metamorworks

metamorworks

PageGroup (OTCPK:MPGPF) introduced its recent annual results with the headline, “Resilient performance in challenging market conditions, restructured cost base, final dividend increased 4.5%”. The benign introduction will hardly excite investors, but it is a microcosm of how the company navigates the cyclical global recruitment industry. PageGroup’s strategic investment strategy and diversified portfolio across multiple sectors and geographies allow the company to produce resilient results in tough market conditions while paying investors an impressive dividend. Investors do need to accept substantial volatility when the cycle turns down, and recent results point to turbulent times ahead, but tough times are often the best times for investors to position themselves for the growth and market share gains that tend to follow as PageGroup’s position as a premium navigator in the global recruiting industry shines through.

The recruiting industry can be terribly cyclical with rapidly changing market conditions. It can also be local with large variations between geographies or even industries. The volatile conditions can lead many recruitment companies to drastically cut headcount or cost in downturns to prevent profit decimation and financial stress. Unfortunately, such short-term cost actions can also lead to brand damage, distrust from clients that value a reliable presence and the inability to grow when markets recover as key fee earners are no longer with the company. It’s a difficult situation, but PageGroup has a few key advantages over competitors which stem from its strategy to hold firm in key markets when others are pushed out.

PageGroup is focused on organic growth, and indeed, the vast majority of its growth over the years has come from investments in its business. PageGroup also seeks to have a robust base to operate from through a diversification of geographies and professional disciplines or industries. Diversification in an industry that can often be quite localized is critical. A derivative of diversification is scale and brand awareness, both of which PageGroup has managed to achieve on a global basis. More importantly, PageGroup has developed an effective system to know where and when to increase investment or pull back on costs.

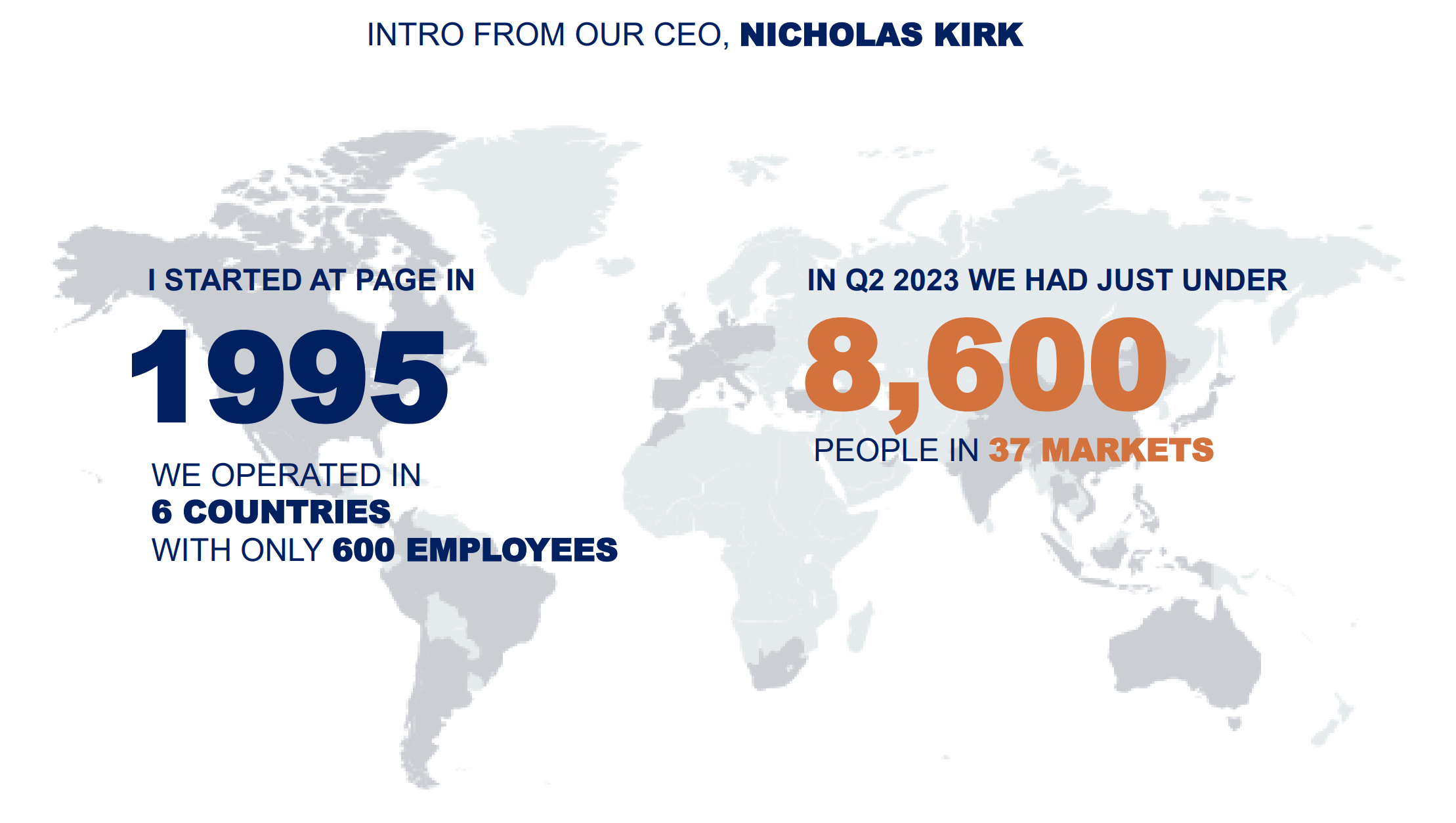

PageGroup has grown rapidly over the last couple decades (PageGroup Capital Markets Event, September 2023)

Source: PageGroup Capital Markets Event, September 2023

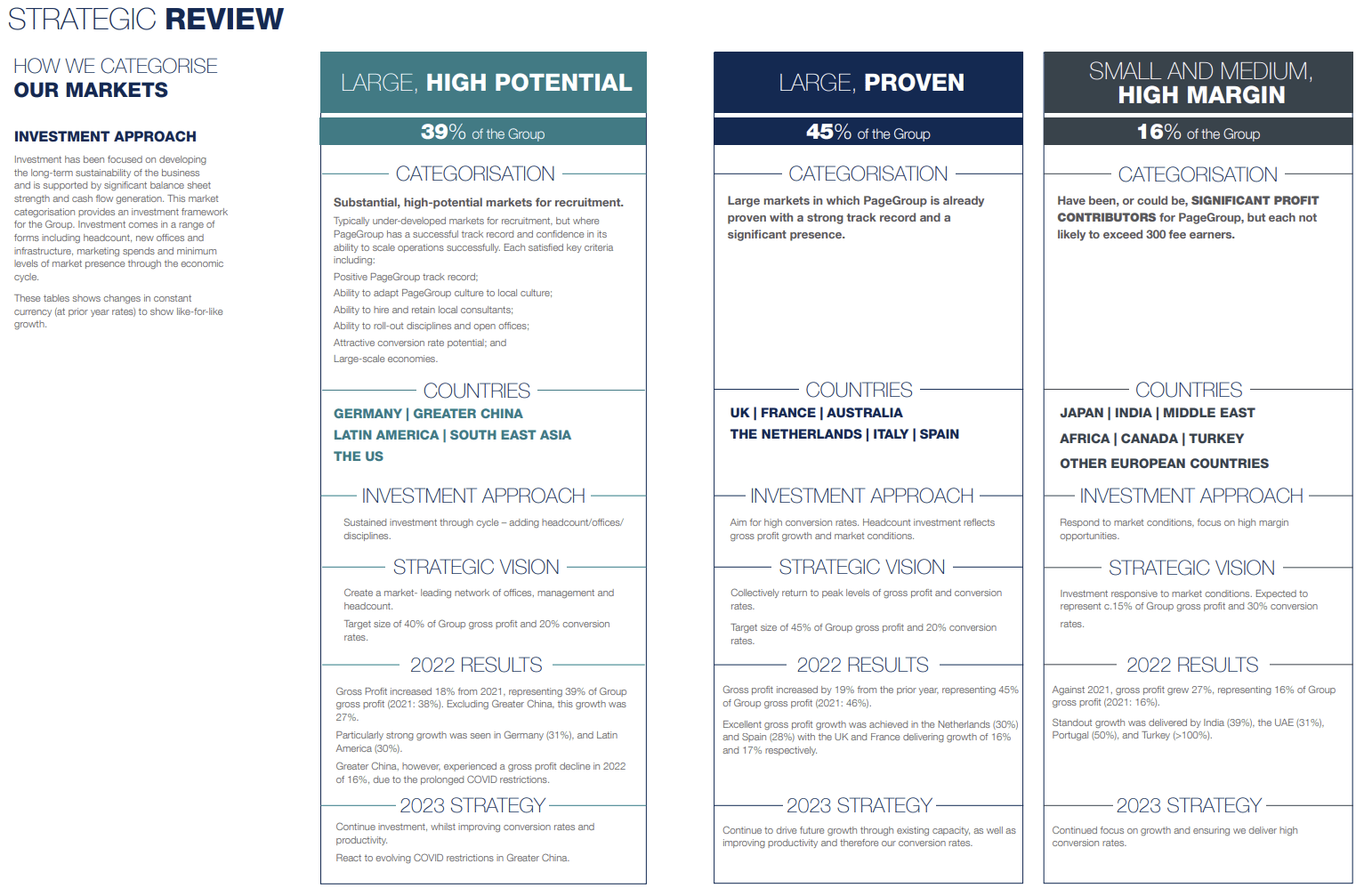

Each geographic area as well as end market discipline is defined in a particular category which then helps determine whether headcount should be protected during a downturn or whether capital investment should continue during difficult market conditions. If PageGroup has a positive long-term view on particular geographies or industries, the company will strategically invest when competitors are suffering and running for the exits. The short-term impact might be slightly lower profit levels, but the long-term impact is significant market share gains and a respected brand, not to mention employee loyalty to a company that supported them during hard times.

Page Group Strategic Review (PageGroup Annual Report 2022)

Source: PageGroup Annual Report 2022

Other companies might have the ambition, if not the diversification and scale, to apply a similar strategy. But few have the critical component that makes it possible. Long-term strategic investment requires management foresight and discipline, but it also requires a strong balance sheet. Many competitors shut up shop and send their key employees into PageGroup’s open arms because they don’t have the financial strength to survive otherwise. PageGroup has a habit of sitting on a substantial net cash position, helping ward off any short-term panic even in the toughest of times. High quality peers such as Robert Half (RHI) or Hays (OTCPK:HAYPF) boast strong balance sheets as well, but that’s not so for the plethora of smaller competitors across their markets.

The 2020 pandemic and its consequent plague of uncertainty and financial stress is a recent example of how PageGroup deploys its strategy. This passage from their annual report sums it up nicely.

“The small size of our specialist teams enables us to grow gross profit quickly with incremental fee-earner headcount. When market conditions tighten, this headcount is reduced mostly via natural attrition, to ensure a lower cost base in a slowdown. We have managed this well through the pandemic and chose to maintain our platform during 2020; this decision has enabled us to accelerate more quickly than our competitors coming out of the pandemic to deliver the record results achieved in 2021.We have retained experienced staff and continue to focus on the training and development of all our employees. We selectively added over 1,100 experienced hires from the competition from Q2 2020 through to the end of 2021. These decisions have helped to drive the productivity gains achieved during the year and put us in a strong position for 2022 and beyond.”

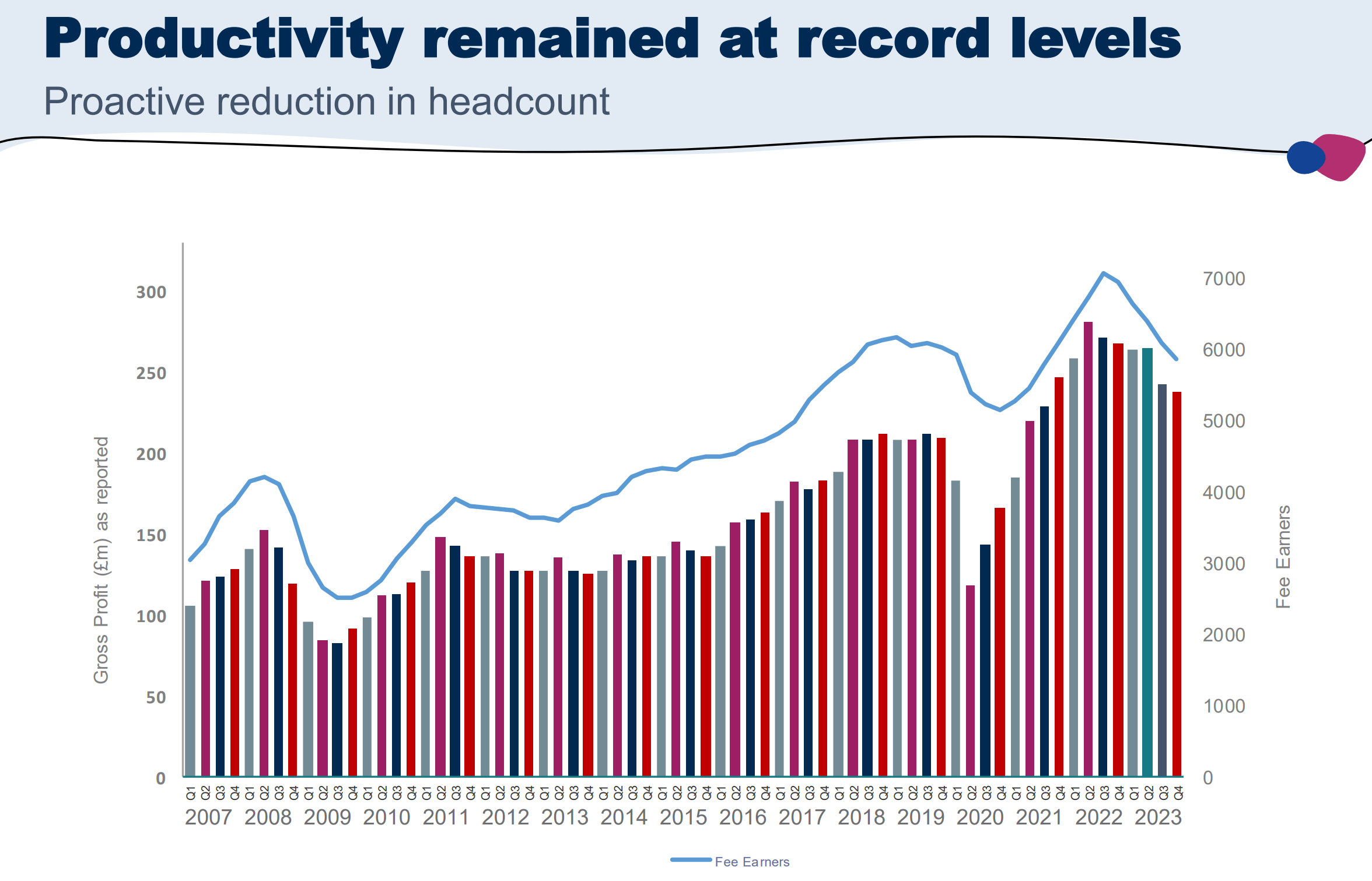

PageGroup’s sales growth in 2021 and 2022 was 26.0% and 21.1% respectively, underscoring the effectiveness of the company’s strategy and implementation. PageGroup has once again cut expenses and Fee Earners at the end of 2023, signaling a tough market environment in 2024. And make no mistake about it, both management and investors do have to deal with challenging markets and stock price volatility. Earnings per share dropped over 40% in 2023 as market conditions tightened, and we expect continuing headwinds in 2024. Longer-term investors have also witnessed stock price swings which have seen the pandemic low near 280 GBX as well as a recent high near 680 GBX in late 2021. But difficult times are when PageGroup builds for future growth as demonstrated by the chart below. Headcount can be increased again following market downturns with growth often recovering as was the case following the pandemic in 2021 and 2022.

PageGroup grows rapidly following down markets. (PageGroup Full Year Results 2023)

Source: PageGroup Full Year Results 2023

PageGroup’s story sounds nice in writing, but let’s look at some evidence in numbers. The company’s asset light business model and exemplary capital allocation has created a track record of impressive value creation and growth. We often view value creation through the lens of return on invested capital, both in its absolute form and in its consistency. A glance at PageGroup’s return on invested capital profile in LSEG shows a decade of return levels well above 20% with the only blemish being a result of the pandemic in 2020. Sales have nearly doubled over the last decade, resulting in a compound annual growth rate of approximately 7.5%.

PageGroup sales. (LSEG, sales in millions of GBP)

Source: LSEG, sales in millions of GBP

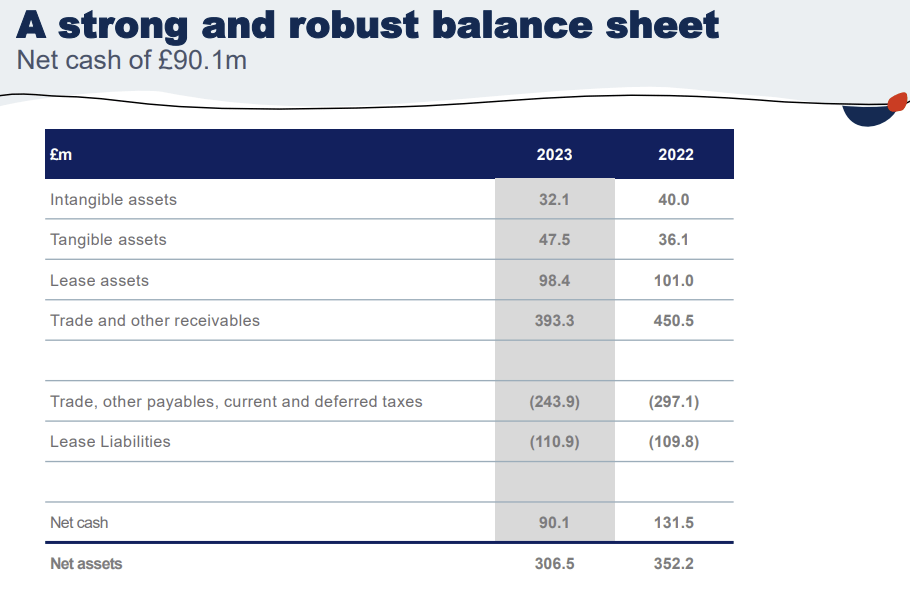

The company’s recent 2023 annual results include a steep drop in profitability, but also remind us of the company's balance sheet strength with the company sitting on net cash of GBP 90.1m – not bad for a company with about a GBP 1.5b market capitalization. The final dividend was also increased by 4.5% which will complement another large special dividend. Investors should keep a close eye on the extreme profitability pressure, but with free cash flow remaining positive and a strong balance sheet, PageGroup remains well positioned to continue to invest in its business and take advantage of any financial stress experienced by its competitors.

PageGroup balance sheet (PageGroup Full Year Results 2023)

Source: PageGroup Full Year Results 2023

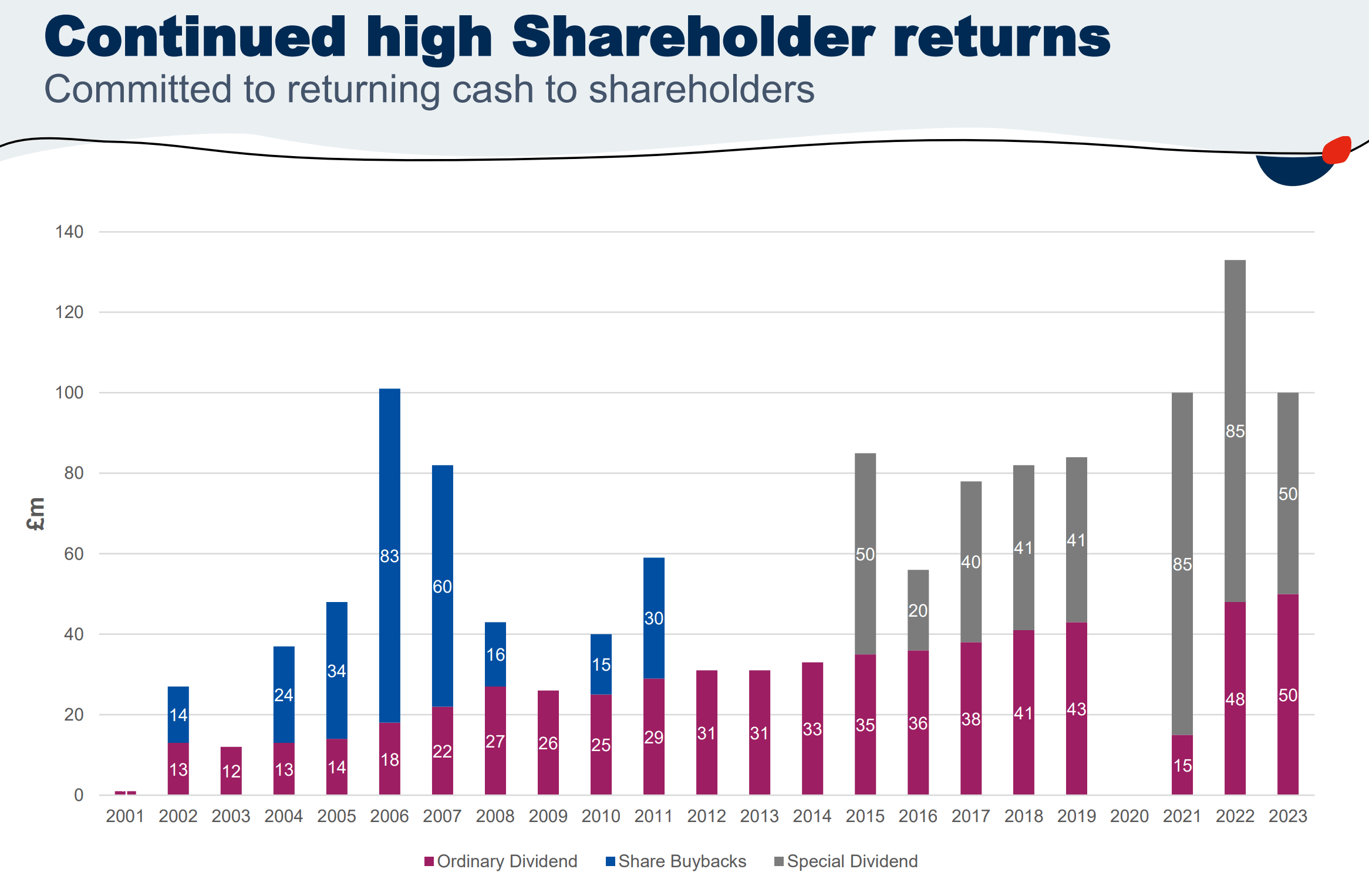

PageGroup’s predictable and efficient capital allocation should also not be underappreciated. The company’s strong cash flow conversion ultimately results in a reliable normal dividend which is often complemented by a special dividend which can more than double the dividend yield. Management has also historically proven adept at converting the special dividend to stock buybacks if the company is trading well below what we would perceive to be intrinsic value, and we can’t help but notice the general upward slope in the graph below. Perhaps shareholder returns are also supported by reasonable executive compensation, which is a fraction of that paid by peers such as Robert Half according to LSEG.

PageGroup's impressive shareholder returns (PageGroup Full Year Results 2023)

Source: PageGroup Full Year Results 2023

So how much should we pay for a growing company with impressive return on invested capital, a pristine balance sheet and exemplary capital allocation? 20x earnings? Or maybe 25x earnings? PageGroup’s average long-term P/E multiple is indeed near 20x, and with consensus expecting earnings per share near 23p for 2024, one could argue the stock is fairly priced (all according to LSEG). But doesn’t that valuation ignore the company’s ability to produce earnings per share of 43.5p in 2022, a year with less tough trading conditions? Or indeed the consensus expectations that PageGroup will again produce earnings per share near 43p by 2026? We prefer to value the company with a discounted cash flow model incorporating our longer-term view of the company. Our base case model has a compound annual growth rate over the next decade of 4% (versus the ~7.5% last decade) and an average net margin of 5.9% (versus a long-term average of 6.3%) combined with a WACC of 9% and a terminal growth rate of 2%. We view the assumptions as conservative, as would management. Our model results in an operating profit of GBP 227m in 2030 versus a company target of GBP 400m. Ultimately, our fair value estimate is 631 Pence Sterling per share resulting in approximately 40% upside. We own a material position in the company at this level and will patiently collect the dividend until the market decides to appreciate the value of PageGroup’s strong market position and financial performance. We will, however, stress the need for patience and the nerves to handle volatility as downturns in the recruiting market can last longer than anticipated and lead to material fluctuations in share price.

We invest via the company’s primary ticker on the London Stock Exchange.

PageGroup is a smaller-cap British recruiting company that seems to be flying under the radar of many investors, despite the global scale of its business. The cyclicality of its industry leads to share price volatility that can scare capital allocators away, while its dividend profile may be misunderstood due to the regularity and size of special dividends. For those that look closer and can stomach some turbulence, a truly compelling opportunity awaits. PageGroup sits atop its net cash, consistently producing double-digit returns on invested capital while continuing to strategically invest in its future. Recent results demonstrate how deep downturns in profitability can be, but also the potential for growth and the strength of PageGroup’s market position. PageGroup's resilience doesn't promise steady results in the short-term, but rather is indicative of its ability to survive the harsh volatility of the global recruiting industry and emerge a stronger company. It’s hard to find such a combination of quality and growth trading at an attractive valuation in today’s markets, making PageGroup a compelling investment choice despite expected headwinds in the recruiting industry.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.