The Good Brigade/DigitalVision via Getty Images

The Good Brigade/DigitalVision via Getty Images

In this market, it can be difficult to find attractively priced firms. Yes, there are many cheap businesses out there. But many of those deserve to be cheap. There are some, however, that are trading on the cheap that probably deserve to trade a bit higher than where they are at the moment.

One firm that I think is a good candidate for that kind of list is Resideo Technologies, Inc. (NYSE:REZI), a producer and developer of products and solutions associated with things like energy management, water management, safety and security, and more, for homeowners. After a robust 2022 fiscal year from a sales perspective, 2023 showed some weakness. Bottom line results have been rather mixed over the past three years now and management is forecasting a likely decline in revenue this year. But even after factoring in these problems, shares look relatively attractively priced to the point that a "buy" rating probably makes sense.

To truly understand Resideo Technologies, it would be best to separate the company into its two segments. The first of these is the Products and Solutions business. Through this, the firm produces products and solutions for energy management, safety and security, and more. Specific examples include temperature and humidity control devices, thermal and combustion solutions, water and indoor air quality products, smoke and carbon monoxide detectors, sensors, video cameras, maintenance tools, and more. It even produces things like fire suppression products, security panels, and it provides certain cloud infrastructure offerings.

At its core, you could argue that Resideo Technologies is at the center of the "connected home" or "smart home" trend that was popular in the media several years ago. Its technologies are currently connected to roughly 11.6 million homes in the markets in which it operates. The company can use the data that it collects from this massive network to provide customers additional insights into their own homes and to even alert the end user about important matters. This is a very exciting trend in my mind, and it could provide additional growth for the firm for years to come.

All things considered, the Products and Solutions segment of Resideo Technologies is responsible for 42.8% of the company's overall revenue. Even larger than this, however, is the ADI Global Distribution segment. Through this unit, the company operates as a wholesale distributor of security products like security, fire, access control, and video products. It distributes over 450,000 different products from more than 1,000 manufacturers that it partners with across 13 different countries. The primary customers here largely consist of professionals who focus on the installation or management of said products. This is an even larger segment, accounting for the remaining 57.2% of the firm's overall revenue.

Author - SEC EDGAR Data

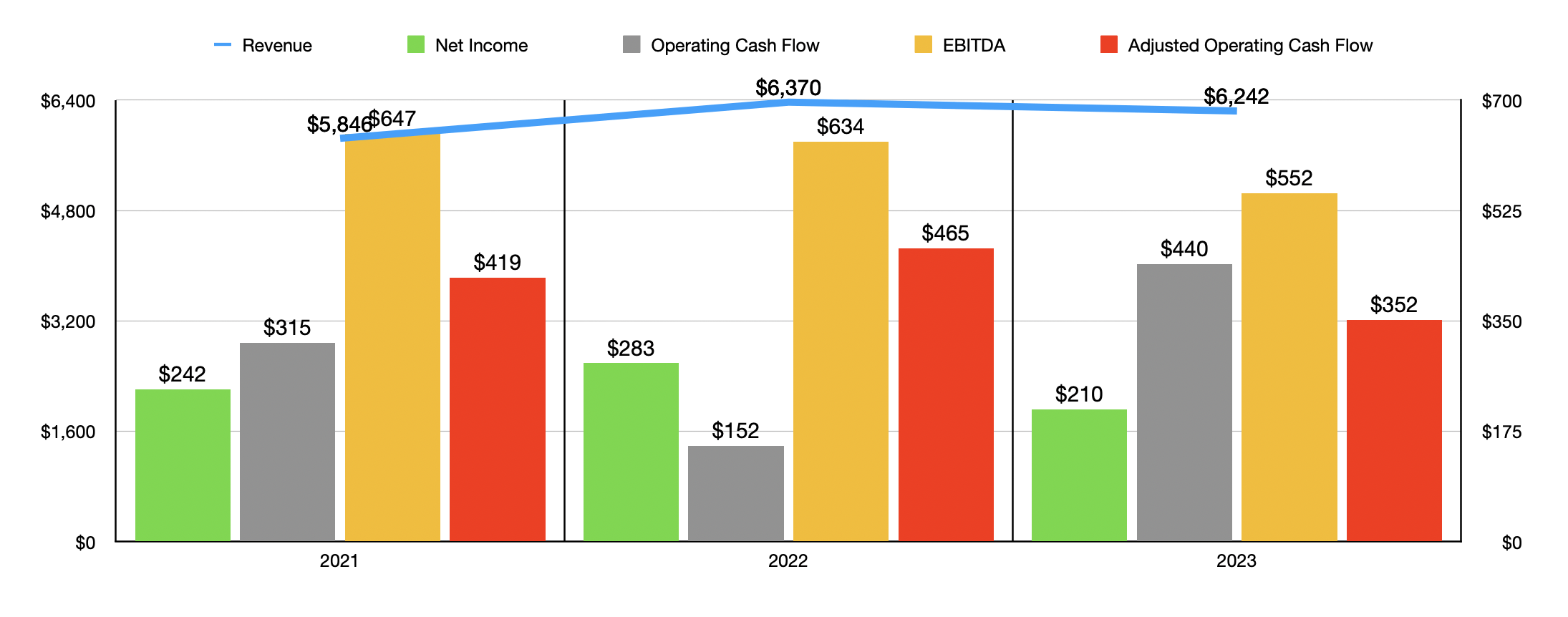

Over the past three years, Resideo Technologies has been on something of a bumpy ride. Revenue jumped nicely from $5.85 billion in 2021 to $6.37 billion in 2022. To be very clear, most of the $524 million increase in sales that the company achieved during this time, about $427 million in all, was thanks to acquisitions. Higher selling prices added another $368 million to the firm's top line.

However, a reduction in product volume in response to these elevated prices hit revenue to the tune of $110 million, while foreign currency fluctuations hit it by another $161 million. Then, from 2022 to 2023, revenue pulled back slightly to $6.24 billion. Lower volume hit sales to the tune of $414 million, while foreign currency fluctuations hit it by another $10 million. It was only thanks to a $153 million benefit associated with acquisitions and a $143 million benefit coming from higher selling prices, that the company was able to avoid seeing an even larger drop in revenue.

On the bottom line, the picture has been somewhat volatile during this window of time. After seeing that profits climbed to $242 million in 2021 to $283 million in 2022, the firm then saw a decline in profits to $210 million last year. Much of the decline from 2022 to 2023 came from lower gross profit, which management attributed largely to decreased sales volume and a price and product mix that negatively affected the bottom line. Other profitability metrics have also been quite volatile. The good news is that operating cash flow peaked at $440 million last year. But the bad news is that, if you adjust for changes in working capital, you get a decline from $465 million in 2022 to $352 million last year. And lastly, EBITDA for the company has been on the decline for at least the past three years now.

To address some of these problems, management has been working on reinvigorating the business. The firm incurred $42 million in restructuring charges last year. Management also succeeded in selling off certain assets such as its Genesis Cable operation for $86 million, though that will cost the business $105 million in annual revenue. The company even went so far as to outsource its work from the San Diego castings facility that it owns. And this year, management is pushing to make other changes that could include the divestiture of certain assets. However, none of this is going to change the fact that we are facing some questionable economic conditions.

For instance, management expects the repair and remodeling industry to either be flat or to see revenues drop at a low single digit rate this year relative to last year. There will be some normalization of inventory in the supply channel when it comes to HVAC offerings. This is expected to normalize in the first half of this year. But it could mean a quarter or two of additional pain.

Perhaps the best news for shareholders is that management anticipates residential new construction to be up at the low single digit to mid-single digit rate. I've actually written about this market before, and I am of the opinion that the worst for the residential construction market is over.

Resideo Technologies

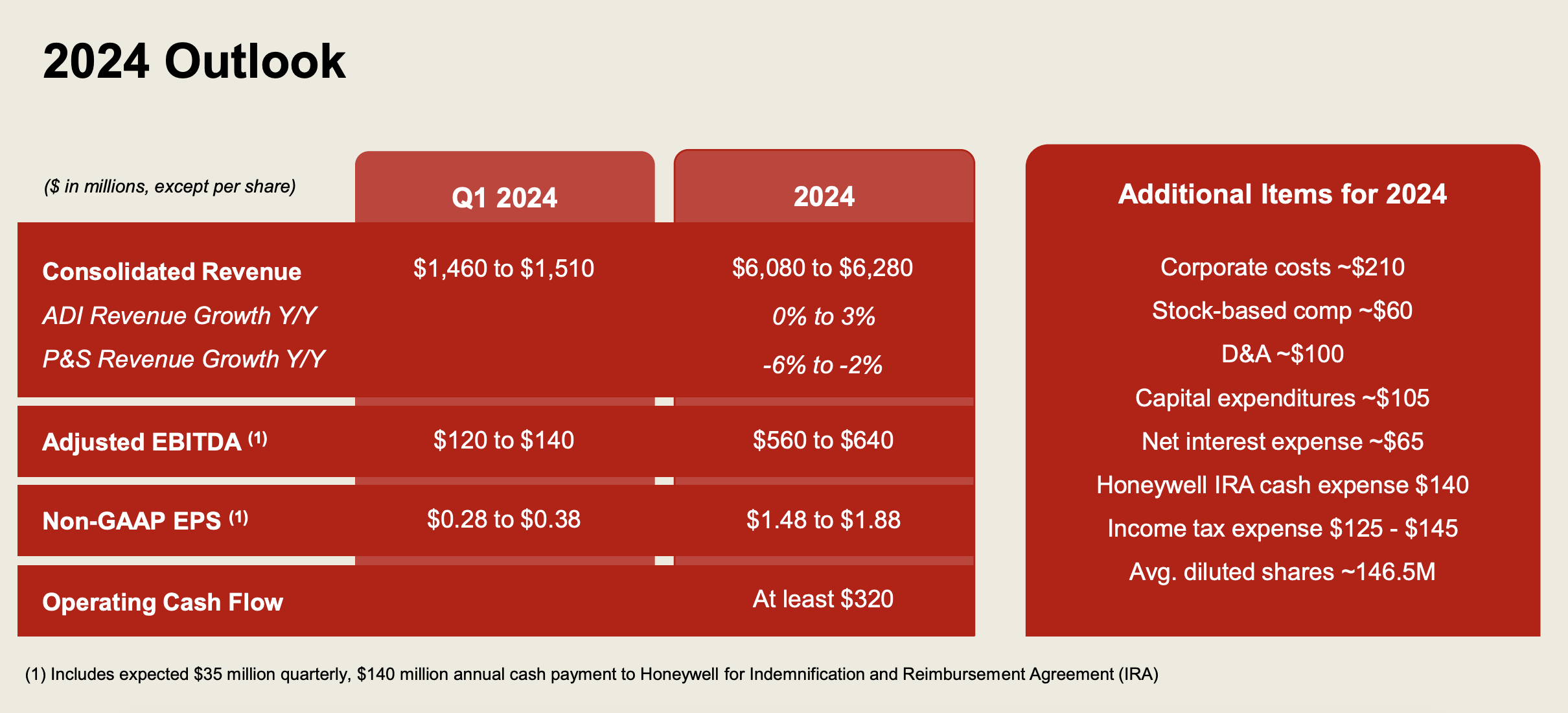

All combined, management believes that revenue this year will be between $6.08 billion and $6.28 billion. They are forecasting earnings per share of between $1.48 and $1.88. At the mid-point, that would translate to net profits of $244.1 million. Management did say that operating cash flow will be some unspecified number above $320 million. According to my own estimates, a reading of about $400 million should be anticipated. And lastly, EBITDA should be between $560 million and $640 million. That's $600 million at the midpoint.

What's really great about this is that all three of these profitability metrics look to be higher this year than they were last year despite what will likely be a decline in revenue. So, it's clear that management's cost cutting initiatives are working or are expected to work.

Author - SEC EDGAR Data

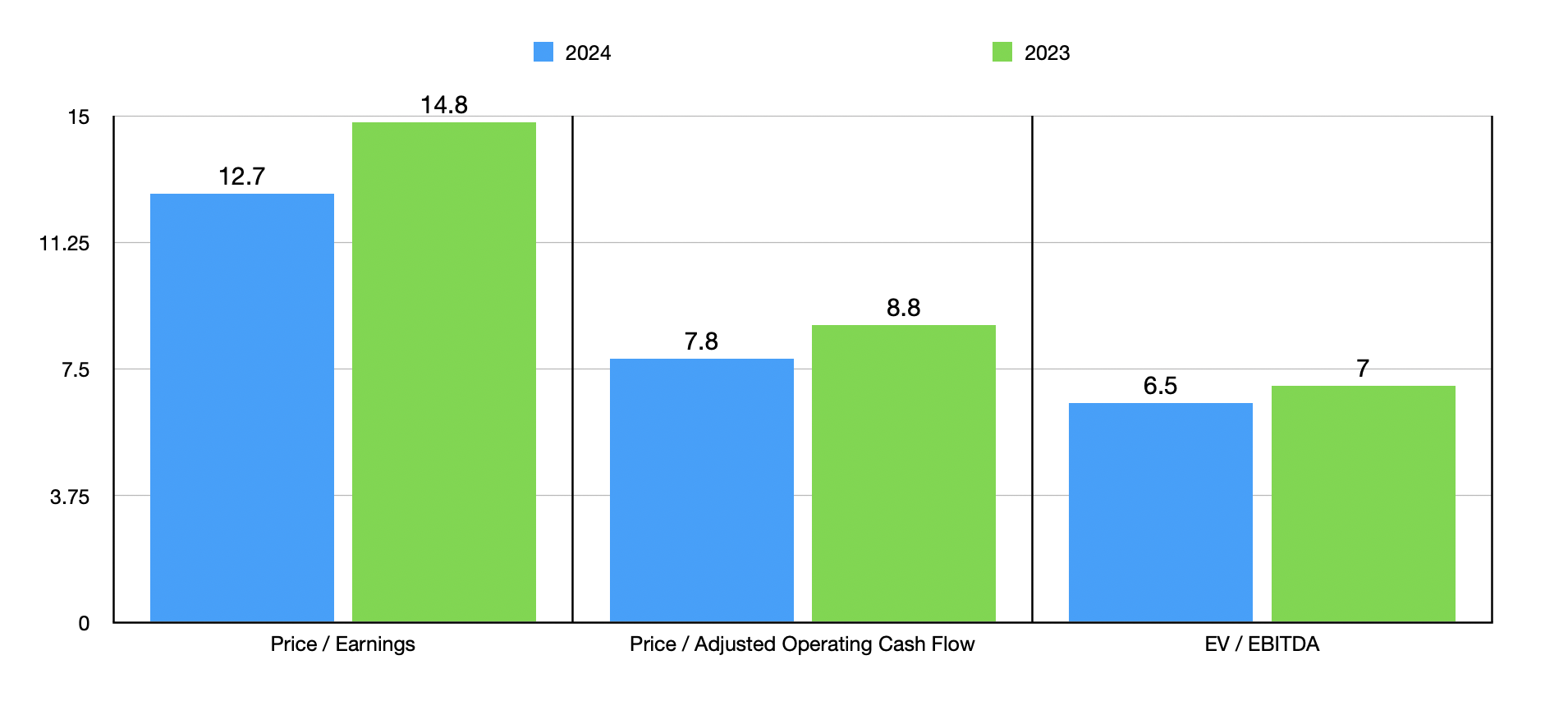

Using the aforementioned metrics, I was able to value the company on a forward basis and value it using 2023 figures. Both results can be seen in the chart above. On an absolute basis, shares are attractively priced. However, we should also pay attention to what other similar firms are trading at. In the table below, I compared Resideo Technologies to five similar enterprises. When it comes to the price to earnings approach and the EV to EBITDA approach, our candidate ended up being the cheapest of the group. And when it involves the price to operating cash flow approach, two of the five firms ended up being cheaper than our target.

| Company | Price/Earnings | Price/Operating Cash Flow | EV/EBITDA |

| Resideo Technologies | 14.8 | 8.8 | 7.0 |

| Griffon Corporation (GFF) | 50.6 | 7.2 | 17.6 |

| CSW Industrials (CSWI) | 37.5 | 20.3 | 20.2 |

| Masonite International (DOOR) | 18.3 | 7.0 | 9.5 |

| Hayward Holdings (HAYW) | 45.0 | 15.3 | 17.2 |

| Gibraltar Industries (ROCK) | 27.7 | 9.7 | 15.6 |

From all that I can tell at the moment, Resideo Technologies is experiencing some volatility. But that's to be expected in this environment. What's important is that management is making changes and that fundamental performance on the bottom line has not materially deteriorated.

Resideo Technologies, Inc. stock is trading at attractive levels, both on an absolute basis and relative to similar firms. So taking all of this together, I have no problem rating the business a "buy."