (ARQT) Zoryve - so far approved in psoriasis only, presenting still more obstacles to Vtama's success, and there is a cautionary tale in Pfizer's Eucrisa cream, which had peak sales expectations of >$2bn when launched in 2016, but never lived up to the hype, earning ~$140m of revenues in 2019.

Nevertheless, Arcutis' share price has been on the rise (up >65% since my "buy" recommendation in a note on the company in January), and although progress has been slow, I still feel relatively optimistic that more recently launched topical creams - which have a far superior safety and efficacy profile to Eucrisa - can be successful long-term.

Perhaps VTAMA will never become a "blockbuster" drug for Roivant, but I don't think >$500m per annum is out of reach, and that could even be enough to prompt a "Big Pharma" company to make a multi-billion takeover bid for Dermavant, the subsidiary responsible for the drug.

Meanwhile, Batoclimab is edging closer to a formal approval shot, it seems, in the not inconsiderable indications of myasthenia gravis and thyroid eye disease ("TED"), where Horizon Therapeutics' drug Tepezza is driving >$2bn revenues per annum - Horizon is in the process of being acquired by Amgen Inc. (AMGN) in a >$25bn deal.

The drug is a member of the FcRn inhibitor class, which has the market excited, given its ability to counteract Immunoglobulin G, whose over-production is common to several auto-immune diseases.

In 2024, Roivant will share Phase 2b clinical study data for batoclimab in chronic inflammatory demyelinating polyneuropathy, as well as Phase 3 data for Myasthenia Gravis, and TED.

argenx SE's (ARGX) efgartigimod, an anti-FcRn drug which has secured approval in generalized myasthenia gravis and is marketed and sold as Vyvgart, earned $1.2bn in 2023, and analysts have suggested it could secure peak revenues >$8bn across all target indications, which includes TED.

Similarly to the topical cream markets, this is both good and bad news for Roivant, in my view. Good, because if batoclimab is as good a drug as efgartigimod, "blockbuster" (>$1bn per annum) revenues ought to be inevitable.

Bad because a crowded field, which also includes UCB's Rystiggo, approved in MG last year, and Johnson & Johnson's (JNJ) nipocalimab, makes competing for market share tough, although some research, at least, suggests batoclimab may be the most efficacious drug, and again, I would not rule out a multi-billion dollar M&A bid for the drug.

Roivant is also developing a next-generation FcRn inhibitor, IMVT-1401, which was discussed as follows by CEO Gline on the most recent earnings call with analysts:

we are very excited about the next-generation antibody there, IMVT-1402, which we think offers deep IgG lowering, similar to batoclimab, we think as deep as any anti-FcRn antibody that we are aware of, with a clean analyte profile, with no and minimal effect on albumin and LDL, formulated for a simple subcutaneous injection, designed to hopefully enable self-administration, with an auto-injector and with patent life that goes out on a competition of matter basis, not excluding PTEs until 2043. So, a tremendously exciting drug.

The final Phase 3 stage asset in Roivant's pipeline is brepocitinib, which will read out data from a "proof-of-concept" study in non-infectious uveitis imminently, and share Phase 3 dermatomyositis data next year. Uveitis is an eye disease that can cause blindness, and brepocitinib could become the first oral drug to be approved to treat the condition.

Brepocitinib flunked a study in systemic lupus erythematosus ("SLE") last year, one of its target indications, although management has suggested this was down to an unexpectedly strong placebo response in the study. The drug has dual targets, in TYK2 and JAK1, both recognised targets in numerous autoimmune conditions.

Once again, that means competition for best-in-class data is fierce, and I would potentially rate brepocitinib as a longer shot for success than the FcRn inhibitor franchise, although were the uveitis study to bear fruit, I would expect the market to respond very positively, given the drug's preferable oral administration (versus injectables).

The short answer to this question is that I do continue to rate Roivant stock as a buy.

In my view, the biggest criticism you could level at the company is that, arguably, it is more hedge fund than biotech. By that I mean, the company has been designed to make strategic investments into areas of drug development that have been pioneered by researchers and scientists at other companies, or academic institutions, and to try to develop better drugs through strong financial stewardship and, essentially, a gut feeling for what might work best.

To put it another way, Roivant did not develop the science it is now investing in, therefore, it's possible it may lack the expertise to develop "best-in-class" drugs. This is a potential concern, however, the reality is that Roivant's business model is working.

To date the company's dealmaking has proven to be extremely astute. Management's partner selection, which resulted in the Pfizer collaboration that produced RVT-3101, to which Roche paid >$7bn to acquire US and Japan rights to, is a perfect example, and I don't believe the market has given Roivant enough credit for this.

The drugs in Roivant's pipeline may be a mixed bag, and the company has discontinued the development of one significant asset, RVT-2001, and sold off other "Vants" for less than it may have hoped for, but in my view, the FcRn franchise looks to have genuine potential, the long term commercial prospects for Vtama may, in fact, be more encouraging than the market believes at the present time, brepocitinib could still spring a surprise in its various indications, and perhaps most importantly, the company has a >$6.5bn war chest to do what it does best - hunt for drug candidates with future "blockbuster" revenue potential.

After its original founder, Vivek Ramaswamy, switched from drug development, to politics, funding a tilt at becoming the next U.S. President, the appointment of CEO Gline, a Harvard-educated former investment banker, meant Roivant is unlikely to change its strategy any time soon.

For my money, that is good news because the business model has proven to be successful so far. Even if VTAMA, batoclimab, and brepocitinib all fail, either in the clinic or commercially, the company will still have a cash position nearly as large as its current market cap, and in fact, the company's approach to the development of its pipeline, from a scientific perspective, seems quite robust.

As such, Roivant continues to strike me as a relatively straightforward "Buy" opportunity. Although there has not been much movement around the share price, even after the sale of televant, with multiple late-stage data readouts arriving this year, and next, and with Vtama expected to secure an approval that quadruples its addressable market, my suspicion is the market will not be ignoring the upside potential in Roivant's share price for much longer.