Lazy_Bear

Lazy_Bear

YCharts

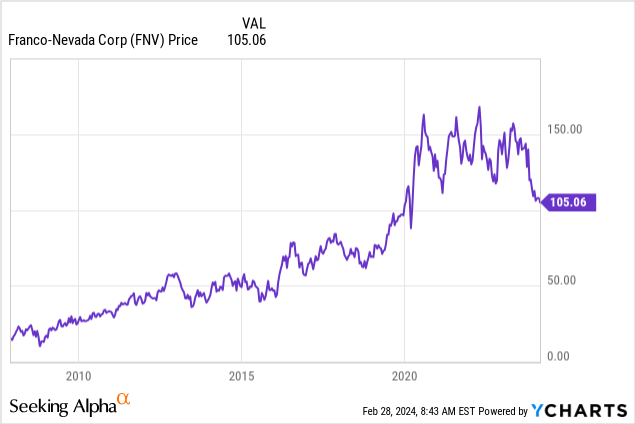

Updating my view on Franco-Nevada Corporation (NYSE:FNV), the behemoth in the streaming and royalty industry boasting over 400 assets globally and an annual production surpassing 600,000 gold equivalent ounces, it seems the tides may have turned for its stock valuation.

In January 2023, I went against the grain by suggesting that Franco-Nevada's premium pricing wasn't justified at $138 per share, despite its history of nearly 20% annual returns since its IPO, making it a standout performer in the precious metals sector.

Since that call, Franco-Nevada's stock has seen a 24% decline, outpacing the 20% drop in the broader gold miners index (GDX) and underperforming peers like Wheaton Precious Metals (WPM), Royal Gold (RGLD), and Triple Flag (TFPM).

Now, with the significant pullback in its share price, Franco-Nevada's valuation appears more attractive, presenting what I believe to be a compelling entry point for investors. The downturn could signal a golden opportunity to invest in a historically resilient and growth-oriented company at a more reasonable price.

The Cobre Panama mine (First Quantum)

Franco-Nevada finds itself in a precarious position with its largest investment to date, having committed US$1 billion toward the development costs of the Cobre Panama project, operated by First Quantum Minerals. The deal, structured as a streaming agreement, is tied directly to producing precious metals from the mine, representing a significant 22% of Franco-Nevada's revenue in 2023.

With a total capital investment of $1+ billion into the project, and having recouped only half of that amount thus far (See: slide 22 of its corporate presentation), the stakes are high for the company.

The situation took a turn for the worse when Panama's Supreme Court declared the license for operating the Cobre Panama mine, extended for another two decades under Law 406, unconstitutional. This law was pivotal for the revised contract between Panama and First Quantum, expected to significantly boost Panama's tax benefits, including a guaranteed minimum fiscal payment of $375 million from First Quantum.

The court's decision comes amid widespread protests from social and environmental groups, challenging the October agreement's validity and its implications for Panama. As a result, the Cobre Panama mine has ceased production and is currently under care and maintenance.

Franco-Nevada is now poised to take all necessary legal steps to safeguard its investment and assert its rights in Panama. This setback not only puts a considerable revenue source in jeopardy, but also tests Franco-Nevada's resilience and strategic response to protect its financial interests amid the legal uncertainty surrounding the Cobre Panama project.

The future of the Cobre Panama mine, despite its current legal and operational predicaments, might not be as bleak as it seems. This mine isn't just another operation; it's a cornerstone of Panama's economy, contributing significantly to copper production and economic impact.

The Cobre Panama mine's contribution to Panama's economy and the global copper supply in 2022 was significant, producing 350,000 tonnes of copper. This accounted for 1.5% of the entire world's copper output and 5% of Panama's GDP! Also, employment and economic contributions from Cobre Panama are substantial, with about 7,000 direct jobs and an estimated 33,000 individuals indirectly relying on the mine for their livelihood, according to First Quantum.

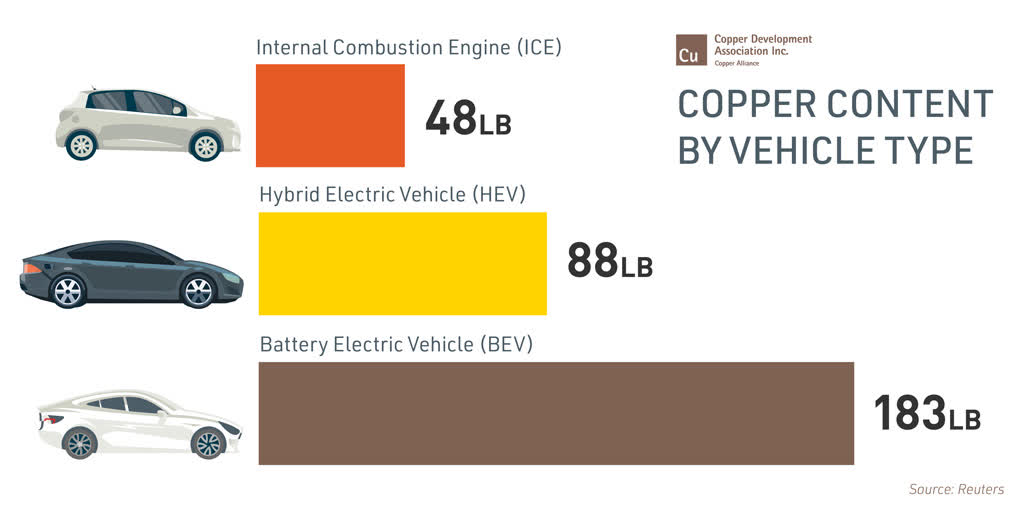

Such figures highlight the mine's critical role within Panama and the wider copper market, underlining its value to the green energy movement (copper is an essential material component of electric vehicles (EVs).

Copper Development Association

Should the situation escalate to that point, the potential costs associated with arbitration loom large over Panama. Industry estimates, including those from The Financial Post, suggest that the economic toll from operational disruptions could reach billions of dollars, a scenario Panama would likely want to avoid.

Also, the socio-political landscape in Panama could be shifting toward a resolution. With national elections on the horizon in May and a recent de-escalation in protests, there has been a dialogue about mining's vital contribution to the nation's economic health. Perhaps this is a window of opportunity for renegotiating the mine's operational status.

Speculation aside, the sheer value and impact of Cobre Panama on both local and international stages make a strong argument for its revival. It's difficult to envision Panama allowing such a significant asset to remain shuttered, especially given its importance to the national economy and the global copper market.

An agreement in 2024, while currently speculative, seems a pretty reasonable outcome when considering the ramifications.

YCharts

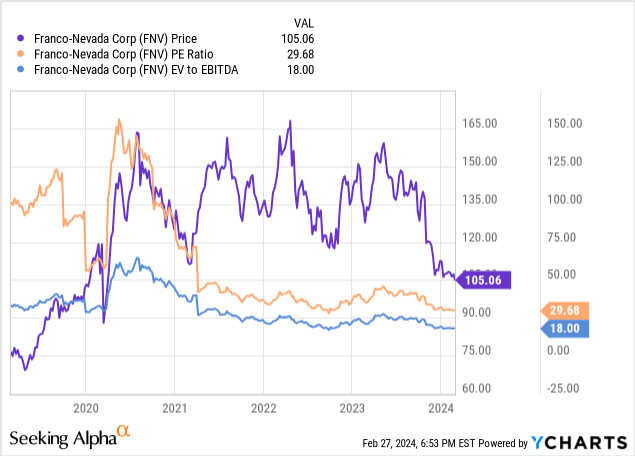

Franco-Nevada's current valuation metrics present a compelling argument for its attractiveness as an investment. The company's price-to-earnings (P/E) ratio stands at 30.17, with a similar forward P/E, positioning it on the higher end when juxtaposed against typical mining companies, which often see P/E ratios between 15 to 19 times earnings.

Yet, Franco-Nevada's valuation is pretty modest within the royalty company sector, especially against peers like Wheaton Precious Metals (WPM) and Triple Flag (TPFM), which boast P/E ratios of 33 and 35, respectively.

Notably, Franco-Nevada's shares are trading at their lowest P/E ratio in a decade, a significant deviation from its historical range of 40 to 60 times earnings, and far from the peak P/E of 100 observed in 2016. This downward adjustment in its P/E ratio signals a rare valuation window for investors, given the company's historically higher multiples.

Franco-Nevada's enterprise value to EBITDA (EV/EBITDA) ratio of 18x is the lowest it has been in over ten years. This offers a more favorable entry point compared to its five-year trading history between 30x to as high as 55x EBITDA.

Franco Nevada

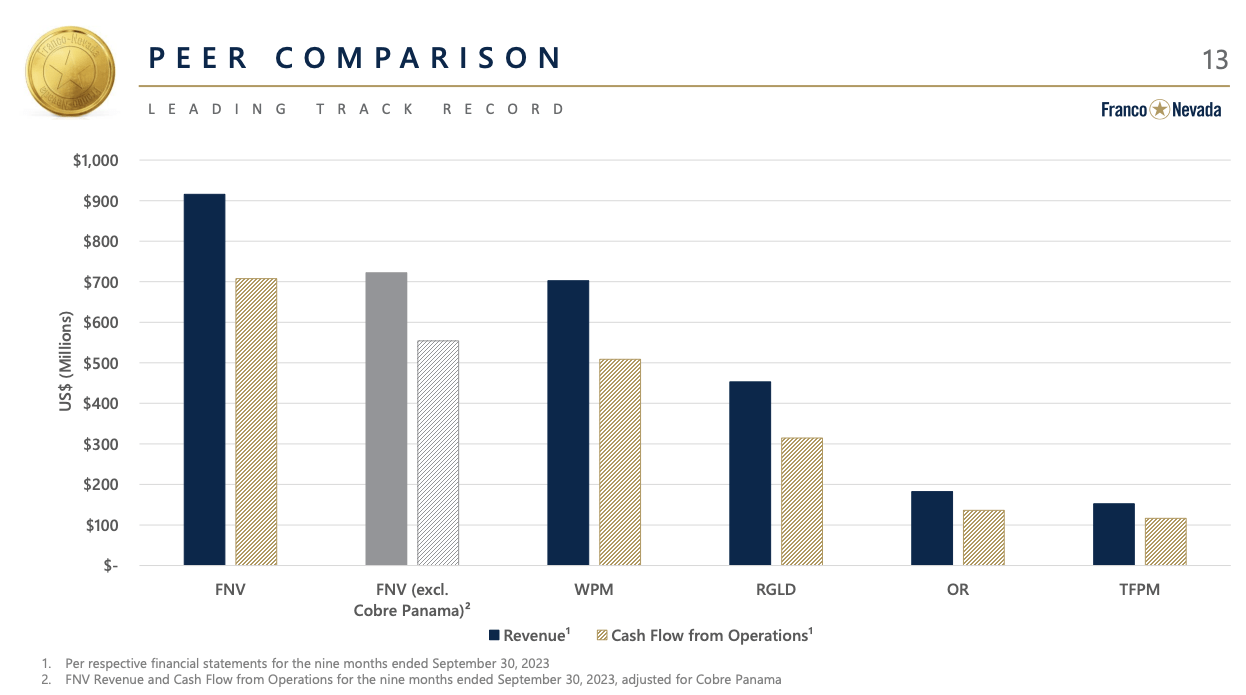

This valuation is especially noteworthy considering the company's robust financial performance, including more than $1 billion in adjusted EBITDA and around $700 million in annual cash flow for the past two years, with impressive 83% margins. (Even without Cobre Panama, the business is a cash flow machine, as seen in the above corporate slide).

According to company estimates, the potential restart of operations at Cobre Panama could further enhance Franco-Nevada's financial outlook, potentially increasing its cash flow and net asset value by 20%. Alternatively, the company stands to gain from arbitration, presenting potential value not yet reflected in its stock price.

So, even in the absence of Cobre Panama's contributions, Franco-Nevada's current valuation levels suggest a compelling value.

Franco Nevada

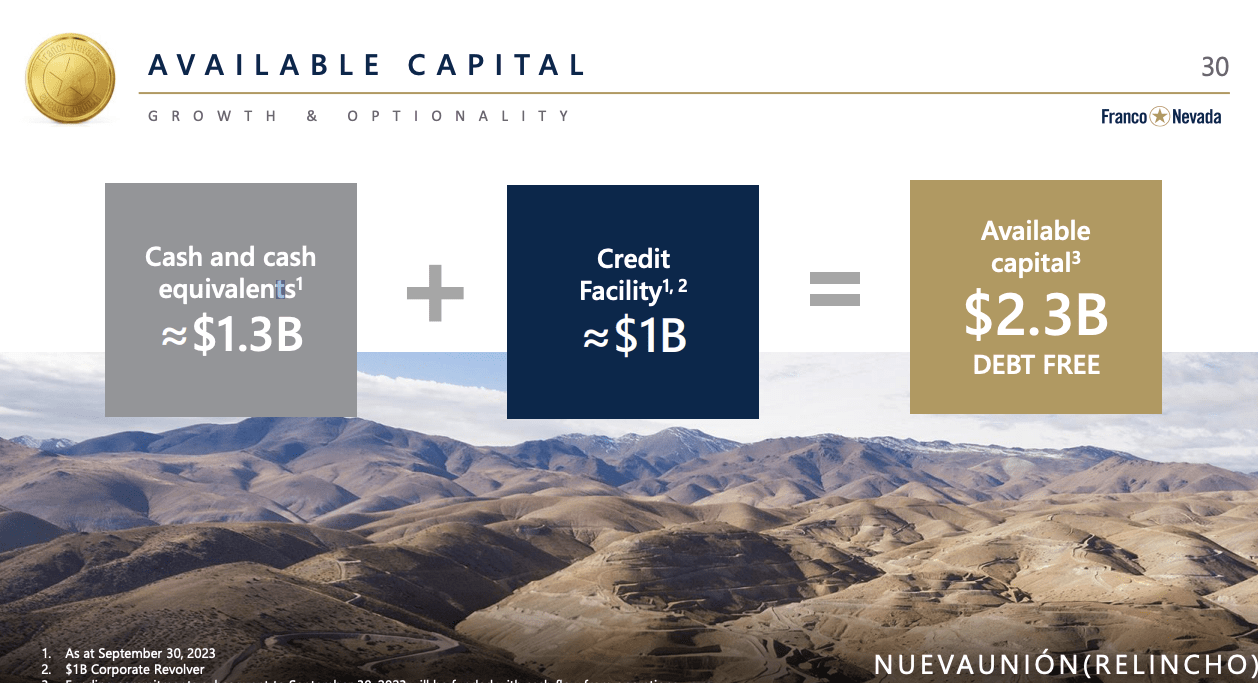

Franco-Nevada showcases a financial position enviable in the precious metals industry. With $1.3 billion in cash and equivalents, coupled with an untapped $1 billion credit facility, the company has $2.3 billion in available capital, all while carrying no debt on its balance sheet.

This robust financial health is pivotal for several reasons. Primarily, it ensures that Franco-Nevada is well-prepared to navigate the challenges posed by the Cobre Panama situation without jeopardizing its finances. Despite the current earnings impact from the mine's operational halt, Franco-Nevada's debt-free status and substantial cash flow from its diverse asset portfolio provide a cushion against the financial strain.

Also, this financial strength enables Franco-Nevada to continue pursuing growth opportunities by acquiring new low-cost royalties and streams. Such strategic investments could mitigate the impact of Cobre Panama's downtime.

Franco Nevada

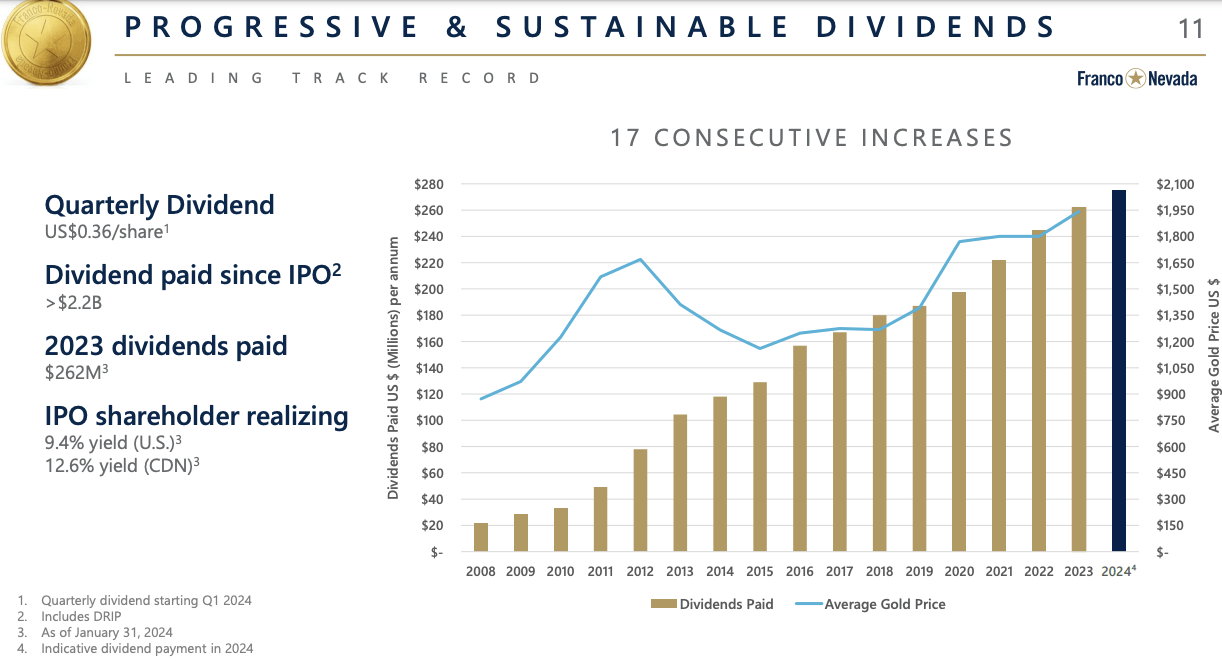

Additionally, Franco-Nevada's commitment to shareholder returns remains strong. The company not only offers a quarterly dividend of $.36, translating to a yield of 1.35% (as of writing on 2/27), but also boasts a remarkable track record of annual dividend increases for 17 consecutive years since its IPO.

The possibility of share buybacks, fueled by its substantial cash reserves, presents another avenue to create shareholder value.

The halt of operations at the Cobre Panama mine has impacted Franco-Nevada, leading to a significant drop in its stock price. This adjustment, however, brings Franco-Nevada's valuation to a more attractive level, suggesting a potential investment opportunity, especially if the mine issue resolves favorably.

Despite the current challenges, Franco-Nevada's core strengths remain. The company has a strong cash flow, a robust balance sheet with $1.3 billion in cash, and no debt, allowing it to navigate the Cobre Panama situation and invest in new opportunities. Its dividend track record is solid, adding to its appeal.

Now trading at the lowest valuation since the 2020 downturn, Franco-Nevada shares presents a buying opportunity. Considering the company's financial strength and the possible positive outcome at Cobre Panama, I've upgraded Franco-Nevada.