JHVEPhoto

JHVEPhoto

Dear readers/followers,

Reinsurance Group of America (NYSE:RGA) is one of the companies that I covered during the COVID-19 pandemic. It was in fact one of my "COVID discounts", in the last in a series of articles I published at the time, many of which have gone on to do really quite well.

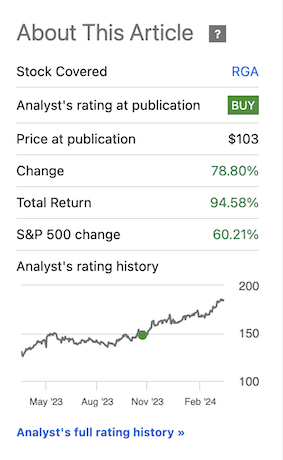

In this case, RGA has performed and generated over 100% RoR inclusive of dividends, FX, and capital appreciation. Since my first article on the company, the official RoR here on Seeking Alpha looks like this.

Seeking Alpha RGA RoR (Seeking Alpha RGA RoR)

You can find the specific article here. So, I would characterize it as fair to say that this has been a very successful investment, beating the market at a safety of A for the company, and with a non-trivial upside here.

However, with such an upside and track record comes the inevitable question if this is good enough to actually "keep around" at over $180/share because this is above the PT that I gave in my previous article. So in this article, I will be updating my targets, explaining to you why I am rotating parts of my position, and why it could be wise to rotate more - and why in fact the company still has a 15% annualized upside for the next few years, which could mean further market-beating returns for those willing to take that investment approach.

Let's get going here.

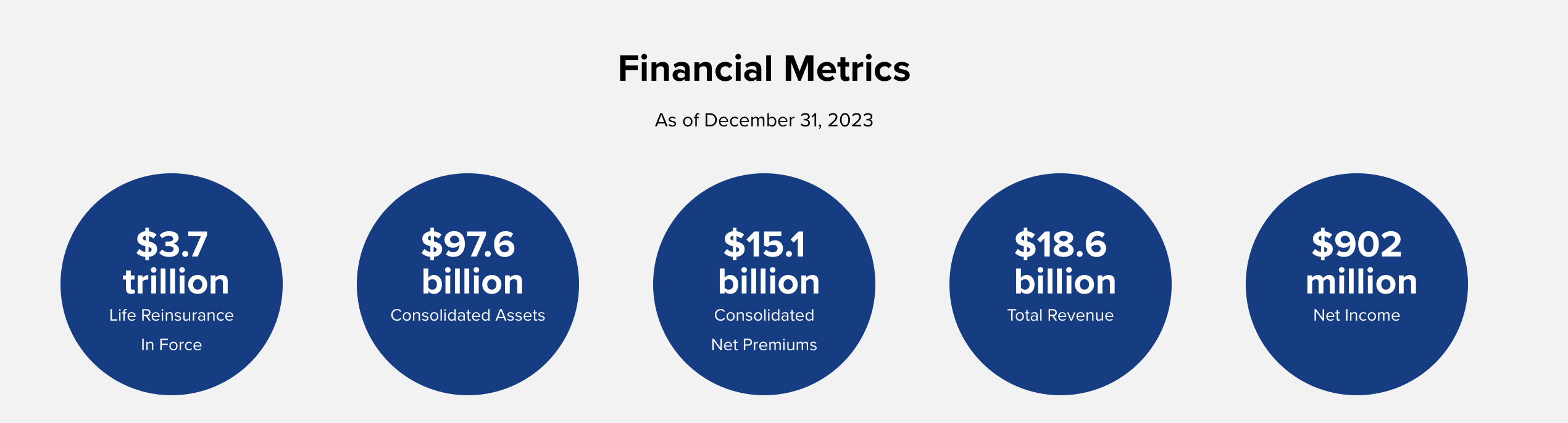

RGA is an above-average insurance company. It's a Fortune 500 business with over $3T of in-force reinsurance and company-level assets in the dozens of billions. It's not the largest life insurance business in the world - that honor goes to some of the company's European counterparts, which are larger and much, much older than RGA, but it's nonetheless a very solid business with a very good overall upside.

40 years of age with roots in Missouri coupled with reinsurance operations, which are generally thought of to be fairly conservative, are good things to invest in.

RGA IR (RGA IR)

The business of reinsurance is a way for insurers to transfer downside risk in their portfolio to a third party, thereby reducing the likelihood of a massive payout obligation from a large insurance. This allows insurers to remain solvent, as they're able through reinsurance to recover some or all of the amounts paid to claimants. That is not only what RGA does, but what virtually all reinsurers do for their ceding companies (the customers), which in turn are not only able to offload risk but also increase their own underwriting ability.

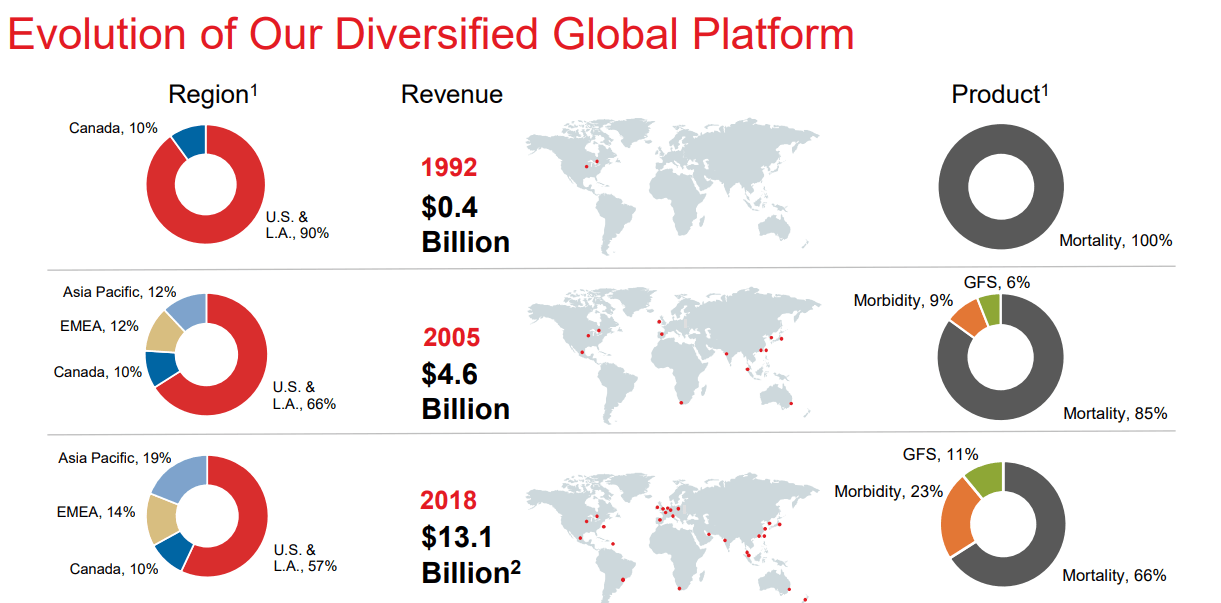

RGA in turn claims a very solid knowledge of mortality, morbidity risks, underwriting knowledge on the life/health side, and other things that make the company a leader in certain fields and geographies. Unlike the European counterparts, RGA, as the name would suggest, primarily works in NA/LATAM.

The company presented 4Q results, or FY results about 1.5 months ago. The results here were strong, with good operational performance and a TTM RoE of 14.4% on an adjusted basis. New business momentum was, like with other reinsurers, at a good volume, and the company keeps being able to deploy further capital into in-force transactions, with almost $350M in fresh capital being invested. (Source: RGA 4Q23 IR)

Shareholder returns have also been strong, with $50M in repurchases and over $50M in dividends.

RGA ended 4Q with excess capital of $1B, which enables it to work and act on a potentially very attractive transaction pipeline. It also launched Ruby Re, which will act as a Missouri-based third-party reinsurance business.

Overall, the new money rate for this company is now at 6.65%, and the company has no impairments or issues at this stage worth noting.(Source: RGA 4Q23 IR)

It's not strange, therefore, that the company's performance has been as stellar/positive as we've been seeing, both now and in the past.

RGA IR (RGA IR)

The company might not be as high-rated as some of its reinsurance peers. Munich Re (OTCPK:MURGY) especially comes to mind here, but it's still very good overall. A rating of A in this sector of finance/insurance is not something that many companies manage, and it's worth noting.

If you recall, this is a market on a global scale that more or less has only five larger players. It's RGA behind the Swiss business Swiss Re (OTCPK:SSREF) which is the largest at a revenue of $14,555M. From then, they include Munich Re, SCOR Global Life RE (no Symbol) and Hannover Ruck SE (OTCPK:HVRRF). These companies by themselves have essentially around 80% of the global market here - and it's a market that I would characterize as almost impossible due to capital requirements and other factors, to gain easy entry into, because all of the existing players can do what you do better, cheaper, faster and with better service.

The only disadvantage to RGA is that the company's yield is now less than 2%. My own YoC due to my extremely low buy-in price is more than 3.3% - so I'm happy with that.(Source: RGA 4Q23 IR)

But at the same time, I do see signs that RGA's business is likely to see some short/medium-term slowdown, at least in earnings, at least this coming year. Even with the company's expertise, current estimates are for a flat development for 2024E. This is despite major deals being struck, such as the recent deal between Prudential (PRU), RGA and Verizon (VZ), where the two insurance businesses are now holding nearly $6B worth of pension promises for the telecommunications giant.

Beyond this year though, the company's forecasts are for a favorable long-term outlook, enabling earnings growth of between 8-10% per year - though I would mention here that the company does have a history of at times overstating its expectations for results.

Premiums growth and non-spread investment results are solid though, and the company's investment portfolio now works at a portfolio yield of 4.86%, out of which over 69% are investment-grade bonds, and he fixed maturities securities are 64%+ at AAA, AA, and A-rating. In short, the company very much deserves its conservative credit ratios.

At any cheap valuation, this company is worth a positive rating with an upside. But we're now 3 years after the fact, and the company has moved up nearly 95% since I wrote about it the first time.

This justifies a look at the valuation and an estimate as to what we can expect here.

Reinsurance Group of America - the valuation

My last article on the company was published during the fall 2023 downturn. Since that time, that position has outperformed, but I believe the forward outperformance to not be as significant as the 3-year one we've seen.

Why?

Well, in my last article, I already made it clear that this company is less of a "BUY" at that time. I even went so far as to not call it "cheap" at the time and give it a price target of $155/share. If I were to call it a continued "BUY" here, I would have to bump that PT significantly. Is this justified?

Maybe.

The company has revised its upside, and now expects around 6%, on average, for the coming 3 years on an annualized basis. Using the company's very conservative long-term valuation trends, we find that at 11x P/E, the company still has the potential for 15% annualized market outperformance - which is the "baseline" of what I am sort of looking for with companies such as these.

RGA upside (FAST Graphs)

In the end though, the 1.8% yield at this time coupled with a forecast of around 6% growth compared to historical averages of around 8-10% means that I don't even think the company should trade at 11x, but closer to 10x. I'm raising my target to account for this, but I am not raising it to more than $175/share, which is the conservative 10-year forward P/E for this year based on a slight decline in adjusted earnings (currently forecasted). Also, remember that RGA negatively misses its targets about 25-30% of the time even with a conservative 10-20% Margin of error.

S&P Global analysts are far more positive than I am, having raised their average targets from around $140 to $195 in less than 1.5 years. With 9 out of 11 analysts at a "BUY" rating, this is a far call from what were once only 2 analysts at a "BUY" rating when the company traded at only $140/share, and when I considered it a "BUY".

I went ahead and actually rotated my stake in the company, at least partially, when the company went above $180/share. This brings to end a very long-term investment for me, at least in part, with a total return of over 100% inclusive of dividends, FX, and capital appreciation.

It's a nice "proof" that valuation, over time, if observed and acted upon, can generate some great alpha, even during an attractive market with the S&P up 60% in as short a time.

Going forward, I do not expect anything life-changing for the company in the next few years - growth in accordance with both company expectations, macro, and forecast. If you recall my last article, I forecasted EPS of around $18/share, the company beat this on an adjusted basis. For 2024E, I expect earnings somewhere along the $19.5 mark based on my current estimates, and not really expecting massive growth or improvements for the company this year, but potentially in the next 1-2 years after.

The main problem for RGA that I see is matching their own historical growth rates. The life/health insurance and reinsurance industries are likely to see macro pressure, which can translate into earnings growth pressure, which is what some analysts are forecasting (Source: F.A.S.T graphs/FactSet). My main worry here is for the sort of one-offs for individual US mortality and the like. The company already saw adverse claims during 4Q, and we've seen in the past what exactly volatility in the space can result in for RGA. It was this which enabled my initial investment into the company when it dropped 85% in terms of 2021E earnings. Now granted, this was from a pandemic, and the company is a life/health reinsurer. A repeat of this seems unlikely at this time, but the simple fact is that other companies in this space have a better exposure mix than RGA. Also, while I would buy this company any day a something like a 4-7x P/E, we're now at almost 10x P/E - so valuation remains something I look at very closely, especially when there's buoyancy in the sentiment that's lifting this company at this time.

I believe you can still "BUY" the company here, and I am not changing my official rating at this time, but this company is not cheap and does not offer, as I see it, more than 15% annualized at most, where I would say there could be better alternatives available.

The reason why I am rotating my stake, while still recommending/rating this a "BUY" is that I do want to realize some of the excellent profits that I've "gathered" here since the COVID-19 drop. But I still believe the company can present an upside - which is why I'm also not selling my entire position. It's an understandably mixed proposal that I am giving here, and one that might elicit a bit of confusion - but my logic here is that this company might not be "finished" rising here, even if the upside is no longer as appealing.

To be clear, I would change my rating to "HOLD" if the company moved up to above $188/share, which would abandon that 15% annualized upside on a conservative basis.

With that in mind, I give you the following forecast for RGA as it stands now.

Remember, I'm all about:

Here are my criteria and how the company fulfills them (italicized).

The company is a "BUY" here, albeit less than it was.