akinbostanci

akinbostanci

RLI Corp. (NYSE:RLI) delivered yet another strong quarter, challenged by some gradual business downsizing in the casualty space as well as by pretty large claims associated to wildfires and storms in 2023. RLI continues to be focused on discipline in underwriting, and it shows on the call, with them being relatively cautious in pushing in the property space despite higher rates due to some onset of less discipline by competitors. Expense ratios are also coming in a little high, but it's from discretionary investment and performance-based compensation, so we see there being an angle on lower expense ratios in the future when the former tapers out. In all, RLI is a dividend aristocrat and continues to prove its skill in working in more niche markets within insurance. However, we continue to note that substantial P/B ratios that define the company, far in excess of industry averages. We understand the confidence of investors, and don't think that the valuation standards would change for the company, but we do note that this is a darling, and as we've reiterated in our previous coverage of the ticker, it is already priced for excellence and perfection.

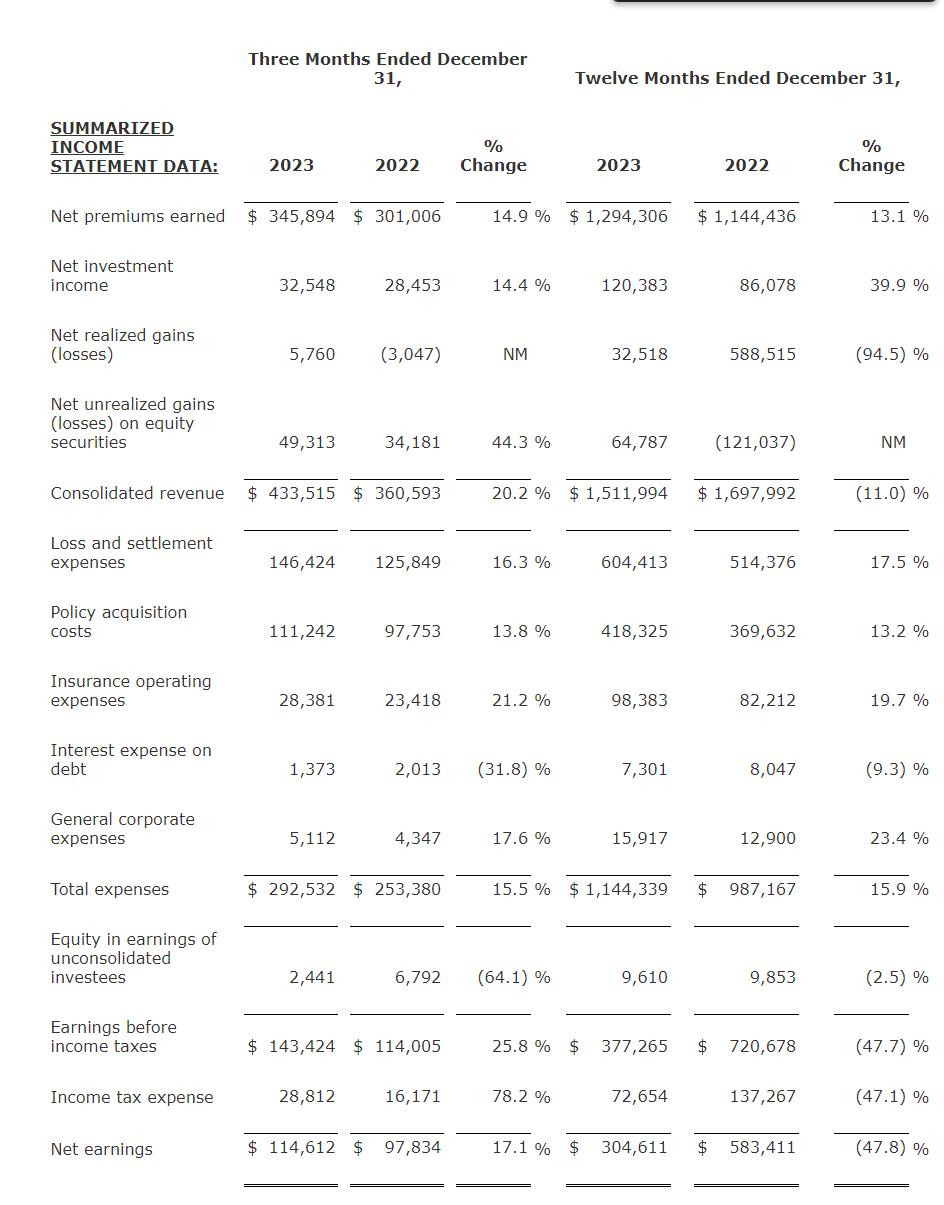

Let's start with just noticing that the Maui Jim profits from last year are seriously affecting comps on the investment side of the business in the net realised gains line item. Otherwise, the returns on the portfolio are strong and at 6.4%, consistent with a higher rate environment, with the higher prevailing rates being a continuous value driver for the industry.

IS (FY PR)

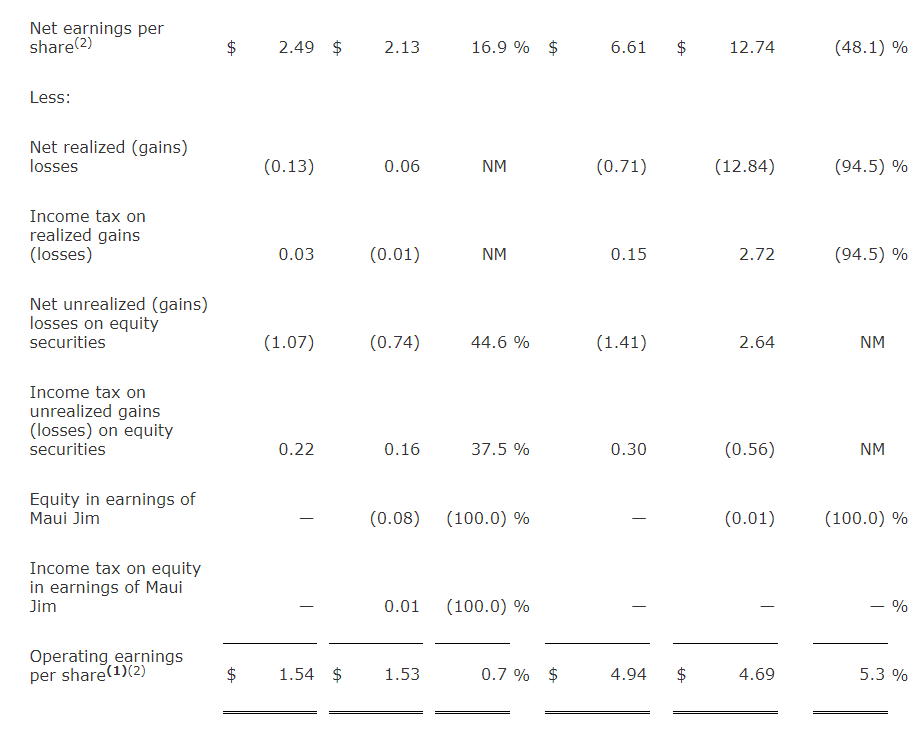

Looking at operating earnings which removes impacts on net income from the investing businesses, we can see how increases in net premiums earned (in all segments) has driven operating earnings up nicely for the FY, but less so for the last Q4 due to tough conditions in casualty despite still strong conditions in property and deceleration of corporate cost increases compared to the FY.

Operating Earnings Reco (FY PR)

Combined ratios did come up a little bit driven by all segments as favourable developments from reserve changes (affecting net premiums positively) weren't as great relative to this year's losses which included storms and wildfires. The increase was less in the Q4, where it would have mainly been driven by expense ratios and not loss ratios. On that point, we note that some of the general corporate expenses came up quite substantially, so expense ratios have been a big contributor to the combined ratio this year. The company has been calling out a 50% increase in technology investments being made by the company over the last couple of years.

Yeah. I think if you look at -- to Jen's point on the technology side, we probably have -- are up 50%-plus in the last couple of years, we're investing there...

The other component is the growth in net premiums is causing higher compensation expense. But the matter of technology investment is important to call out because it is discretionary and can eventually taper.

Let's start talking about the specific segments and trends in income from each. IBNR estimates are driving some of the loss ratios in casualty, but also a general mix shift and a wait to conduct rate increases to try generate some incremental income from the business. Some of the businesses are being dialed down in casualty, such as D&O, executive and energy casualty, where they are trying to get rate increases where possible but have to expect that irrationality in the industry is making it hard to underwrite new policies. For the Q4, combined ratios here were actually 99, which means underwriting profit is being really strained. So casualty is being a bit of a problem area. Transportation is doing well, but it's a tough business with a not so great industry structure, and quite a few large customers that determine the direction off the business. There is quite a lot of competition too to underwrite policies. We expect continued pressure here, but a positive development in rates to salvage the poorer trend in combined ratios can be expected. We also note that historically, combined ratios have come down nicely from these high levels following rate increases, it's possible that retrenchment and rate increases here will be followed by the industry and bring combined ratios back to the 85 level or so.

We have received regulatory approvals that we expect will accelerate rate increases into 2024.

Jen Klobnak, RLI COO

There are also mounting pressures in property too, particularly in hurricane, where after a tough season and major rate increases, limits are coming up and the market seems to be softening. Still, great underwriting profits highlighted by the property segment's 55 combined ratio (always seasonally lower, but lower than 62 in the Q4 2022) makes it an area that must be capitalised on, but the trend to a softening market is going to turn RLI off the business slightly going forward. Rate increases are really driving this business, including in E&S. In general, volumes are flat or actually declining. So they are focusing on getting the good deals rather than driving much deeper into the market. Competition is expected to continue to dial up and even accelerate into 2024, so we don't expect quite as strong a year next year for property, likely with deceleration as waning rate growth and slower rates of underwriting start to pull things down slowly.

Combined ratios are coming up for surety, although premiums continue to grow here and it is an investment area. But the company calls out the weaker financial conditions and is being careful, which is essential as they'll be on the hook for customers' financial issues. So they are in some cases not renewing accounts.

RLI continues to be an excellent company, but we are seeing limits starting to increase and competition to increase in some of RLI's rainmaking businesses. It's not a major concern, as RLI will simply underwrite more in less competitive areas, which is its M.O. It will continuously move its resources to underwrite more in businesses that are going to see stronger trends in combined ratios and rates. But we are seeing some peaking going on in some of its more attractive areas, as well as attrition of businesses in its more challenged areas, although awaiting some more rate increases. Financial conditions and financial deterioration are also concerns in surety, and concerns generally for the economy, particularly in light of maturity walls. As operating earnings are already decelerating into Q4, we don't expect the next FY to be as great for RLI, unless discretionary investments stop and help out the expense ratio.

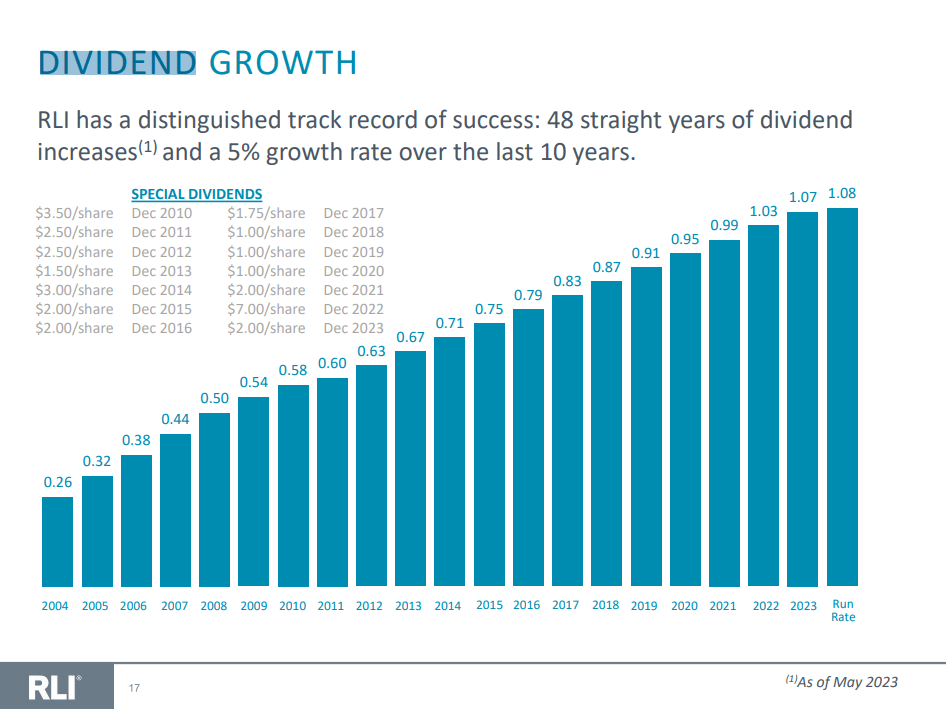

RLI trades at P/Bs above 4.3x, while the industry averages are around 2x. RLI definitely comes with a premium, and that is owed to its phenomenal track record and related dividend aristocrat status for the ordinary dividend which goes back to at least 2004, occasionally supplemented with specials, but apparently as far back as 48 years according to the PR. It's paying another dividend in line with the last quarter on an ordinary basis at $0.27, and also coming in with a special dividend of $2.

Dividends (RLI Q4 Pres)

Niche markets have also allowed it to find better underwriting income on a sustained basis, and to avoid intense competition, and get away from businesses as the cycle starts to turn, which is inevitable in insurance as competition grows to underwrite areas and the ability to underwrite profitably is crimped on. We don't raise any major alarms, also noting that generally higher fixed rate returns will support insurance, but some signs of peaking in property is a little worrisome, and casualty is already under pressure with policy writing getting very selective, and even run-offs happening in some of casualty's subsegments. However, we do also note that there is space to drive down the expense ratio due to the presence of discretionary tech investments, which will taper eventually once those projects are complete. Expense ratios have had a meaningful effect on overall combined ratios increasing, actually driving 2/3rds of the Q4 ratio increases.

Still, we pass on RLI's premium given the expectations of some deceleration in the FY signaled by deceleration in operating income growth in this latest Q4, all due to the softening market and lower volume growth we mentioned in the rainmaking property segment, which may slow down the music there sometime next year, while noting that casualty may see incremental improvement from the tough underwriting conditions in Q4 with rate increases coming while still being under pressure. It's a premium company which limits margin of safety on valuation, so we'd rather wait and see what happens in its markets given softening signs.