Returns On Capital At Rio Tinto Group (LON:RIO) Have Stalled

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. In light of that, when we looked at Rio Tinto Group (LON:RIO) and its ROCE trend, we weren't exactly thrilled.

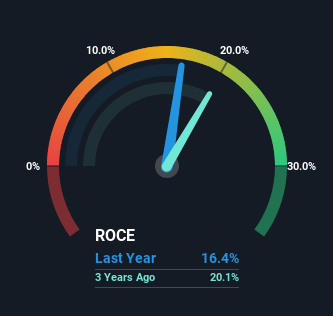

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Rio Tinto Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = US$15b ÷ (US$104b - US$13b) (Based on the trailing twelve months to December 2023).

Therefore, Rio Tinto Group has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Metals and Mining industry average of 7.7% it's much better.

Check out our latest analysis for Rio Tinto Group

Above you can see how the current ROCE for Rio Tinto Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Rio Tinto Group .

What Does the ROCE Trend For Rio Tinto Group Tell Us?

Things have been pretty stable at Rio Tinto Group, with its capital employed and returns on that capital staying somewhat the same for the last five years. This tells us the company isn't reinvesting in itself, so it's plausible that it's past the growth phase. So don't be surprised if Rio Tinto Group doesn't end up being a multi-bagger in a few years time. That being the case, it makes sense that Rio Tinto Group has been paying out 61% of its earnings to its shareholders. These mature businesses typically have reliable earnings and not many places to reinvest them, so the next best option is to put the earnings into shareholders pockets.

In Conclusion...

In a nutshell, Rio Tinto Group has been trudging along with the same returns from the same amount of capital over the last five years. Since the stock has gained an impressive 80% over the last five years, investors must think there's better things to come. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.