pxhidalgo/iStock via Getty Images

pxhidalgo/iStock via Getty Images

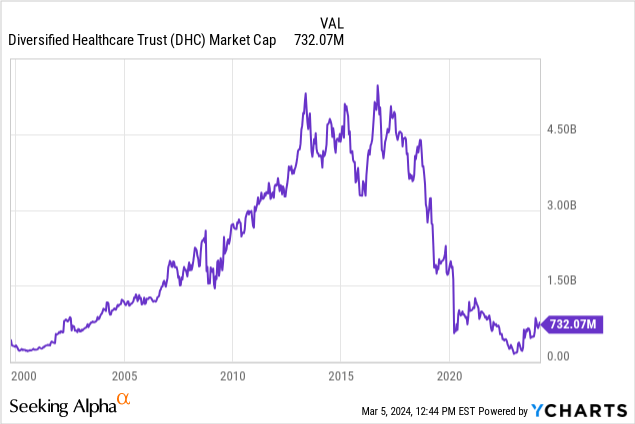

On our previous coverage of Diversified Healthcare Trust (NASDAQ:DHC), we rejected the idea that the stock was worth anywhere close to $9.00. This was contrary to speculation by Flat Footed LLC, which had established a large position based on that belief.

This default flies in the face of the $9.00 NAV as suggested by Flat Footed LLC. Some investors may reject this NAV drop, but this is about what we have seen for many REITs.

Source: Seeking Alpha.

We suggested that bullish investors buy the February 2028 bonds at 75 cents or better as those offered the best relative setup amongst bonds and equity. We examine the key developments since then and update our view on related securities.

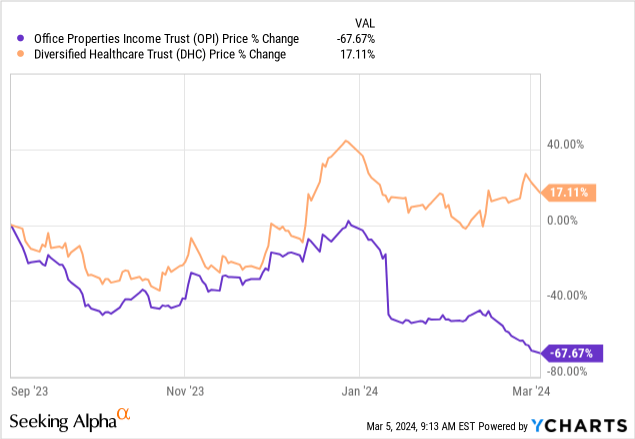

In a remarkable victory for activism, DHC's merger with Office Properties Income Trust (OPI) was called off. This merger was the brainchild of The RMR Group Inc. (RMR), which manages both. In an even greater vindication of the logic behind terminating the merger, OPI has underperformed DHC by a whopping 85% since then.

Investors might recall that the original argument was that DHC needed OPI to survive.

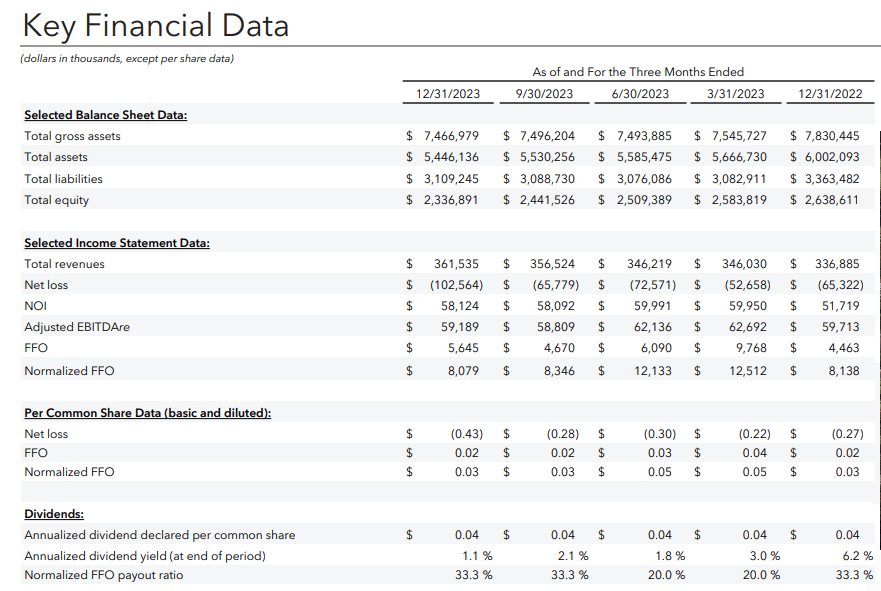

DHC's Q4 2023 results were showcased with the slide showing the massive improvement in SHOP net operating income (NOI). Year-over-year, this segment was up 168.9%. Consolidated NOI was not too shabby, either, with a 26.8% gain.

DHC Q4-2023 Presentation

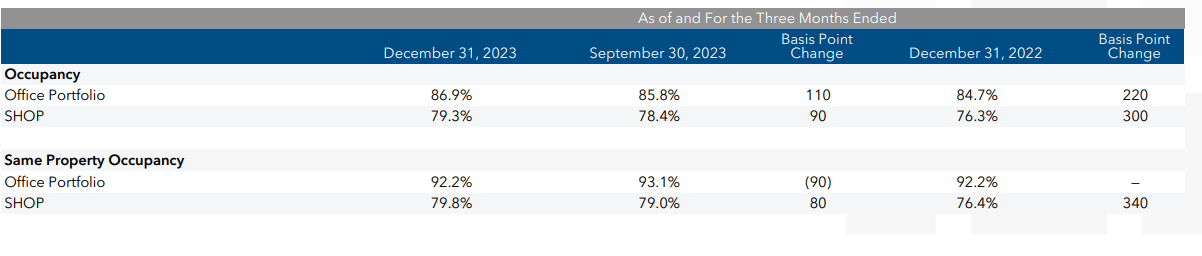

The company showed occupancy gains in the medical office portfolio as well as in SHOP. You also saw some small gains in overall occupancy quarter-over-quarter.

DHC Q4-2023 Presentation

When examining the key financial data, one thing stood out. DHC is translating very little NOI into funds from operations (FFO). In Q4 2023 NOI was $58.12 million and FFO was just $5.6 million ($8.0 million if you use the more generous normalized version).

DHC Q4-2023 Presentation

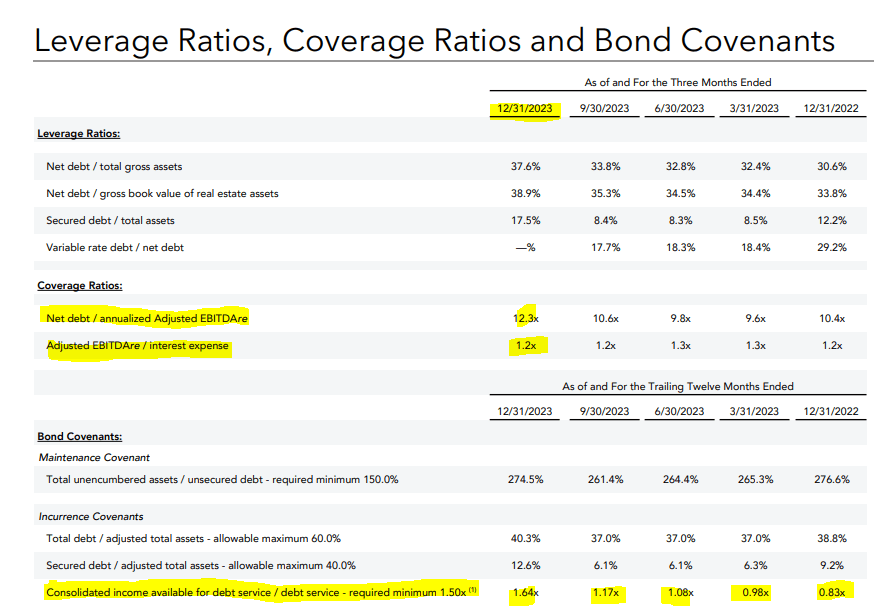

So, as blockbuster as those results looked at the NOI level, let us not forget why DHC is trading at these levels. Net debt to Adjusted EBITDA was at 12.3X and interest coverage was at 1.2X. Their official debt service ratio which uses a slightly different metric was at 1.64X.

DHC Q4-2023 Presentation

But there is no denying that is a levered structure and the leverage levels have actually become worse since last year (10.4X debt to EBITDA).

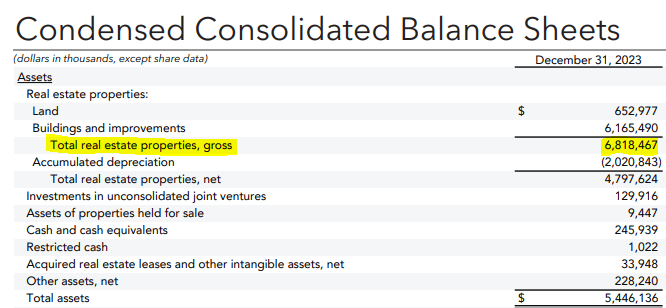

On last check, there were over $6.8 billion in gross assets on the balance sheet.

DHC Q4-2023 Presentation

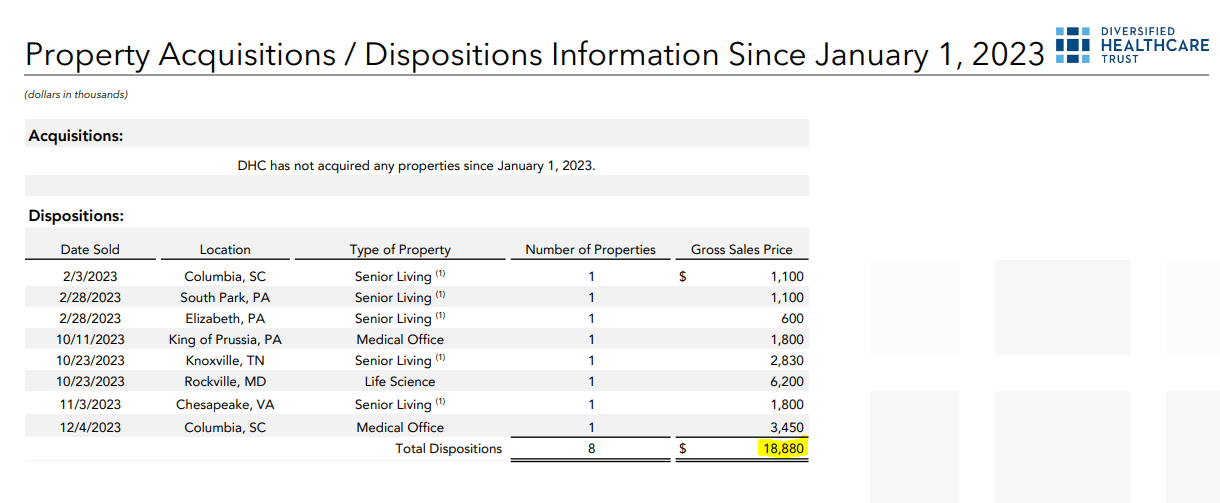

Gross here refers to before depreciation and does not in any way hint at their quality. So with $6.8 billion of assets or even $4.8 billion if you believe real estate depreciates over time (really should not), what do you think DHC's asset sale figure was? Would you believe $18.88 million for all of 2023?

DHC Q4-2023 Presentation

That was an awful number, and made even more awful by how much DHC spent on improving its existing properties.

During 2023, we invested $183 million of maintenance and value-enhancing capital across our SHOP communities, which included cosmetic or full renovations at nearly 65 communities. These investments, coupled with operational improvements that the community serve as a platform to drive performance.

We expect to continue with improvements across our communities into 2024 with roughly 25 refresh projects currently underway, specifically targeted in communities where we expect improvement to enable higher rents and occupancy.

Source: DHC Q4 2023 Conference Call Transcript.

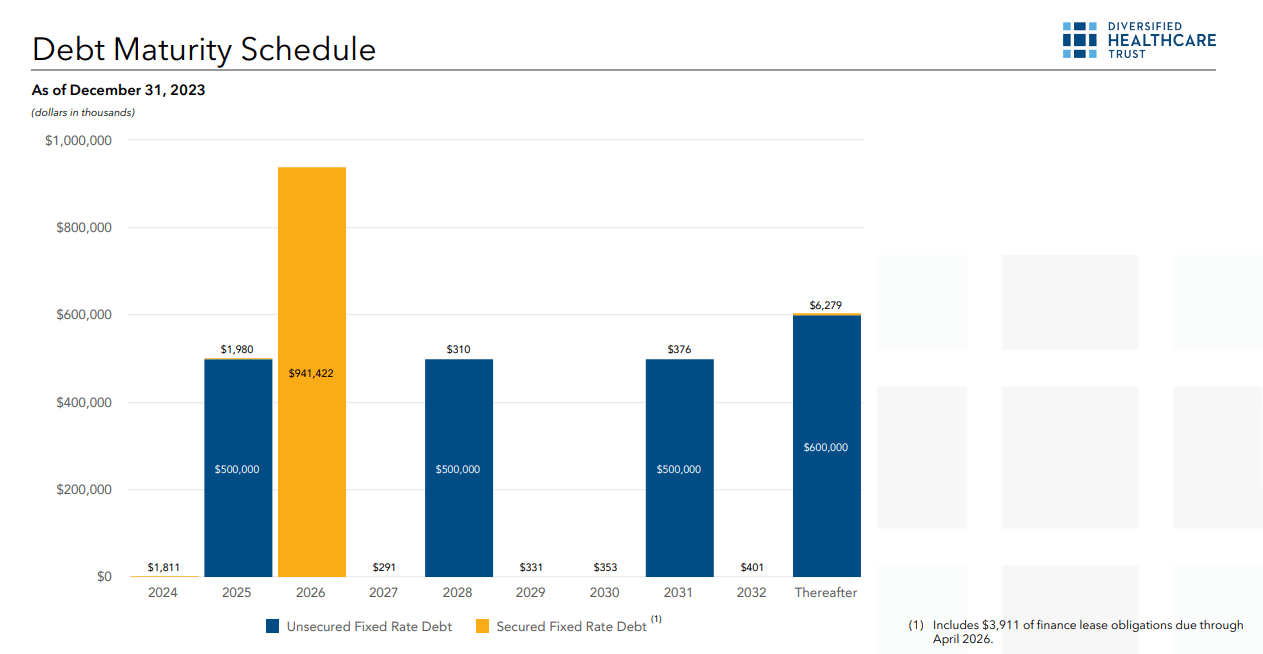

This all is very relevant considering that DHC was flirting quite liberally with a "going concern" notice. It has since withdrawn that as it addressed its liquidity via an expensive "zero coupon" note.

Issued $940.5 million of zero coupon senior secured notes due January 2026, with a one-year extension option. Net proceeds, after deducting initial purchaser discounts and estimated offering costs, of approximately $730.4 million were used to repay and terminate DHC's then $450.0 million secured credit facility and to redeem $250.0 million of its senior notes that were scheduled to mature in May 2024. As a result, DHC is in compliance with all of its debt covenants and has no significant debt maturities until June 2025. DHC has concluded that the conditions that created the substantial doubt about its ability to continue as a going concern have been alleviated as a result of the financing activities described above and that no substantial doubt about its ability to continue as a going concern exists as of the date of issuance of DHC's financial statements, February 26, 2024.

Source: DHC Q4 2023 Presentation.

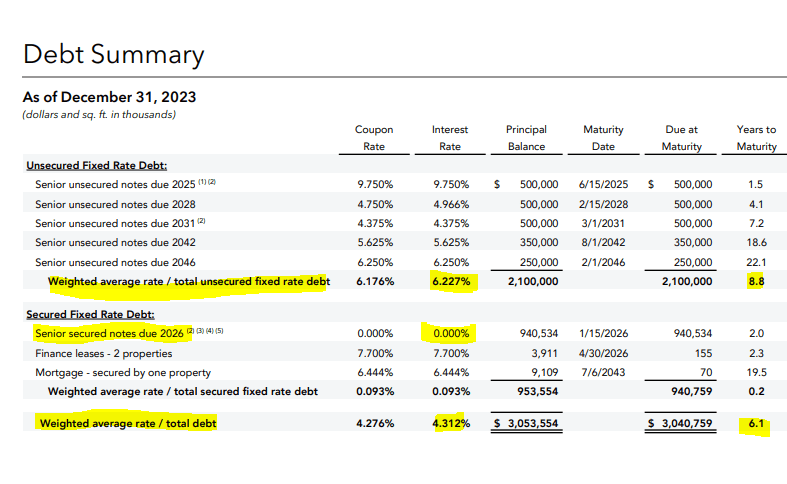

Those are two year notes sold at a 22.4% discount to face value, so no Brownie points for calculating the interest rate on that. With that done, you have $500 million coming due in June 2025 and the note in question the year after that.

DHC Q4-2023 Presentation

Market is very clear in its belief that the 2025 notes are ok and they are actually trading at par currently. So, the near-term stress is gone.

The weighted average interest rate on the debt is currently at 4.312%. This of course involves the beautiful sleight of hand positioning of the senior secured notes with a "zero coupon," even though they are actually paying through their nose for that one.

DHC Q4-2023 Presentation

Realistically with their credit rating, one going concern warning and 12.4X debt to EBITDA, they would have a hard time refinancing that entire stack at 8% even in a ZIRP era. Of course, the counterargument is that the assets are worth more than the debt. That is certainly possible considering there are close to $7.0 billion in gross assets and $3.0 billion in debt. But at a minimum to be convinced about that, DHC needs to sell $0.5 billion every year, and not the $18.8 million they actually did in 2023. So far, nothing that even appears remotely like urgency from the company on this front.

Currently, we are marketing for sale on additional 9 non-core properties, mostly within our office portfolio with estimated sales proceeds of $60 million to $70 million. However, we are in the early innings with respect to the demand outlook from buyers and overall execution of these sales.

Source: DHC Q4-2023 Conference Call Transcript.

While Diversified Healthcare Trust equity could have upside, considering the market cap is a fraction of the difference between gross assets and net debt, we are still reluctant to pitch for that.

Last time around, we had made a case for the 2028 bonds, and they have appreciated slightly, and you have modest total returns. We don't think those have the same merit at present, and we are hesitant to back them considering the CRE climate. Diversified Healthcare Trust NT 42 (NASDAQ:DHCNI) bonds currently yield 9.1% and are trading at a price of 59 cents on the dollar ($14.75 on $25 par value). Diversified Healthcare Trust 6.25% SR NT 46 (NASDAQ:DHCNL) are trading slightly higher on account of their higher coupon ($15.84 on $25 par value). The closest regular bonds we have are trading at $76.47 and yield 8.95% to maturity. That is yield to maturity and the current yield on those is just 5.72%.

Even if you assume that Diversified Healthcare Trust has no chance of making it to 2042 or even 2031, the baby bonds actually make more sense than the regular bonds. We are staying out of all of these as we don't like the risk-reward setup at present. But if we had to buy one, we would go with DHCNI.