LUMIKK555/iStock via Getty Images

LUMIKK555/iStock via Getty Images

RCI Hospitality Holdings (NASDAQ:RICK) operates nightclubs and sports-bar restaurants. The company’s nightclub brands include Risk’s Cabaret, PT’s Showclub, Club Onyx, and Tootsie’s Cabaret. RCI Hospitality’s restaurant brand is the military-inspired Bombshells. The company has a long track record of acquisitions and some organic growth initiatives, growing its footprint in the United States into 56 revenue contributing nightclubs and 14 Bombshells restaurants as of Q1/FY2024 according to the company’s Q1 investor presentation.

The stock has performed well on a long-term basis with RCI Hospitality’s good execution of capital allocation. In the past decade, the stock has compounded at a CAGR of 17.2%. The company does also pay out a dividend, but the yield is very low at 0.42% as RCI Hospitality tries to find more opportunistic allocations for its cash flows.

Ten Year Stock Chart (Seeking Alpha)

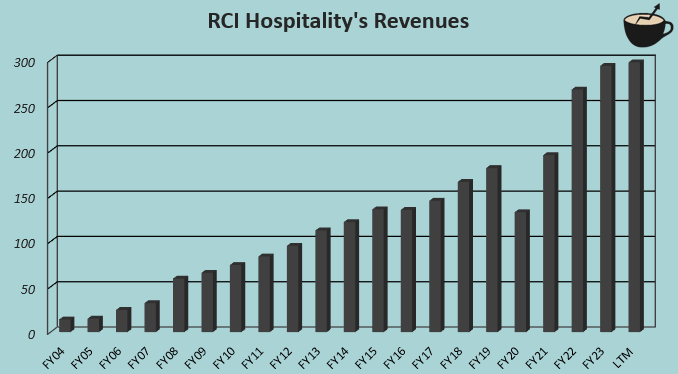

RCI Hospitality’s long-term strategy of acquisitions has resulted in a very good amount of growth – from FY2004 to current trailing revenues as of Q1/FY2024, the company has a revenue CAGR of 17.3%.

Author's Calculation Using TIKR Data

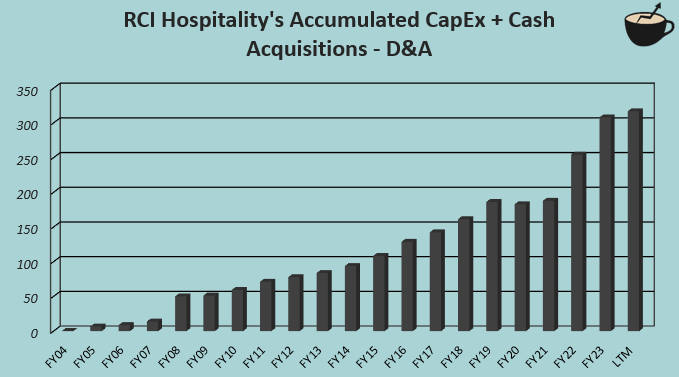

The growth has been achieved through constant growth investments – from FY2004, to scale the company’s operations, RCI Hospitality has now spent over $300 million in capital expenditures and cash acquisitions in total excluding depreciation & amortization that should relate quite well to maintenance capital expenditures. The company’s capital allocation has also allowed for reducing outstanding shares through share buybacks, as weighted average outstanding shares have decreased slightly from 9.8 million in FY2014 into a current 9.4 million.

I believe that the capital allocation strategy is great, proven by the fantastic stock appreciation, and great EPS growth going from $1.15 in FY2014 into a current trailing $2.80. The company constantly targets new nightclub acquisitions at 3-5x EBITDA, opportunistic share buybacks and organic new unit investments for growth. RCI Hospitality targets to own 200 locations in the long term; the company is still relatively small, and has a great amount of space for growth in the future. In FY2023 alone, the company deployed $77.9 million into nightclubs, $17.3 million for Bombshells restaurants, and $7.5 million for current casino investments.

Author's Calculation Using TIKR Data

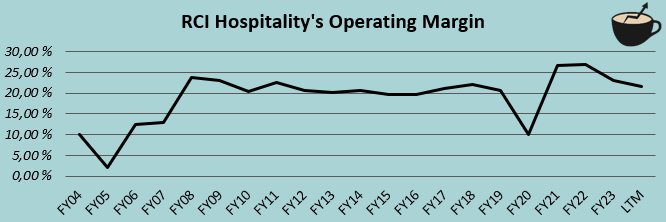

RCI Hospitality is also able to keep a good profitability – the company has had quite a stable operating margin a bit above 20% in past years, excluding some turbulence during the Covid pandemic. RCI Hospitality prefers to buy the real estate for its owned locations, contributing into the earnings greatly; while owning the real estate makes the growth strategy more expensive, it does provide stability and a higher level to the company’s profitability.

Author's Calculation Using TIKR Data

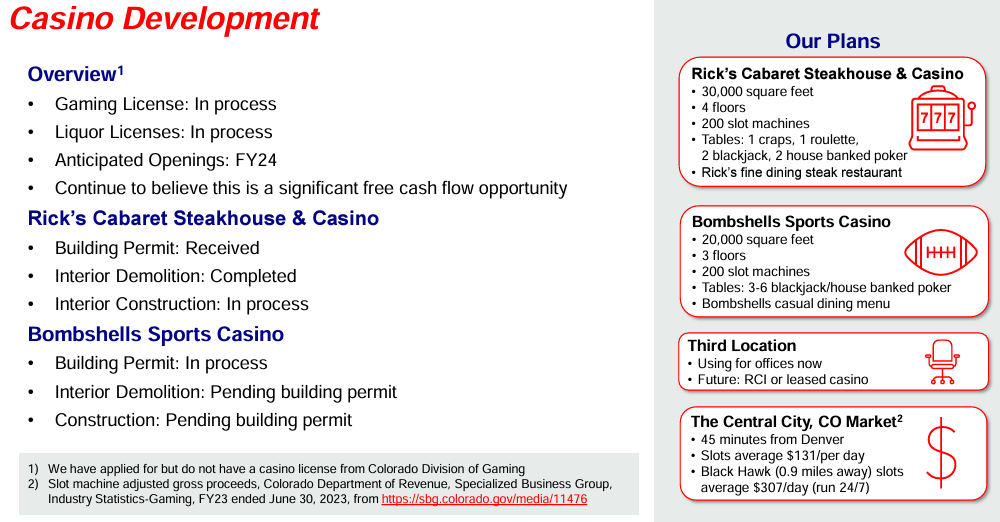

RCI Hospitality plans to expand into the casino segment with a planned 30 thousand square feet Rick’s Cabaret Steakhouse & Casino, as well as a 20 thousand square feet Bombshells Sports Casino. The company anticipates to open both in FY2024, with some pending permits still slowing down the progress.

RICK Q1 Investor Presentation

RCI Hospitality’s management seemed confident in the casinos’ cash flow generation in the Q1 earnings call. The businesses were mentioned to have significant cash flow potential for the company, and the vertical seems to be a new addition to RCI Hospitality’s growth avenues, with potential to expand the casino model into other states being mentioned in the earnings call on a more long-term view.

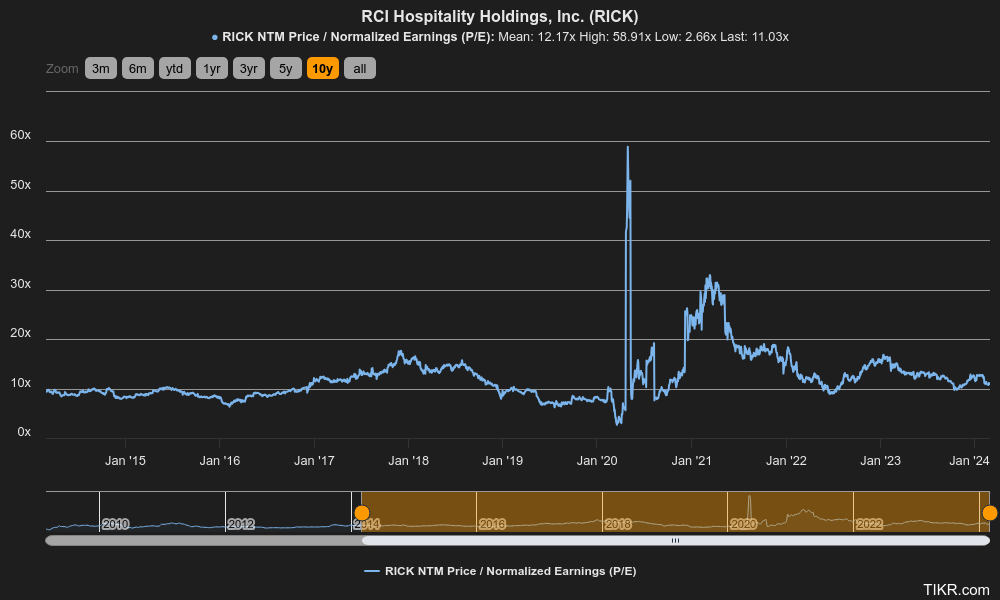

In the past decade, RCI Hospitality has traded at an average forward P/E multiple of 12.2. Currently, the stock trades slightly below the historical figure at 11.0, as interest rates are currently higher than in the prior decade on average.

Historical Forward P/E (TIKR)

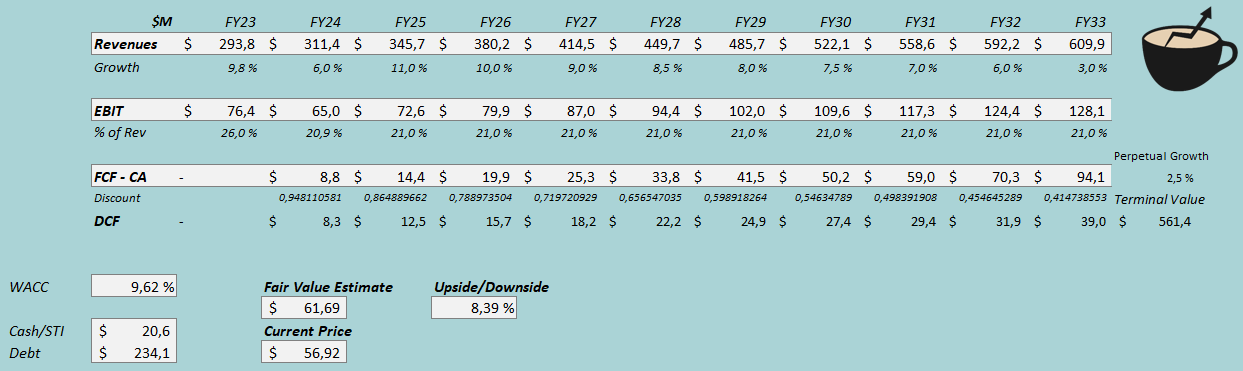

To estimate a rough fair value for the stock, I constructed a discounted cash flow model. In the DCF model, I factor in acquisitions as they are critical in RCI Hospitality’s strategy; for FY2024, I estimate a growth of 6% with a slower macroeconomic development affecting same-store sales negatively. Afterwards, I estimate a growth of 11% in FY2025 that slows down into a perpetual growth of 2.5% in steps, effectively translating to slowing down acquisitions that mostly stop in FY2033 with a growth of 3%. The total estimated revenue CAGR is 7.6% from FY2023 to FY2033. In the company’s Q1 earnings call, CEO Eric Langan related to a target of 10% growth in free cash flow over the next two years.

I expect the company’s profitability to stay stable, and only to increase by 0.1 percentage point from an estimate of 20.9% into 21.0% in FY2025 and forward. With the slowing estimated growth, I estimate RCI Hospitality’s cash flow conversion to improve from a poor conversion estimate in FY2024 into quite a good one in FY2033 as acquisitions stop in the model.

With the mentioned estimates along with a cost of capital of 9.62%, the DCF model estimates RCI Hospitality’s fair value at $61.69, around 8% above the stock price at the time of writing. While the company has great capital allocation, I do not see significant short-term upside for the stock. Still, the stock seems to have some slight undervaluation, and the long-term appreciation potential should be quite good. The company could also continue the acquisition strategy significantly longer than the ten-year period which I estimate in the DCF model, proving a better fair value than my model estimates.

DCF Model (Author's Calculation)

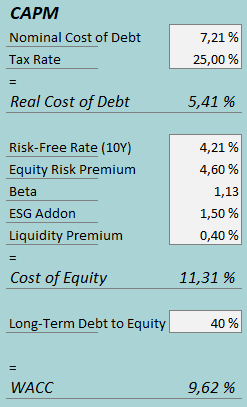

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q1/FY2024, RCI Hospitality had $4.2 million in interest expenses. With the company’s current amount of interest-bearing debt, RCI Hospitality’s annualized interest rate comes up to 7.21%. The company itself communicates a weighted average interest rate of 6.61%, but I believe that the actual interest including lease interest is a fairer estimate to use. The company uses quite a good amount of debt, and I estimate the long-term debt-to-equity ratio to be around 40%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.21%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates RCI Hospitality’s beta at a figure of 1.66. I believe the business to be more macro resistant than the figure lets believe; instead, I use Zacks’ estimate of 1.13, which the stock had at the end of 2019 prior to the pandemic that seems to have caused an uptick in beta in recent years. Finally, I add an ESG add-on of 1.5% and a small liquidity premium of 0.4%, creating a cost of equity of 11.31% and a WACC of 9.62%.

As an interesting note, RCI Hospitality’s capital allocation strategy includes opportunistic share buybacks in case the shares’ free cash flow yield exceeds 10%. My CAPM estimates the company’s cost of equity at 11.31%; when factoring in modest organic free cash flow growth, the share buyback rule of thumb sounds like a reasonable strategy.

RCI Hospitality has a great strategy of creating shareholder value through acquisitions. The company drives value through cheap acquisition valuations, opportunistic share buybacks, and organic investments such as the newly developed casinos. The strategy includes owning the real estate in which RCI Hospitality operates, making the growth more capital intensive but providing earnings stability. While the strategy is good, I do not see very significant short-term upside in the stock’s value – for the time being, I have a hold rating on the stock.