silvestra

silvestra

Co-authored with “Hidden Opportunities.”

In the era of digital finance, where access to markets is simplified and commission-free, the average investor has embraced a short-term mindset: Buy, Sell, Repeat! This mantra echoes from Main Street to Wall Street, but it's not my game plan. While some thrive on the adrenaline of short-term trading, my focus lies elsewhere. I aim to harness the market's potential for passive income with minimal day-to-day involvement.

In a conversation with a group of financial analysts, one of them raised a question asking if I was recommending any cash position at all, given our economy is headed into a recession. I answered:

"As income investors, we always have cash. Our portfolio produces a lot of cash every month that we can use as we see fit. If implemented correctly the Income Method produces cash infusions in excess of your requirements allowing room for opportunistic reinvestments. Why would we need to accumulate something that is reliably being produced in quantities more than we need?"

As an income-focused investor, the best thing that can happen to you is that you find an investment that pays you regularly, and you never have to sell a piece of it to generate usable profits. As the Oracle of Omaha says – if you find a great business, just hang on for dear life.

While others are focused on storing a reservoir of cash, I focus on strengthening my river of cash. Instead of cash sitting there, doing nothing, my cash is at work producing even more cash, creating a constant flow that replenishes itself.

Now, let's delve into two securities worth holding onto indefinitely.

BDCs (Business Development Companies) serve the rather underserved middle market companies by providing them with much-needed capital to grow or survive amidst challenging economic situations. Investors often assume that BDCs only thrive when interest rates are elevated, but that is not true.

A BDC’s performance is largely influenced by how well management assembles its portfolio of borrowers and the spread between lending and borrowing costs. And blue-chip BDCs benefit from their larger scale and deeper experience in navigating such conditions. We examine Ares Capital Corporation (ARCC), the largest and time-tested public BDC with a $21.9 billion asset portfolio. It is important to remember that when rates were near-zero, it wasn't like every company out there was able to enjoy those cheap borrowing costs. Notably, at the end of FY 2021, ARCC reported its weighted average yield on debt and other income-producing securities as 8.7%

Blue-chip BDCs like ARCC stand to benefit from the rising demand for non-bank capital through their affiliations with deep-pocket investment manager platforms as competition for new deals increases.

ARCC is much better diversified today compared to the pre-pandemic period, with 505 portfolio companies and an average position size of 0.2%. The average LTV of ARCC’s loans was 43% at the end of Q4, and all new investments originated in the fiscal year carried a low LTV of 33%.

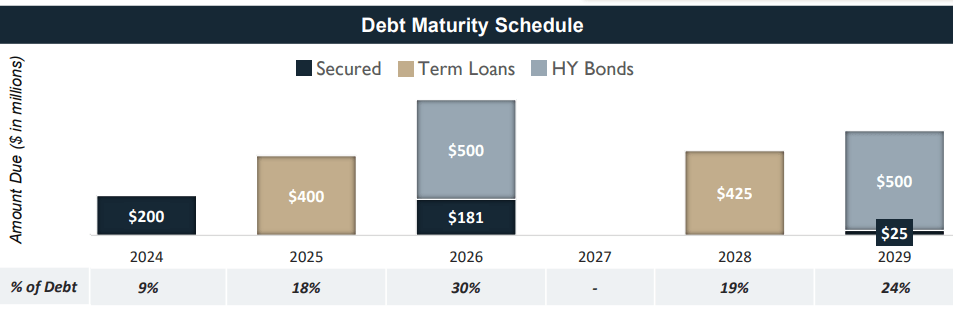

87% of ARCC’s portfolio comprised senior secured loans, and the BDC ended FY 2023 with non-accruals at only 1.3% of amortized cost and 0.6% of fair value: The BDC maintains investment grade ‘BBB’ ratings, with adequate liquidity and well-laddered maturities, positioning it well for a prolonged period of higher rates or a slowing economy. It is worth noting that ARCC has managed to produce these results while operating at a net leverage ratio of just 1.02x debt to equity. Typically, ARCC operates closer to 1.2x debt/equity so it has a lot of room to leverage up. In January, ARCC also proved that it can issue debt at reasonable prices, issuing $1 billion in 5-year Notes at 5.875%.

ARCC maintains 14+ years of stable to increasing dividends, adequately covered by the BDC’s prudent operations. The $2.37/share core EPS for FY 2023 places the BDC’s dividend at a comfortable 81% payout ratio.

ARCC is coming into 2024 from a position of strength, with low leverage, high liquidity, few credit problems in its portfolio, and positive momentum. The Blue-Chip BDC currently yields 9.5%, and its deep diversification and high-quality management make it an excellent long-term investment toward growing income.

While air travel demand in 2023 zoomed past pre-pandemic levels, the same cannot be said about the domestic lodging industry. The domestic hotel industry has not yet recovered to 2019 levels due to two broad themes:

"Revenge travel" from 2022 shifted internationally in 2023, with Americans keen to vacation outside the country, leading to greater demand in Europe and Asia.

Tourism into the U.S. from other countries was negatively impacted due to massive backlogs and over 500-day wait times for residents of several nations to have their visa interviews. The long delays are dissuading travelers, who simply choose other destinations.

Despite a slower recovery vs pre-pandemic levels, quality hotel operators still demonstrated YoY improvement in operating metrics. RLJ Lodging Trust (RLJ) is one of the largest public lodging REITs, owning and operating a portfolio of 96 hotels with ~21,300 rooms located in 23 states. RLJ owns premium-branded hotels in markets with multiple demand generators, with a property base operating under popular global brands – Marriott, IGH, Hilton, Hyatt, Choice, and Wyndham. Source.

RLJ Lodging Trust

RLJ’s performance metrics showed considerable improvements YoY. The hotel REIT reported 71.8% occupancy for FY 2023 (up 4.2% YoY) with the ADR (Average Daily Rate) at $196.77 (up from $188.21 in FY 2022) and Revenue per Available Room (RevPAR) was up 9% at $141.24 (up from $129.61 last year). RLJ’s Q3 RevPAR was 2x that of the industry, reaching 98% of 2019 levels, and Q4 was 4x the peer group, indicating that the REIT is firing on all cylinders.

"Our results this quarter exceeded our expectations and capped off a very successful year for RLJ where we achieved top quartile RevPAR growth of 9%, driven by our urban portfolio and strong performance from our conversions. Our RevPAR grew by 5.2% over the prior year, outperforming the industry by 4x and our competitive set by 290 basis points." - Leslie Hale, CEO, Q4 2023 earnings call.

Business demand growth led to RLJ’s urban markets RevPAR showing a 5.2% YoY increase. These markets also benefited from healthy urban leisure trends due to the return of large-scale events like college football, conferences, and other events, leading to improved domestic and inbound international demand.

For FY 2023, RLJ reported comparable hotel EBITDA of $401.4 million, and adjusted funds from operations ("AFFO") per share between $1.66/share. Quarterly results do reflect normal seasonality, but RLJ saw business travel reach 79% of 2019 levels, and leisure travel in several markets ended either close to or above pre-pandemic demand.

RLJ raised its common dividend by 25% during Q3, and the company’s projected FFO for FY 2023 places the annualized new dividend at a modest 24% payout ratio, an unbelievably low number for a REIT. Management revealed that there is room for payout growth this year and in upcoming years towards the target payout ratio between 60-65%. During Q4, RLJ also repurchased $9.9 million of common shares, bringing the total shares repurchased in FY 2023 to $77.2 million. After these purchases, the company has ~$170 million available in its authorized share repurchase program.

RLJ has staggered debt maturities, with $200 million maturing in 2024, which is comfortably covered by the company’s $516 million cash position. Source.

Q4 Investor Presentation

$1.95 Series A Cumulative Convertible Perpetual Preferred Shares (RLJ.PR.A)

RLJ-A offers attractive perpetual income prospects. A growing common dividend and aggressive share buybacks provides an additional layer of safety to the investors of the cumulative preferred.

RLJ-A cannot be redeemed but conversion to common stock can be forced if RLJ common shares trade at or above $89.09 for 20 out of 30 trading days. As such, for the preferred to become convertible, the common stock would have to experience a rather unlikely 650% upside. We consider this highly unlikely, making RLJ-A a busted convertible that will pay dividends for the foreseeable future.

During FY 2023, RLJ spent $25.1 million on preferred dividends, which was adequately covered by the company’s $76.4 million net income. With growing common dividends, share buybacks, and improving operational metrics, RLJ-A is one of the rare preferreds that is a buy-and-hold forever.

Warren Buffett has famously advised the average investor to resist the emotional temptation created by Mr. Market, which often results in poor financial decisions.

"Mr. Market is there to serve you, not to guide you. It is his pocketbook, not his wisdom, that you will find useful. If he shows up some day in a particularly foolish mood, you are free to either ignore him or to take advantage of him, but it will be disastrous if you fall under his influence." – Warren Buffett.

While this isn’t as easy as it sounds, it certainly gets easier when the investment places a big juicy cash amount into your account every quarter. When you are tempted to sell in fear of volatility, you must consider the loss of income and the need to find a suitable replacement.

Our Investing Group adheres to a long-term approach to our holdings. With over 45 dividend-paying assets in our "model portfolio," targeting a +9% overall yield, we have numerous positions intended for perpetual ownership, ensuring a steady income stream for the foreseeable future. This exemplifies the beauty of the Income Method: a reliable infusion of cash, always at your disposal!