David Gyung/iStock via Getty Images

David Gyung/iStock via Getty Images

Rocket Companies Inc. (NYSE:RKT) is attempting to navigate the challenging housing market where decade-high interest rates have pressured mortgage originations and refinancing activity.

We last covered the stock with a bullish article back in 2022 following what had already been a major reset of expectations from the pandemic-era highs. Favorably, there are signs conditions are at least stabilizing with the company's latest quarterly report highlighted by improving profitability.

The attraction of the stock is the company's continued market share gains implying RKT is consolidating its leadership position. We believe the long-term outlook remains positive with the ability of Rocket to unlock value going forward.

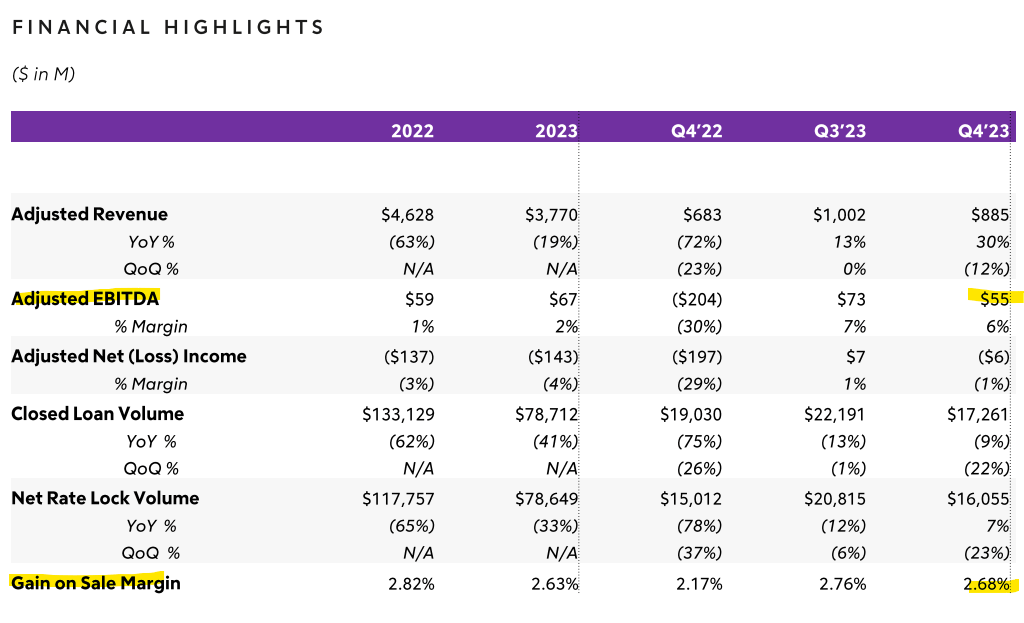

RKT Q4 non-GAAP EPS broke even at $0.00, beating expectations by $0.05 while reversing a loss of -$0.10 in the period last year. Revenue of $885 million also beat estimates, climbing by 30% year-over-year in the context of a historically weak Q4 2022.

A major theme over the past year has been an effort to reduce the cost structure. The total employee headcount ended the year at 14,700 from as high as 26,000 at the end of 2021.

Even as the total closed loan volume at $17.3 billion was down by -9% y/y reflecting the broader weakness of the housing market, net rate lock volume improved by 7% higher. Nevertheless, the gain on sale margin as the total spread of origination to where the loans are sold at 2.68% was materially higher from the 2.17% in Q4 2022.

The result here is an adjusted EBITDA of $55 million was positive for the third consecutive quarter and in contrast to -$204 million in the prior year quarter.

source: company IR

Keep in mind that the entire Rocket Companies platform encompasses various businesses including "Amrock" for title and settlement services, "Lendesk" as software for Canadian Mortgage lenders, along the smaller Rocket Loans for personal financing arm.

During the earnings conference call, management highlighted how the group is integrating more artificial intelligence features intended to make the systems more efficient at the user level while also driving higher conversions.

In terms of guidance, there is some optimism that 2024 will be stronger than 2023 as a continuation of the apparent early stages of a recovery seen in this last quarter. Rocket is targeting Q1 2024 revenue between $925 million to $1.1 billion, representing a 16% y/y.

Finally, we note that the balance sheet remains solid ending the year with $3.6 billion in available cash and $9.0 billion of total liquidity including undrawn lines of credit.

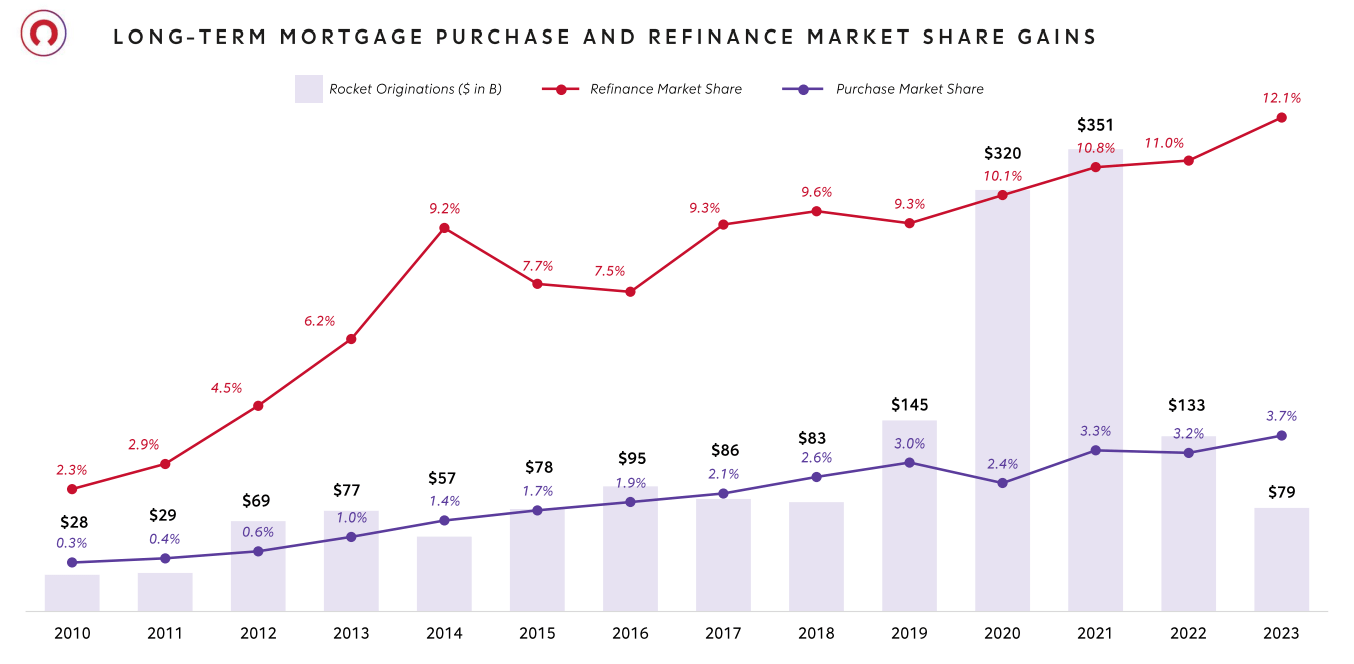

The chart that stands out to us is the trend in market share gains, with Rocket now commanding 12.1% of the total refinancing market in the U.S., up from 11.0% in 2022 and even 9.3% in 2019 as a pre-pandemic benchmark.

This is important because when we start thinking about a scenario where mortgage rates decline whether later this year or into 2025, that dynamic should spur refinancing activity that Rocket would be well-positioned to capture.

Our interpretation of the risking purchase market share which has reached 3.7% from 3.2% in 2022 is that even as the housing market has contracted, Rocket is simply capturing a bigger slice of the existing opportunities.

source: company IR

We believe these factors play into a perception of strong brand momentum, where a cohort of prior customers will be more likely to use the platform again as an incremental growth driver as market conditions improve.

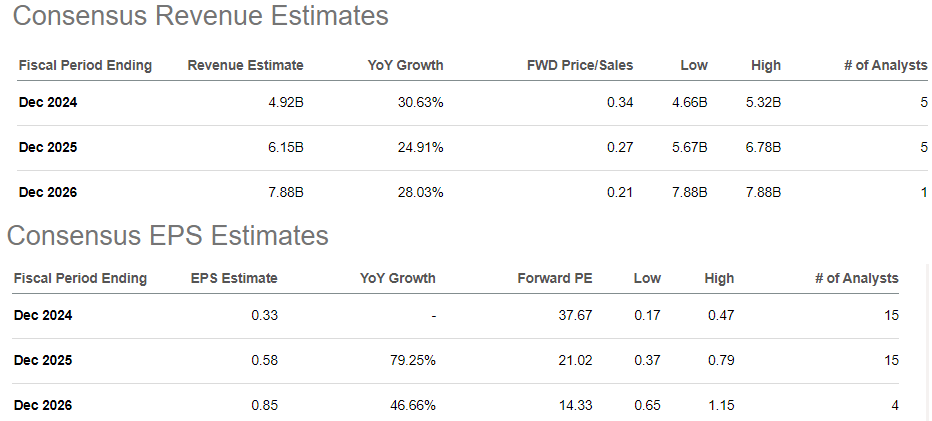

Some of that optimism is captured in the current consensus estimates where the market is forecasting revenue to rebound to $4.9 billion this year, 31% higher than 2024. For 2025 and 2026, the expectation is for annual top-line growth to remain above 25% while EPS more than doubles from the $0.33 2024 estimate.

Seeking Alpha

When we look at the current valuation multiples between a 39x forward P/E or 22x against the fiscal 2025 consensus EPS, these levels could be justified assuming this apparent housing market turnaround materializes.

Naturally, the bullish case for the stock is that Rocket will indeed approach or exceed these targets although we'd say that there is significant uncertainty here on the macro side.

We can praise the company for having the best mortgage origination software platform and otherwise excellent strategic execution, but that all takes a back seat to the actual evolution of the housing market.

There are lingering question marks as it relates to the path of mortgage rates even in a scenario where the Federal Reserve begins cutting short-term policy benchmarks.

Beyond any possibility that the U.S. housing market deteriorates from here with a leg lower in transaction activity, we can bring up the tail risk event that mortgage rates even move higher from current levels that would further pressure Rocket's operating environment.

We're cautiously bullish on RKT balancing those uncertainties in mortgage demand in the next stage in the housing market and against what we believe remain strong points in the company's fundamentals. For the record, we rate shares as a buy with a price target of $17.50 for the year ahead representing a 30x P/E multiple on the current consensus 2025 EPS of $0.58.

Ultimately, we believe RKT stock price will need macro indicators to cooperate as a catalyst for shares to break out higher. Monitoring points here include monthly existing home sales updates, the trend in national mortgage applications, as well as a more convincing decline in long-term interest rates.

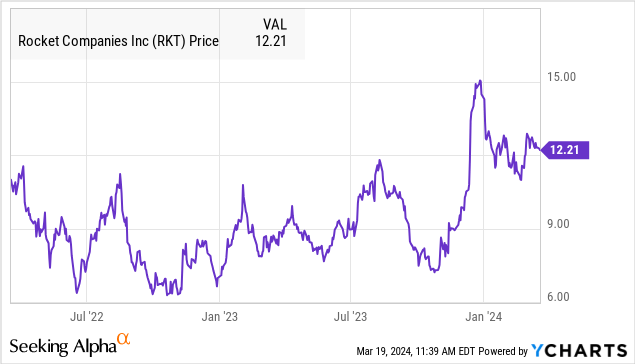

The base case here is for shares to remain volatile, exposed to the ebb and flow of housing market headlines. The $12.00 stock price level appears to represent an important area of technical support going back to early 2022 bulls will want to hold defense.