champc

champc

I've written a total of 6 articles on SA about Radiant Logistics (NYSE:RLGT) and the company is on my watchlist. The latest article was in November and back then I said that Radiant Logistics was performing well in a challenging market and that it looked undervalued at below 7x annualized EV/EBITDA.

On February 8, the company released its Q2 FY24 results, and I think they were decent in light of continuing weakness in the US freight sector. With the price to tangible book value at below 3x and EV/EBITDA dipping to 8.5x, I feel comfortable upgrading my rating on Radiant Logistics’ stock strong buy. Let’s review.

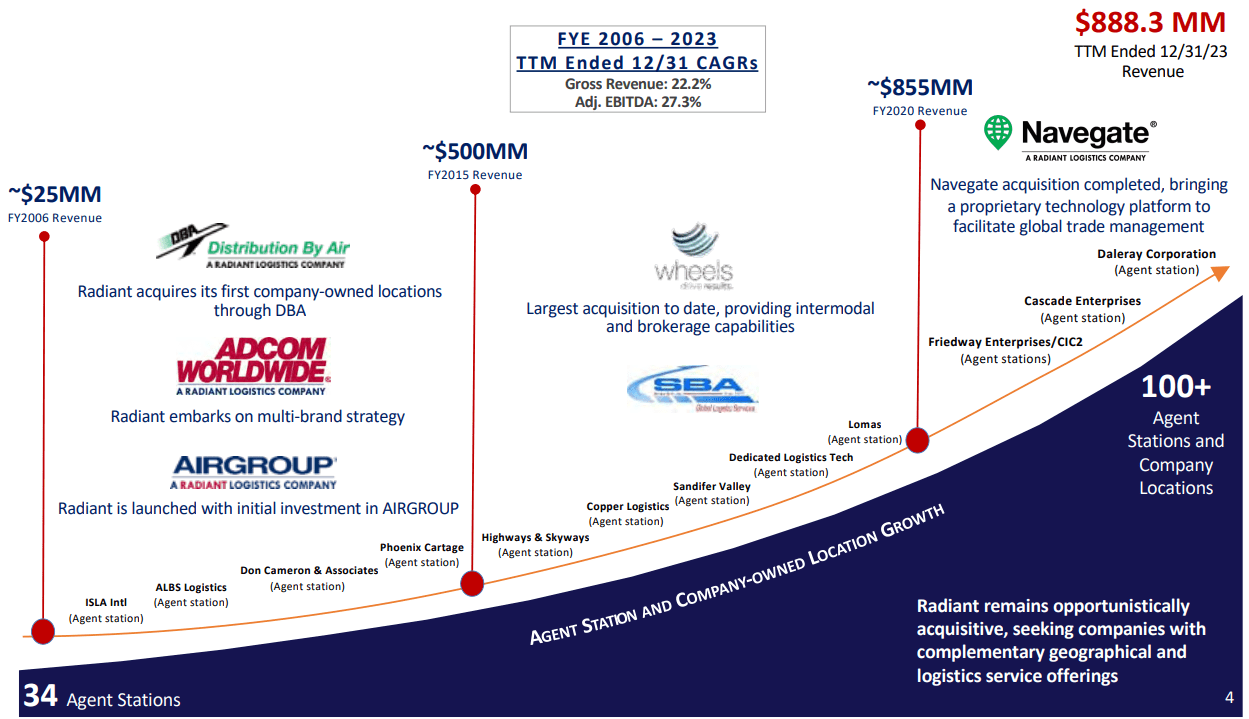

If you're not familiar with the company or my earlier coverage, here's a brief description of the business. Radiant Logistics was founded in 2006 and is a US logistics firm focused on air and ocean freight forwarding and truckload, less-than-truckload, and intermodal freight brokerage solutions in North America. It currently has a network of more than 120 company-owned locations and strategic operating partners (also known as agents) across the USA and Canada and most of its revenues come from freight forwarding. The company serves various industries including automotive, pharmaceuticals, and electronics, among others. Radiant Logistics has an asset-light business model, and it has been growing mainly through acquisitions since its inception. The company has made over a dozen acquisitions to date which has enabled it to grow its annual gross revenue from about $25 million in FY06 to almost $900 million in Q2 FY24 on a TTM basis.

Radiant Logistics Radiant Logistics

The latest acquisition of Radiant Logistics was announced in February 2024, and it included South Florida-focused Select Logistics and Select Cartage. The latter have operated as part of the company's Adcom Worldwide brand since 2007 and I expect this purchase to provide a small boost to profitability. When Radiant Logistics converts an existing agent station to a company-owned location, its revenues and gross margin don’t improve but it gets to eliminate agent station commissions. Usually, these agent stations can bring anywhere from $0.5 million to $2 million of annual incremental EBITDA to the bottom line according to the Q2 FY24 earnings call of Radiant Logistics.

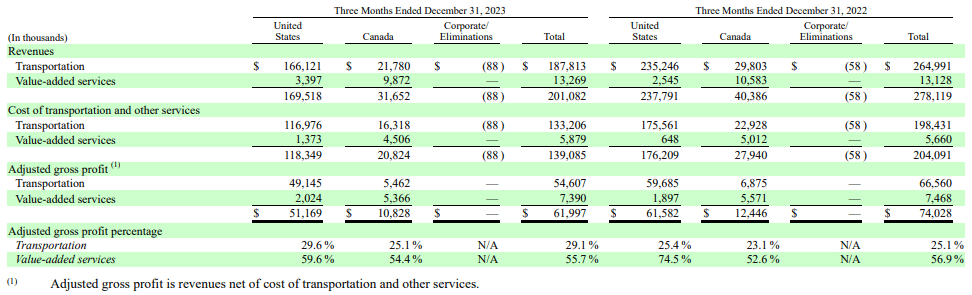

Turning our attention to the Q2 FY24 financial results, we can see that revenues slumped by 27.7% year on year to $201.1 million as international and ocean rates fell. On a positive note, the net transportation margins improved to 29.1% from 25.1% a year earlier thanks to a higher mix of domestic shipments which usually have better margins than ocean and charter shipments. In addition, revenues from value-added services inched up by 1.1% to $13.3 million.

Radiant Logistics

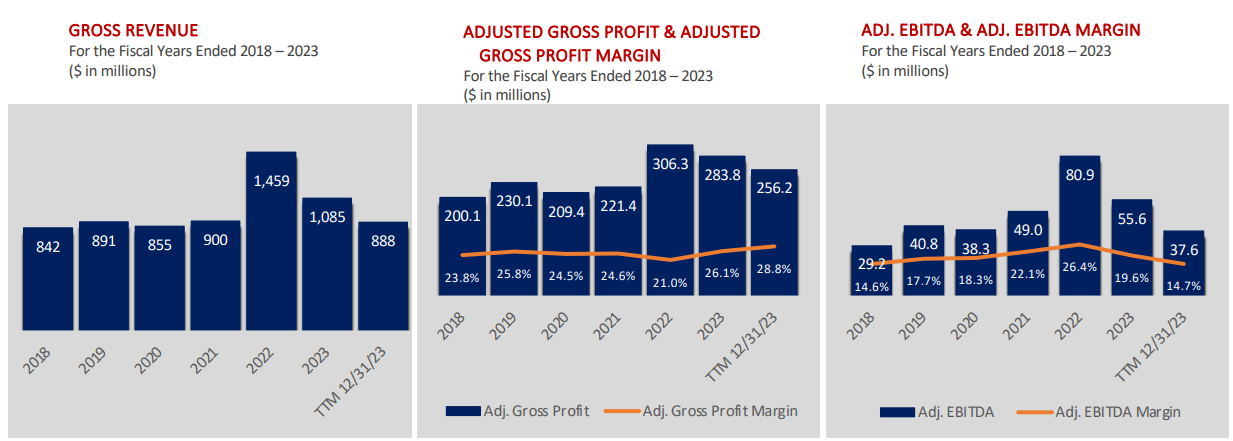

With net transportation margins contracting due to a tough freight market, EBITDA slumped by 39.2% to $5.5 million while attributable net income went down by 79.6% to $1 million. Overall, I think Radiant Logistics performed well in a weak market and I’m pleasantly surprised that the company managed to stay in the black. Looking at the TTM margins, we can see that the adjusted EBITDA margin is now at FY18 levels.

Radiant Logistics

Looking at the balance sheet, Radiant Logistics finished December with a net cash balance of $29.8 million compared to a net cash position of $26.6 million at the end of FY23. The enterprise value (EV) is thus $214.3 million as of the time of writing. As this is an asset-light business, free cash flow (FCF) came in at $7.2 million for the H1 FY24 and the company used $3.1 million for share buybacks and $2.6 million for debt repayment. Overall, I think the balance sheet looks solid and that Radiant Logistics can weather the slump in the US freight market without slowing down its M&A activity.

Looking at what to expect in the coming quarters, Radiant Logistics said in its Q2 FY24 earnings call that business could continue to be slow into Q3 FY24 before we begin to see sequential improvement. It seems that we have passed or we are near the worst of it and I’m optimistic that annualized EBITDA could return above $50 million by mid FY25. Looking farther into the future, the compound annual growth rate (CAGR) for gross revenue was 22.2% and the CAGR for adjusted EBITDA stood at 27.3% between FY06 and FY23 and I think the EBITDA margins of the business are likely to continue to improve over the coming years thanks to economies of scale from both organic and inorganic growth.

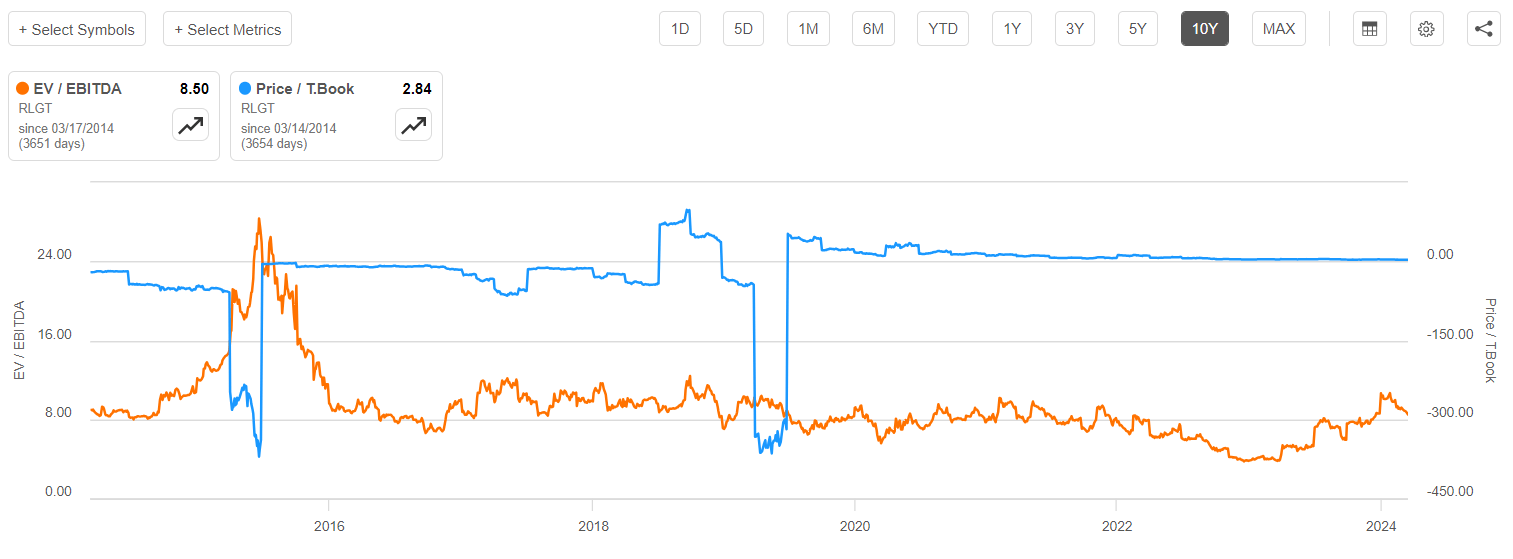

As you can see from the chart below, Radiant Logistics has often traded at EV/EBITDA multiples of between 7x and 10x over the past decade and the company is starting to look cheap compared to FY18 when it had a similar adjusted EBITDA margin to today (the EV/EBITDA even surpassed 11x in January 2018). In addition, Radiant Logistics is currently trading at a historically low price to tangible book value multiple of 2.8x. While this might seem high at first glance, these levels are not unusual for asset-light businesses and this ratio for the company didn’t fall below 10x until June 2021. In addition, the price to tangible book value multiple has been negative for close to half of the past decade.

Seeking Alpha

The balance sheet of Radiant Logistics is strong at the moment which I think could translate into more aggressive share buybacks in the coming months. With the US freight market close to or at a bottom, I think that the valuation could improve to about 10x EV/EBITDA by the end of 2024.

Looking at the downside risks, I think the major one here is that Radiant Logistics could be overly optimistic about the improvement of the US freight market over the remainder of 2024. If the growth of the US economy slows down in the coming months, this is likely to bring several more tough quarters for the sector. The cause of this could be macroeconomic headwinds in China and Europe gradually spreading across North America. If this happens, the valuation of Radiant Logistics is likely to remain depressed over 2024 and potentially through the first half of 2025.

Radiant Logistics operates in a cyclical industry, but it has managed to grow both revenues and EBITDA at a CAGR of over 20% since its inception. In my view, the company is navigating a tough US freight market as well as the TTM adjusted EBITDA margin is close to 15%. Yet, the balance sheet has never been stronger in the history of Radiant Logistics and the company seems optimistic that market conditions will improve soon. With EV/EBITDA dropping to 8.5x, I’m considering opening a position in the coming weeks.