MonthiraYodtiwong

MonthiraYodtiwong

Real Estate Investment Trusts (i.e., REITs) look like a highly compelling sector to invest in right now for several reasons:

As a result, some investors who are not otherwise familiar with the REIT sector may be tempted to simply buy the Vanguard Real Estate Index Fund ETF (NYSEARCA:VNQ). After all, it charges a very low 0.12% expense ratio, offers a decent 4.1% trailing twelve-month dividend yield, and is very well diversified with 163 holdings. Moreover, with over $62 billion in assets under management, it offers investors tight bid-ask spreads and even the ability to trade options with decent liquidity if they so desire.

In our view, however, there are several reasons why VNQ is not a worthwhile REIT investment right now:

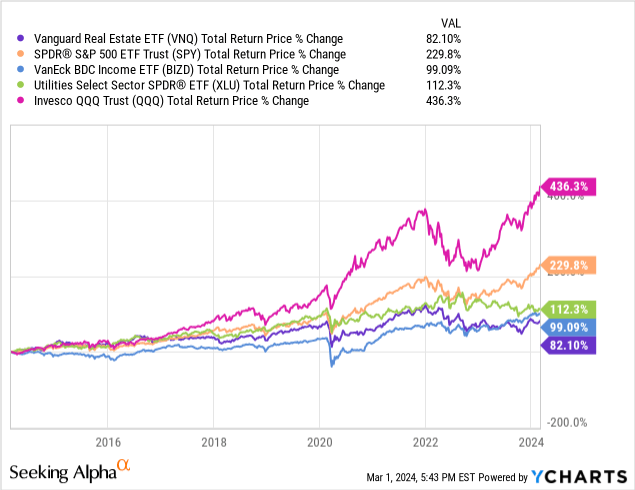

The first big reason is that VNQ has delivered quite poor long-term total return performance. For example, over the past decade, VNQ has not only underperformed the tech-heavy Nasdaq (QQQ) and S&P 500 (SPY) by a wide margin (which is not surprising given that the market has been in a long-running tech boom), but it has also underperformed fellow high-yield sectors such as BDCs (BIZD) and utilities (XLU):

As a result, even against other sectors - like utilities - that suffer and benefit similarly from rising and falling interest rates and tend to generate stable long-term cash flows, VNQ has proven to be a subpar investment.

Moreover, VNQ is not particularly compelling to dividend/passive income investors either. First of all, its 4.1% dividend yield is well below what is being offered by CDs and short-term treasuries (SGOV) right now. Moreover, even relative to other REIT funds, its yield seems to be on the low side, as the Cohen&Steers Quality Income Realty Fund (RQI) offers an 8.1% TTM yield and the Hoya Capital High Dividend Yield ETF (RIET) offers a 10.2% TTM yield.

Moreover, VNQ's three-year dividend CAGR is just 1.56% and its 10-year dividend CAGR is 2.27%. Those growth rates do not even keep up with inflation, making it a very poor dividend growth investment.

With a mediocre dividend yield and very poor dividend growth from a fund that holds what are supposed to be yield-focused investments, why bother?

Last, but not least, skilled active investing has proven to generate superior returns to passive investing in the REIT sector. This is due to three main factors:

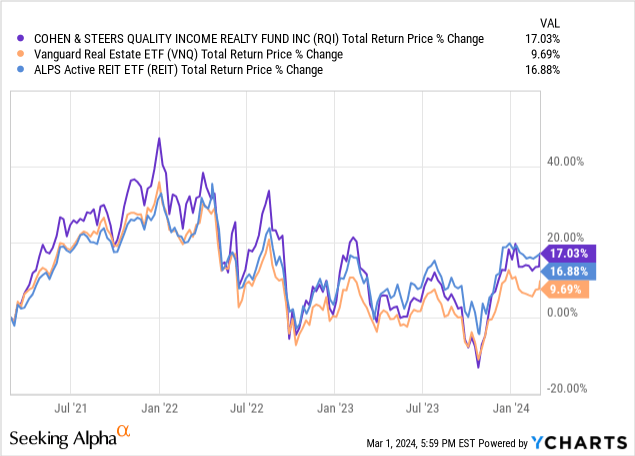

As a result, we should not be surprised to see that funds like RQI and the ALPS Active REIT ETF (REIT) have significantly outperformed VNQ:

While VNQ looks like a simple way to invest in REITs (and it is), it is not a winning way to do so. As history has shown, VNQ has not only underperformed other sectors - including fellow interest rate-sensitive high yielders like utilities - but has also materially underperformed actively managed REIT funds.

As a result, while we are certainly bullish on REITs right now for the reasons mentioned at the beginning of this article, our approach is to buy individual REITs employing a value-oriented and long-term approach as if we were investing in physical real estate. This approach has served us very well and generated significant outperformance over time.

However, for investors who still want to invest in a diversified REIT fund, actively-managed 8.1%-yielding RQI looks like a compelling opportunity as well.